Brent Buyse Thesis

47

UNIVERSIDAD COMILLAS – FACULTAD DE DERECHO (ICADE) Shadow Banking: Lucrative lending by non-bank financial entities in the gaps of regulation. Brent Thomas Buyse Supervised by: Bernardino Muñiz 15 April 2015

-

Upload

brent-buyse -

Category

Documents

-

view

121 -

download

1

Transcript of Brent Buyse Thesis

UNIVERSIDAD COMILLAS – FACULTAD DE DERECHO (ICADE)

Shadow Banking: Lucrative lending by non-bank financial entities in the

gaps of regulation.

Brent Thomas Buyse Supervised by: Bernardino Muñiz

15 April 2015

i

Submitted to the Faculty of the School of Law (ICADE) of Universidad Pontificia Comillas in

partial discharge of the requirements for the Master in International and European Business Law.

Plagiarism Statement

I certify that this thesis is my own work, based on my personal study and/or research and that I have acknowledged all material and sources used in its preparation, whether they be books, articles, reports, lecture notes, and any other kind of document, electronic or personal communication. I also certify that this thesis has not previously been submitted for assessment in any other institution, except where specific permission has been granted from all institutions involved, or at any other time in this institution, and that I have not copied in part or whole or otherwise plagiarized the work of other students and/or persons.

ii

Table of Contents Abstract ............................................................................................................................................................. iii

I. Introduction .................................................................................................................................................. 1

II. How does shadow banking work? ....................................................................................................... 4

a. Alternative payment forms ................................................................................................................. 12

b. P2P Lending .......................................................................................................................................... 14

c. Inter-connectedness ............................................................................................................................ 17

III. Global reality of shadow banking ..................................................................................................... 19

a. Financial Stability Board Monitoring ............................................................................................. 21

b. Shadow Banking in the United States ........................................................................................... 23

c. Shadow Banking in the European Union ..................................................................................... 26

d. Shadow Banking in China ................................................................................................................. 28

e. Shadow Banking in Asia..................................................................................................................... 31

f. Shadow Banking in Switzerland ....................................................................................................... 33

IV. Financial Stability Board Policy and Regulations ........................................................................ 34

a. System wide monitoring ..................................................................................................................... 35

b. Improved oversight .............................................................................................................................. 36

i. Mitigating risk in banks’ interactions with shadow banking activities ......................................................... 36

ii. Reducing the susceptibility of MMFs to “runs” ......................................................................................... 37

iii. Improving transparency and aligning incentives in securitization ................................................................ 38

iv. Dampening pro-cyclicality and other financial stability risks in securities financing transactions such as repos

and securities lending .................................................................................................................................... 38

v. Assessing and mitigating systemic risks posed by other shadow banking entities and activities ...................... 39

V. Conclusion ................................................................................................................................................. 40

Bibliography ................................................................................................................................................... 42

iii

Abstract

This thesis is going to introduce shadow banking as a global financial reality. Shadow

banking is when non-banks facilitate business just like a normal bank would. Shadow banking is an

increasingly complex idea that is responsible for the transaction of trillions of dollars of assets. It is a

system that employs simple concepts like peer-to-peer lending to more complicated such as

securitization and even more elaborate.

For the purpose of this thesis, the discussion will remain with forms of lending. The

financial crisis of 2007-2008 was posited on the flaws of poor lending practices that were

exceptionally accelerated at the fault of poorly managed, understood, and regulated shadow bank

entities. Today that reality is quickly changing.

Regulators around the world are taking notice of what risks are associated with shadow

banking. However, regulators are also seeing the large benefits that shadow banking can relate back

to national economies and the global financial system. By shrinking the size of banks by heavy

regulation it ultimately forces a lot of the lending practices out of traditional banks and into the

arena of shadow banking. That’s ultimately what regulators want in order to not have such an over

reliance on massive financial institutions.

Going forward, regulators are drafting and implementing new regulations to bring shadow

banks out from the shadows and embrace the system and an integral part of the entire financial

system. With the help of the Financial Stability Board, regulators around the world will soon realize

a financial system that sees both traditional banks and shadow banks competing for business in a

resilient financial market. This ultimately is the best scenario for both investors and tax payers.

1

I. Introduction

Put simply, shadow banking is when non-bank entities act like banks. Shadow banks are

more specifically defined as financial intermediaries that conduct functions of banking without

access to central bank liquidity or public sector credit guarantees.1 The Financial Stability Board

(FSB), an international watchdog set up to guard against future financial crises, defined shadow

banking as "credit intermediation involving entities and activities outside the regular banking system,

or non-bank credit intermediation. Shadow banking, when conducted appropriately, provides a

valuable alternative to bank funding which supports positive economic activity as well as quality

competition for banks.

