COVID-19 Dashboard of Economic Indicators

101

COVID-19 Dashboard of Economic Indicators 28 October 2020

Transcript of COVID-19 Dashboard of Economic Indicators

COVID-19 Dashboardof Economic Indicators

28 October 2020

2

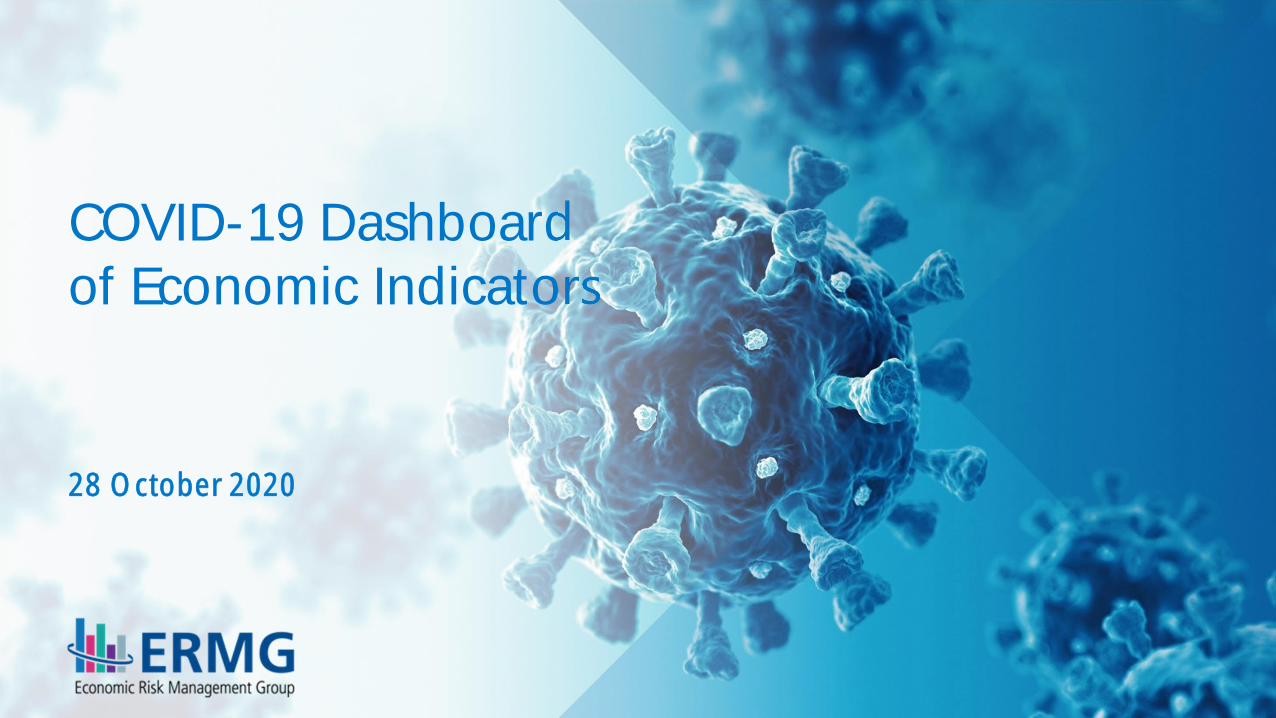

COVID-19 in België

Evolutie van het aantal opnames in het ziekenhuis629

689

252

60125554

0

1000

2000

3000

4000

5000

6000

7000

0

100

200

300

400

500

600

70015

/03/

2020

20/0

3/20

2025

/03/

2020

30/0

3/20

2004

/04/

2020

09/0

4/20

2014

/04/

2020

19/0

4/20

2024

/04/

2020

29/0

4/20

2004

/05/

2020

09/0

5/20

2014

/05/

2020

19/0

5/20

2024

/05/

2020

29/0

5/20

2003

/06/

2020

08/0

6/20

2013

/06/

2020

18/0

6/20

2023

/06/

2020

28/0

6/20

2003

/07/

2020

08/0

7/20

2013

/07/

2020

18/0

7/20

2023

/07/

2020

28/0

7/20

2002

/08/

2020

07/0

8/20

2012

/08/

2020

17/0

8/20

2022

/08/

2020

27/0

8/20

2001

/09/

2020

06/0

9/20

2011

/09/

2020

16/0

9/20

2021

/09/

2020

26/0

9/20

2001

/10/

2020

06/1

0/20

2011

/10/

2020

16/1

0/20

2021

/10/

2020

26/1

0/20

20

Aantal nieuwe opnames (linkeras) Totaal aantal patiënten in het ziekenhuis (rechteras)

3Bron: Sciensano, Belgisch Instituut voor de Volksgezondheid, 28 oktober 2020.https://epidemio.wiv-isp.be/ID/Documents/Covid19/Meest%20recente%20update.pdf

1. COVID-19 in België: aantal gehospitaliseerde patiënten stijgtonrustwekkend en de situatie is stilaan dezelfde als eind maart

4

GDP and confidence indicatorsfor Belgium

70

75

80

85

90

95

100

105

110

Current statistics

70

75

80

85

90

95

100

105

11020

19Q

1

2019

Q2

2019

Q3

2019

Q4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

2021

Q1

2021

Q2

2021

Q3

2021

Q4

2022

Q1

2022

Q2

2022

Q3

2022

Q4

p.m. NBB Autumn projections NBB Spring projections FPB projections (June)

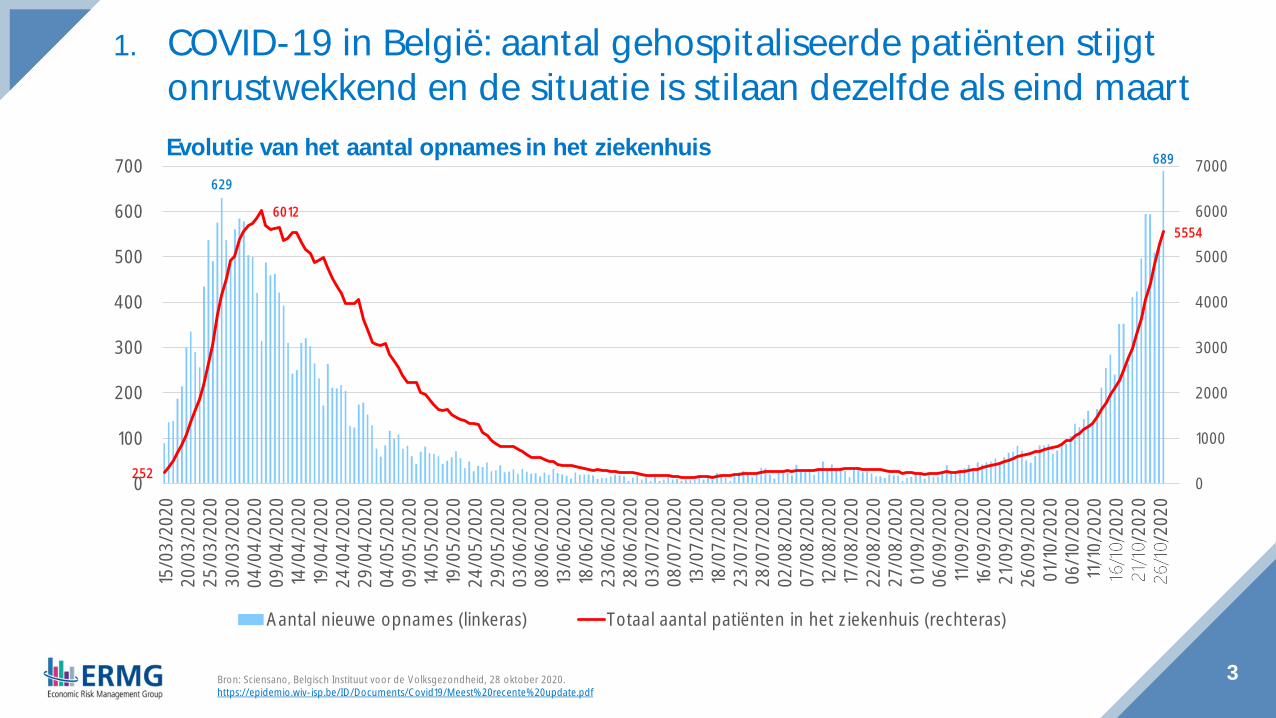

5Sources: Federal Planning Bureau (FPB), National Accounts Institute (NAI), National Bank of Belgium (NBB).

Real GDP in Belgium(quarterly data, index 2019Q4=100, unless otherwise stated)

The downturn in 2020 Q2 appears to have been less severe thanpredicted

2019Q1 0.10

2019Q2 0.29

2019Q3 0.41

2019Q4 0.48

2020Q1 -3.51

2020Q2 -12.07

Real GDP in Belgium(quarterly data, QoQ growth rate in %)

6

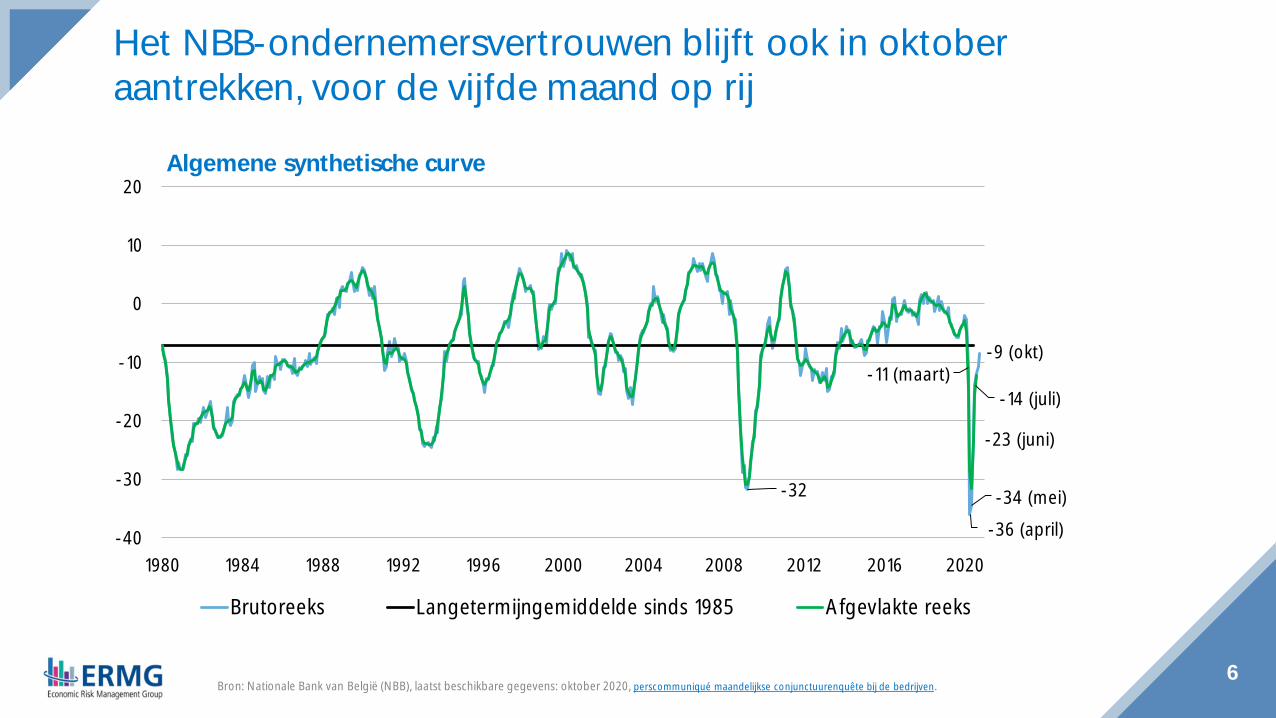

Het NBB-ondernemersvertrouwen blijft ook in oktoberaantrekken, voor de vijfde maand op rij

-32

-11 (maart)

-36 (april)-34 (mei)

-23 (juni)

-14 (juli)

-9 (okt)

-40

-30

-20

-10

0

10

20

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

Brutoreeks Langetermijngemiddelde sinds 1985 Afgevlakte reeks

Algemene synthetische curve

Bron: Nationale Bank van België (NBB), laatst beschikbare gegevens: oktober 2020, perscommuniqué maandelijkse conjunctuurenquête bij de bedrijven.

-70-60-50-40-30-20-10

01020

2015 2016 2017 2018 2019 2020

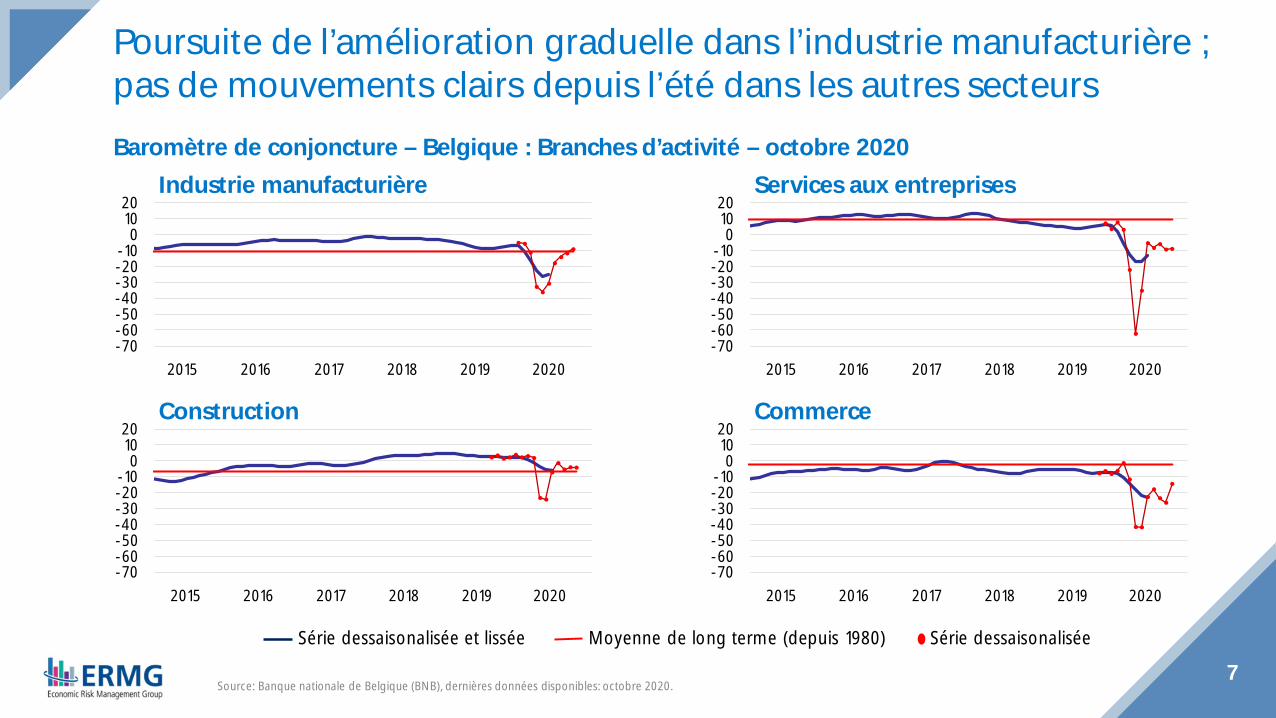

Baromètre de conjoncture – Belgique : Branches d’activité – octobre 2020

Poursuite de l’amélioration graduelle dans l’industrie manufacturière ;pas de mouvements clairs depuis l’été dans les autres secteurs

7

Industrie manufacturière

CommerceConstruction

Services aux entreprises

-70-60-50-40-30-20-10

01020

2015 2016 2017 2018 2019 2020

-70-60-50-40-30-20-10

01020

2015 2016 2017 2018 2019 2020

-70-60-50-40-30-20-10

01020

2015 2016 2017 2018 2019 2020

Moyenne de long terme (depuis 1980)Série dessaisonalisée et lissée Série dessaisonalisée

Source: Banque nationale de Belgique (BNB), dernières données disponibles: octobre 2020.

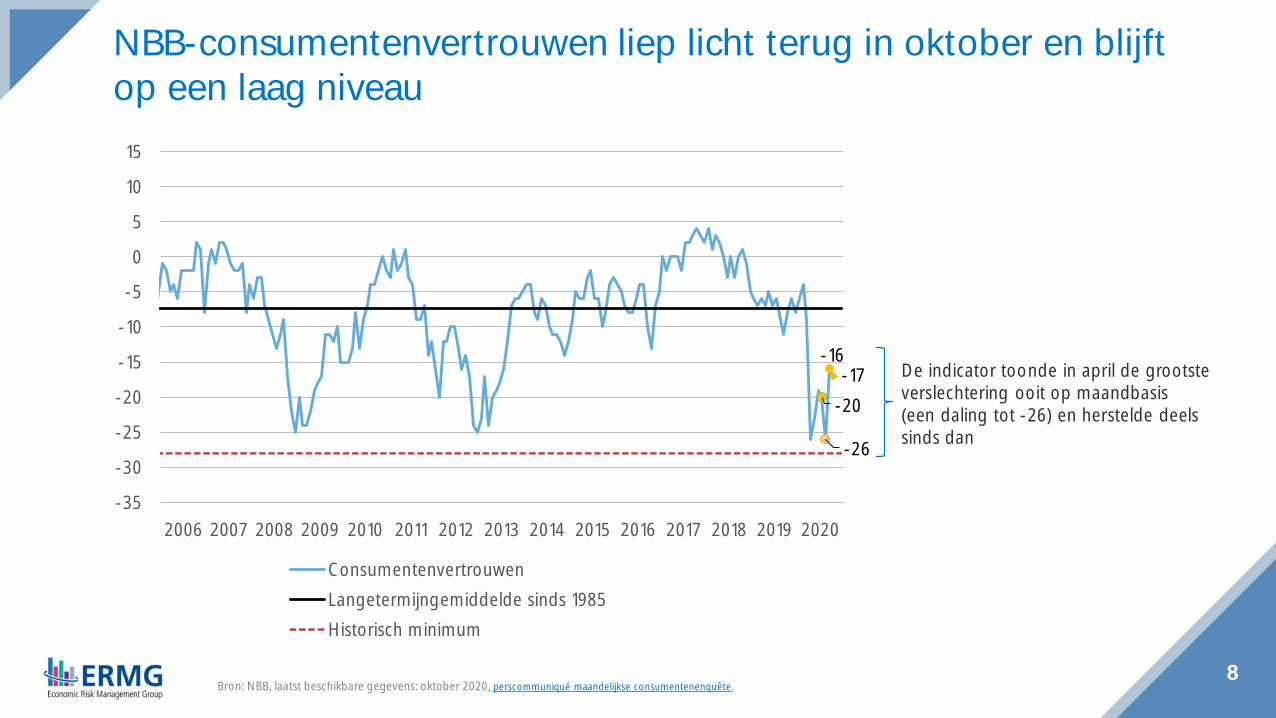

-20

-26

-16-17

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

ConsumentenvertrouwenLangetermijngemiddelde sinds 1985Historisch minimum

8

NBB-consumentenvertrouwen liep licht terug in oktober en blijftop een laag niveau

De indicator toonde in april de grootsteverslechtering ooit op maandbasis(een daling tot -26) en herstelde deelssinds dan

Bron: NBB, laatst beschikbare gegevens: oktober 2020, perscommuniqué maandelijkse consumentenenquête.

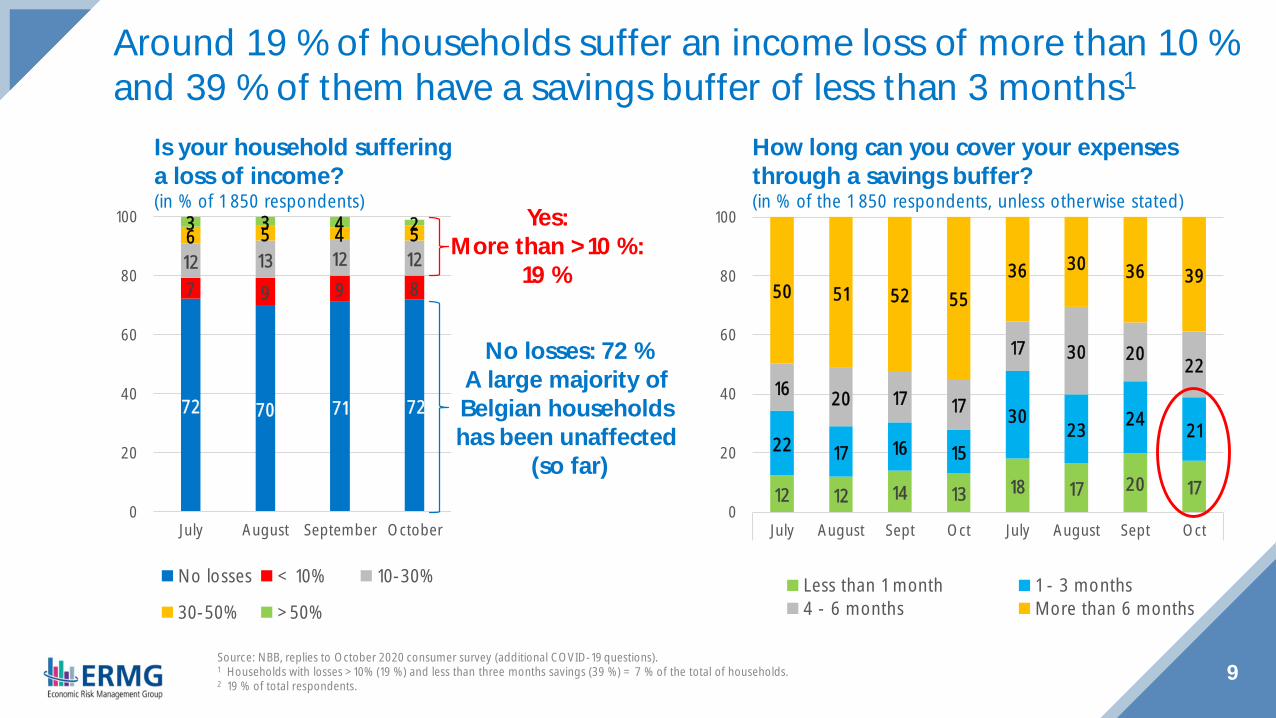

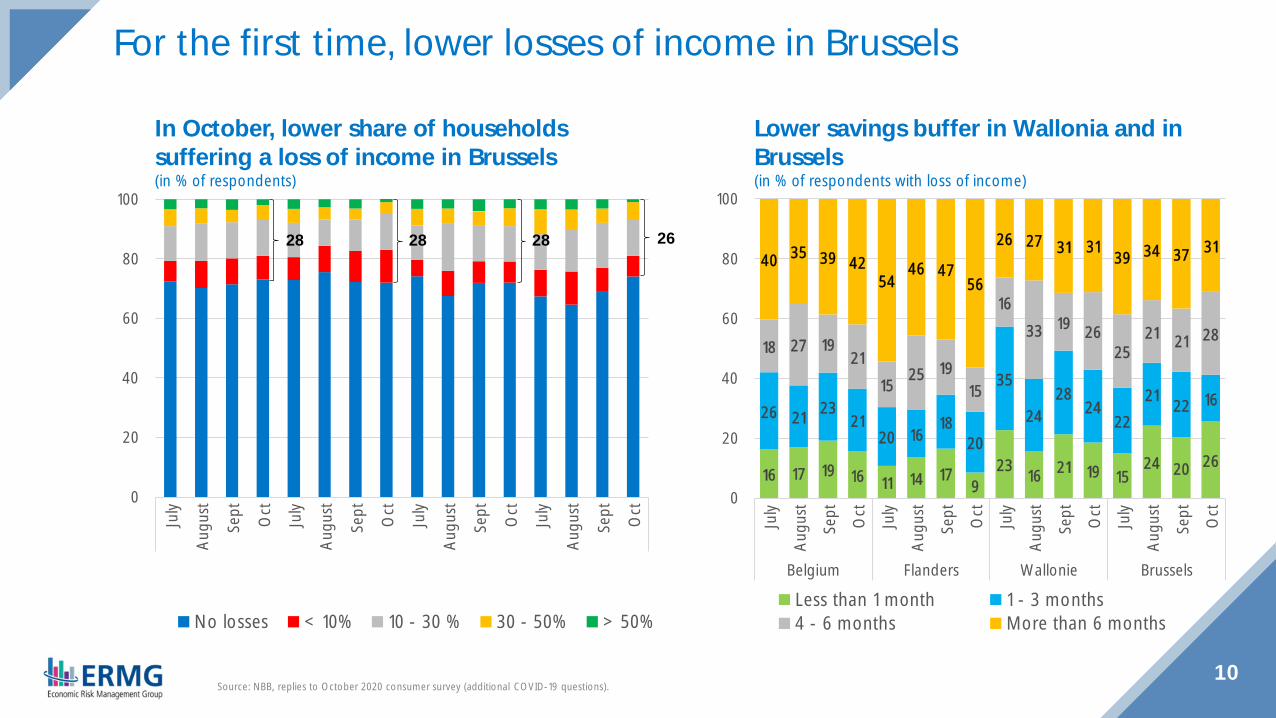

9Source: NBB, replies to October 2020 consumer survey (additional COVID-19 questions).1 Households with losses >10% (19 %) and less than three months savings (39 %) = 7 % of the total of households.2 19 % of total respondents.

How long can you cover your expensesthrough a savings buffer?(in % of the 1 850 respondents, unless otherwise stated)

Is your household sufferinga loss of income?(in % of 1 850 respondents)

Around 19 % of households suffer an income loss of more than 10 %and 39 % of them have a savings buffer of less than 3 months1

Yes:More than >10 %:

19 %

72 70 71 72

7 9 9 812 13 12 126 5 4 53 3 4 2

0

20

40

60

80

100

July August September October

No losses < 10% 10-30%

30-50% >50%

12 12 14 13 18 17 20 17

22 17 16 15

3023 24 21

16 20 17 17

17 30 20 22

50 51 52 5536 30 36 39

0

20

40

60

80

100

July August Sept Oct July August Sept Oct

Less than 1 month 1 - 3 months4 - 6 months More than 6 months

No losses: 72 %A large majority ofBelgian householdshas been unaffected

(so far)

0

20

40

60

80

100Ju

ly

Augu

st

Sept Oct

July

Augu

st

Sept Oct

July

Augu

st

Sept Oct

July

Augu

st

Sept Oct

No losses < 10% 10 - 30 % 30 - 50% > 50%

10Source: NBB, replies to October 2020 consumer survey (additional COVID-19 questions).

Lower savings buffer in Wallonia and inBrussels(in % of respondents with loss of income)

In October, lower share of householdssuffering a loss of income in Brussels(in % of respondents)

For the first time, lower losses of income in Brussels

26282828

16 17 19 16 11 14 179

23 16 21 19 1524 20 26

26 21 2321

20 1618

20

35

2428

2422

21 22 16

18 27 1921

1525 19

15

1633 19 26

2521 21 28

40 35 39 4254

46 4756

26 27 31 31 39 34 37 31

0

20

40

60

80

100

July

Augu

st

Sept Oct

July

Augu

st

Sept Oct

July

Augu

st

Sept Oct

July

Augu

st

Sept Oct

Belgium Flanders Wallonie Brussels

Less than 1 month 1 - 3 months4 - 6 months More than 6 months

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

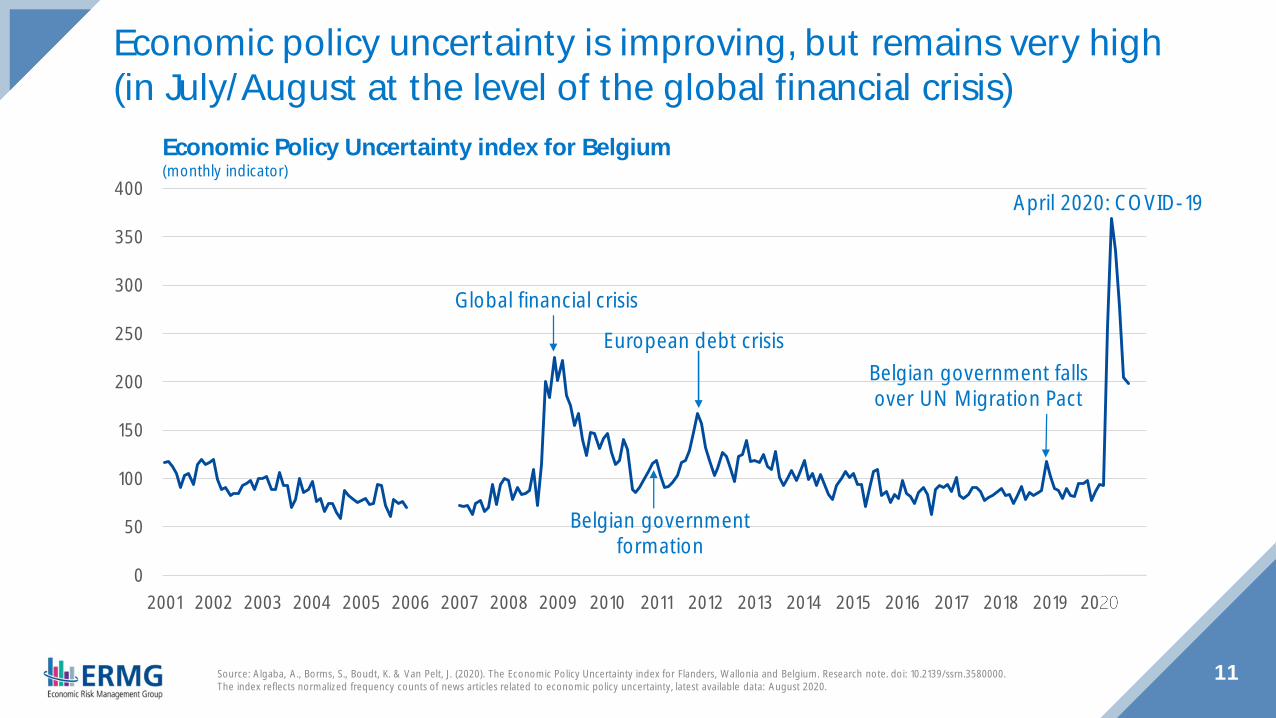

11Source: Algaba, A., Borms, S., Boudt, K. & Van Pelt, J. (2020). The Economic Policy Uncertainty index for Flanders, Wallonia and Belgium. Research note. doi: 10.2139/ssrn.3580000.The index reflects normalized frequency counts of news articles related to economic policy uncertainty, latest available data: August 2020.