The FSB has recognized five economic functions that are considered shadow banking. These

five activities are: i. management of collective investment vehicles, ii. Loan provision that is

dependent on short term funding, iii. Intermediation of market activities that is dependent on short-

term funding or on secured funding of client assets, iv. Facilitation of credit creation, and v.

securitization and securitization based credit intermediation and funding of financial activities.2

The FSB estimates that shadow banking accounts for a quarter of the global financial

system, with assets of $71 trillion at the beginning of 2013, up from $26 trillion a decade earlier.3 In

some countries, shadow banks are expanding even faster: in China, for instance, they grew by 42%

in 2012 alone.4

Mark Carney, the governor of the Bank of England and head of the Financial Stability Board

was asked to identify the greatest danger to the world economy. He stated shadow banking and in

particular in the emerging markets.5 Shadow banking certainly has the size and reach to be a global

1 (The Economist, 2014) 2 (Financial Stability Board, 2014) 3 Id. 4 Id. 5 (The Economist, 2014)

2

crisis by its very inherent nature. Shadow Banking is huge, fast-growing, in certain forms poorly

understood. Shadow banking can be very good but, if carelessly managed like previously realized,

has the potential to be globally devastating.

But there is disagreement about what counts as shadow banking. The central core of shadow

banking is credit. Everything from China’s loan-making trust companies to Western peer-to-peer

lending schemes and money-market funds. A broader definition, however, would include any bank-

like activity undertaken by a firm not regulated as a bank including the mobile-payment systems

offered by Vodafone, the bond-trading platforms set up by technology firms, online crowd source

lenders like Lending Club, or the investment products sold by BlackRock.

Shadow banks differ from other nonregulated lending institutions in that these nonregulated

lenders are not lending capital of which it has an obligation to pay back. Investors put forth money

in hopes of gaining a profitable return but are not promised nor obliged to a return. Whereas

shadow banks are lending money in which they are obligated to return. This is what makes shadow

banking such a sometimes ominous figure in the financial sector.

Shadow banks can be a big boon for a country's financial sectors. Shadow banking, especially

in emerging markets, expands access to credit because the traditional banks currently are faced with

burdensome regulatory hurdles as well as problems with lending capacities. In advanced economies,

traditional banks have been lending less as a result of new regulatory landscapes. Shadow banks

provide long term credit while traditional banks cannot. As reforms continue, authorities are

recognizing that banking activities can slowly be pushed into the more resilient shadow banking

sector.6

In some ways, it is a good thing that lending is coming from outside traditional banks. Banks

are regulated for a simple reason: they have big “maturity mismatches”. Traditional banks also have

6 (Carney, 2014)

3

become enormously leveraged and are linked and connected in massively complicated ways with

other financial institutions. This makes traditional banks especially fragile. And when traditional

banks get into trouble, taxpayers are left to foot the bill in order to avoid an even greater

catastrophe, because governments both guarantee deposits and are frightened to let such big and

complicated institutions fail. So if some lending is moving from traditional banks to less dangerous

shadow bank entities, the financial system should be safer in the long run.

If a business takes a long-term loan from a pension retirement fund or a life insurer with

long-term liabilities instead of from a bank and if the loan goes wrong, the creditor will lose money.

Without the complexities of leverage coupled with the expanding web of counterparties and then

the depositors demanding their deposits, losses in one institution are less likely to damage others.

Yet shadow banks, if poorly regulated, can be just as dangerous as the traditional banks. One

of the principal culprits in the financial crisis was the “structured investment vehicle”, a legal entity

created by banks to sell loans repackaged as bonds.7 These were notionally independent, but when

they got into trouble they pulled in the banks that had set them up.8 Another source of instability

were money-market funds, through which firms and individuals invested spare cash for short-terms.

Originally, MMFs had been thought of as containing zero risk. When it became evident that these

MMFs were not risk free, they suffered a lightning fast run.

Shadow banks are proliferating because traditional banks are struggling and reorganizing.

Traditional banks have been plagued with losses incurred during the financial crisis and stifled by

new heavier regulation, questionable higher capital requirements, and perpetual legal troubles

coupled with outrageously expensive fines. The traditional banks are reshaping themselves as a

result. Lending has been cut significantly. Shadow banks are filling these gaps. Shadow banking

7 (The Economist, 2014) 8 Id.