Economic Policy Uncertainty index for Belgium(monthly indicator)

Economic policy uncertainty is improving, but remains very high(in July/August at the level of the global financial crisis)

Belgian governmentformation

April 2020: COVID-19

Belgian government fallsover UN Migration Pact

European debt crisis

Global financial crisis

12

Labour market

13Source: Institut des Comptes Nationaux (ICN), dernières données disponibles: deuxième trimestre 2020.

L’emploi salarié plus durement impacté au 1er semestre 2020 quel’emploi indépendant(emploi en personnes - variation trimestrielle en %)

0,50,4 0,4 0,4

-0,2

-0,7

-1,0

-0,8

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

0,8

2019-T1 2019-T2 2019-T3 2019-T4 2020-T1 2020-T2

Indépendants Salariés Emploi total

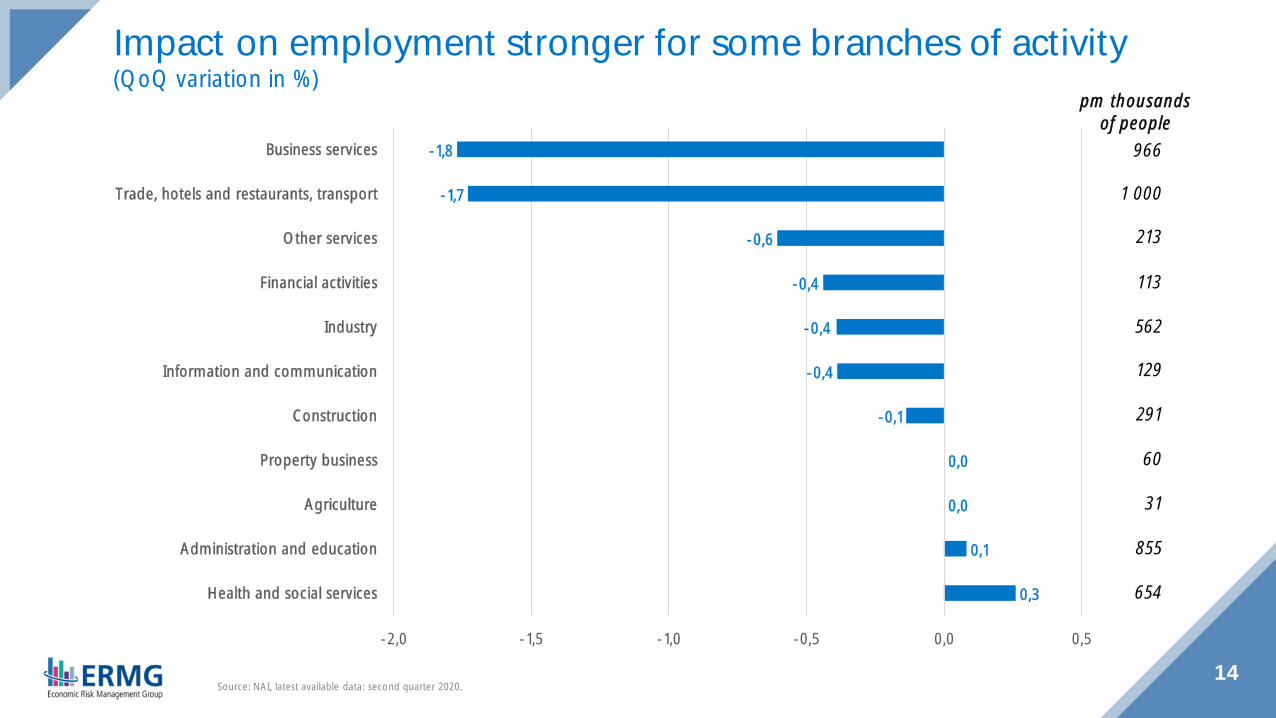

0,3

0,1

0,0

0,0

-0,1

-0,4

-0,4

-0,4

-0,6

-1,7

-1,8

-2,0 -1,5 -1,0 -0,5 0,0 0,5

Health and social services

Administration and education

Agriculture

Property business

Construction

Information and communication

Industry

Financial activities

Other services

Trade, hotels and restaurants, transport

Business services

Source: NAI, latest available data: second quarter 2020.14

Impact on employment stronger for some branches of activity(QoQ variation in %)

pm thousandsof people

966

1 000

213

113

562

129

291

60

31

855

654

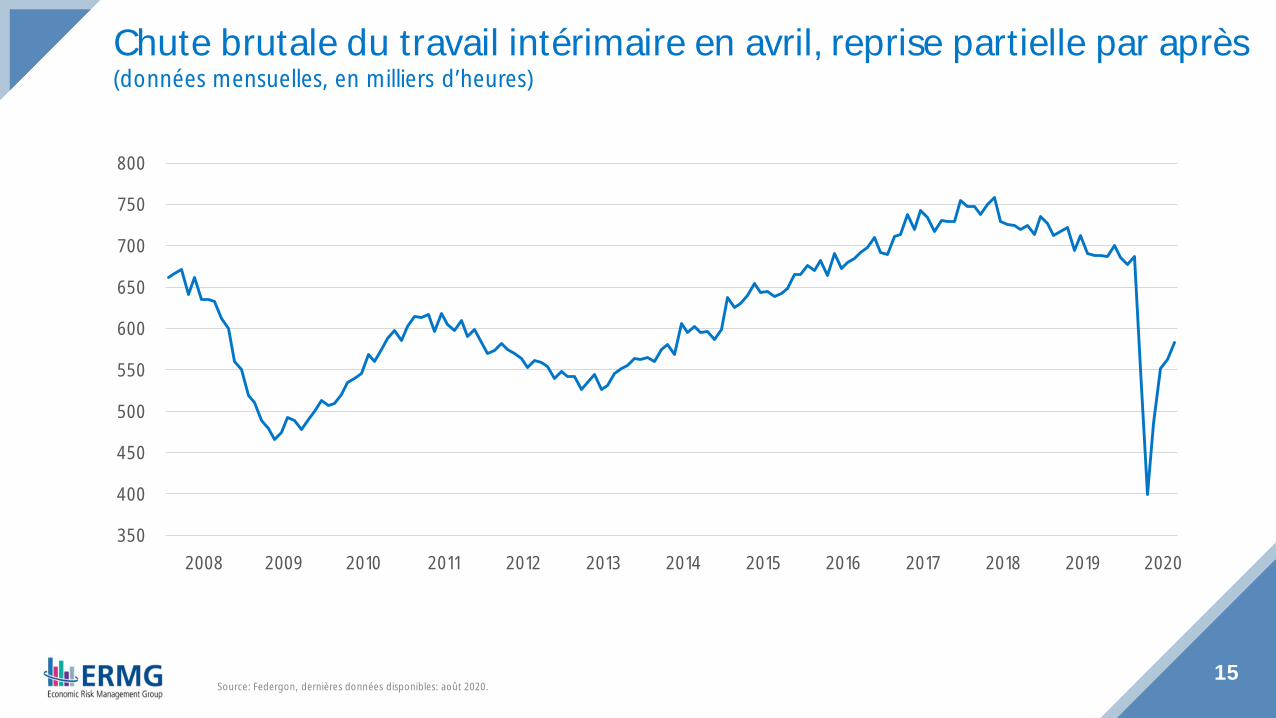

15Source: Federgon, dernières données disponibles: août 2020.

Chute brutale du travail intérimaire en avril, reprise partielle par après(données mensuelles, en milliers d’heures)

350

400

450

500

550

600

650

700

750

800

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

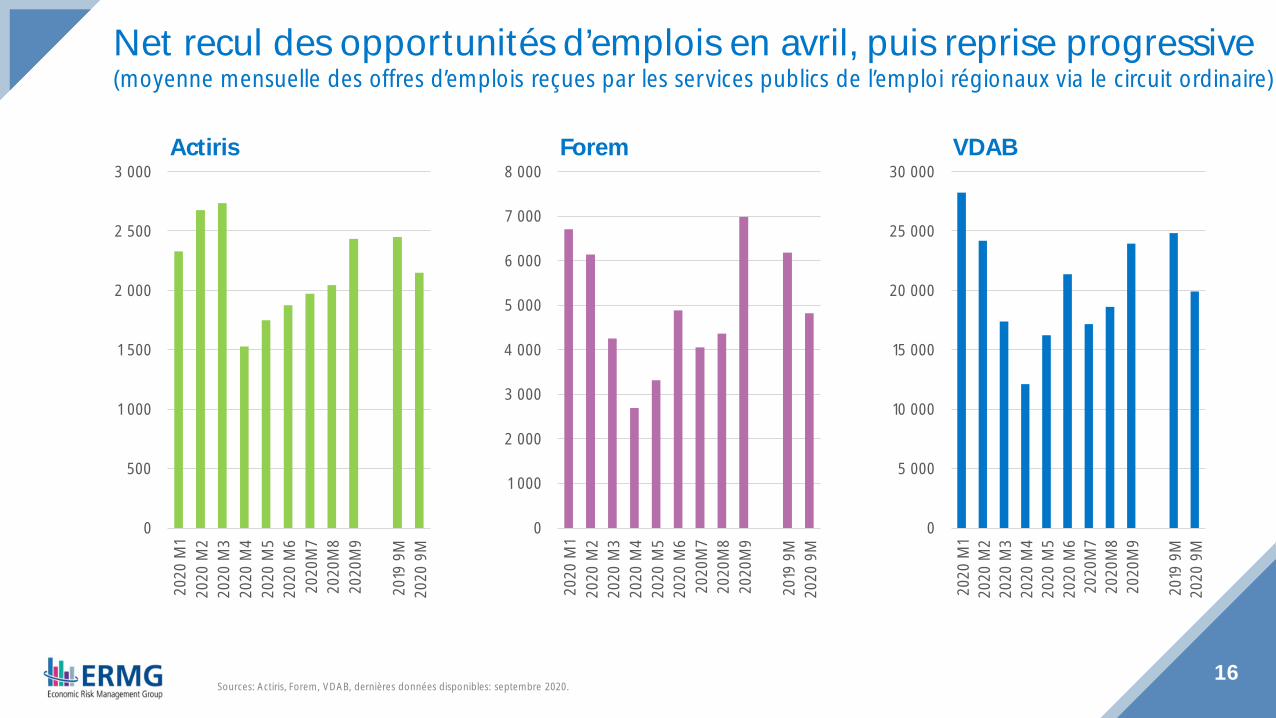

16Sources: Actiris, Forem, VDAB, dernières données disponibles: septembre 2020.

VDABActiris

Net recul des opportunités d’emplois en avril, puis reprise progressive(moyenne mensuelle des offres d’emplois reçues par les services publics de l’emploi régionaux via le circuit ordinaire)

Forem

0

500

1 000

1 500

2 000

2 500

3 00020

20 M

120

20 M

220

20 M

320

20 M

420

20 M

520

20 M

620

20M

720

20M

820

20M

9

2019

9M

2020

9M

0

5 000

10 000

15 000

20 000

25 000

30 000

2020

M1

2020

M2

2020

M3

2020

M4

2020

M5

2020

M6

2020

M7

2020

M8

2020

M9

2019

9M

2020

9M

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2020

M1

2020

M2

2020

M3

2020

M4

2020

M5

2020

M6

2020

M7

2020

M8

2020

M9

2019

9M

2020

9M

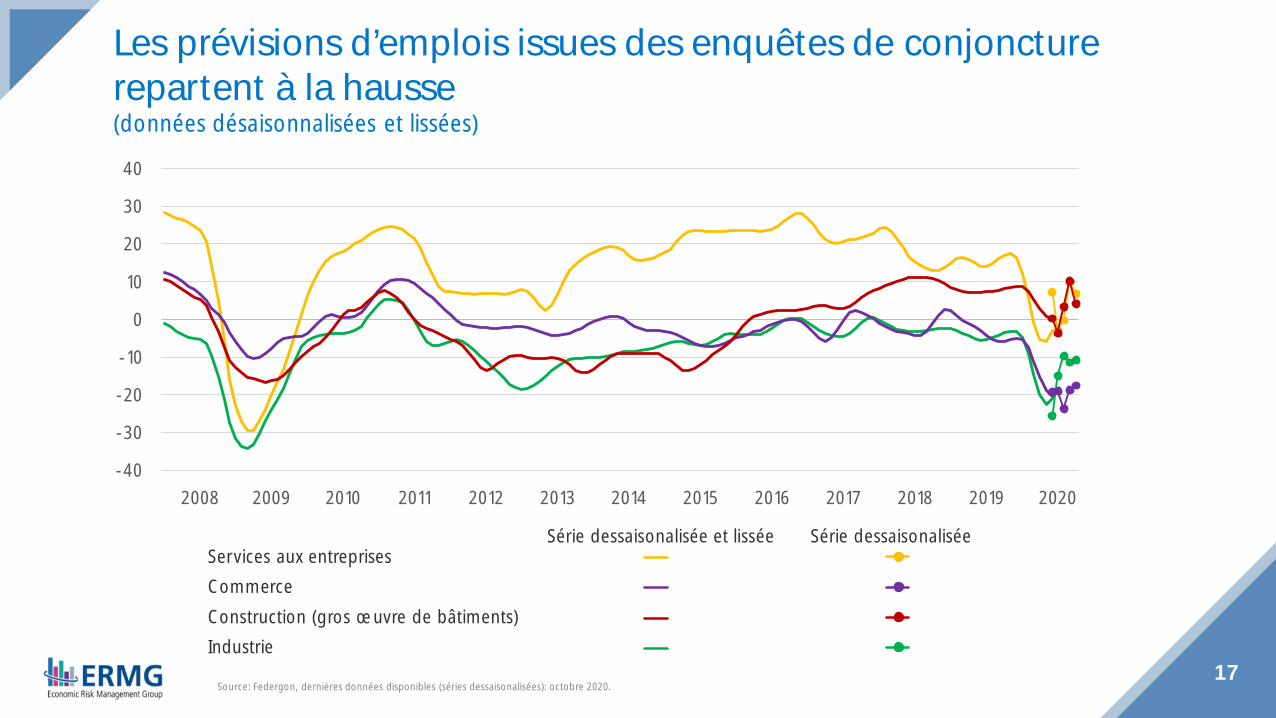

17Source: Federgon, dernières données disponibles (séries dessaisonalisées): octobre 2020.

Les prévisions d’emplois issues des enquêtes de conjoncturerepartent à la hausse(données désaisonnalisées et lissées)

-40

-30

-20

-10

0

10

20

30

40

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

IndustrieConstruction (gros œuvre de bâtiments)CommerceServices aux entreprises

Série dessaisonalisée et lissée Série dessaisonalisée

Mass redundancy procedures: already above 2019 average

◆ Since lockdown (April 2020)

◇ 74 procedures

◇ 6 688 workers concerned

◆ pm January 2019 – December 2019

◇ 81 procedures

◇ 5 087 workers concerned

18Source: Federal Public Service Employment, Labour and Social Dialogue (FPS ELSD), latest data available: 26 October 2020.

0

5

10

15

20

25

0

500

1 000

1 500

2 000

2 500

Janu

ary

Febr

uary

Mar

ch

April

May

June July

Augu

st

Sept

embe

r

Oct

ober

Workers (LHS) pm Average 2019 (LHS)

Cases (RHS) pm Average 2019 (RHS)

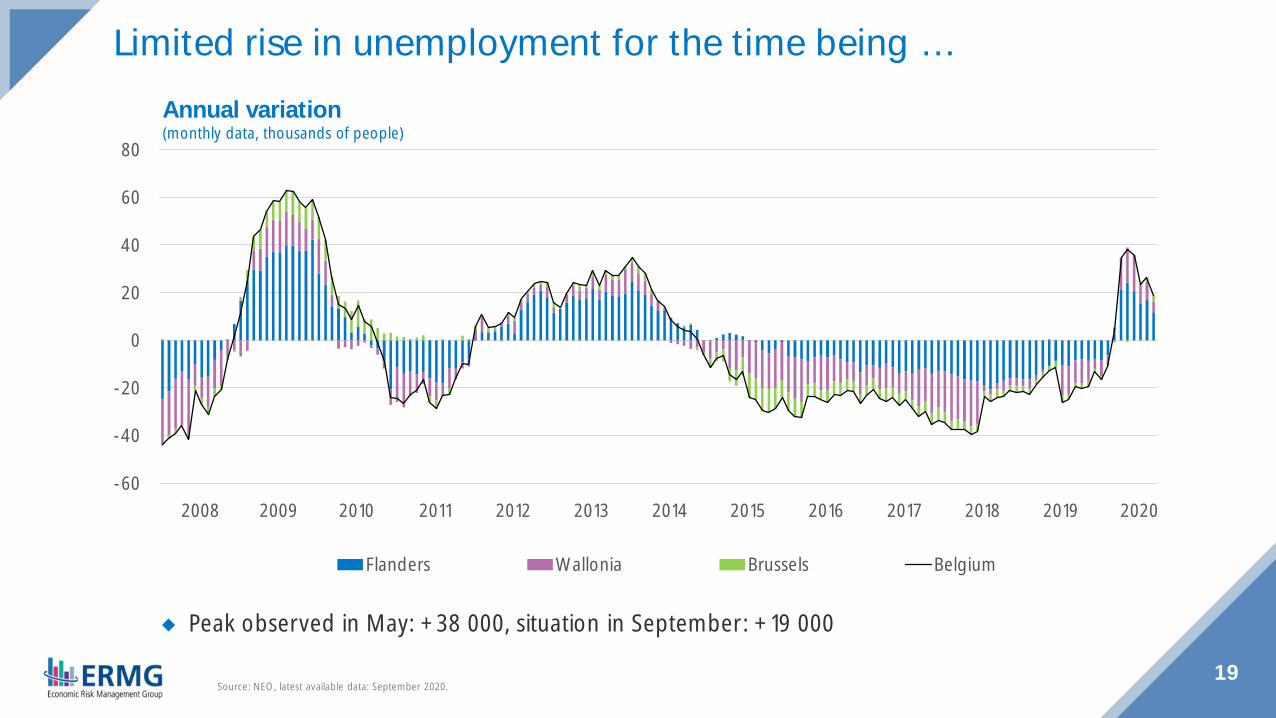

19Source: NEO, latest available data: September 2020.

Annual variation(monthly data, thousands of people)

Limited rise in unemployment for the time being …

-60

-40

-20

0

20

40

60

80

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Flanders Wallonia Brussels Belgium

◆ Peak observed in May: +38 000, situation in September: +19 000

20Source: NEO, latest available data: August 2020.

… concentrated on young educated peopleAnnual variation(monthly data)

-5

0

5

10

15

20

25M

en

Wom

en

Less

than

6 m

onth

s

6-12

mon

ths

1 yea

r and

mor

e

Youn

ger t

han

20

20-3

0 ye

ars

30-5

0 ye

ars

50 a

nd o

lder

Low-

educ

ated

Med

ium

-edu

cate

d

High

ly-ed

ucat

ed

In thousands of people In %

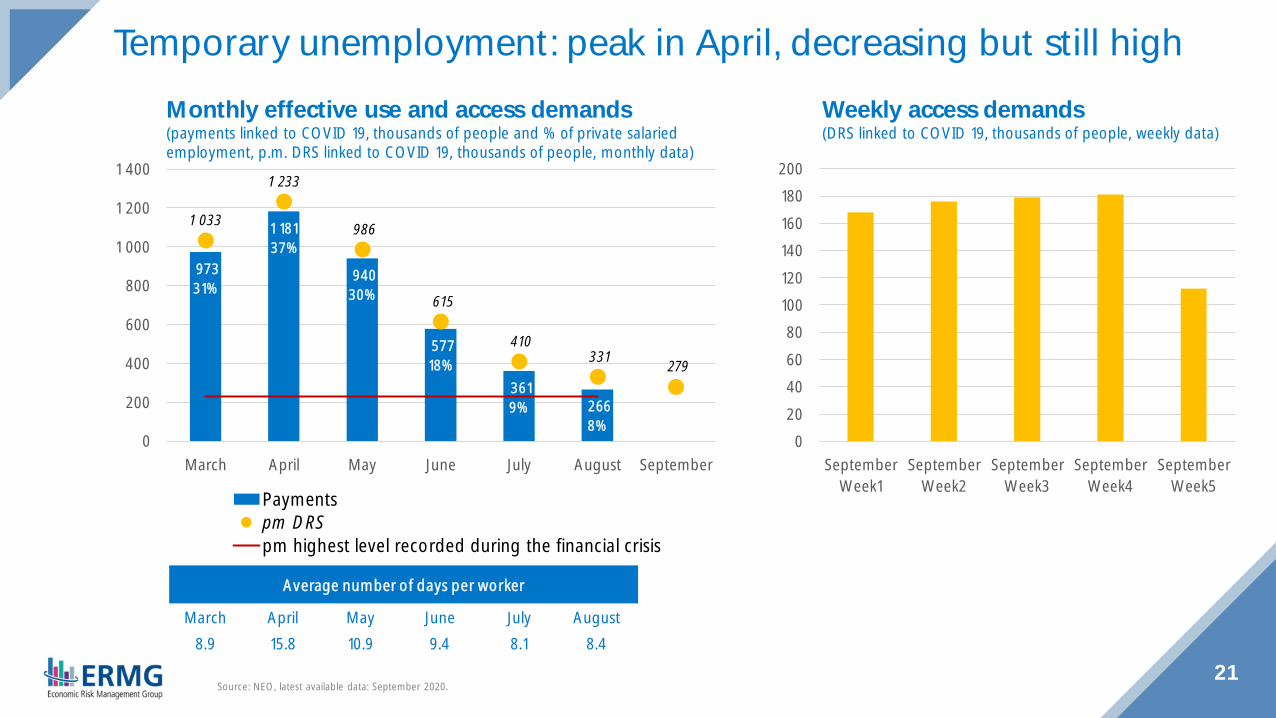

Monthly effective use and access demands(payments linked to COVID 19, thousands of people and % of private salariedemployment, p.m. DRS linked to COVID 19, thousands of people, monthly data)

21Source: NEO, latest available data: September 2020.

Temporary unemployment: peak in April, decreasing but still high

97331%

1 18137%

94030%

57718%

3619% 266

8%

1 033

1 233

986

615

410331 279

0

200

400

600

800

1 000

1 200

1 400

March April May June July August September

Paymentspm DRSpm highest level recorded during the financial crisis

Weekly access demands(DRS linked to COVID 19, thousands of people, weekly data)

Average number of days per worker

March April May June July August8.9 15.8 10.9 9.4 8.1 8.4

020406080

100120140160180200

SeptemberWeek1

SeptemberWeek2

SeptemberWeek3

SeptemberWeek4

SeptemberWeek5

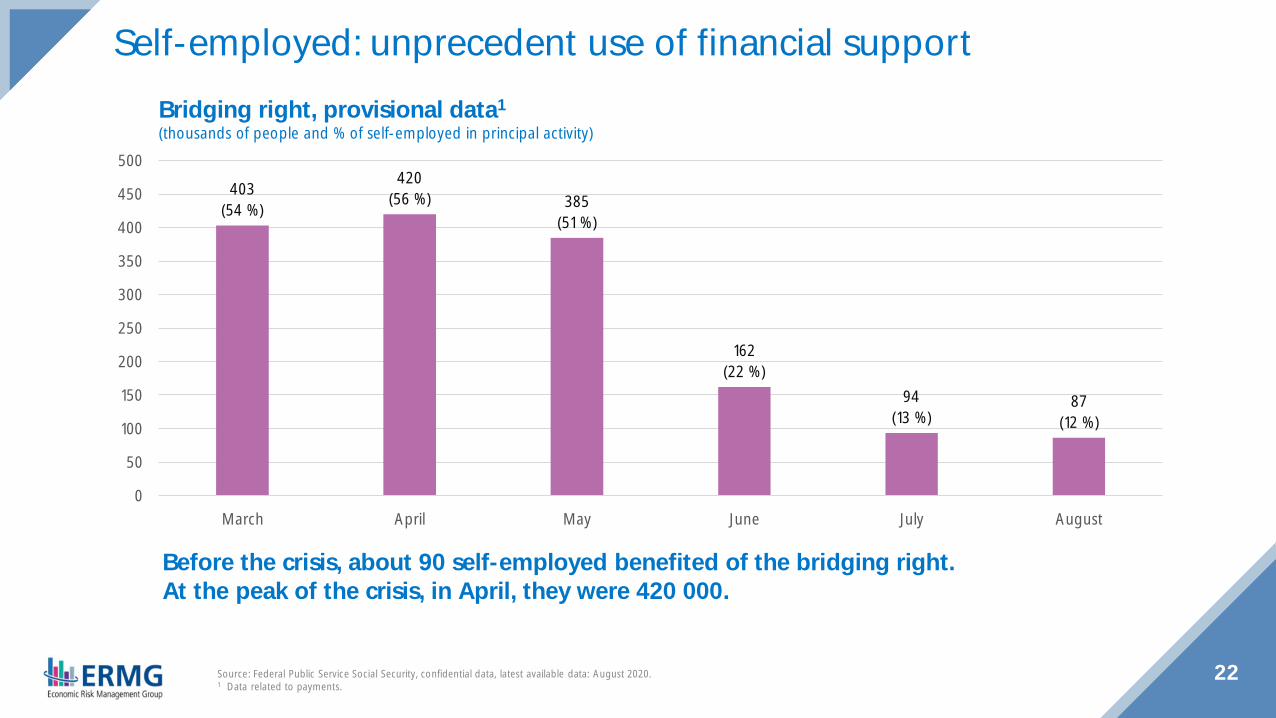

22Source: Federal Public Service Social Security, confidential data, latest available data: August 2020.1 Data related to payments.

Bridging right, provisional data1

(thousands of people and % of self-employed in principal activity)

Self-employed: unprecedent use of financial support

403(54 %)

420(56 %) 385

(51 %)

162(22 %)

94(13 %)

87(12 %)

0

50

100

150

200

250

300

350

400

450

500

March April May June July August

Before the crisis, about 90 self-employed benefited of the bridging right.At the peak of the crisis, in April, they were 420 000.

23Source: Statbel, dernières données disponibles: août 2020.1 Les indicateurs mensuels sont sujets à de plus fortes fluctuations aléatoires que les résultats trimestriels et annuels car ils reposent sur un douzième de l’échantillon annuel. Pour juin 2020 par

exemple, il s’agit d’environ 8 600 répondants. Les variations d’une période à l’autre doivent être interprétés avec prudence.

Taux de chômage(15-64)

Taux d’emploi(20-64)

La crise sanitaire a interrompu une dynamique positive(taux harmonisés issus des enquêtes force de travail1)

64

65

66

67

68

69

70

71

7220

16T1

2016

T220

16T3

2016

T420

17T1

2017

T220

17T3

2017

T420

18T1

2018

T220

18T3

2018

T420

19T1

2019

T220

19T3

2019

T420

20T1

2020

T2

2020

M7

e20

20M

8 e

Trimestriel Mensuel

0

1

2

3

4

5

6

7

8

9

2016

T120

16T2

2016

T320

16T4

2017

T120

17T2

2017

T320

17T4

2018

T120

18T2

2018

T320

18T4

2019

T120

19T2

2019

T320

19T4

2020

T120

20T2

2020

M7

e20

20M

8 e

24

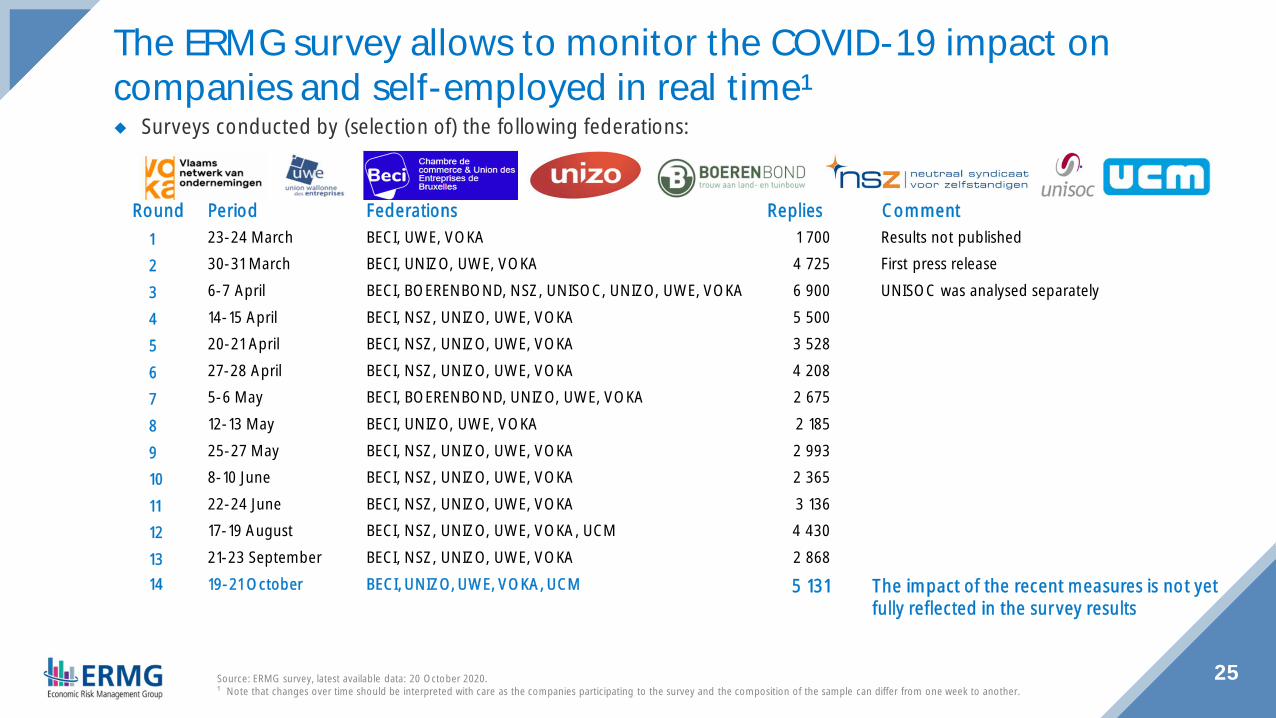

ERMG survey

The ERMG survey allows to monitor the COVID-19 impact oncompanies and self-employed in real time¹◆ Surveys conducted by (selection of) the following federations:

25

Round Period Federations Replies Comment1 23-24 March BECI, UWE, VOKA 1 700 Results not published

2 30-31 March BECI, UNIZO, UWE, VOKA 4 725 First press release

3 6-7 April BECI, BOERENBOND, NSZ, UNISOC, UNIZO, UWE, VOKA 6 900 UNISOC was analysed separately

4 14-15 April BECI, NSZ, UNIZO, UWE, VOKA 5 500

5 20-21 April BECI, NSZ, UNIZO, UWE, VOKA 3 528

6 27-28 April BECI, NSZ, UNIZO, UWE, VOKA 4 208

7 5-6 May BECI, BOERENBOND, UNIZO, UWE, VOKA 2 675

8 12-13 May BECI, UNIZO, UWE, VOKA 2 185

9 25-27 May BECI, NSZ, UNIZO, UWE, VOKA 2 993

10 8-10 June BECI, NSZ, UNIZO, UWE, VOKA 2 365

11 22-24 June BECI, NSZ, UNIZO, UWE, VOKA 3 136

12 17-19 August BECI, NSZ, UNIZO, UWE, VOKA, UCM 4 430

13 21-23 September BECI, NSZ, UNIZO, UWE, VOKA 2 86814 19-21 October BECI, UNIZO, UWE, VOKA, UCM 5 131 The impact of the recent measures is not yet

fully reflected in the survey results

Source: ERMG survey, latest available data: 20 October 2020.¹ Note that changes over time should be interpreted with care as the companies participating to the survey and the composition of the sample can differ from one week to another.

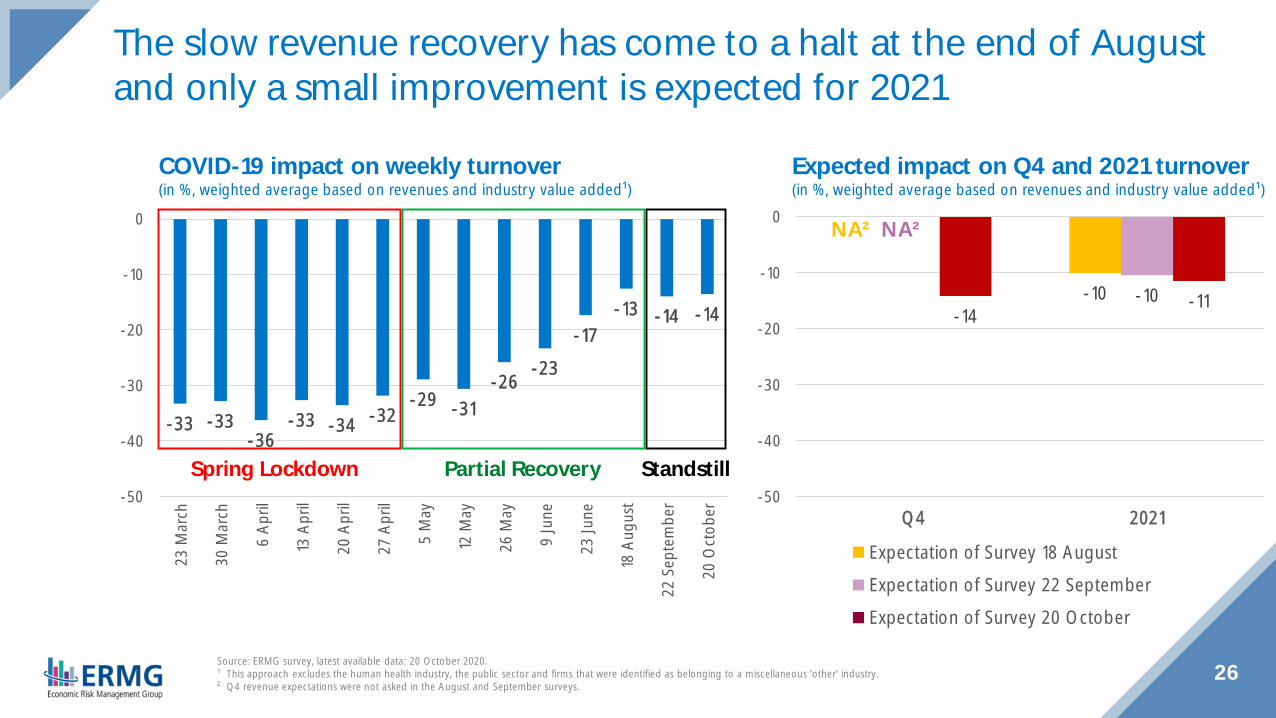

-33 -33-36

-33 -34 -32-29 -31

-26-23

-17-13 -14 -14

-50

-40

-30

-20

-10

0

23 M

arch

30 M

arch

6 Ap

ril

13 A

pril

20 A

pril

27 A

pril

5 M

ay

12 M

ay

26 M

ay

9 Ju

ne

23 Ju

ne

18 A

ugus

t

22 S

epte

mbe

r

20 O

ctob

er

26Source: ERMG survey, latest available data: 20 October 2020.¹ This approach excludes the human health industry, the public sector and firms that were identified as belonging to a miscellaneous ‘other’ industry.² Q4 revenue expectations were not asked in the August and September surveys.

Expected impact on Q4 and 2021 turnover(in %, weighted average based on revenues and industry value added¹)

COVID-19 impact on weekly turnover(in %, weighted average based on revenues and industry value added¹)

-10 -10-14

-11

-50

-40

-30

-20

-10

0

Q4 2021

Expectation of Survey 18 August

Expectation of Survey 22 September

Expectation of Survey 20 October

The slow revenue recovery has come to a halt at the end of Augustand only a small improvement is expected for 2021

Spring Lockdown Partial Recovery

NA² NA²

Standstill

-100

-80

-60

-40

-20

0

Arts,entertainmentand recreation

Accommodationand foodservices

Retail sales(non-food)

Wholesale Transportationand logistics

Manufacturing Support services Real estateactivities

Financial andinsuranceactivities

Construction Information andcommunication

Agriculture Retail sales(food)

April average(Rounds 2-6)

May average(Rounds 7-9)

June average(Rounds 10-11)

Week of 18 August(Round 12)

Week of 22 September(Round 13)

Week of 20 October(Round 14)

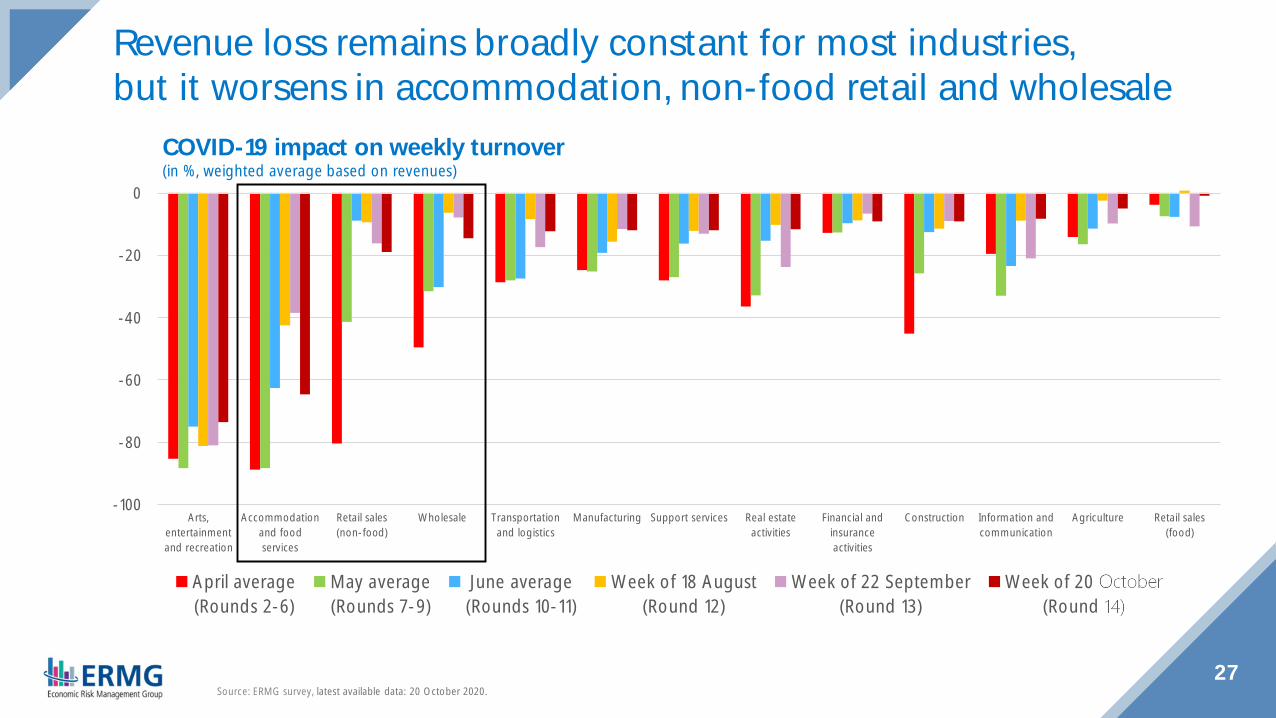

27

Revenue loss remains broadly constant for most industries,but it worsens in accommodation, non-food retail and wholesale

Source: ERMG survey, latest available data: 20 October 2020.

COVID-19 impact on weekly turnover(in %, weighted average based on revenues)

-100

-80

-60

-40

-20

0

Arts,entertainmentand recreation

Accommodationand foodservices

Retail sales(non-food)

Wholesale Transportationand logistics

Manufacturing Support services Real estateactivities

Financial andinsuranceactivities

Construction Information andcommunication

Agriculture Retail sales(food)

Week of 20 October Q4 expectation 2021 expectation

28

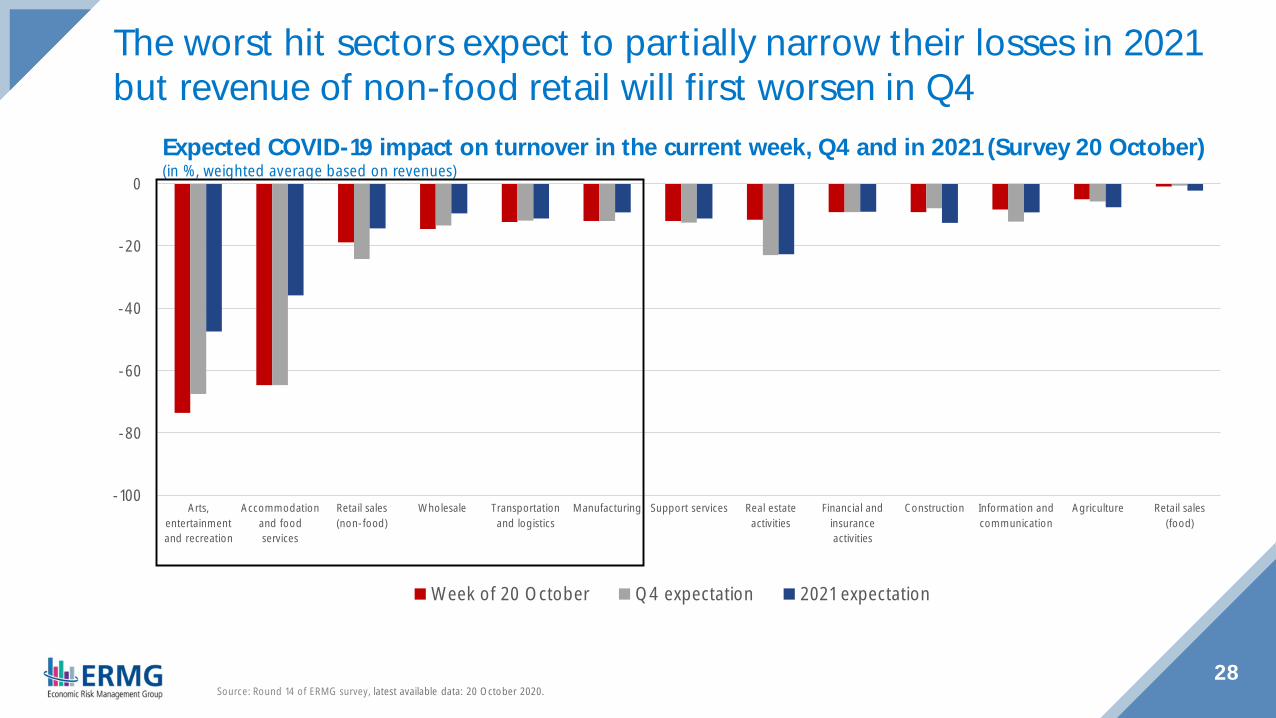

The worst hit sectors expect to partially narrow their losses in 2021but revenue of non-food retail will first worsen in Q4

Source: Round 14 of ERMG survey, latest available data: 20 October 2020.

Expected COVID-19 impact on turnover in the current week, Q4 and in 2021 (Survey 20 October)(in %, weighted average based on revenues)

29Source: ERMG survey, latest available data: 20 October 2020.¹ Weighted average based on the industry value added.² The results for this sector are based on only a few respondents and should therefore be interpreted with caution.

Impact of the COVID-19 crisis on company turnover by industry(in %, weighted average based on revenues)

< -25%in October

≥ -10%in October

-10 to -25%in October

-70

-60

-50

-40

-30

-20

-10

0

Self-employed 1 - 10 10 - 20 20 - 50 50 - 250 250 - 1000 > 1000

April average(Rounds 2-6)

May average(Rounds 7-9)

June average(Rounds 10-11)

Week of 18 August(Round 12)

Week of 22 September(Round 13)

Week of 20 October(Round 14)

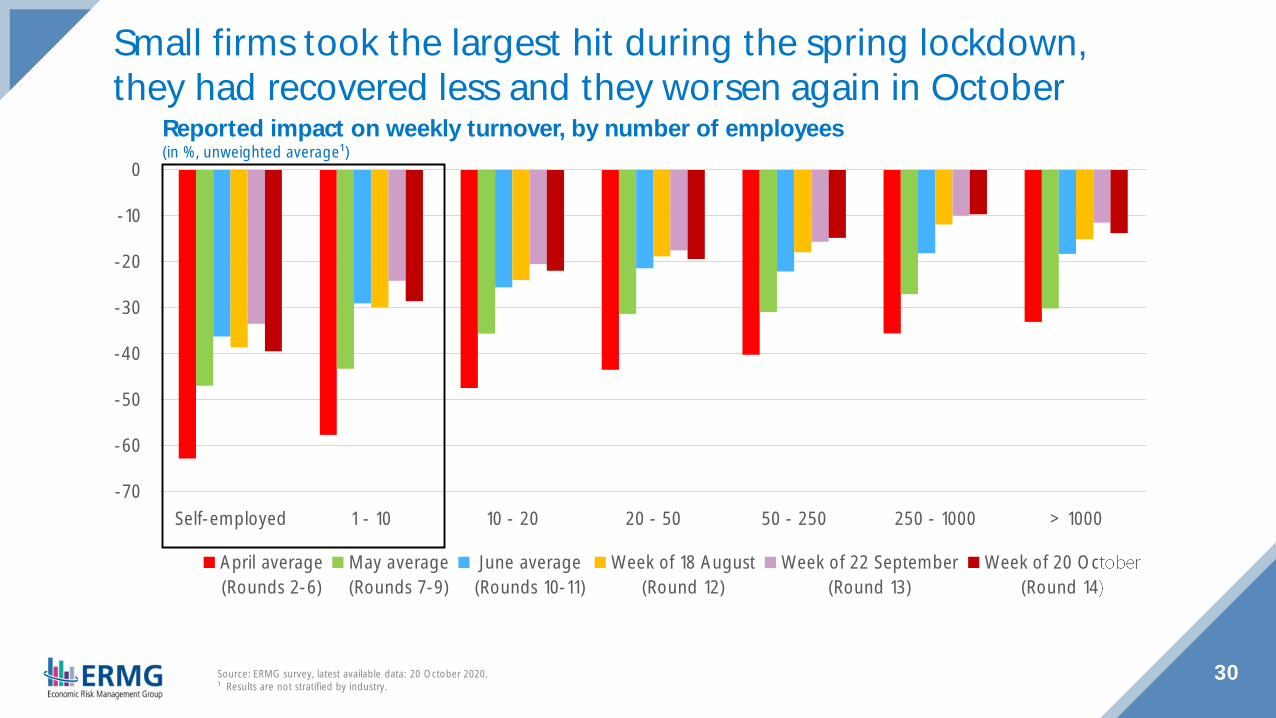

30Source: ERMG survey, latest available data: 20 October 2020.¹ Results are not stratified by industry.

Reported impact on weekly turnover, by number of employees(in %, unweighted average¹)

Small firms took the largest hit during the spring lockdown,they had recovered less and they worsen again in October

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Self-employed 1 - 10 10 - 20 20 - 50 50 - 250 250 - 1000 > 1000

Flemish Region Walloon Region Brussels-Capital Region

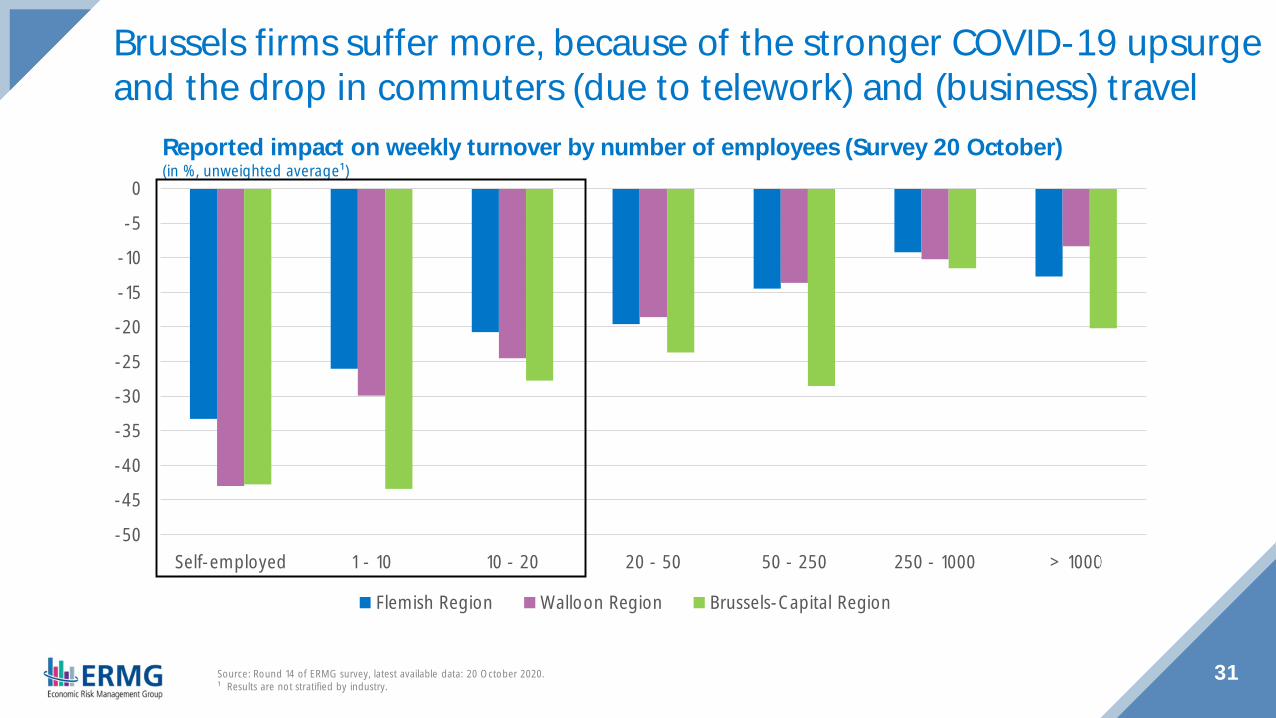

31Source: Round 14 of ERMG survey, latest available data: 20 October 2020.¹ Results are not stratified by industry.

Reported impact on weekly turnover by number of employees (Survey 20 October)(in %, unweighted average¹)

Brussels firms suffer more, because of the stronger COVID-19 upsurgeand the drop in commuters (due to telework) and (business) travel

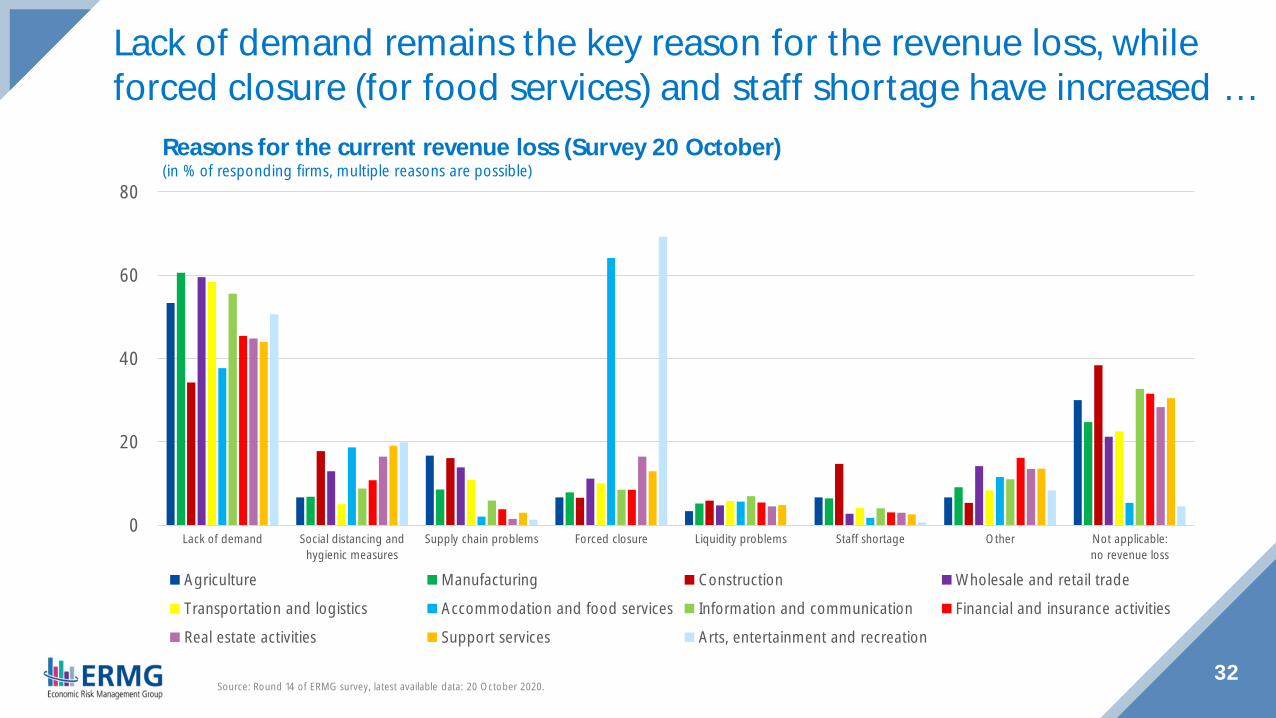

32Source: Round 14 of ERMG survey, latest available data: 20 October 2020.

Reasons for the current revenue loss (Survey 20 October)(in % of responding firms, multiple reasons are possible)

Lack of demand remains the key reason for the revenue loss, whileforced closure (for food services) and staff shortage have increased …

0

20

40

60

80

Lack of demand Social distancing andhygienic measures

Supply chain problems Forced closure Liquidity problems Staff shortage Other Not applicable:no revenue loss

Agriculture Manufacturing Construction Wholesale and retail trade

Transportation and logistics Accommodation and food services Information and communication Financial and insurance activities

Real estate activities Support services Arts, entertainment and recreation

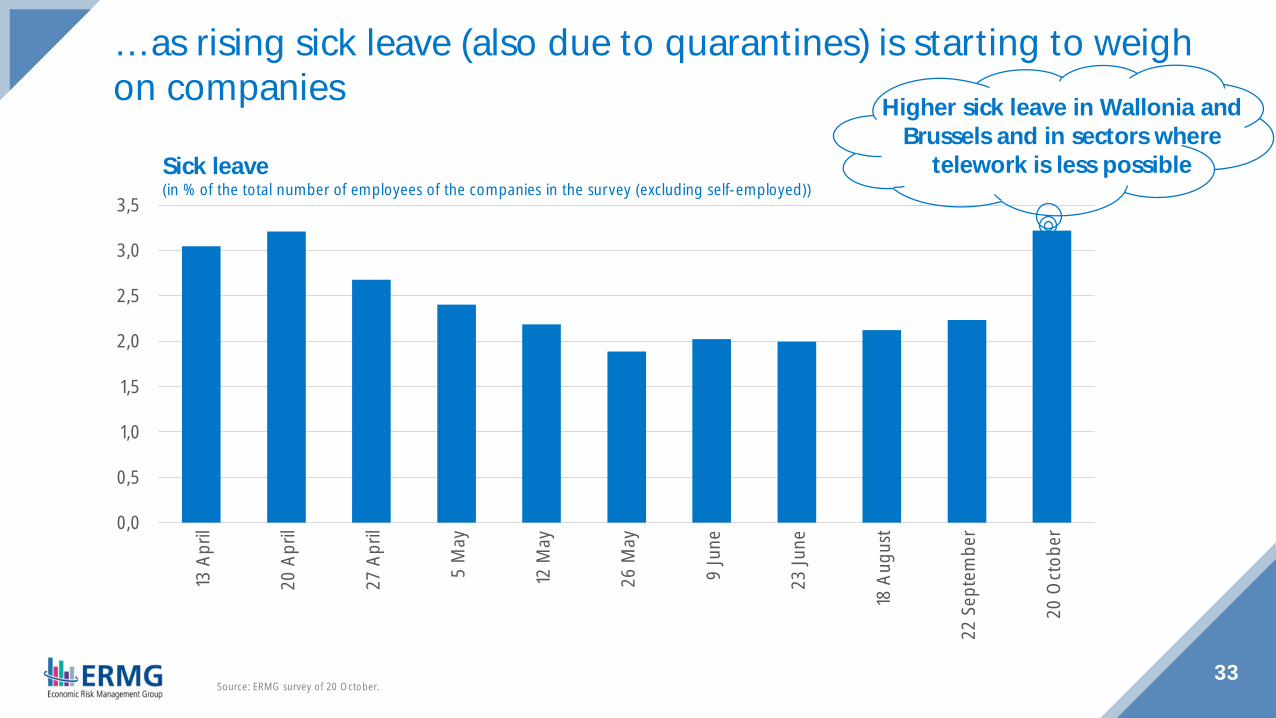

33Source: ERMG survey of 20 October.

… as rising sick leave (also due to quarantines) is starting to weighon companies

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,513

Apr

il

20 A

pril

27 A

pril

5 M

ay

12 M

ay

26 M

ay

9 Ju

ne

23 Ju

ne

18 A

ugus

t

22 S

epte

mbe

r

20 O

ctob

er

Sick leave(in % of the total number of employees of the companies in the survey (excluding self-employed))

Higher sick leave in Wallonia andBrussels and in sectors where

telework is less possible

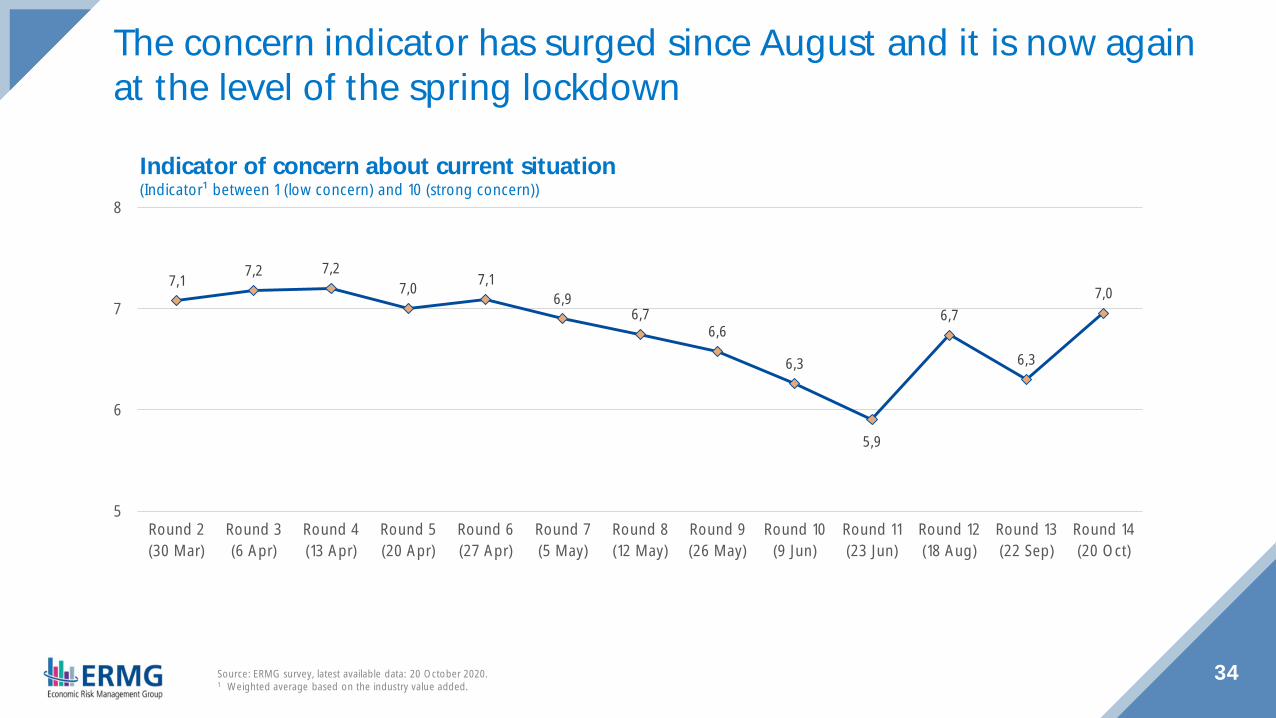

34Source: ERMG survey, latest available data: 20 October 2020.1 Weighted average based on the industry value added.

The concern indicator has surged since August and it is now againat the level of the spring lockdown

Indicator of concern about current situation(Indicator¹ between 1 (low concern) and 10 (strong concern))

7,1 7,2 7,27,0 7,1

6,96,7

6,6

6,3

5,9

6,7

6,3

7,0

5

6

7

8

Round 2(30 Mar)

Round 3(6 Apr)

Round 4(13 Apr)

Round 5(20 Apr)

Round 6(27 Apr)

Round 7(5 May)

Round 8(12 May)

Round 9(26 May)

Round 10(9 Jun)

Round 11(23 Jun)

Round 12(18 Aug)

Round 13(22 Sep)

Round 14(20 Oct)

34

35

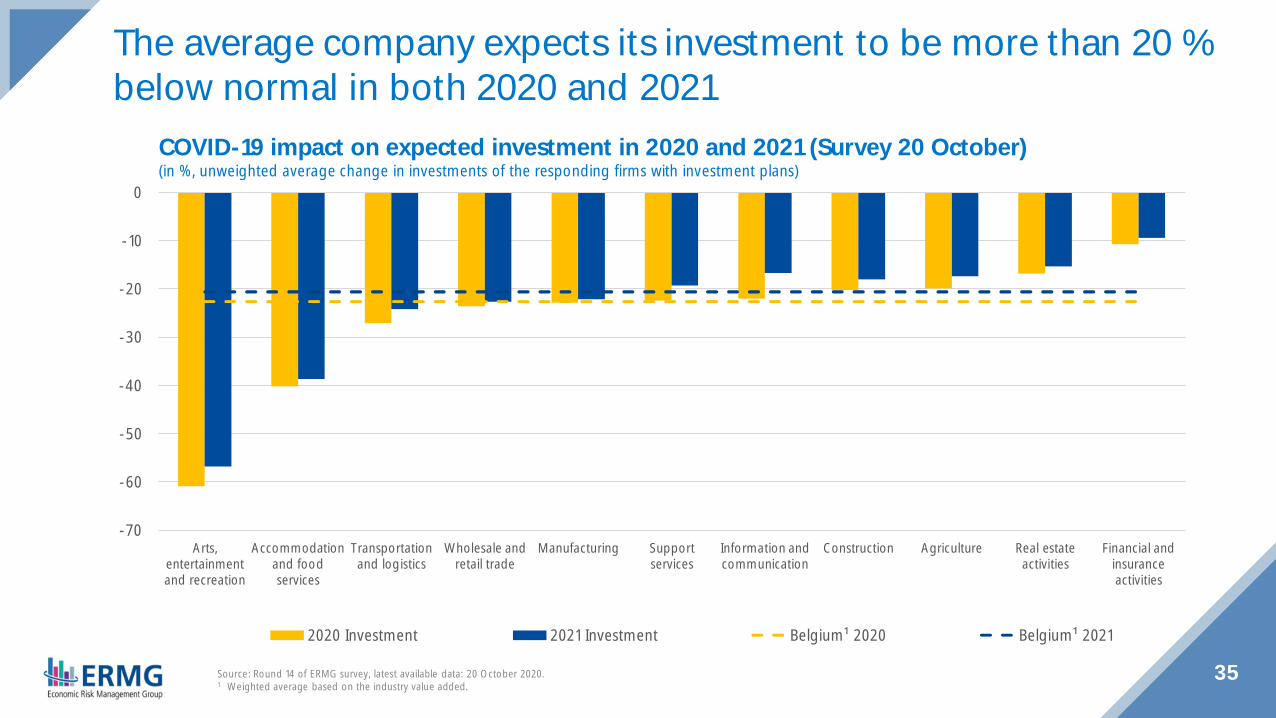

The average company expects its investment to be more than 20 %below normal in both 2020 and 2021

-70

-60

-50

-40

-30

-20

-10

0

Arts,entertainmentand recreation

Accommodationand foodservices

Transportationand logistics

Wholesale andretail trade

Manufacturing Supportservices

Information andcommunication

Construction Agriculture Real estateactivities

Financial andinsuranceactivities

2020 Investment 2021 Investment Belgium¹ 2020 Belgium¹ 2021

COVID-19 impact on expected investment in 2020 and 2021 (Survey 20 October)(in %, unweighted average change in investments of the responding firms with investment plans)

35Source: Round 14 of ERMG survey, latest available data: 20 October 2020.1 Weighted average based on the industry value added.

0

10

20

30

40

50

60

70

80

No, I do not have liquidityproblems

Yes, due to revenue loss Yes, due to late payments of ourclients

Yes, due to delayed governmentpayments

Yes, due to insufficient credit lines

April average(Rounds 2-6)

May average(Rounds 7-9)

June average(Rounds 10-11)

Week of 18 August(Round 12)

Week of 22 September(Round 13)

Week of 20 October(Round 14)

36

The liquidity of the companies had improved since the lockdown,but it deteriorates again in October …

Source: ERMG survey, latest available data: 20 October 2020.¹ Weighted average based on the industry value added.

Do you have liquidity problems?(in % of responding firms¹, multiple answers are possible)

0

10

20

30

40

50

60

70

80

90

100

Belgium¹ Arts,entertainmentand recreation

Accommodationand food services

Information andcommunication

Agriculture Retail sales(non-food)

Wholesale Construction Support services Real estateactivities

Manufacturing Transportationand logistics

Retail sales(food)

Financial andinsuranceactivities

< 1 month 1 - 3 months 3 - 6 months 6 - 12 months >12 months

37

… as 60 % of firms need additional financing in the short run to meettheir current financial obligations

Source: Round 14 of ERMG survey, latest available data: 20 October 2020.¹ Weighted average based on the industry value added.

How long can you still meet your current financial obligations (debt repayment, rent, taxes, …)without having to rely on additional equity or credit? (Survey 20 October)(in % of responding firms)

0

5

10

15

20

25

30

35

Belgium¹ Accommodationand food services

Arts,entertainmentand recreation

Transportationand logistics

Real estateactivities

Retail sales(food)

Retail sales(non-food)

Information andcommunication

Support services Agriculture Manufacturing Construction Financial andinsuranceactivities

Wholesale

April average(Rounds 2-6)

May average(Rounds 7-9)

June average(Rounds 10-11)

Week of 18 August(Round 12)²

Week of 22 September(Round 13)

Week of 20 October(Round 14)²

38

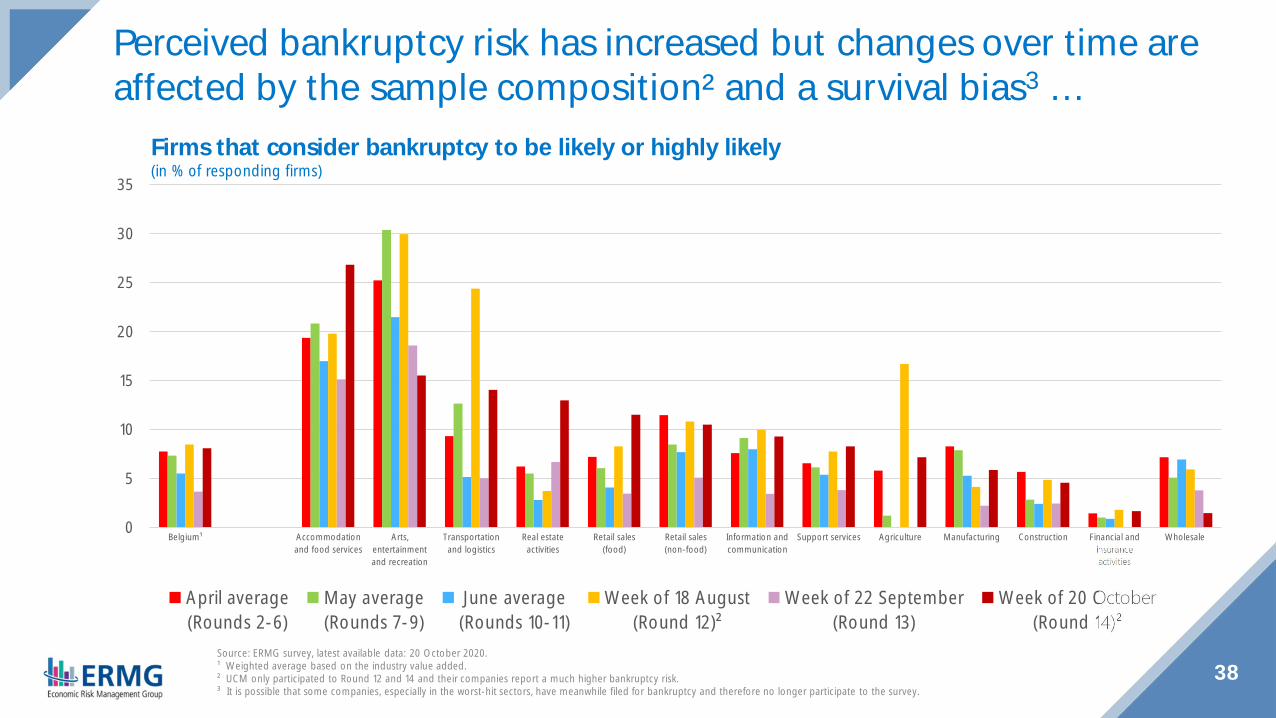

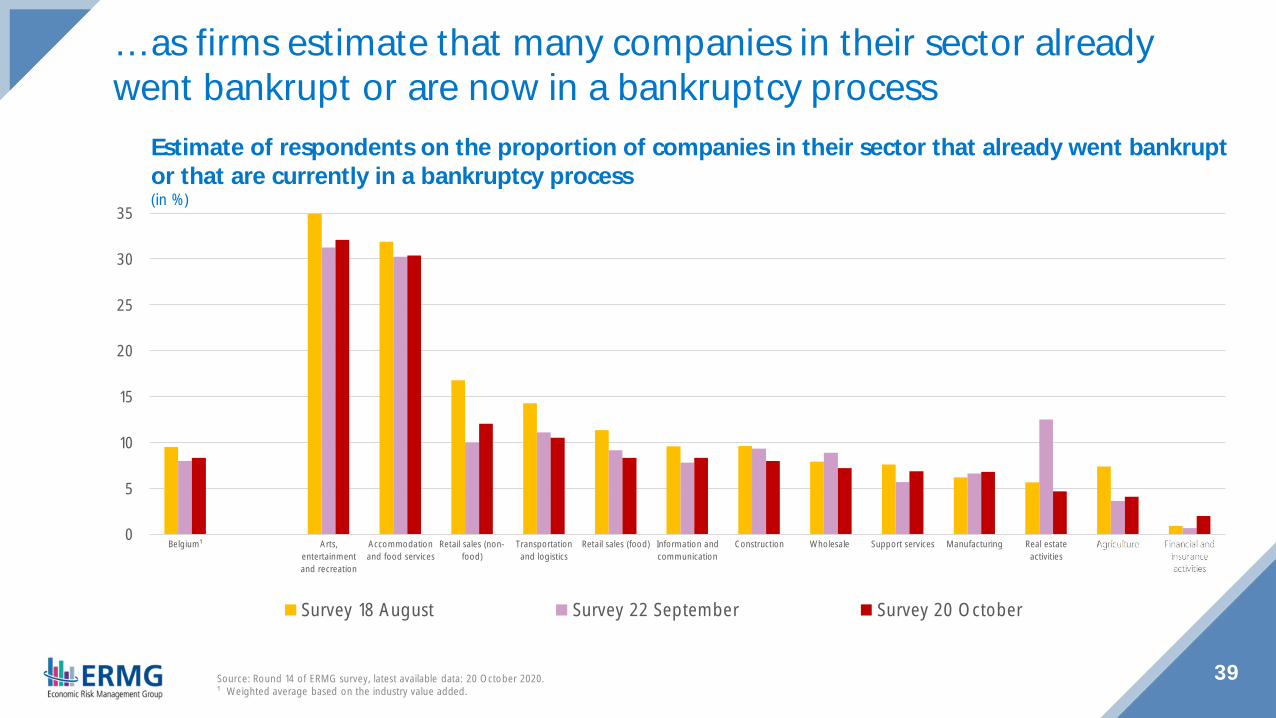

Perceived bankruptcy risk has increased but changes over time areaffected by the sample composition² and a survival bias3 …

Source: ERMG survey, latest available data: 20 October 2020.¹ Weighted average based on the industry value added.² UCM only participated to Round 12 and 14 and their companies report a much higher bankruptcy risk.³ It is possible that some companies, especially in the worst-hit sectors, have meanwhile filed for bankruptcy and therefore no longer participate to the survey.

Firms that consider bankruptcy to be likely or highly likely(in % of responding firms)

0

5

10

15

20

25

30

35

Belgium¹ Arts,entertainmentand recreation

Accommodationand food services

Retail sales (non-food)

Transportationand logistics

Retail sales (food) Information andcommunication

Construction Wholesale Support services Manufacturing Real estateactivities

Agriculture Financial andinsuranceactivities

Survey 18 August Survey 22 September Survey 20 October

39

… as firms estimate that many companies in their sector alreadywent bankrupt or are now in a bankruptcy process

Source: Round 14 of ERMG survey, latest available data: 20 October 2020.¹ Weighted average based on the industry value added.

Estimate of respondents on the proportion of companies in their sector that already went bankruptor that are currently in a bankruptcy process(in %)

-35

-30

-25

-20

-15

-10

-5

0

5

Belgium¹ Arts,entertainmentand recreation

Accommodationand foodservices

Retail sales(non-food)

Financial andinsuranceactivities

Transportationand logistics

Wholesale Manufacturing Retail sales(food)

Construction Agriculture Support services Information andcommunication

Real estateactivities

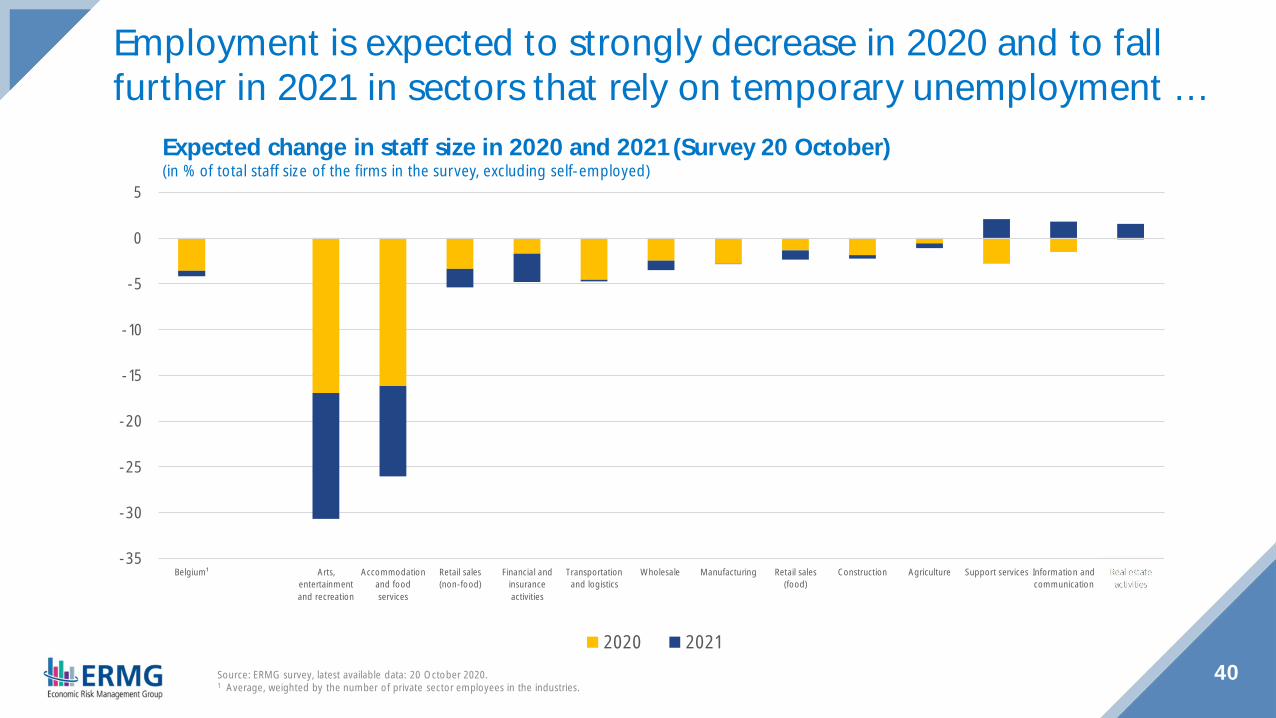

2020 202140Source: ERMG survey, latest available data: 20 October 2020.

1 Average, weighted by the number of private sector employees in the industries.

Expected change in staff size in 2020 and 2021 (Survey 20 October)(in % of total staff size of the firms in the survey, excluding self-employed)

Employment is expected to strongly decrease in 2020 and to fallfurther in 2021 in sectors that rely on temporary unemployment …

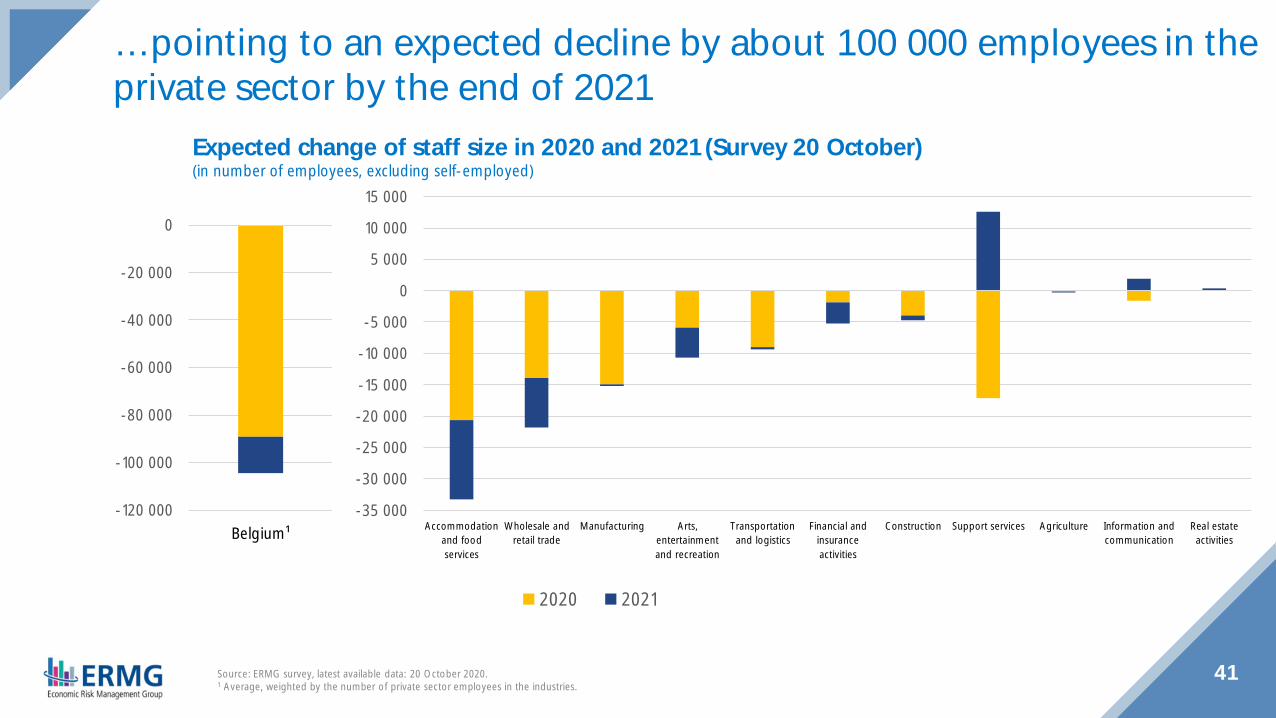

41Source: ERMG survey, latest available data: 20 October 2020.1 Average, weighted by the number of private sector employees in the industries.

Expected change of staff size in 2020 and 2021 (Survey 20 October)(in number of employees, excluding self-employed)

… pointing to an expected decline by about 100 000 employees in theprivate sector by the end of 2021

-120 000

-100 000

-80 000

-60 000

-40 000

-20 000

0

Belgium¹-35 000

-30 000

-25 000

-20 000

-15 000

-10 000

-5 000

0

5 000

10 000

15 000

Accommodationand foodservices

Wholesale andretail trade

Manufacturing Arts,entertainmentand recreation

Transportationand logistics

Financial andinsuranceactivities

Construction Support services Agriculture Information andcommunication

Real estateactivities

2020 2021

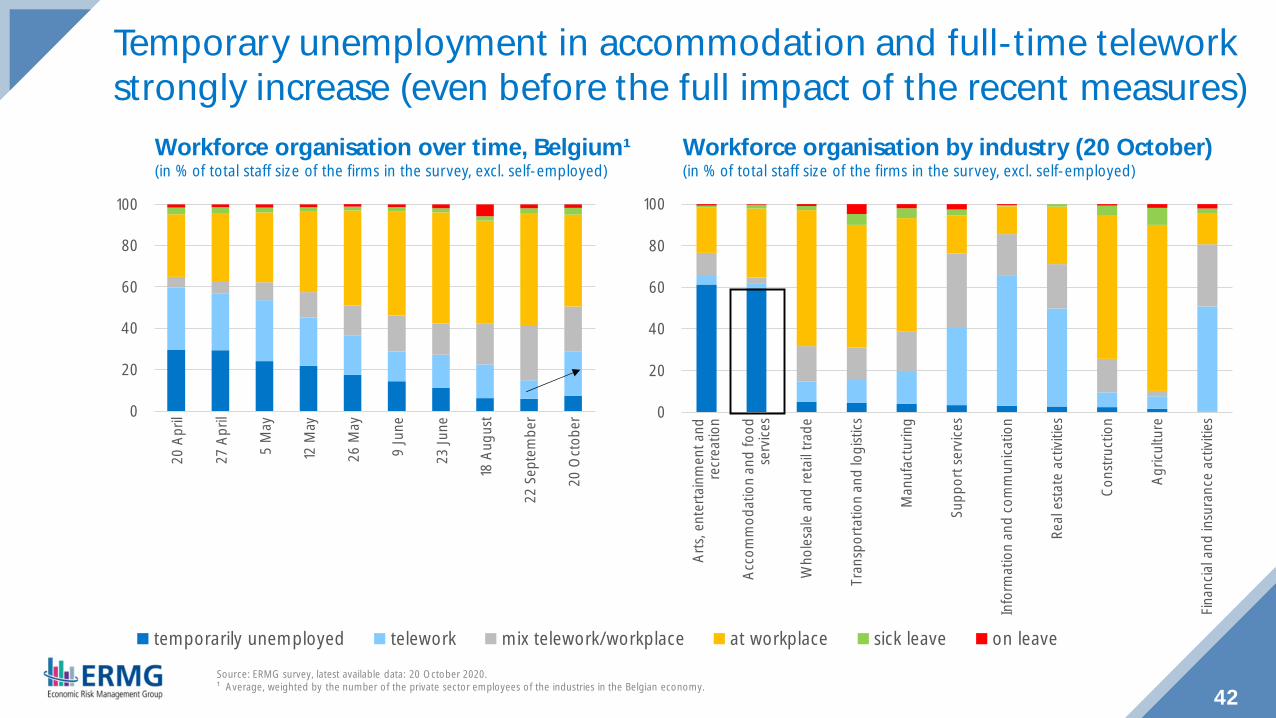

42Source: ERMG survey, latest available data: 20 October 2020.¹ Average, weighted by the number of the private sector employees of the industries in the Belgian economy.

Workforce organisation over time, Belgium¹(in % of total staff size of the firms in the survey, excl. self-employed)

Temporary unemployment in accommodation and full-time teleworkstrongly increase (even before the full impact of the recent measures)

0

20

40

60

80

10020

Apr

il

27 A

pril

5 M

ay

12 M

ay

26 M

ay

9 Ju

ne

23 Ju

ne

18 A

ugus

t

22 S

epte

mbe

r

20 O

ctob

er

temporarily unemployed telework mix telework/workplace at workplace sick leave on leave

0

20

40

60

80

100

Arts,

ent

erta

inm

ent a

ndre

crea

tion

Acco

mm

odat

ion

and

food

serv

ices

Who

lesa

le a

nd re

tail t

rade

Tran

spor

tatio

n an

d lo

gisti

cs

Man

ufac

turin

g

Supp

ort s

ervic

es

Info

rmat

ion

and

com

mun

icatio

n

Real

esta

te a

ctivi

ties

Cons

truct

ion

Agric

ultu

re

Finan

cial a

nd in

sura

nce

activ

ities

Workforce organisation by industry (20 October)(in % of total staff size of the firms in the survey, excl. self-employed)

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

Belgium¹ Support services Information andcommunication

Financial andinsuranceactivities

Real estateactivities

Manufacturing Transportationand logistics

Arts,entertainmentand recreation

Wholesale andretail trade

Construction Agriculture Accommodationand foodservices

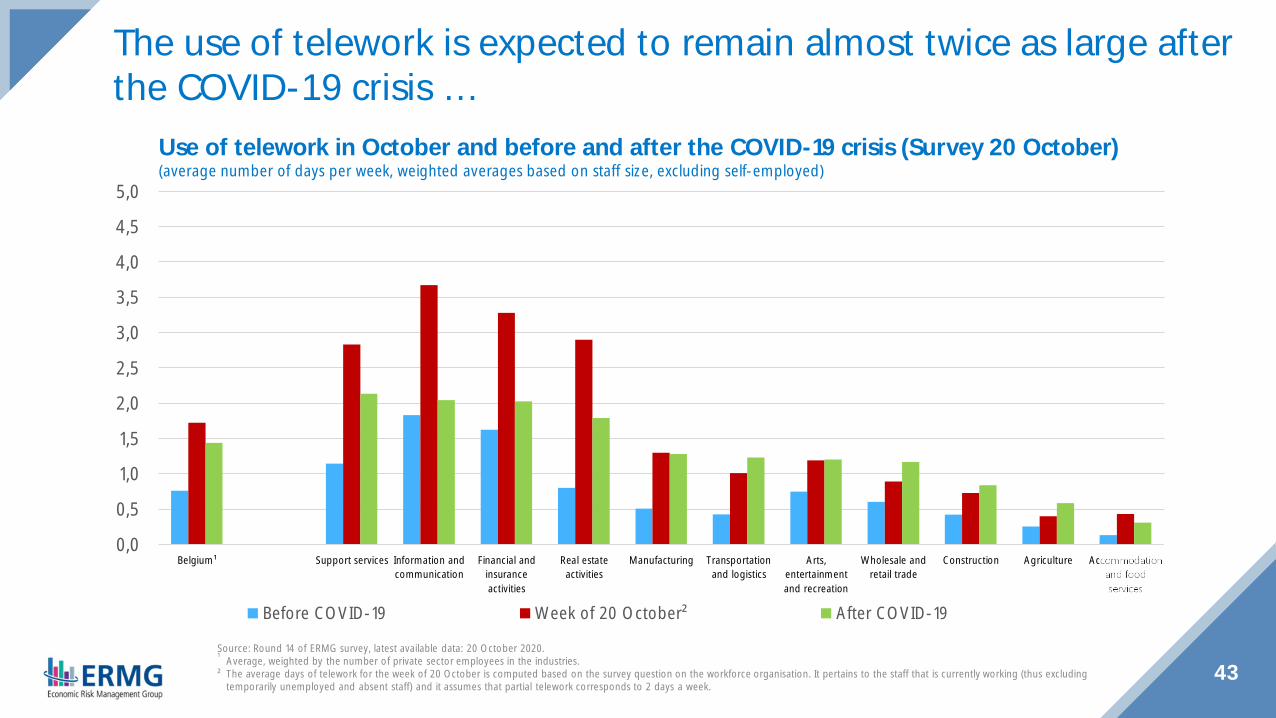

Before COVID-19 Week of 20 October² After COVID-19

43Source: Round 14 of ERMG survey, latest available data: 20 October 2020.¹ Average, weighted by the number of private sector employees in the industries.² The average days of telework for the week of 20 October is computed based on the survey question on the workforce organisation. It pertains to the staff that is currently working (thus excluding

temporarily unemployed and absent staff) and it assumes that partial telework corresponds to 2 days a week.

Use of telework in October and before and after the COVID-19 crisis (Survey 20 October)(average number of days per week, weighted averages based on staff size, excluding self-employed)

The use of telework is expected to remain almost twice as large afterthe COVID-19 crisis …

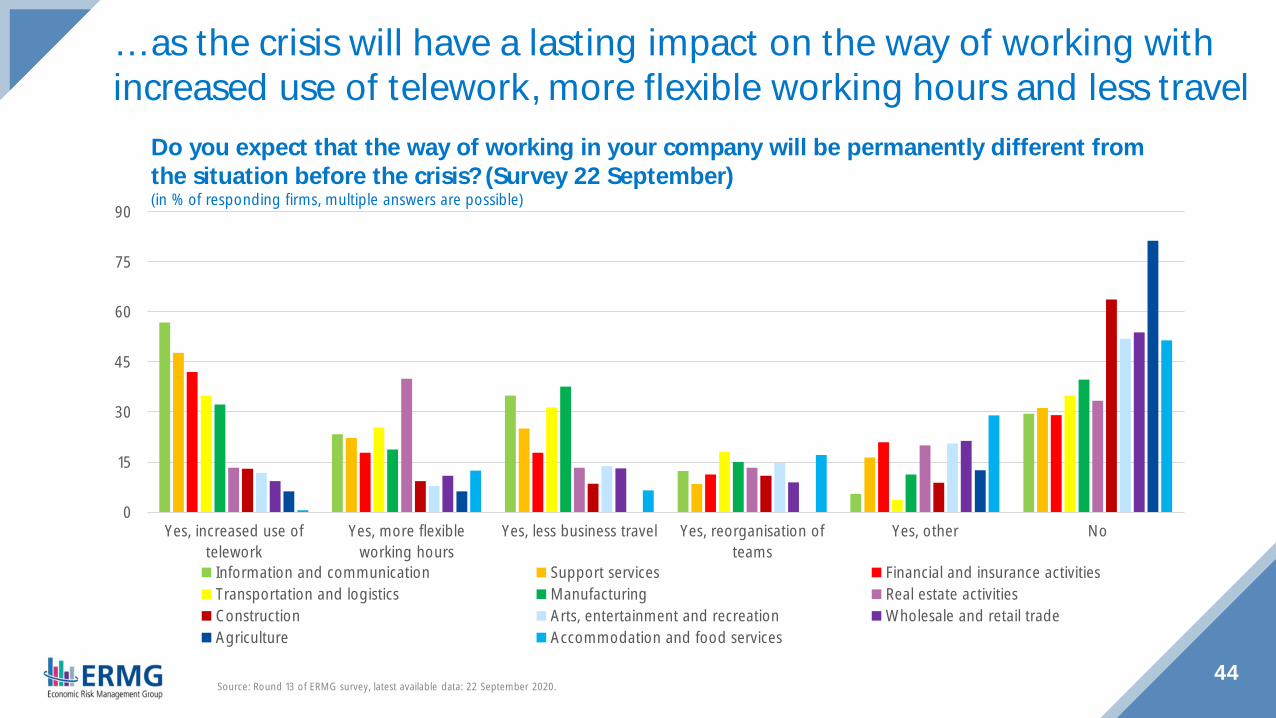

44Source: Round 13 of ERMG survey, latest available data: 22 September 2020.

Do you expect that the way of working in your company will be permanently different fromthe situation before the crisis? (Survey 22 September)(in % of responding firms, multiple answers are possible)

… as the crisis will have a lasting impact on the way of working withincreased use of telework, more flexible working hours and less travel

0

15

30

45

60

75

90

Yes, increased use oftelework

Yes, more flexibleworking hours

Yes, less business travel Yes, reorganisation ofteams

Yes, other No

Information and communication Support services Financial and insurance activitiesTransportation and logistics Manufacturing Real estate activitiesConstruction Arts, entertainment and recreation Wholesale and retail tradeAgriculture Accommodation and food services

45Source: Round 12 of ERMG survey, latest available data: 18 August 2020.

Do you expect that, as a result of the COVID-19 crisis, the production of your company that iscurrently produced outside the EU will be moved to a country within the EU? (Round 12)(In % of responding firms)

Few firms have non-EU production and the vast majority of thesefirms will not reshore this production

0

20

40

60

80

100

Yes, 100% of ournon-EU production

Yes, 20-50% of ournon-EU production

Yes, 0-50% of ournon-EU production

No, we keep ournon-EU production

Not applicable:I do not have

non-EU production

Agriculture Manufacturing Financial and insurance activities Transportation and logisticsInformation and communication Wholesale and retail trade Support services Arts, entertainment and recreationAccommodation and food services Construction Real estate activities

46

Credit indicatorshouseholds

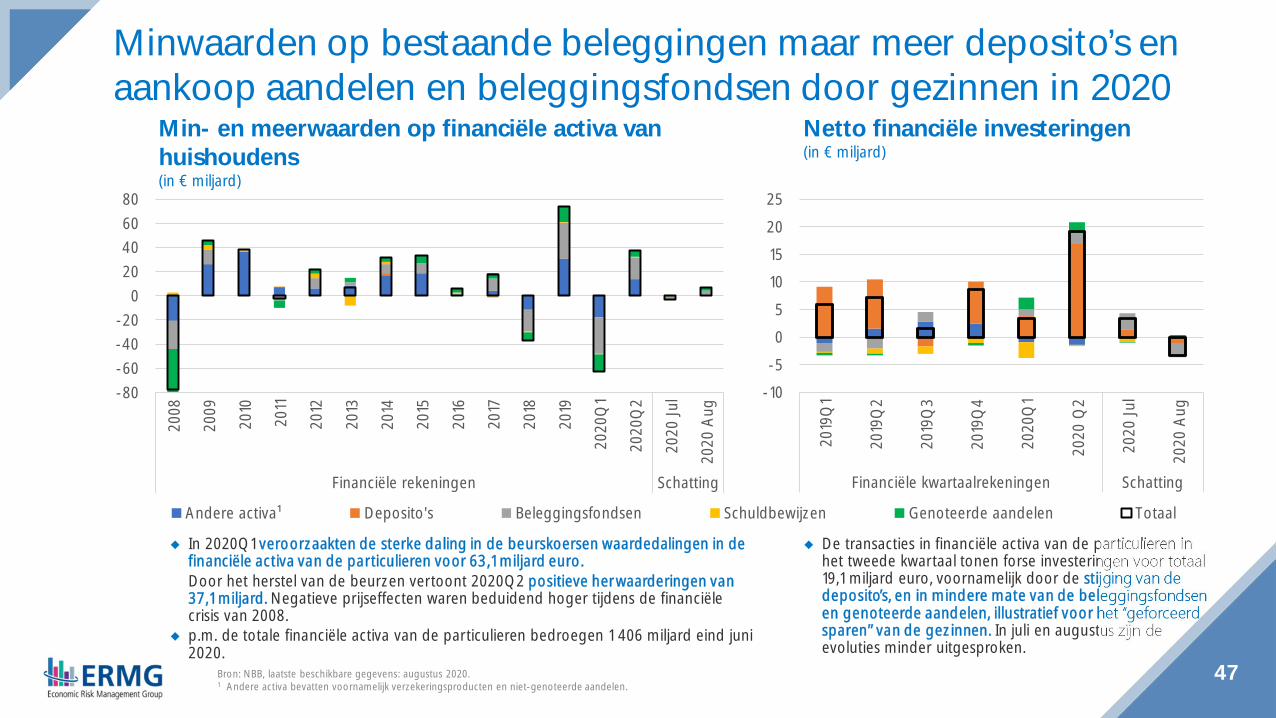

◆ De transacties in financiële activa van de particulieren inhet tweede kwartaal tonen forse investeringen voor totaal19,1 miljard euro, voornamelijk door de stijging van dedeposito’s, en in mindere mate van de beleggingsfondsenen genoteerde aandelen, illustratief voor het “geforceerdsparen” van de gezinnen. In juli en augustus zijn deevoluties minder uitgesproken.

47Bron: NBB, laatste beschikbare gegevens: augustus 2020.1 Andere activa bevatten voornamelijk verzekeringsproducten en niet-genoteerde aandelen.

Minwaarden op bestaande beleggingen maar meer deposito’s enaankoop aandelen en beleggingsfondsen door gezinnen in 2020

Netto financiële investeringen(in € miljard)

Min- en meerwaarden op financiële activa vanhuishoudens(in € miljard)

◆ In 2020Q1 veroorzaakten de sterke daling in de beurskoersen waardedalingen in definanciële activa van de particulieren voor 63,1 miljard euro.Door het herstel van de beurzen vertoont 2020Q2 positieve herwaarderingen van37,1 miljard. Negatieve prijseffecten waren beduidend hoger tijdens de financiëlecrisis van 2008.

◆ p.m. de totale financiële activa van de particulieren bedroegen 1 406 miljard eind juni2020.

-80-60-40-20

020406080

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Q1

2020

Q2

2020

Jul

2020

Aug

Financiële rekeningen Schatting

Andere activa¹ Deposito's Beleggingsfondsen Schuldbewijzen Genoteerde aandelen Totaal

-10-505

10152025

2019

Q1

2019

Q2

2019

Q3

2019

Q4

2020

Q1

2020

Q2

2020

Jul

2020

Aug

Financiële kwartaalrekeningen Schatting

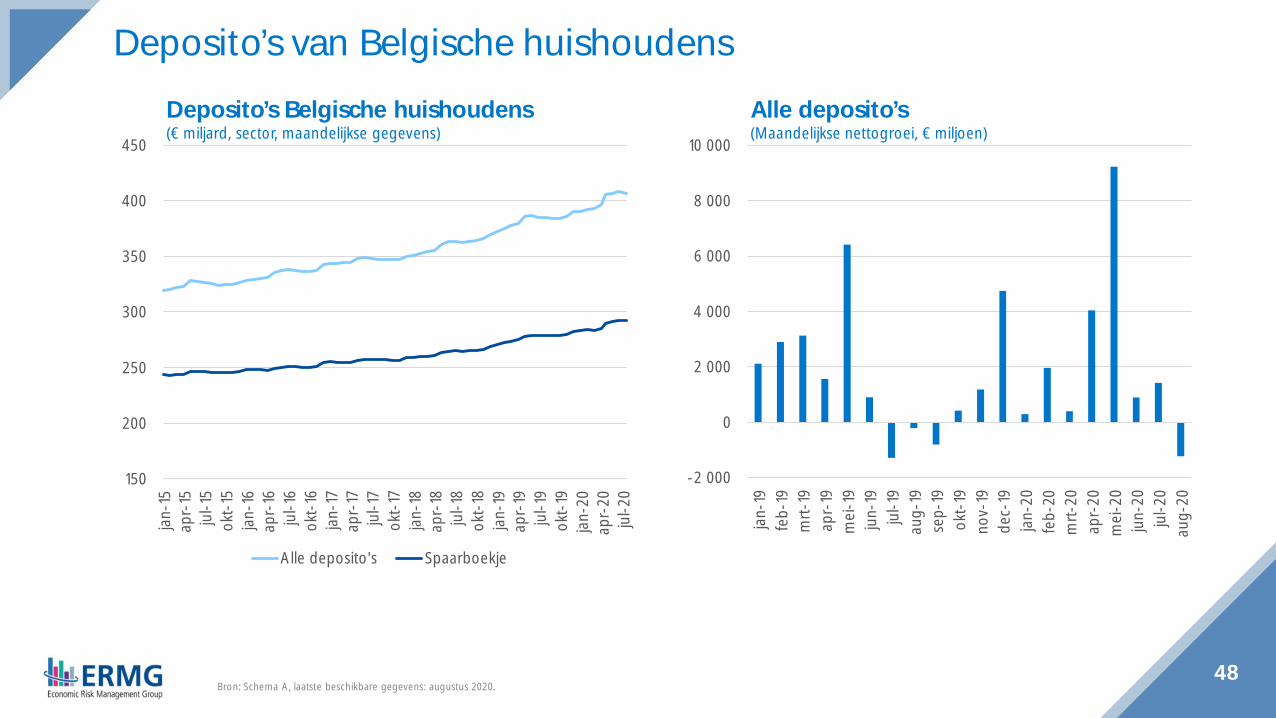

48Bron: Schema A, laatste beschikbare gegevens: augustus 2020.

Alle deposito’s(Maandelijkse nettogroei, € miljoen)

Deposito’s Belgische huishoudens(€ miljard, sector, maandelijkse gegevens)

Deposito’s van Belgische huishoudens

150

200

250

300

350

400

450jan

-15

apr-

15ju

l-15

okt-

15jan

-16

apr-

16ju

l-16

okt-

16jan

-17

apr-

17ju

l-17

okt-

17jan

-18

apr-

18ju

l-18

okt-

18jan

-19

apr-

19ju

l-19

okt-

19jan

-20

apr-

20ju

l-20

Alle deposito's Spaarboekje

-2 000

0

2 000

4 000

6 000

8 000

10 000

jan-1

9fe

b-19

mrt-

19ap

r-19

mei

-19

jun-

19ju

l-19

aug-

19se

p-19

okt-

19no

v-19

dec-

19jan

-20

feb-

20m

rt-20

apr-

20m

ei-2

0ju

n-20

jul-2

0au

g-20

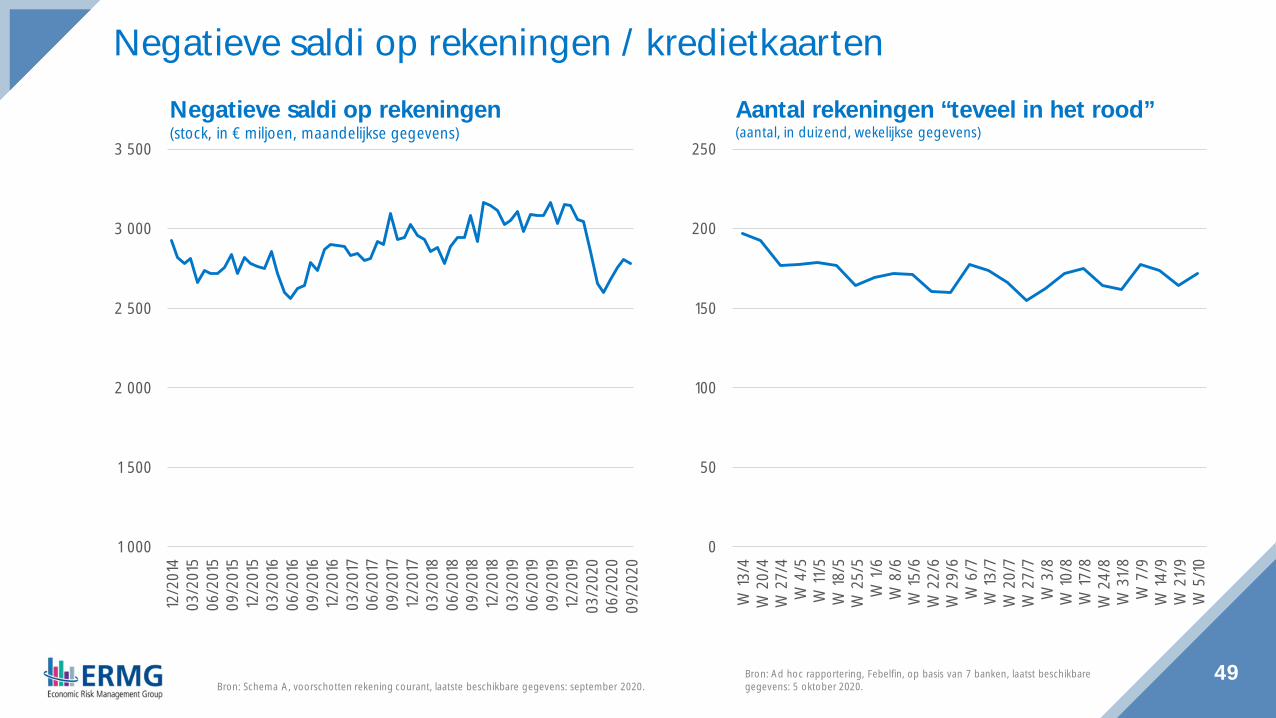

Negatieve saldi op rekeningen / kredietkaarten

49

Negatieve saldi op rekeningen(stock, in € miljoen, maandelijkse gegevens)

Bron: Ad hoc rapportering, Febelfin, op basis van 7 banken, laatst beschikbaregegevens: 5 oktober 2020.Bron: Schema A, voorschotten rekening courant, laatste beschikbare gegevens: september 2020.

Aantal rekeningen “teveel in het rood”(aantal, in duizend, wekelijkse gegevens)

1 000

1 500

2 000

2 500

3 000

3 50012

/201

403

/201

506

/201

509

/201

512

/201

503

/201

606

/201

609

/201

612

/201

603

/201

706

/201

709

/201

712

/201

703

/201

806

/201

809

/201

812

/201

803

/201

906

/201

909

/201

912

/201

903

/202

006

/202

009

/202

0

0

50

100

150

200

250

W 13

/4W

20/

4W

27/

4W

4/5

W 11

/5W

18/5

W 2

5/5

W 1/

6W

8/6

W 15

/6W

22/

6W

29/

6W

6/7

W 13

/7W

20/

7W

27/

7W

3/8

W 10

/8W

17/8

W 2

4/8

W 3

1/8

W 7

/9W

14/9

W 2

1/9

W 5

/10

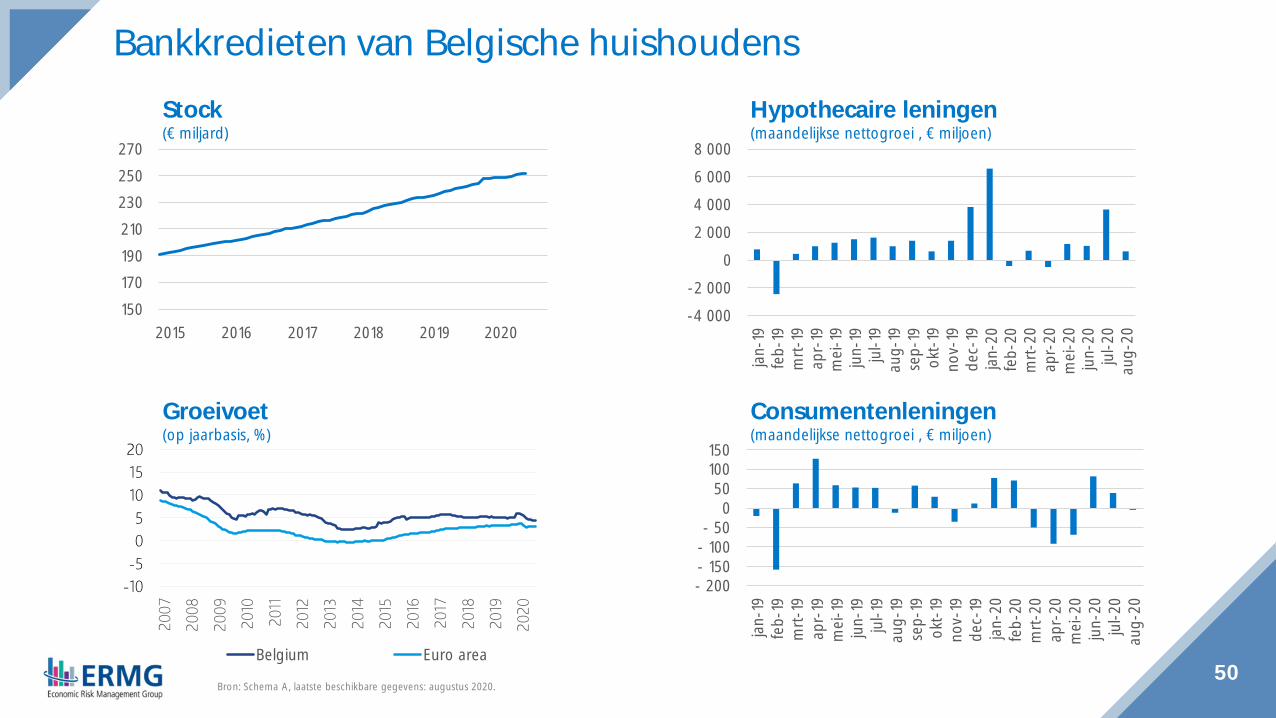

Bankkredieten van Belgische huishoudens

50Bron: Schema A, laatste beschikbare gegevens: augustus 2020.

Hypothecaire leningen(maandelijkse nettogroei , € miljoen)

Stock(€ miljard)

Consumentenleningen(maandelijkse nettogroei , € miljoen)

Groeivoet(op jaarbasis, %)

-10-505101520

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Belgium Euro area

150170190210230250270

2015 2016 2017 2018 2019 2020-4 000-2 000

02 0004 0006 0008 000

jan-1

9fe

b-19

mrt-

19ap

r-19

mei

-19

jun-

19ju

l-19

aug-

19se

p-19

okt-

19no

v-19

dec-

19jan

-20

feb-

20m

rt-20

apr-

20m

ei-2

0ju

n-20

jul-2

0au

g-20

- 200- 150- 100- 50

0 50

100 150

jan-1

9fe

b-19

mrt-

19ap

r-19

mei

-19

jun-

19ju

l-19

aug-

19se

p-19

okt-

19no

v-19

dec-

19jan

-20

feb-

20m

rt-20

apr-

20m

ei-2

0ju

n-20

jul-2

0au

g-20

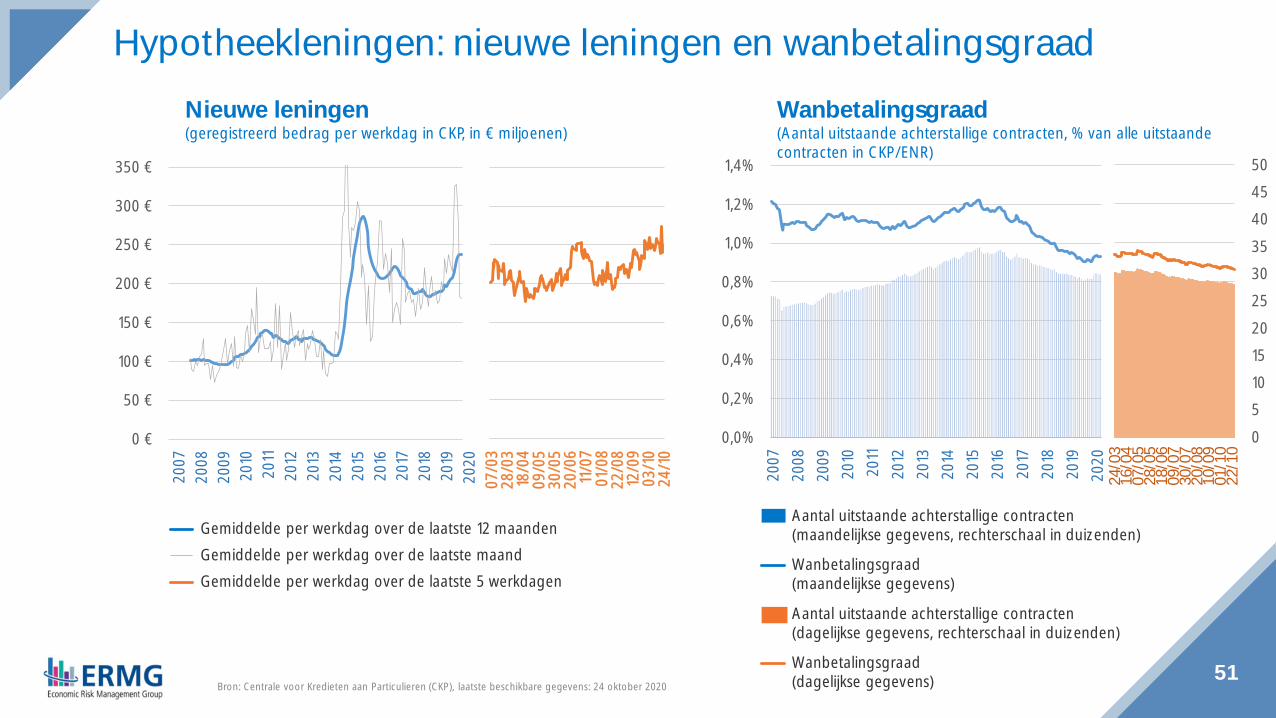

51Bron: Centrale voor Kredieten aan Particulieren (CKP), laatste beschikbare gegevens: 24 oktober 2020

Wanbetalingsgraad(Aantal uitstaande achterstallige contracten, % van alle uitstaandecontracten in CKP/ENR)

Nieuwe leningen(geregistreerd bedrag per werkdag in CKP, in € miljoenen)

Hypotheekleningen: nieuwe leningen en wanbetalingsgraad

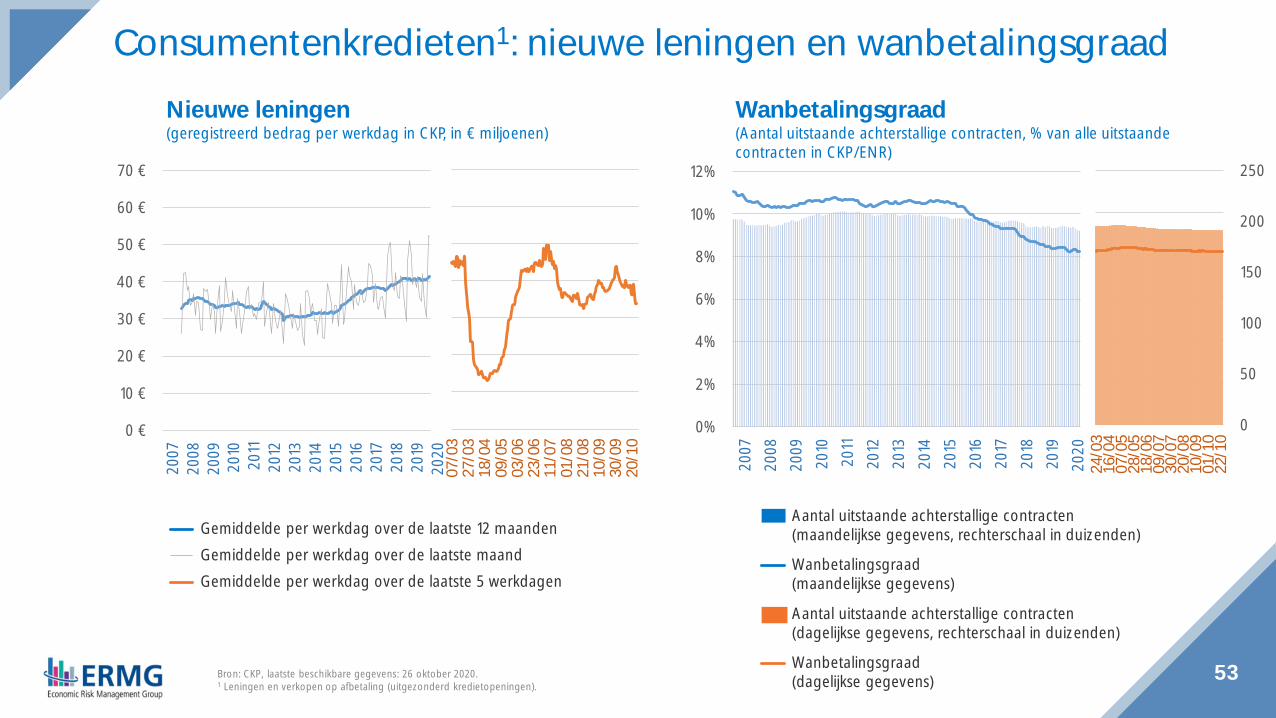

Gemiddelde per werkdag over de laatste 12 maandenGemiddelde per werkdag over de laatste maandGemiddelde per werkdag over de laatste 5 werkdagen

Aantal uitstaande achterstallige contracten(dagelijkse gegevens, rechterschaal in duizenden)

Aantal uitstaande achterstallige contracten(maandelijkse gegevens, rechterschaal in duizenden)

Wanbetalingsgraad(dagelijkse gegevens)

Wanbetalingsgraad(maandelijkse gegevens)

0 €

50 €

100 €

150 €

200 €

250 €

300 €

350 €20

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

2007

/03

28/0

318

/04

09/0

530

/05

20/0

611

/07

01/0

822

/08

12/0

903

/10

24/1

0

-

5

10

15

20

25

30

35

40

45

50

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

05101520253035404550

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

24/0

316

/04

07/0

528

/05

18/0

609

/07

30/0

720

/08

10/0

901

/10

22/1

0

52Bron: Centrale voor Kredieten aan Particulieren (CKP), laatste beschikbare gegevens: 21 oktober 2020..1 De cijfers meten het totaal aantal geregistreerde moratoria in CKP, dus exclusief de aangevraagde moratoria waarvoor de verwerking nog loopt en de verleende moratoria die nog geregistreerd

moeten worden in CKP.2 Het resterend uitstaand kredietbedrag is niet beschikbaar in CKP.

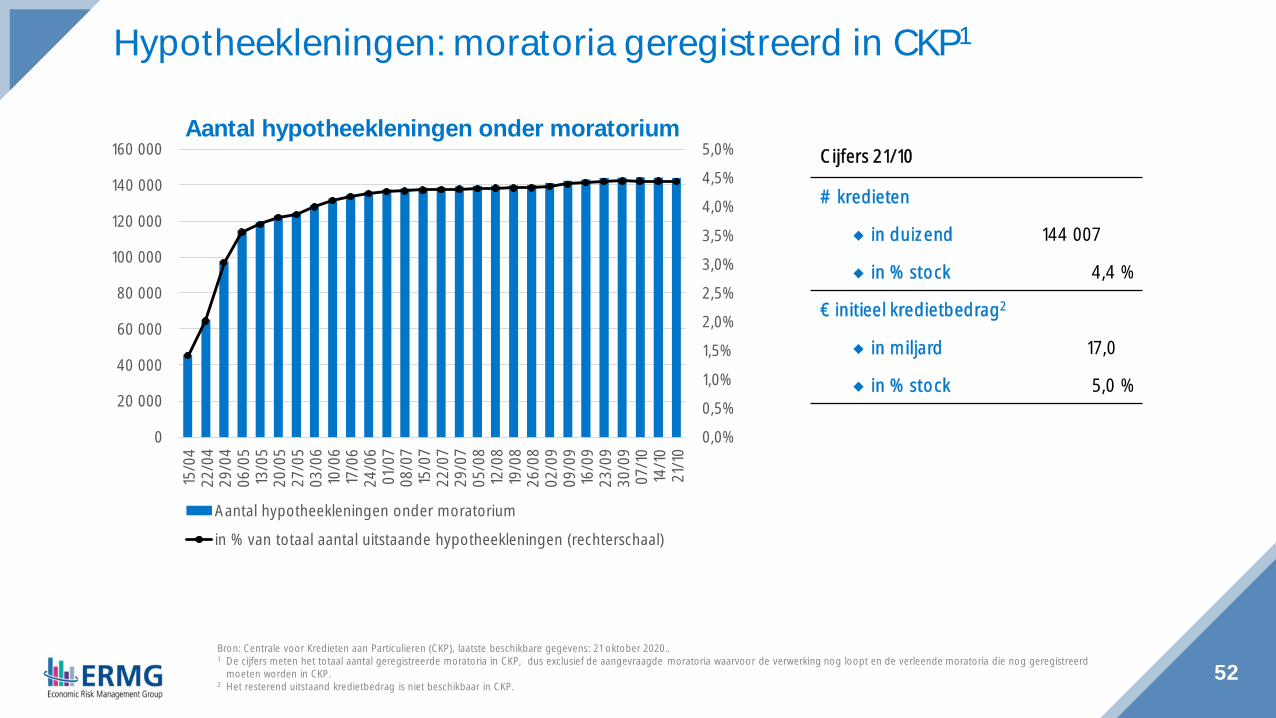

Aantal hypotheekleningen onder moratorium

Hypotheekleningen: moratoria geregistreerd in CKP1

Cijfers 21/10

# kredieten

in duizend 144 007

in % stock 4,4 %

€ initieel kredietbedrag2

in miljard 17,0

in % stock 5,0 %

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

15/0

422

/04

29/0

406

/05

13/0

520

/05

27/0

503

/06

10/0

617

/06

24/0

601

/07

08/0

715

/07

22/0

729

/07

05/0

812

/08

19/0

826

/08

02/0

909

/09

16/0

923

/09

30/0

907

/10

14/1

021

/10

Aantal hypotheekleningen onder moratorium

in % van totaal aantal uitstaande hypotheekleningen (rechterschaal)

53Bron: CKP, laatste beschikbare gegevens: 26 oktober 2020.1 Leningen en verkopen op afbetaling (uitgezonderd kredietopeningen).

Wanbetalingsgraad(Aantal uitstaande achterstallige contracten, % van alle uitstaandecontracten in CKP/ENR)

Nieuwe leningen(geregistreerd bedrag per werkdag in CKP, in € miljoenen)

Consumentenkredieten1: nieuwe leningen en wanbetalingsgraad

Gemiddelde per werkdag over de laatste 12 maandenGemiddelde per werkdag over de laatste maandGemiddelde per werkdag over de laatste 5 werkdagen

Aantal uitstaande achterstallige contracten(dagelijkse gegevens, rechterschaal in duizenden)

Aantal uitstaande achterstallige contracten(maandelijkse gegevens, rechterschaal in duizenden)

Wanbetalingsgraad(dagelijkse gegevens)

Wanbetalingsgraad(maandelijkse gegevens)

0 €

10 €

20 €

30 €

40 €

50 €

60 €

70 €20

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

200

50.00 0

10 0.000

15 0.000

200.0 00

250.0 00

0%

2%

4%

6%

8%

10%

12%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

07/0

327

/03

18/0

409

/05

03/0

623

/06

11/0

701

/08

21/0

810

/09

30/0

920

/10

0

50

100

150

200

250

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

24/0

316

/04

07/0

528

/05

18/0

609

/07

30/0

720

/08

10/0

901

/10

22/1

0

54Bron: CKP, laatste beschikbare gegevens: 21 oktober 20201 De cijfers meten het totaal aantal geregistreerde moratoria in CKP, dus exclusief de aangevraagde moratoria waarvoor de verwerking nog loopt en de verleende moratoria die nog geregistreerd

moeten worden in CKP.2 Het resterend uitstaand kredietbedrag is niet beschikbaar in CKP.

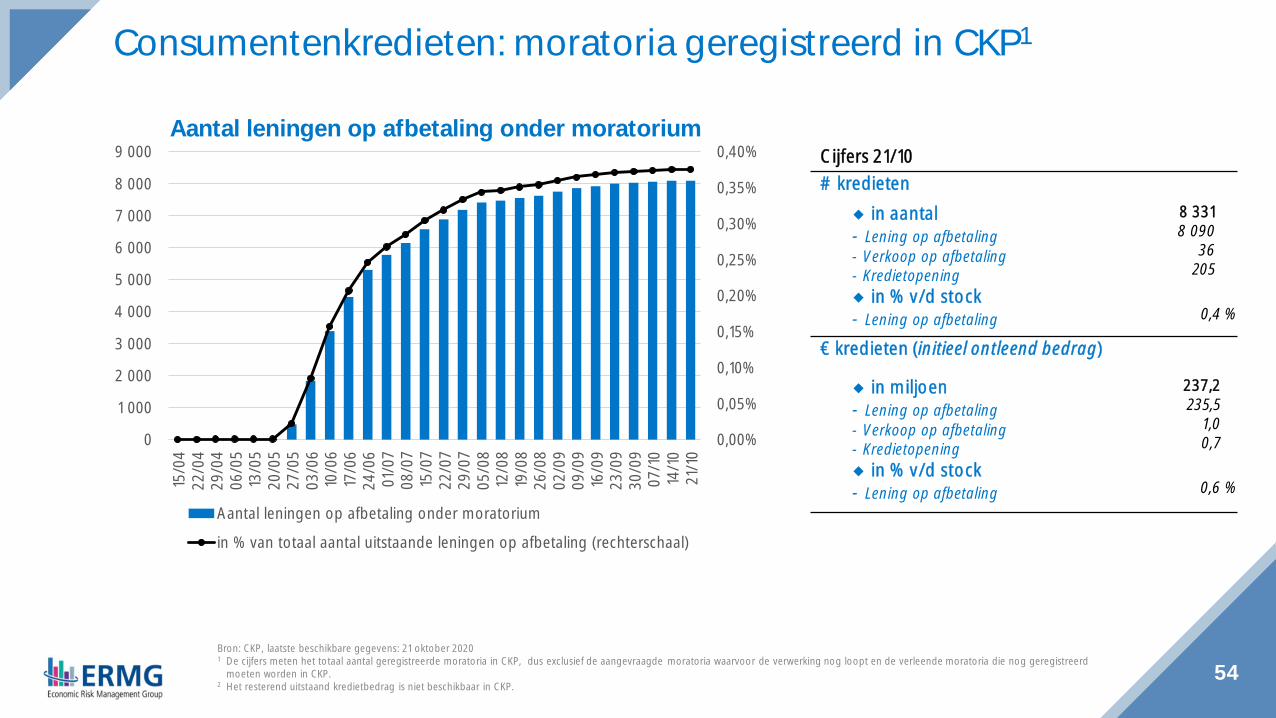

Aantal leningen op afbetaling onder moratorium

Consumentenkredieten: moratoria geregistreerd in CKP1

Cijfers 21/10# kredieten

in aantal- Lening op afbetaling- Verkoop op afbetaling- Kredietopening

8 3318 090

36205

in % v/d stock- Lening op afbetaling 0,4 %

€ kredieten (initieel ontleend bedrag)

in miljoen- Lening op afbetaling- Verkoop op afbetaling- Kredietopening

237,2235,5

1,00,7

in % v/d stock- Lening op afbetaling 0,6 %

0,00%

0,05%

0,10%

0,15%

0,20%

0,25%

0,30%

0,35%

0,40%

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 00015

/04

22/0

429

/04

06/0

513

/05

20/0

527

/05

03/0

610

/06

17/0

624

/06

01/0

708

/07

15/0

722

/07

29/0

705

/08

12/0

819

/08

26/0

802

/09

09/0

916

/09

23/0

930

/09

07/1

014

/10

21/1

0

Aantal leningen op afbetaling onder moratorium

in % van totaal aantal uitstaande leningen op afbetaling (rechterschaal)

55Bron: Febelfin, laatste beschikbare gegevens: 5 oktober 2020.

Betalingsachterstand (1-30 dagen) op hypothecaire leningen en consumentenleningen(wekelijkse gegevens)

Achterstanden bij leningen aan huishoudens stabiel sinds juni

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%13

/4

20/4

27/4 4/5

11/5

18/5

25/5 1/6

8/6

15/6

22/6

29/6 6/7

13/7

20/7

27/7 3/8

10/8

17/8

24/8

31/8 7/9

14/9

21/9

5/10

Hypothecaire leningen Consumentenkredieten

56

Credit indicatorscorporates

57Sources: ECB, NBB.

Impact of the COVID-19 crisis on lending to non-financialcorporations (NFCs)◆ Credit developments: (see next slides)

◇ While annual NFC growth of utilised loans had accelerated in March and April (in large part due todrawdowns of credit lines by multinationals), it has slowed since May.

◇ The annual growth rate of authorised (granted) credit is comparable to that observed before the pandemic◇ Monthly growth rates of utilised and authorised were negative in June◇ Loan arrears have been stable since May◇ Small or medium-sized enterprises (SMEs) have larger proportions of loans in moratorium than larger firms

◆ According to the July 2020 Bank lending survey:◇ Demand for loans from Belgian enterprises in 2020Q2 was driven by liquidity needs, but also curbed by a

decline in fixed investment◇ Slight tightening in credit standards prompted by higher risk perception and lower risk tolerance

58Sources: ECB, NBB.

Firms perceived less favorable credit conditions◆ Belgian firms reported for the second time a deterioration of their credit conditions in 2020Q2

◇ Deterioration in the assessment of the general credit conditions by firms- In all branches of activity and all categories of firms irrespective of size- From 2020, the balance of the opinions (favorable vs unfavorable) is below the historical mean

◇ Small deterioration with respect to 2020Q1 regarding requirements for collateral, costs other thaninterest rates and level of interest rates(source: NBB survey on credit conditions)

◆ SMEs feared a significant impact on bank loan availability in 2020Q2◇ No significant changes regarding obstacles impeding access to bank financing between October 2019

and March 2020- Proportion of SMEs not applying for bank credit because of possible rejection, or applying for a loan but only

receiving a limited part of the amount requested, refusing credit because the cost was too high, or having theirapplication rejected = 5,2 % (against 5,9 % on average in 2017-2019)

◇ But SMEs expected a sharp deterioration in availability of bank loans over the next six months(April-September 2020)- Widespread across sectors

(source: SAFE survey, conducted between 2 March and 8 April 2020.)

59

Non-financial corporations

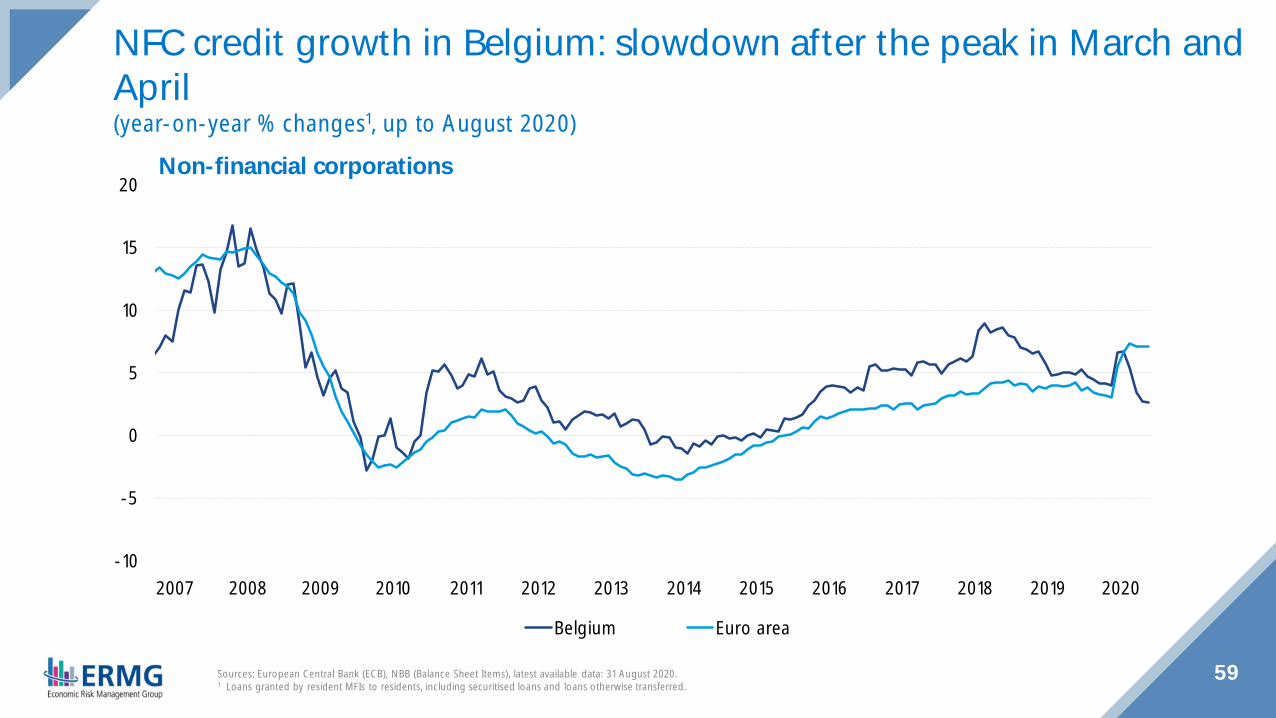

NFC credit growth in Belgium: slowdown after the peak in March andApril(year-on-year % changes1, up to August 2020)

-10

-5

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Belgium Euro area

Sources: European Central Bank (ECB), NBB (Balance Sheet Items), latest available data: 31 August 2020.1 Loans granted by resident MFIs to residents, including securitised loans and loans otherwise transferred.

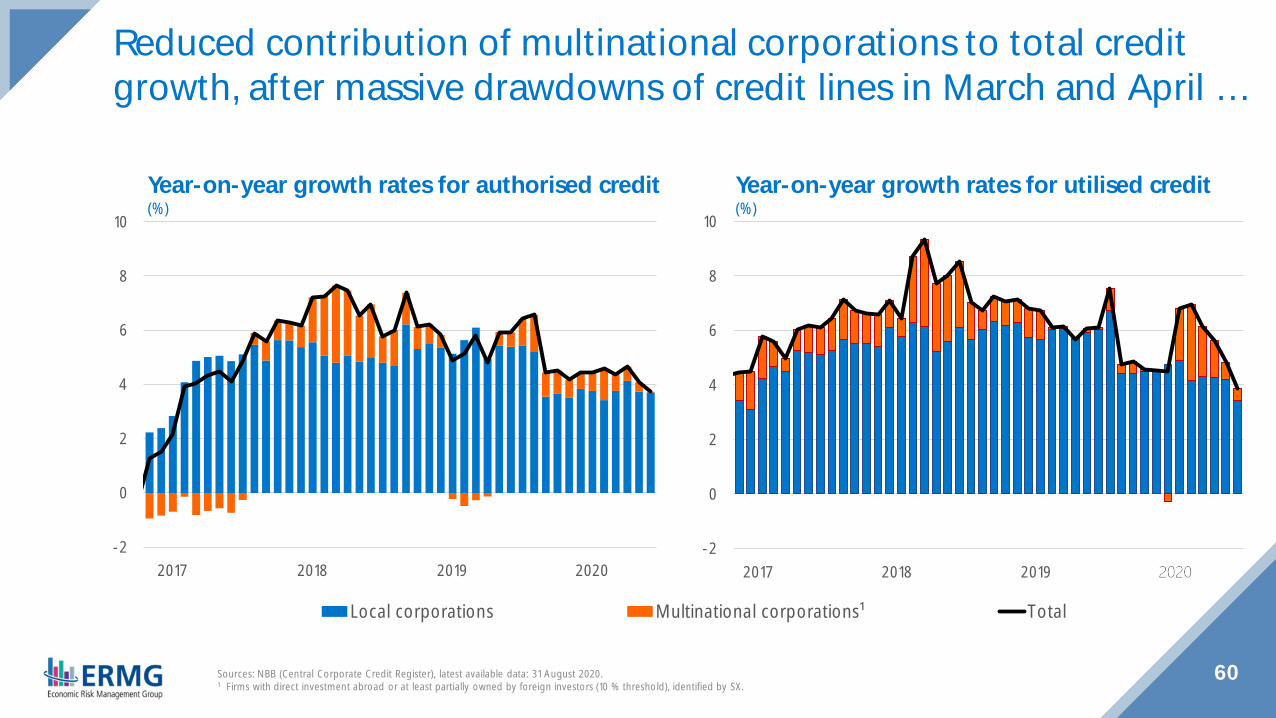

Reduced contribution of multinational corporations to total creditgrowth, after massive drawdowns of credit lines in March and April …

-2

0

2

4

6

8

10

2017 2018 2019 2020

Local corporations Multinational corporations¹ Total

-2

0

2

4

6

8

10

2017 2018 2019 2020

60Sources: NBB (Central Corporate Credit Register), latest available data: 31 August 2020.1 Firms with direct investment abroad or at least partially owned by foreign investors (10 % threshold), identified by SX.

Year-on-year growth rates for utilised credit(%)

Year-on-year growth rates for authorised credit(%)

-2

0

2

4

6

8

10

2017 2018 2019 2020

Up to one year (or undefined) One to two years Two to five years Over five years Total

-2

0

2

4

6

8

10

2017 2018 2019 2020

61Source: NBB (Central Corporate Credit Register), latest available data: 31 August 2020.

Decomposition of YoY used corporate creditgrowth by maturity(%)

… which also translates into a lower contribution of short-term loans

Decomposition of YoY authorized corporatecredit growth by maturity(%)

-2

-1

0

1

2

3

2020m3 2020m4 2020m5 2020m6 2020m7 2020m8

utilised authorised

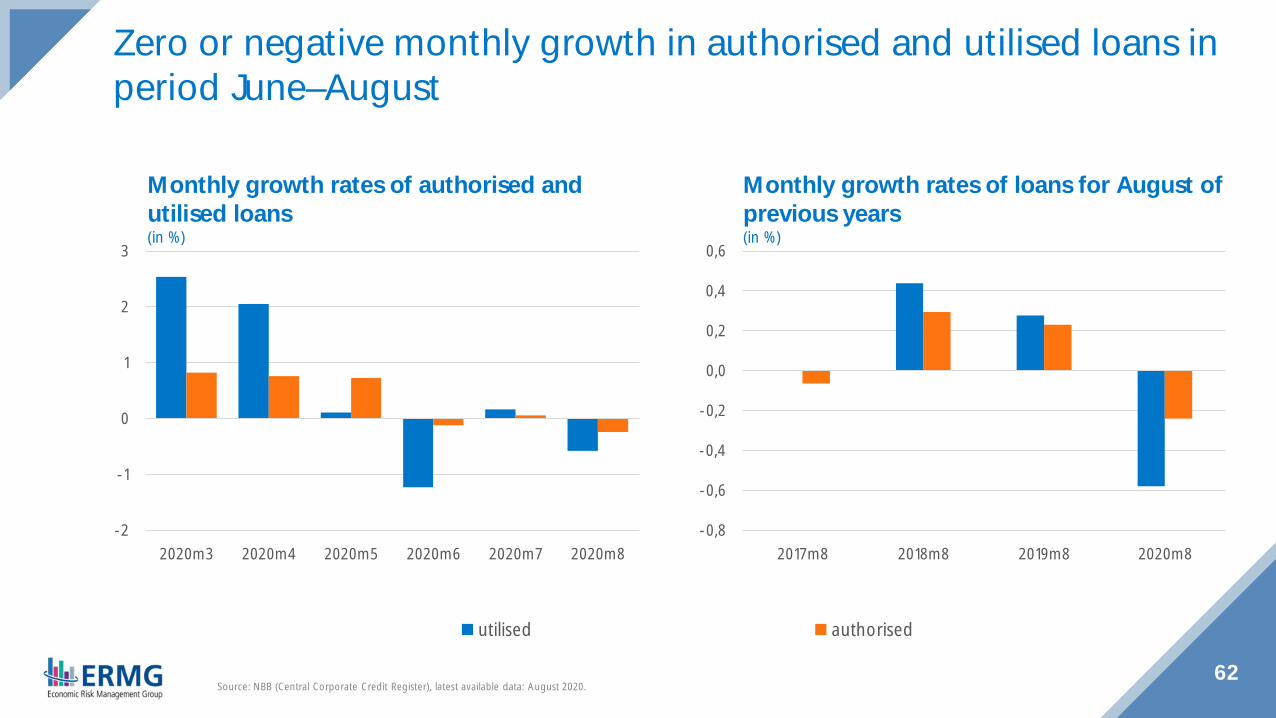

Zero or negative monthly growth in authorised and utilised loans inperiod June–August

62Source: NBB (Central Corporate Credit Register), latest available data: August 2020.

Monthly growth rates of loans for August ofprevious years(in %)

Monthly growth rates of authorised andutilised loans(in %)

-0,8

-0,6

-0,4

-0,2

0,0

0,2

0,4

0,6

2017m8 2018m8 2019m8 2020m8

63Source: NBB (Central Corporate Credit Register), latest available data: August 2020.Note: Sectors are ordered based on the initial fall in sales due to the crisis (greater declines from right to left). “Other” contains all other sectors in the economy.

March-August growth rates of utilised loans(in %)

March-August growth rates of authorised loans(in %)

March–August growth in authorised and utilised loans is belowhistorical averages for many vulnerable sectors

- 4- 2 0 2 4 6 8

10 12

Arts,

ent

erta

inm

ent

and

recr

eatio

n

Hore

ca

Who

lesa

le a

ndre

tail t

rade

Real

esta

te a

ctivi

ties

Cons

truct

ion

Man

ufac

turin

g

Tran

spor

tatio

nan

d sto

rage

Info

rmat

ion

and

com

mun

icatio

n

Supp

ort s

ervic

es

Agric

ultu

re, f

ores

try

and

fishi

ngFin

ancia

l and

insu

ranc

eac

tiviti

es

Oth

er

Mar-Aug 2020 4-y average Mar-Aug

-4-202468

1012

Arts,

ent

erta

inm

ent

and

recr

eatio

n

Hore

ca

Who

lesa

le a

ndre

tail t

rade

Real

esta

te a

ctivi

ties

Cons

truct

ion

Man

ufac

turin

g

Tran

spor

tatio

nan

d sto

rage

Info

rmat

ion

and

com

mun

icatio

n

Supp

ort s

ervic

es

Agric

ultu

re, f

ores

try

and

fishi

ngFin

ancia

l and

insu

ranc

eac

tiviti

es

Oth

er

60

98

57

92

47

84

20

91

48

89

0

10

20

30

40

50

60

70

80

90

100

ShortTerm

LongTerm

ShortTerm

LongTerm

ShortTerm

LongTerm

ShortTerm

LongTerm

ShortTerm

LongTerm

Self-employed(1)

SMEs(2)

Corporates(3)

Public(4)

Sum of(1) to (4)= total

64

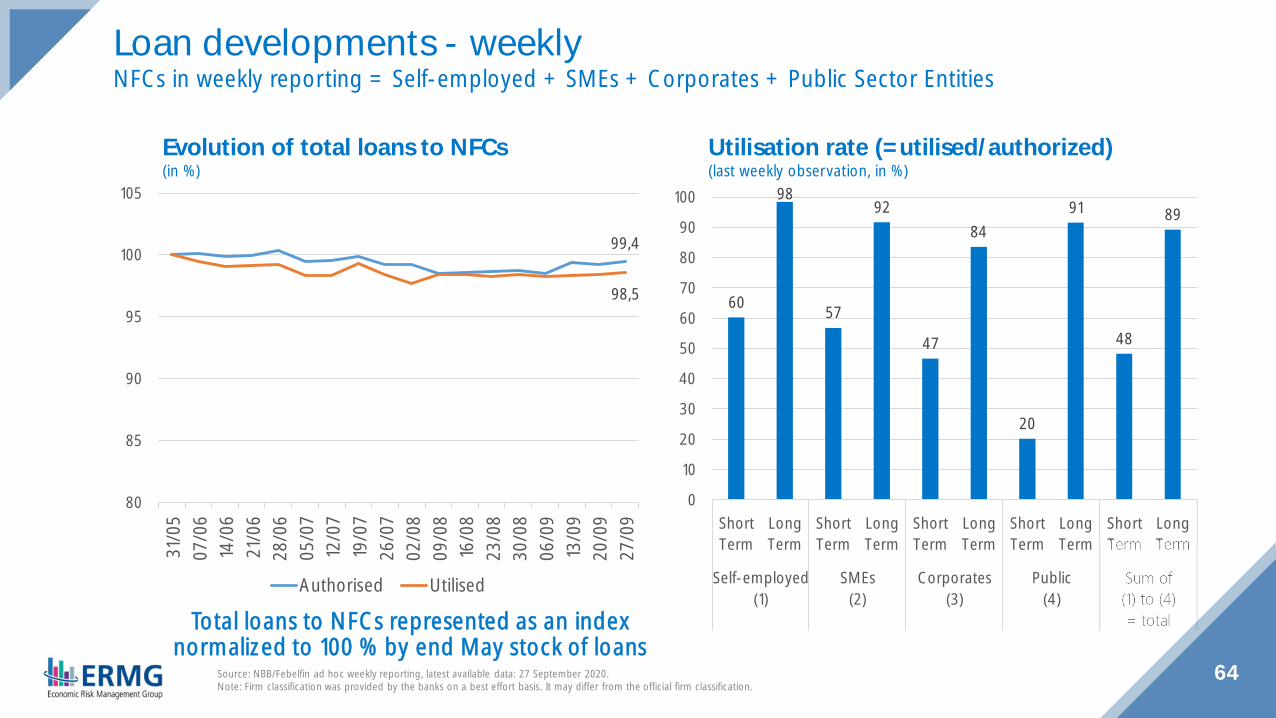

Loan developments - weeklyNFCs in weekly reporting = Self-employed + SMEs + Corporates + Public Sector Entities

Utilisation rate (=utilised/authorized)(last weekly observation, in %)

Evolution of total loans to NFCs(in %)

99,4

98,5

80

85

90

95

100

10531

/05

07/0

614

/06

21/0

628

/06

05/0

712

/07

19/0

726

/07

02/0

809

/08

16/0

823

/08

30/0

806

/09

13/0

920

/09

27/0

9

Authorised Utilised

Total loans to NFCs represented as an indexnormalized to 100 % by end May stock of loans

Source: NBB/Febelfin ad hoc weekly reporting, latest available data: 27 September 2020.Note: Firm classification was provided by the banks on a best effort basis. It may differ from the official firm classification.

102,0

101,0

90

95

100

105

31/0

507

/06

14/0

621

/06

28/0

605

/07

12/0

719

/07

26/0

702

/08

09/0

816

/08

23/0

830

/08

06/0

913

/09

20/0

927

/09

97,2

95,2

9092949698

100102

31/0

507

/06

14/0

621

/06

28/0

605

/07

12/0

719

/07

26/0

702

/08

09/0

816

/08

23/0

830

/08

06/0

913

/09

20/0

927

/09

Authorised Utilised

100,6

100,8

9092949698

100102

31/0

507

/06

14/0

621

/06

28/0

605

/07

12/0

719

/07

26/0

702

/08

09/0

816

/08

23/0

830

/08

06/0

913

/09

20/0

927

/09

Total loans to NFCs represented as an index normalized to 100 % by end May stock of loans65

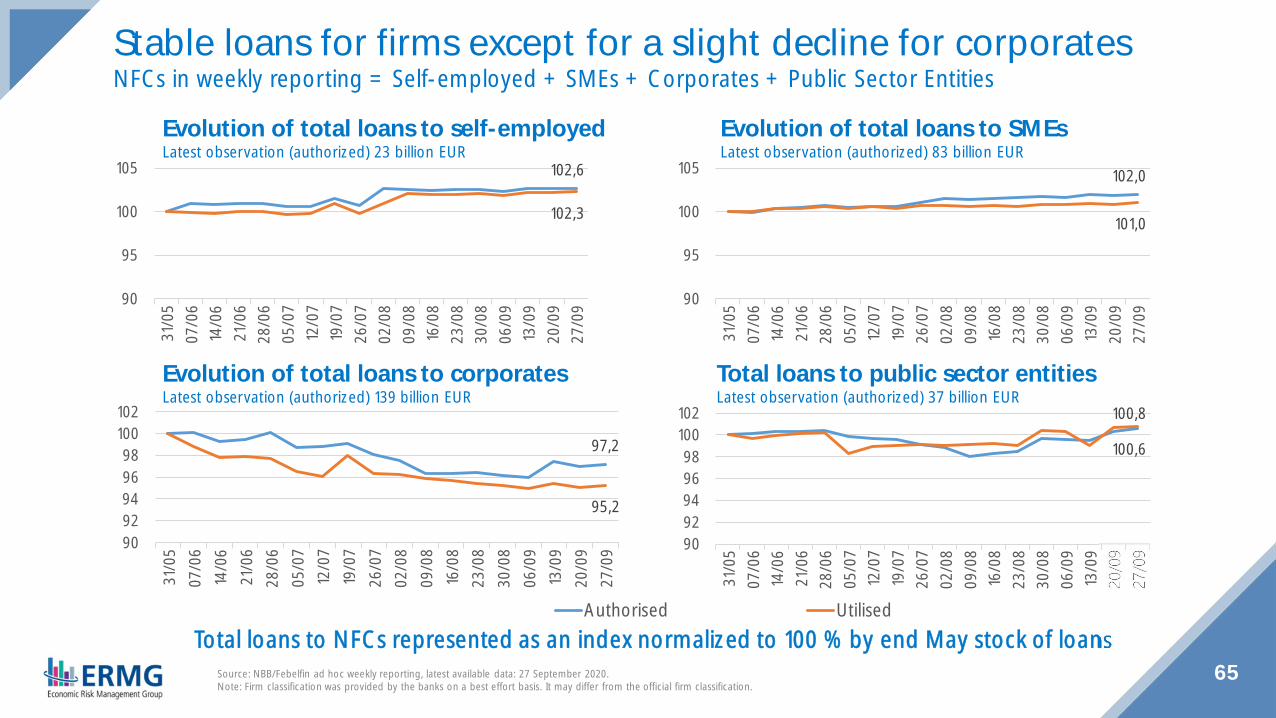

Stable loans for firms except for a slight decline for corporatesNFCs in weekly reporting = Self-employed + SMEs + Corporates + Public Sector Entities

Evolution of total loans to SMEsLatest observation (authorized) 83 billion EUR

Evolution of total loans to self-employedLatest observation (authorized) 23 billion EUR

102,6

102,3

90

95

100

10531

/05

07/0

614

/06

21/0

628

/06

05/0

712

/07

19/0

726

/07

02/0

809

/08

16/0

823

/08

30/0

806

/09

13/0

920

/09

27/0

9

Total loans to public sector entitiesLatest observation (authorized) 37 billion EUR

Evolution of total loans to corporatesLatest observation (authorized) 139 billion EUR

Source: NBB/Febelfin ad hoc weekly reporting, latest available data: 27 September 2020.Note: Firm classification was provided by the banks on a best effort basis. It may differ from the official firm classification.

0

200

400

600

800

1000

1200

1400

1600

3/05

10/0

517

/05

24/0

531

/05

7/06

14/0

621

/06

28/0

65/

0712

/07

19/0

726

/07

2/08

9/08

16/0

823

/08

30/0

86/

0913

/09

20/0

927

/09

Self-employed SMEs Corporates Public

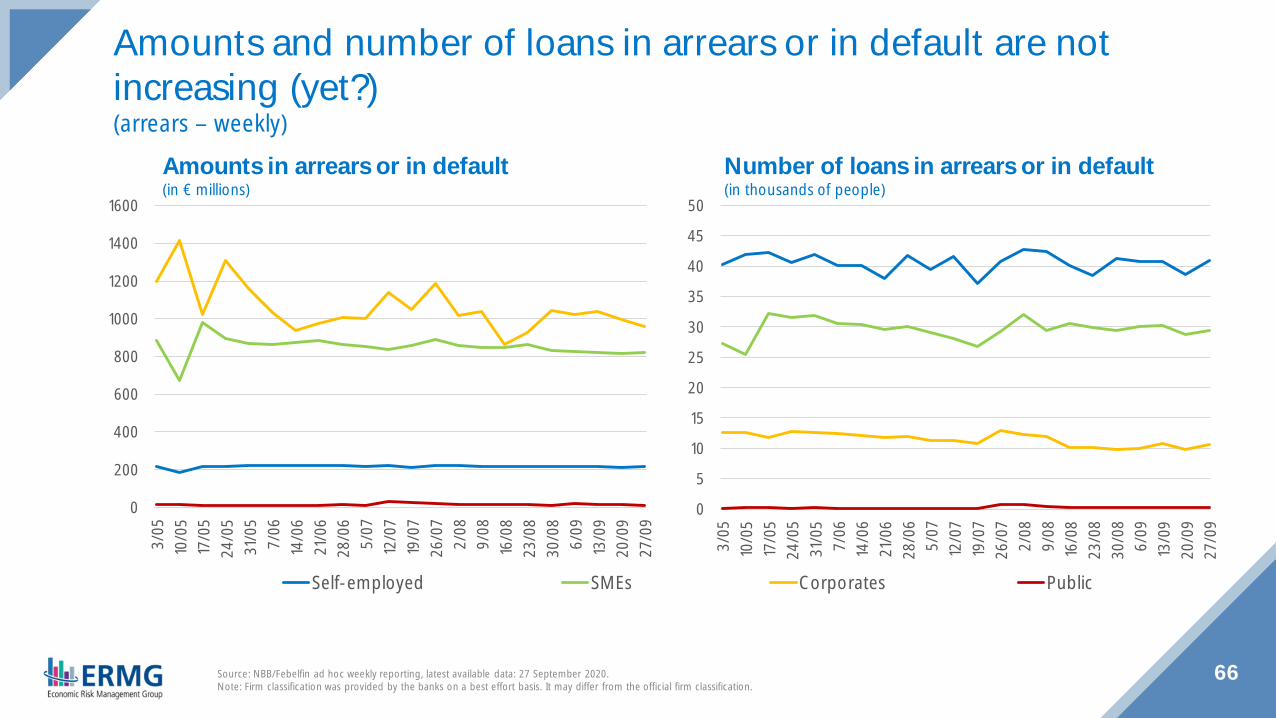

66

Amounts and number of loans in arrears or in default are notincreasing (yet?)(arrears – weekly)

Number of loans in arrears or in default(in thousands of people)

Amounts in arrears or in default(in € millions)

0

5

10

15

20

25

30

35

40

45

50

3/05

10/0

517

/05

24/0

531

/05

7/06

14/0

621

/06

28/0

65/

0712

/07

19/0

726

/07

2/08

9/08

16/0

823

/08

30/0

86/

0913

/09

20/0

927

/09

Source: NBB/Febelfin ad hoc weekly reporting, latest available data: 27 September 2020.Note: Firm classification was provided by the banks on a best effort basis. It may differ from the official firm classification.

4%

54%

39%

3%

Self-employed SMEs Corporates Public

8%

30%

49%

13%

67

Total loan amounts by type of counterpartyLoan amounts in moratorium by type of counterparty

SMEs are the main beneficiaries of moratorium relative to their shareof total loans(moratorium – weekly)

Source: NBB/Febelfin ad hoc weekly reporting, latest available data: 27 September 2020.Note: Firm classification was provided by the banks on a best effort basis. It may differ from the official firm classification.

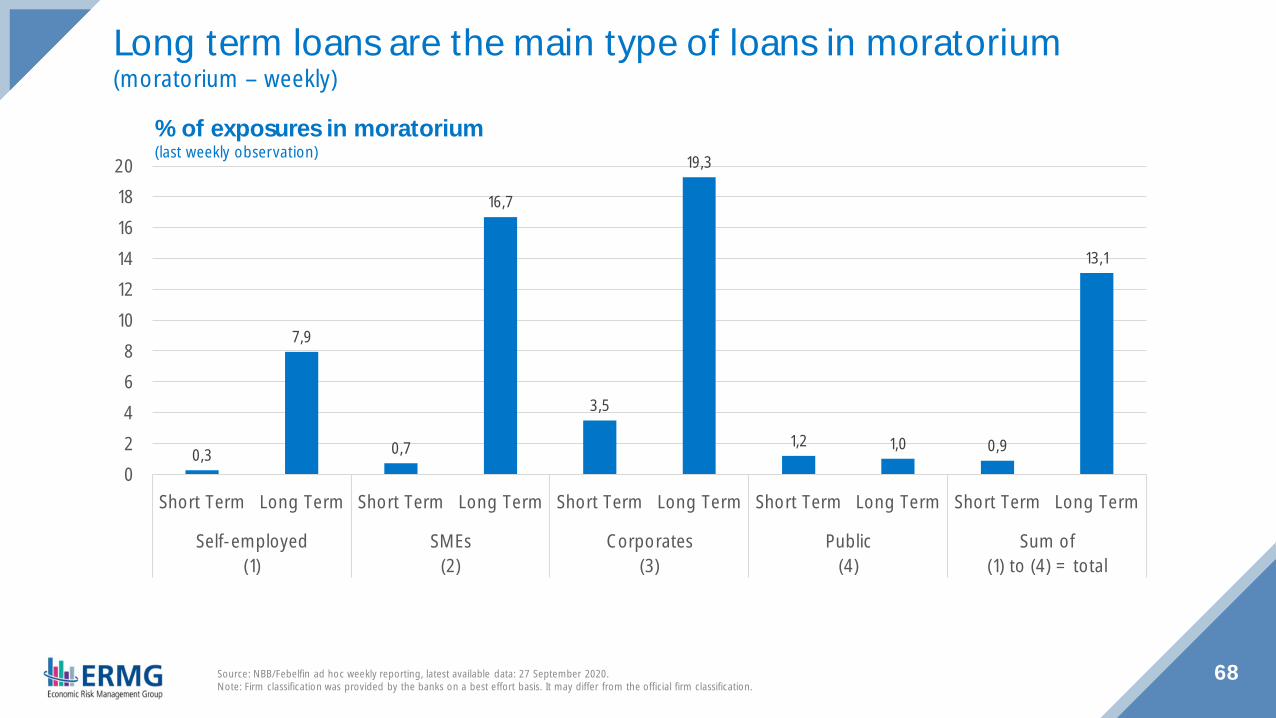

68

0,3

7,9

0,7

16,7

3,5

19,3

1,2 1,0 0,9

13,1

02468

101214161820

Short Term Long Term Short Term Long Term Short Term Long Term Short Term Long Term Short Term Long Term

Self-employed(1)

SMEs(2)

Corporates(3)

Public(4)

Sum of(1) to (4) = total

Long term loans are the main type of loans in moratorium(moratorium – weekly)

% of exposures in moratorium(last weekly observation)

Source: NBB/Febelfin ad hoc weekly reporting, latest available data: 27 September 2020.Note: Firm classification was provided by the banks on a best effort basis. It may differ from the official firm classification.

69

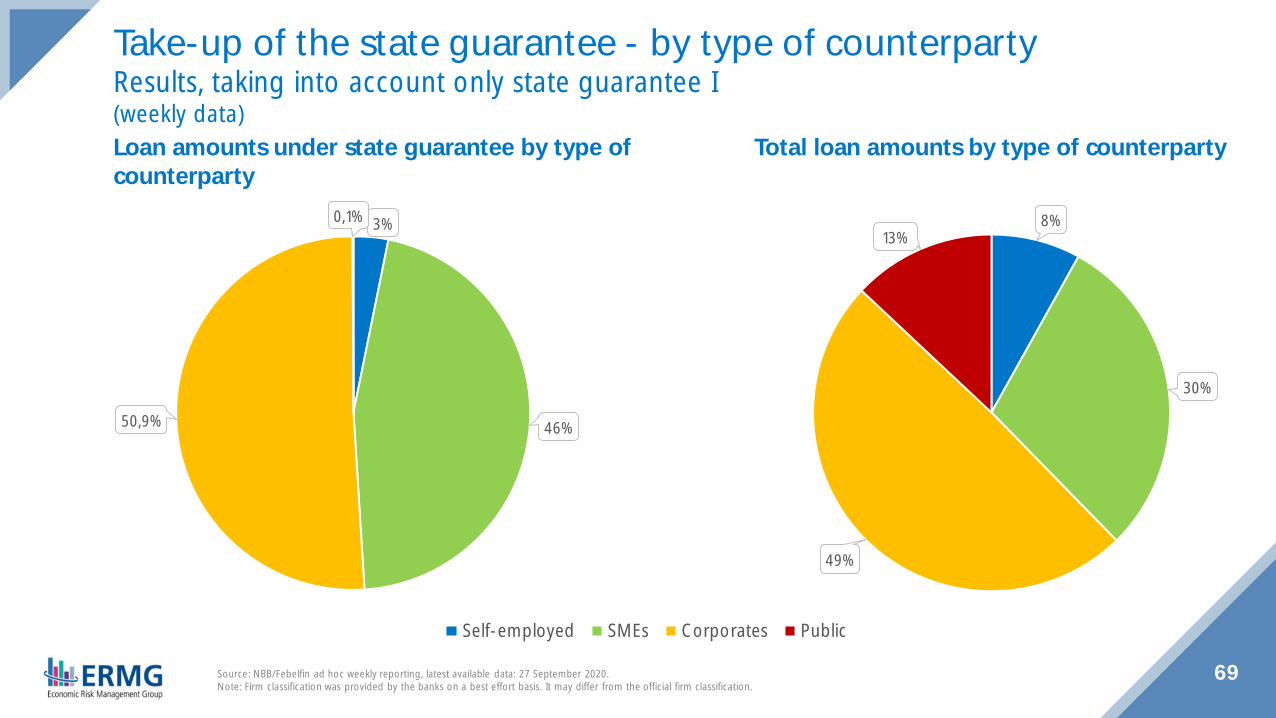

Total loan amounts by type of counterpartyLoan amounts under state guarantee by type ofcounterparty

Take-up of the state guarantee - by type of counterpartyResults, taking into account only state guarantee I(weekly data)

3%

46%50,9%

0,1%

Self-employed SMEs Corporates Public

8%

30%

49%

13%

Source: NBB/Febelfin ad hoc weekly reporting, latest available data: 27 September 2020.Note: Firm classification was provided by the banks on a best effort basis. It may differ from the official firm classification.

70

Bankruptcies andnew business registrations

0

100

200

300

400

500

600

700

August 2020 September 2020 Mid-October 2020(current month)

71Source: Statbel, latest available data: 18 October 2020.1 March, April & May: limited activities from business courts. 24 April to 17 June: temporary moratorium on filings for bankruptcy. July & August: judicial summer recess.2 Declaration of bankruptcy by the company court.3 Such as the deferment of payment of social security contributions (until 15 December 2020) and of the annual company contribution (until 31 October 2020).

(# by activity)Bankruptcies(# by region)

Despite a marked growth in September after the summer recess1,the number of bankruptcies2 remains lower than in September 2019... with some supporting measures to enterprises still in place3

Transport & other servicesHotel & restaurantTradeBuildingIndustries & energyAgriculture & fisheries

◆ About 96 % of bankruptcies are within the ‘0 to 9 workers’company size class

0

200

400

600

800

1 000

1 200

1 400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2020 VLA 2020 BRU 2020 WAL 2019 Belgium

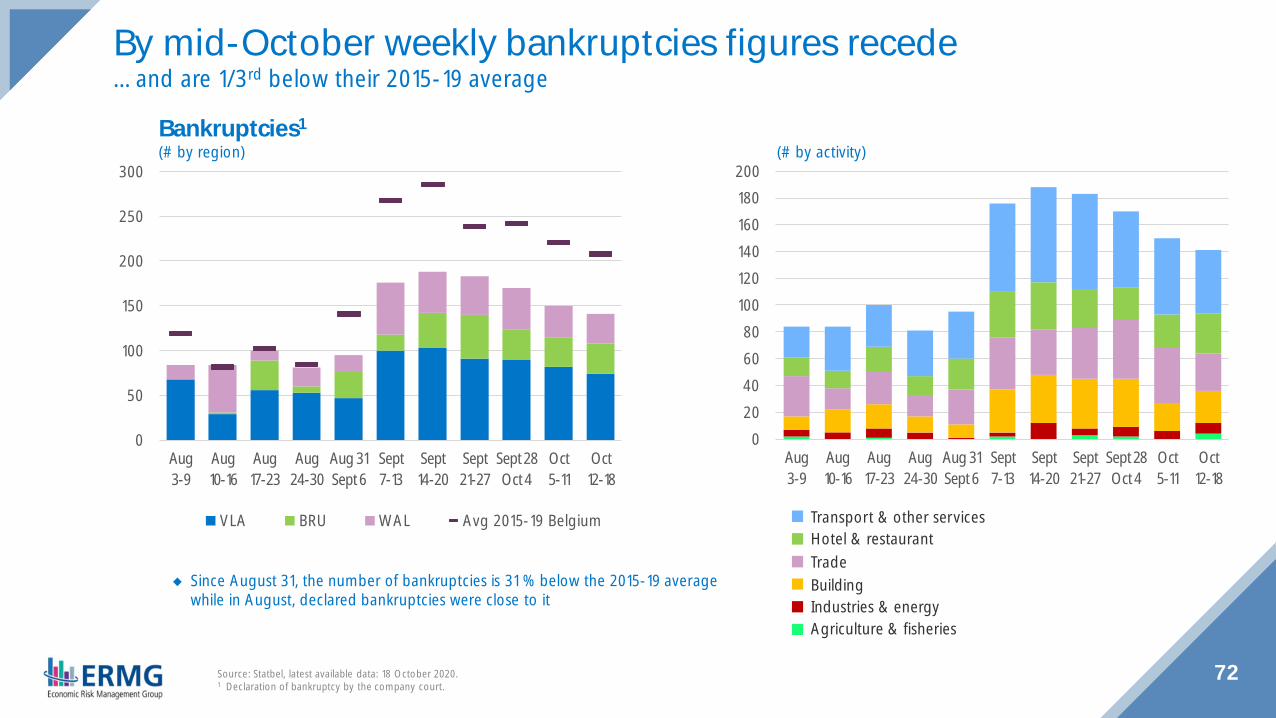

72Source: Statbel, latest available data: 18 October 2020.1 Declaration of bankruptcy by the company court.

(# by activity)Bankruptcies1

(# by region)

By mid-October weekly bankruptcies figures recede… and are 1/3rd below their 2015-19 average

Transport & other servicesHotel & restaurantTradeBuildingIndustries & energyAgriculture & fisheries

0

50

100

150

200

250

300

Aug3-9

Aug10-16

Aug17-23

Aug24-30

Aug 31Sept 6

Sept7-13

Sept14-20

Sept21-27

Sept 28Oct 4

Oct5-11

Oct12-18

VLA BRU WAL Avg 2015-19 Belgium

◆ Since August 31, the number of bankruptcies is 31 % below the 2015-19 averagewhile in August, declared bankruptcies were close to it

020406080

100120140160180200

Aug3-9

Aug10-16

Aug17-23

Aug24-30

Aug 31Sept 6

Sept7-13

Sept14-20

Sept21-27

Sept 28Oct 4

Oct5-11

Oct12-18

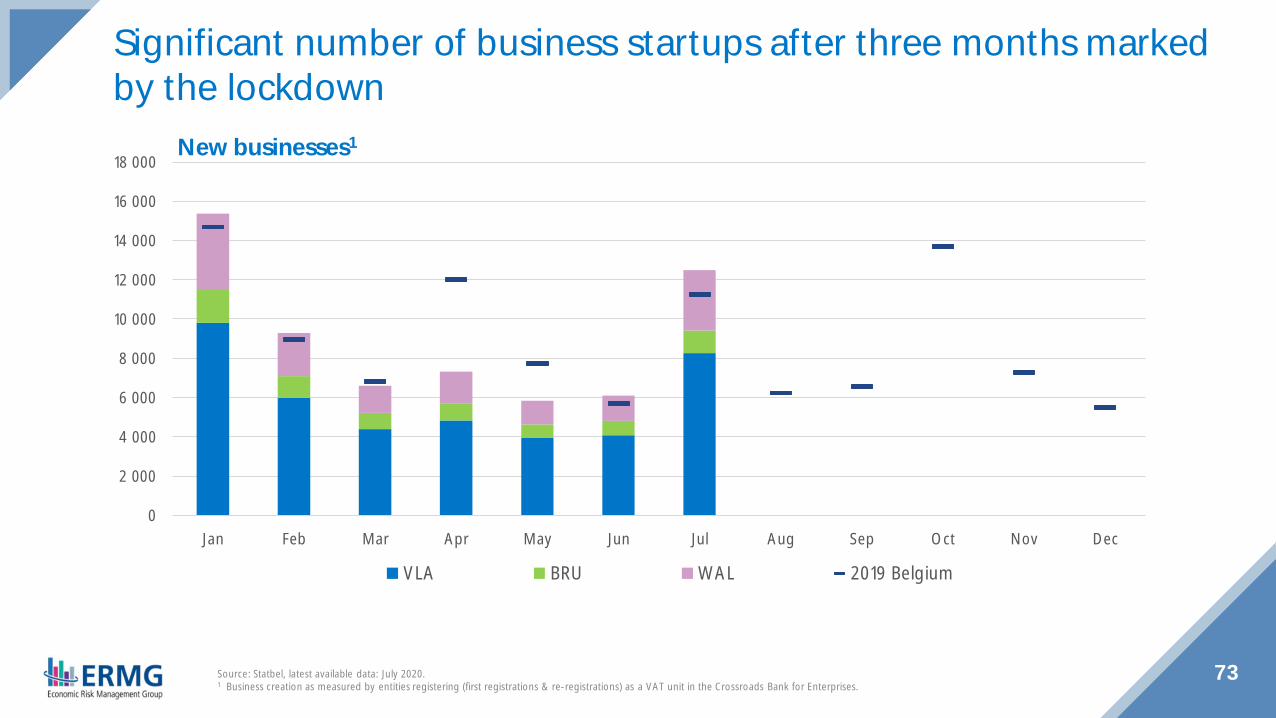

73Source: Statbel, latest available data: July 2020.1 Business creation as measured by entities registering (first registrations & re-registrations) as a VAT unit in the Crossroads Bank for Enterprises.

New businesses1

Significant number of business startups after three months markedby the lockdown

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

VLA BRU WAL 2019 Belgium

74

Financial markets

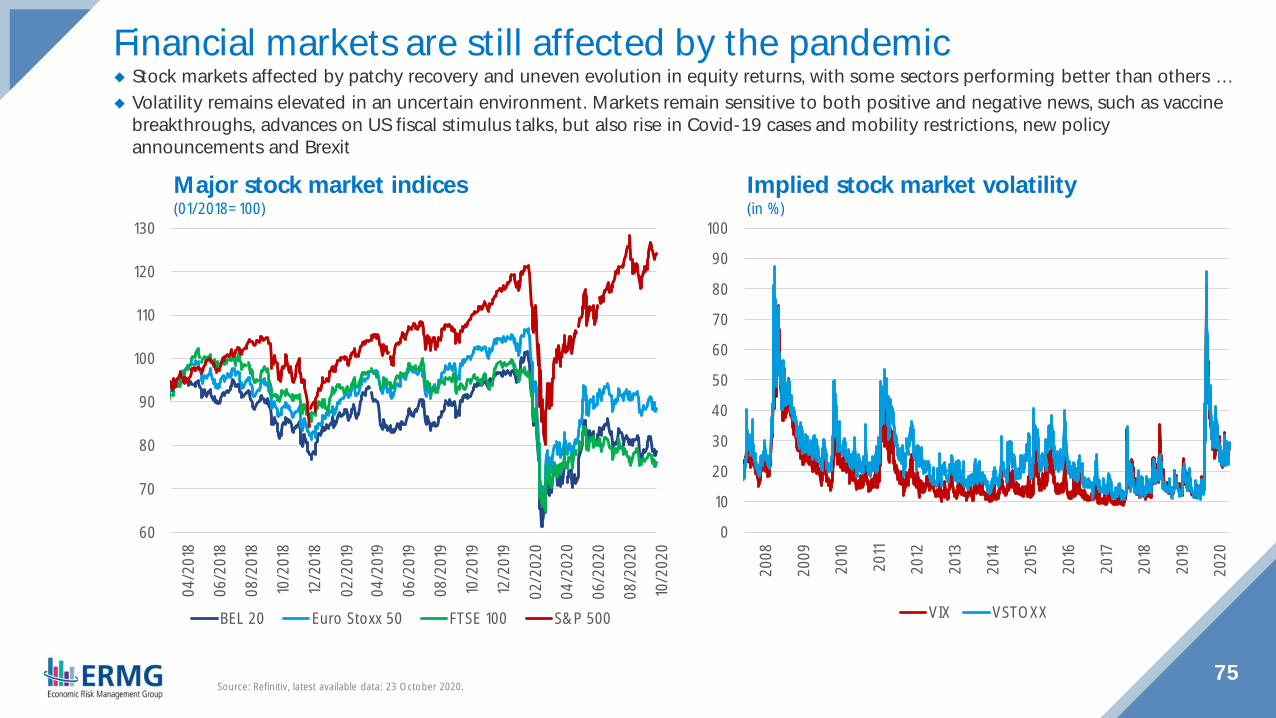

Financial markets are still affected by the pandemic

60

70

80

90

100

110

120

130

04/2

018

06/2

018

08/2

018

10/2

018

12/2

018

02/2

019

04/2

019

06/2

019

08/2

019

10/2

019

12/2

019

02/2

020

04/2

020

06/2

020

08/2

020

10/2

020

BEL 20 Euro Stoxx 50 FTSE 100 S&P 500

◆ Stock markets affected by patchy recovery and uneven evolution in equity returns, with some sectors performing better than others …◆ Volatility remains elevated in an uncertain environment. Markets remain sensitive to both positive and negative news, such as vaccine

breakthroughs, advances on US fiscal stimulus talks, but also rise in Covid-19 cases and mobility restrictions, new policyannouncements and Brexit

75Source: Refinitiv, latest available data: 23 October 2020.

Major stock market indices(01/2018=100)

Implied stock market volatility(in %)

0

10

20

30

40

50

60

70

80

90

100

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

VIX VSTOXX

-80-60-40-20

020406080

100120140160

07/2

019

08/2

019

09/2

019

10/2

019

11/2

019

12/2

019

01/2

020

02/2

020

03/2

020

04/2

020

05/2

020

06/2

020

07/2

020

08/2

020

09/2

020

10/2

020

Crude Oil WTI Metals index

Copper Gold

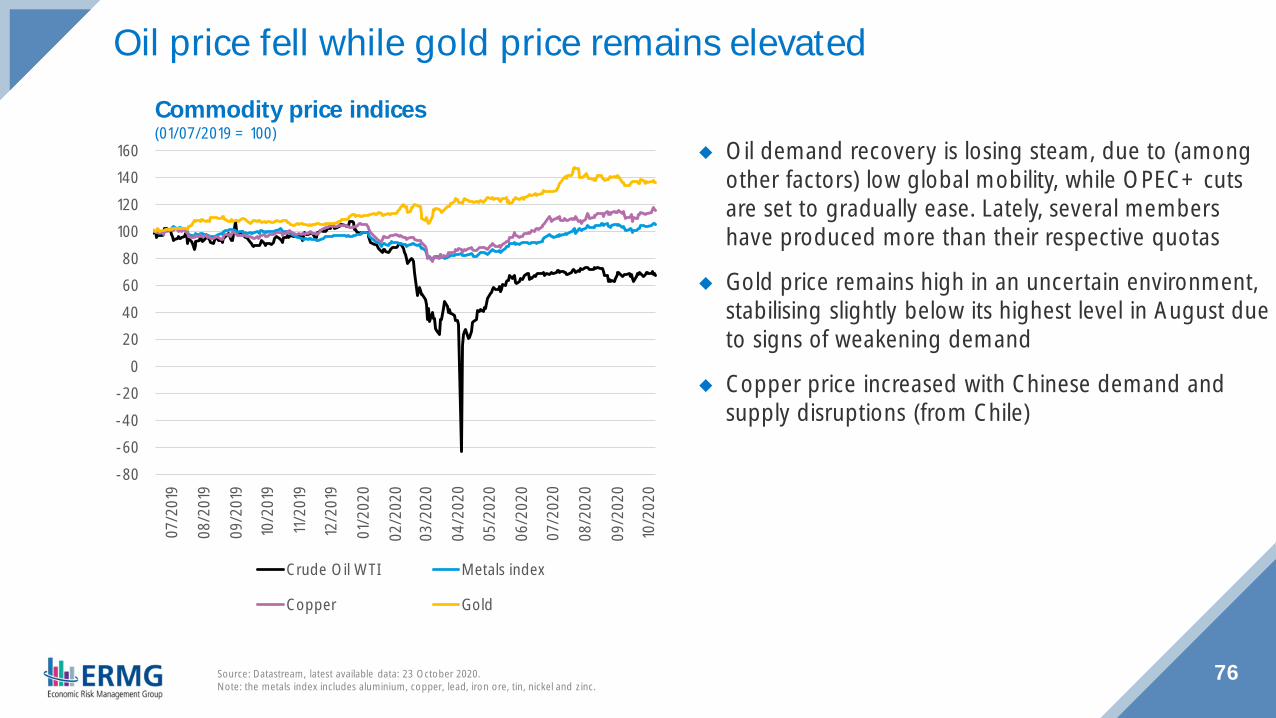

◆ Oil demand recovery is losing steam, due to (amongother factors) low global mobility, while OPEC+ cutsare set to gradually ease. Lately, several membershave produced more than their respective quotas

◆ Gold price remains high in an uncertain environment,stabilising slightly below its highest level in August dueto signs of weakening demand

◆ Copper price increased with Chinese demand andsupply disruptions (from Chile)

76Source: Datastream, latest available data: 23 October 2020.Note: the metals index includes aluminium, copper, lead, iron ore, tin, nickel and zinc.

Commodity price indices(01/07/2019 = 100)

Oil price fell while gold price remains elevated

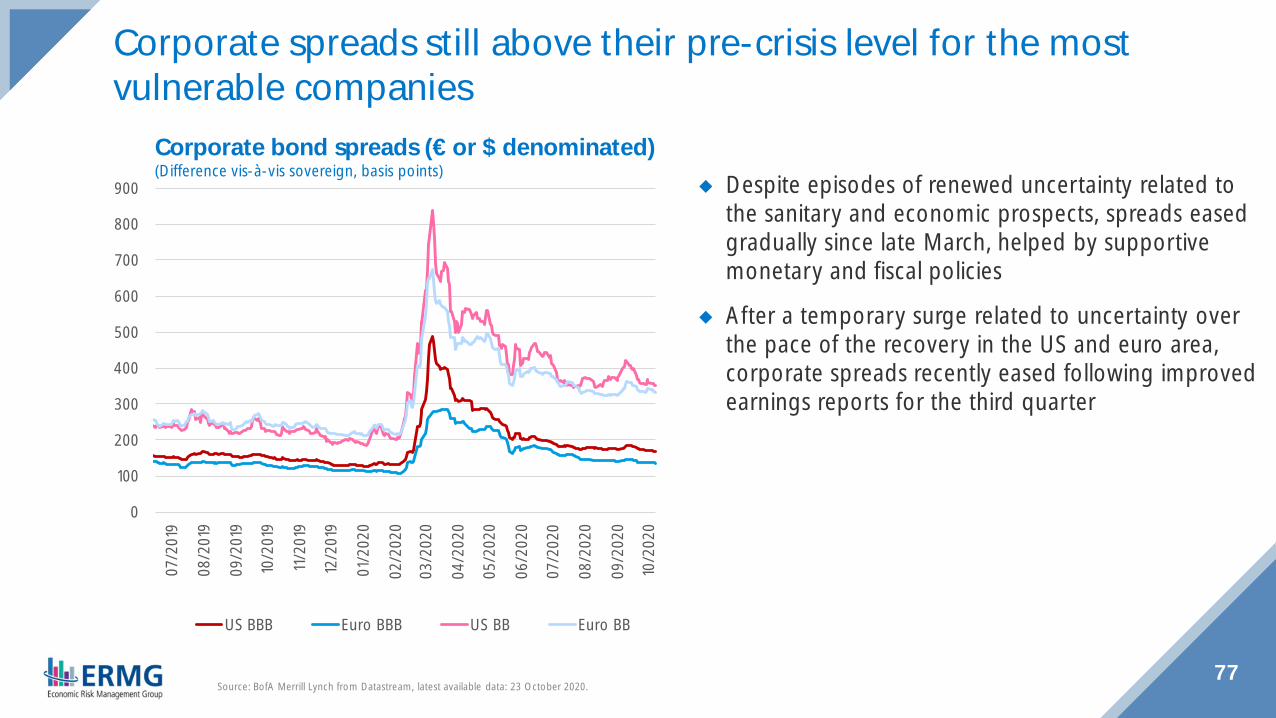

Corporate spreads still above their pre-crisis level for the mostvulnerable companies

0

100

200

300

400

500

600

700

800

90007

/201

9

08/2

019

09/2

019

10/2

019

11/2

019

12/2

019

01/2

020

02/2

020

03/2

020

04/2

020

05/2

020

06/2

020

07/2

020

08/2

020

09/2

020

10/2

020

US BBB Euro BBB US BB Euro BB

◆ Despite episodes of renewed uncertainty related tothe sanitary and economic prospects, spreads easedgradually since late March, helped by supportivemonetary and fiscal policies

◆ After a temporary surge related to uncertainty overthe pace of the recovery in the US and euro area,corporate spreads recently eased following improvedearnings reports for the third quarter

77Source: BofA Merrill Lynch from Datastream, latest available data: 23 October 2020.

Corporate bond spreads (€ or $ denominated)(Difference vis-à-vis sovereign, basis points)

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,501

/201

8

03/2

018

05/2

018

07/2

018

09/2

018

11/2

018

01/2

019

03/2

019

05/2

019

07/2

019

09/2

019

11/2

019

01/2

020

03/2

020

05/2

020

07/2

020

09/2

020

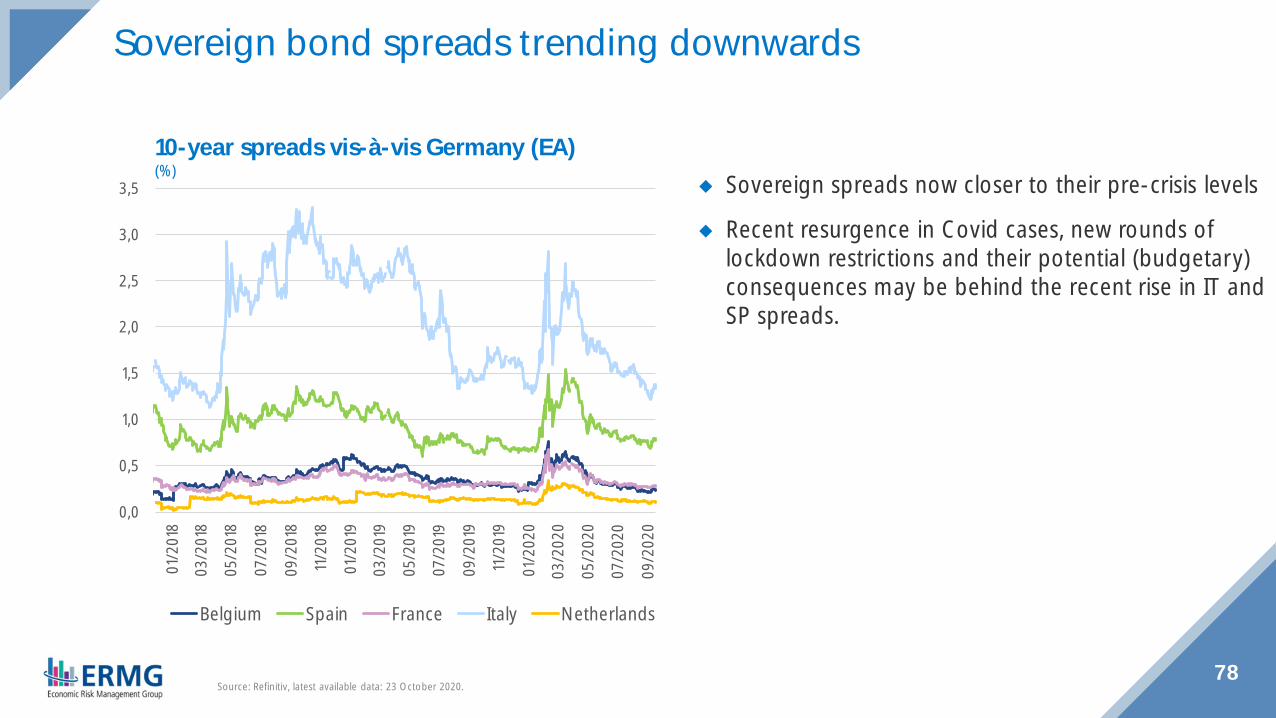

Belgium Spain France Italy Netherlands

Sovereign bond spreads trending downwards

◆ Sovereign spreads now closer to their pre-crisis levels

◆ Recent resurgence in Covid cases, new rounds oflockdown restrictions and their potential (budgetary)consequences may be behind the recent rise in IT andSP spreads.

78Source: Refinitiv, latest available data: 23 October 2020.

10-year spreads vis-à-vis Germany (EA)(%)

79

International outlook

80

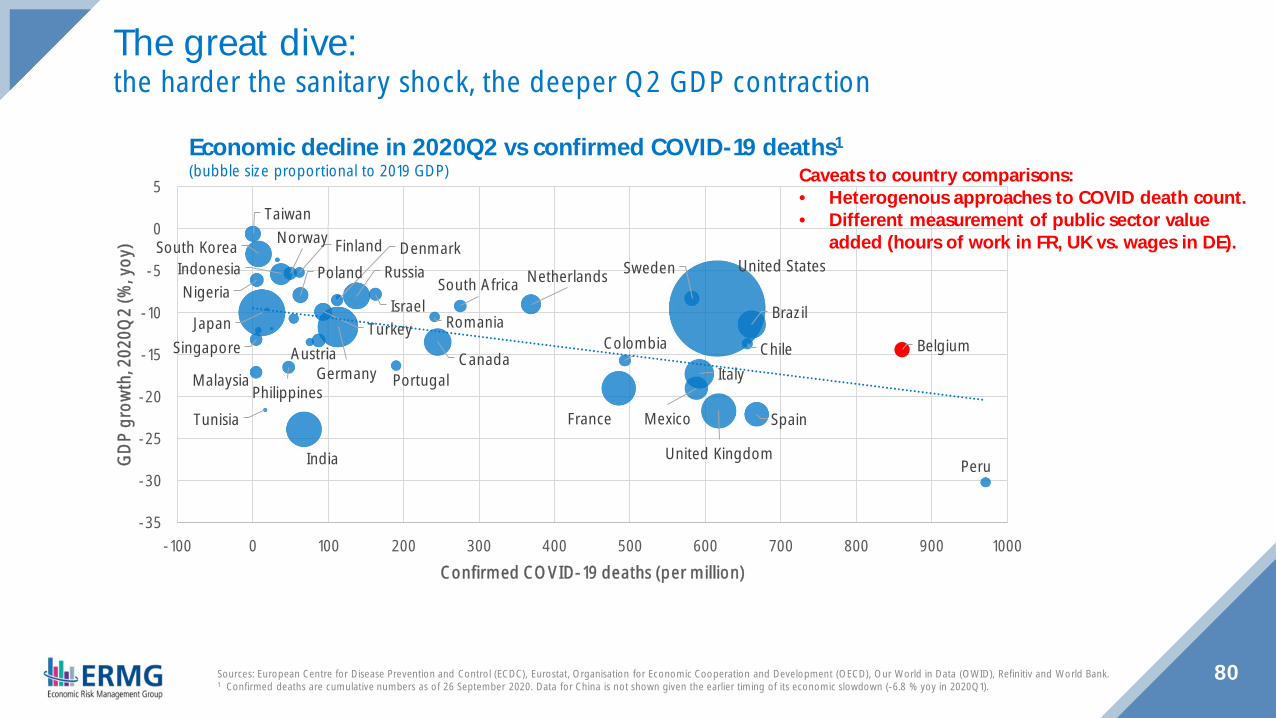

Economic decline in 2020Q2 vs confirmed COVID-19 deaths1

(bubble size proportional to 2019 GDP)

The great dive:the harder the sanitary shock, the deeper Q2 GDP contraction

Austria Belgium

Brazil

Canada ChileColombia

Germany

Denmark

Spain

Finland

France

United Kingdom

Indonesia

India

Israel

Italy

Japan

South Korea

Mexico

Malaysia

NigeriaNetherlands

Norway

Peru

Philippines

Poland

Portugal

Romania

Russia

Singapore

Sweden

Tunisia

Turkey

United States

Taiwan

South Africa

-35

-30

-25

-20

-15

-10

-5

0

5

-100 0 100 200 300 400 500 600 700 800 900 1000

GDP

grow

th, 2

020Q

2 (%

, yoy

)

Confirmed COVID-19 deaths (per million)

Sources: European Centre for Disease Prevention and Control (ECDC), Eurostat, Organisation for Economic Cooperation and Development (OECD), Our World in Data (OWID), Refinitiv and World Bank.1 Confirmed deaths are cumulative numbers as of 26 September 2020. Data for China is not shown given the earlier timing of its economic slowdown (-6.8 % yoy in 2020Q1).

Caveats to country comparisons:• Heterogenous approaches to COVID death count.• Different measurement of public sector value

added (hours of work in FR, UK vs. wages in DE).

81

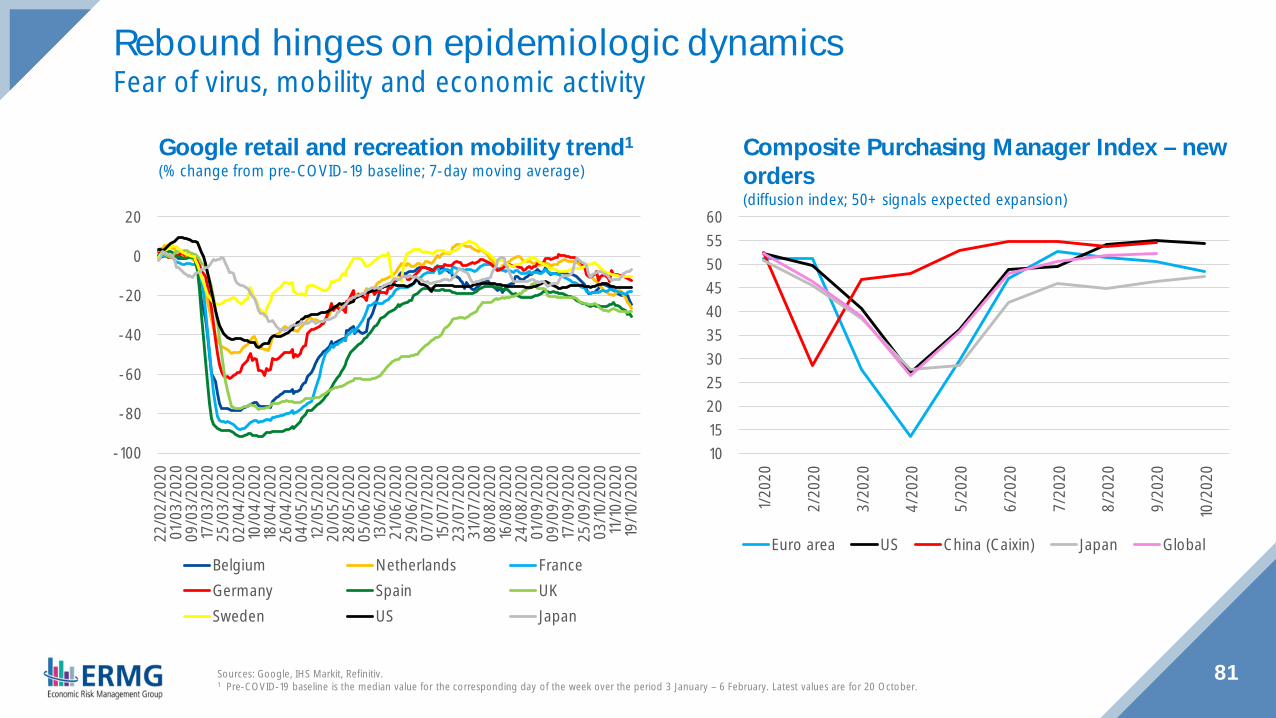

Composite Purchasing Manager Index – neworders(diffusion index; 50+ signals expected expansion)

Google retail and recreation mobility trend1

(% change from pre-COVID-19 baseline; 7-day moving average)

Rebound hinges on epidemiologic dynamicsFear of virus, mobility and economic activity

-100

-80

-60

-40

-20

0

20

22/0

2/20

2001

/03/

2020

09/0

3/20

2017

/03/

2020

25/0

3/20

2002

/04/

2020

10/0

4/20

2018

/04/

2020

26/0

4/20

2004

/05/

2020

12/0

5/20

2020

/05/

2020

28/0

5/20

2005

/06/

2020

13/0

6/20

2021

/06/

2020

29/0

6/20

2007

/07/

2020

15/0

7/20

2023

/07/

2020

31/0

7/20

2008

/08/

2020

16/0

8/20

2024

/08/

2020

01/0

9/20

2009

/09/

2020

17/0

9/20

2025

/09/

2020

03/1

0/20

2011

/10/

2020

19/1

0/20

20

Belgium Netherlands FranceGermany Spain UKSweden US Japan

1015202530354045505560

1/20

20

2/20

20

3/20

20

4/20

20

5/20

20

6/20

20

7/20

20

8/20

20

9/20

20

10/2

020

Euro area US China (Caixin) Japan Global

Sources: Google, IHS Markit, Refinitiv.1 Pre-COVID-19 baseline is the median value for the corresponding day of the week over the period 3 January – 6 February. Latest values are for 20 October.

82

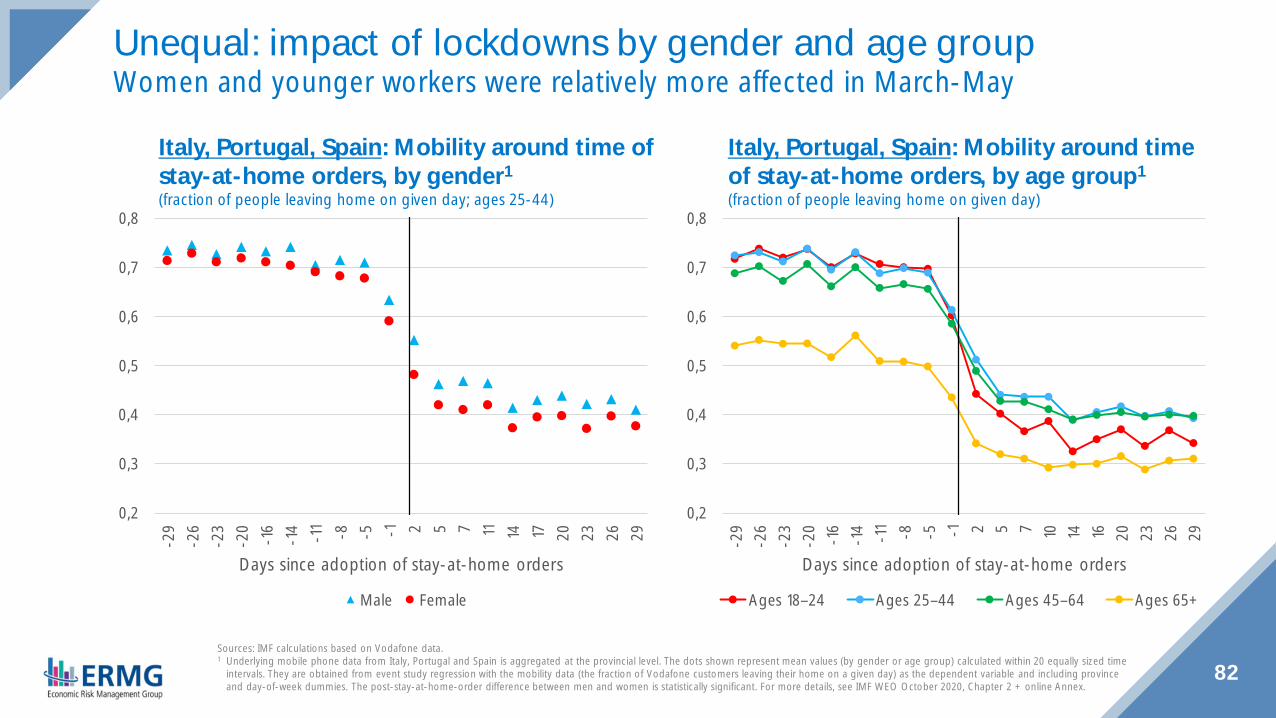

Italy, Portugal, Spain: Mobility around timeof stay-at-home orders, by age group1

(fraction of people leaving home on given day)

Italy, Portugal, Spain: Mobility around time ofstay-at-home orders, by gender1

(fraction of people leaving home on given day; ages 25-44)

Unequal: impact of lockdowns by gender and age groupWomen and younger workers were relatively more affected in March-May

0,2

0,3

0,4

0,5

0,6

0,7

0,8

-29

-26

-23

-20

-16

-14 -11 -8 -5 -1 2 5 7 11 14 17 20 23 26 29

Days since adoption of stay-at-home orders

Male Female

Sources: IMF calculations based on Vodafone data.1 Underlying mobile phone data from Italy, Portugal and Spain is aggregated at the provincial level. The dots shown represent mean values (by gender or age group) calculated within 20 equally sized time

intervals. They are obtained from event study regression with the mobility data (the fraction of Vodafone customers leaving their home on a given day) as the dependent variable and including provinceand day-of-week dummies. The post-stay-at-home-order difference between men and women is statistically significant. For more details, see IMF WEO October 2020, Chapter 2 + online Annex.

0,2

0,3

0,4

0,5

0,6

0,7

0,8

-29

-26

-23

-20

-16

-14 -11 -8 -5 -1 2 5 7 10 14 16 20 23 26 29

Days since adoption of stay-at-home orders

Ages 18–24 Ages 25–44 Ages 45–64 Ages 65+

83

Euro area: extra-EA-19 goods export volumes2

(% change yoy)World goods trade volumes1

(average of exports and imports, % change yoy)

World tradeTowards a protracted repair of global value chains?

-30

-25

-20

-15

-10

-5

0

5

10

15

20

1/20

18

4/20

18

7/20

18

10/2

018

1/20

19

4/20

19

7/20

19

10/2

019

1/20

20

4/20

20

7/20

20World Advanced economiesEmerging economies Euro areaChina

-40-35-30-25-20-15-10-505

101520

1/20

18

3/20

18

5/20

18

7/20

18

9/20

18

11/2

018

1/20

19

3/20

19

5/20

19

7/20

19

9/20

19

11/2

019

1/20

20

3/20

20

5/20

20

7/20

20

Consumer goods (excl. transport eqp.)

Intermediate goods

Capital goodsSources: Central Planning Bureau (CPB), Eurostat, Refinitiv.1 Latest available data: August 2020.2 Latest available data: July 2020.

Chinese exportsboosted by demandfor COVID-19-relatedproducts, incl. PPE,medical equipment,work-from-homeelectronics.

84

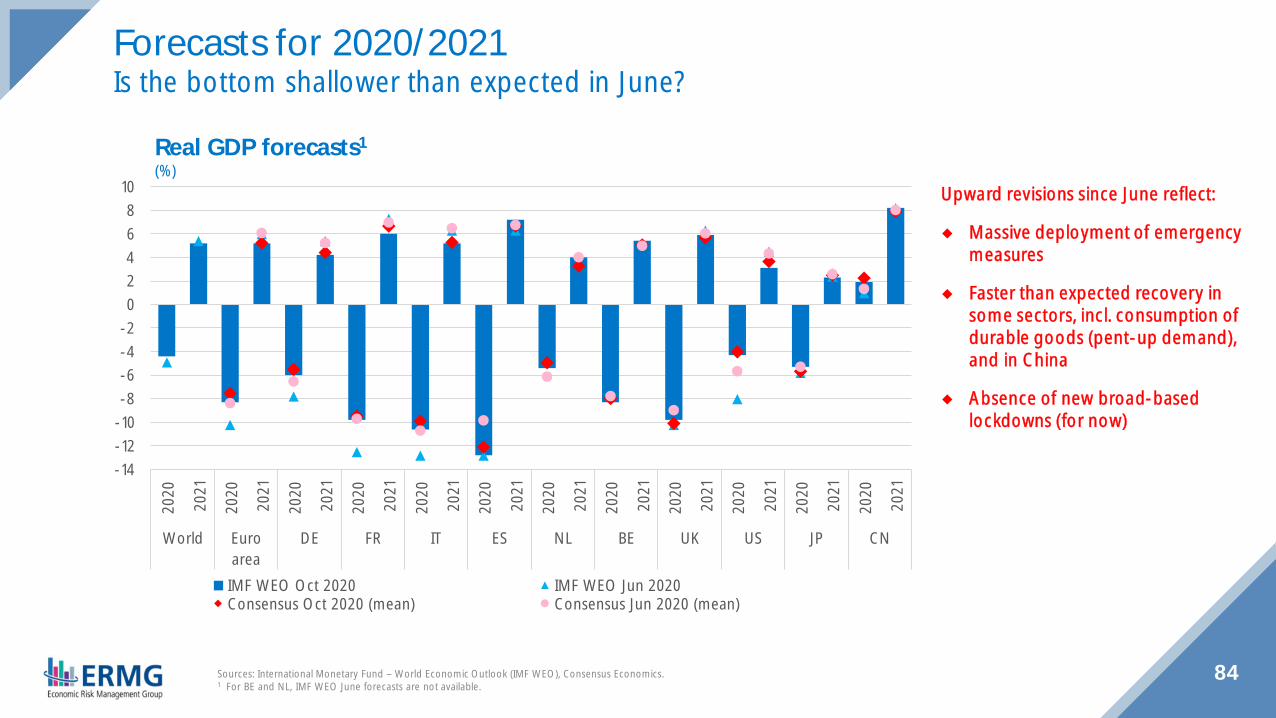

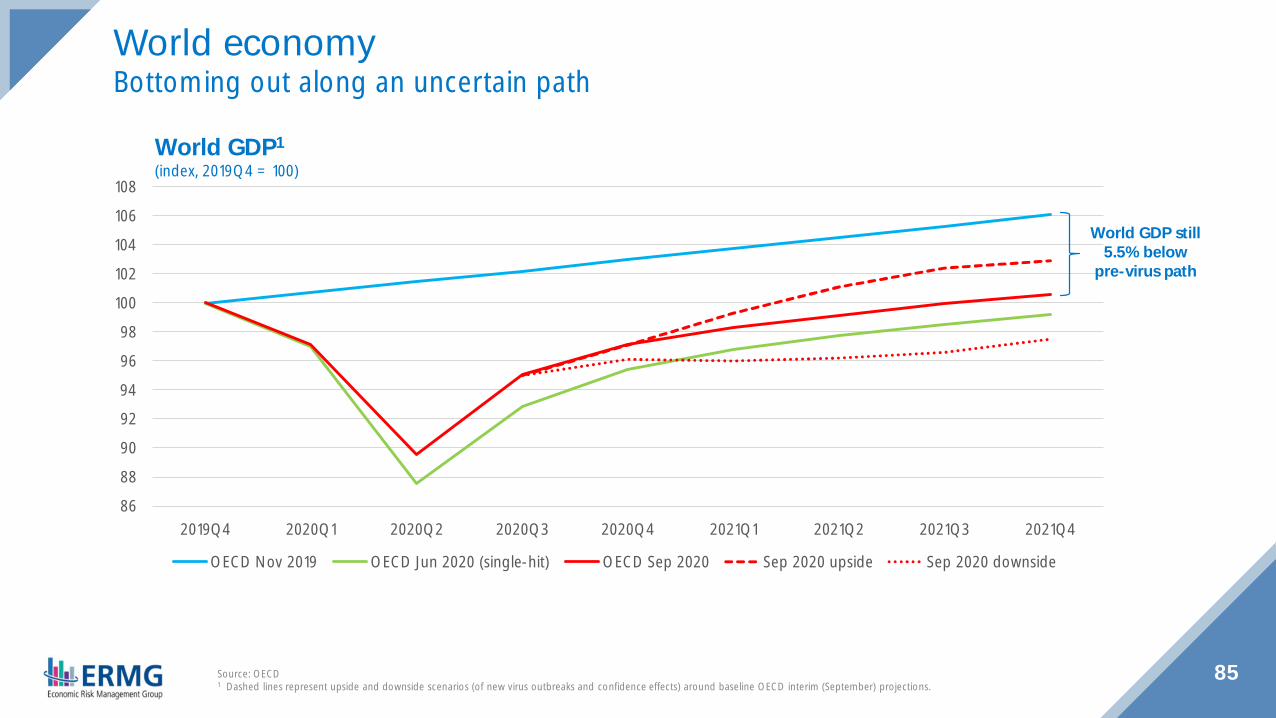

Real GDP forecasts1

(%)

Forecasts for 2020/2021Is the bottom shallower than expected in June?

-14-12-10-8-6-4-202468

1020

20

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

2020

2021

World Euroarea

DE FR IT ES NL BE UK US JP CN