4

encompasses a wide array of complex financial activities. As a result, this thesis will be specifically

addressing shadow banking activities as they relate to lending.

II. How does shadow banking work?

Shadow banking tends to grow rapidly when there are strict banking regulations in place, as

well as when interest rates are low resulting in investors searching for better returns, and when there

is a large demand for assets. The current environment in advanced economics is very conducive to

further the growth of shadow banking.

To better understand shadow banking, it is first important to understand how normal

traditional banks operate which gives rise to shadow banking. Banks operate by taking deposits from

individuals and commercial entities, depositors. Banks then take these assets and provide funds to

borrowers in the form of a loan. There is generally an overall maturity mismatch with this behavior

however. Depositors generally need quick short term access to their funds that have been deposited

while at the same time borrowers need long term sources of funding. Banks are able to take

advantage of this because it is very rare that all depositors will demand withdraw on their deposits at

the same time. Therefore, banks can maintain only a small portion of total deposits in the form of

liquid assets and be able to lend out the rest in loans. This is known as "quantitative asset

transformation"9 because it changes the maturity of a short term asset into that of a long term asset,

being the loan. This also changes the liquidity of the bank in that the deposits are in a leveraged

state. This is the most common form in which banks generate revenue. Unfortunately, as history has

shown us, this can leave banks in a very tight position and with little avenues of escape in the event

9 (Noeth & Sengupta, 2011)

5

that all the depositors desire their funds in a simultaneous wave. Such an event is known as a panic

and such events have occurred several times over the centuries of modern banking.

In response to such depositor behavior, many modern economies have created deposit

insurance for bank deposits. Thus resulting in central banks becoming the "lender of last resort" to

banks. By creating deposit insurance it gives depositors and the banks a guarantee to a specific value

thus allowing depositors access to their deposits and it prevents banks from becoming insolvent and

collapsing. This is not a perfect system in that it create a moral hazard on the part of the banks. This

moral hazard is arguable the origin of the shadow banking sector.

Banks investing in risky loans benefit from a higher return on the loan issued. The higher the

risk, the greater the likelihood the burden is then placed on taxpayers to pay and bailout depositors

in the event that the enormity of risky loans fail resulting in an issue of insolvency for the bank. This

has resulted in regulators to require banks to maintain capital levels at certain minimum standards in

relation to the riskiness of their lending behavior. This means that banks whose lending practice is

very prudent and does not take on large risks is thus not required to maintain the same capital level

as a bank who engages in chronically risky lending behavior with slim chances of successful return.

The tradeoff is prudent lending does not lead to a high return whereas risky lending does. This is the

inherent dichotomy of risk vs reward to which regulators try to mitigate risk in order to ensure a

banks do not fail and a healthy banking system is maintained for the overall stability of a healthy and

growing economy.

In response to capital requirements regulation, banks created what are known as "off-

balance-sheet entities."10 These off-balance-sheet entities, also known as incognito leveraged entities,

are design is to create the perspective of a less burdened bank in order to lower the capital

requirement. The balance sheet of a bank shows the various assets, liabilities, and net value. This is

10 (Smith, 2015)

6

the most fundamental evaluation of the real position that a bank, or any commercial entity, currently

sits. "Off-balance-sheet entities are assets or debts that do not appear on a company's balance sheet.

For example, oil-drilling companies often establish off-balance-sheet subsidiaries as a way to finance

oil exploration projects. In a clean and clear example, a parent company can set up a subsidiary

company and spin it off by selling a controlling interest or the entire company to investors. Such a

sale generates profits for the parent company from the sale, transfers the risk of the new business

failing to the investors and lets the parent company remove the subsidiary from its balance sheet.”11

This is a common practice which mitigates risk while allowing a parent corporation to create

separateness and limited liability. Too often, however, off–balance-sheet entities are used to

artificially make commercial entities look more financially secure than they actually are. A complex

array of investment vehicles, most famously the subprime-mortgage securities and credit default

swaps, are used to remove debts from corporate balance sheets. The parent company lists proceeds

from the sale of these items as assets but does not list the financial obligations that come with them

as liabilities. When banks issue loans the loans are typically kept on the bank's books as an asset. If

those loans are securitized and sold off as investments the securitized debt, for which the bank is

ultimately liable, is not kept on the bank's books. Herein lies the foundation of shadow banking. It is

an alternative form to the main practice of tradition banks which is qualitative asset transformation.

The credit intermediation, the act of lending funds raised by depositors, through the shadow

banking system is very similar to traditional bank and this is what fulfills the principle functions of

banks being that of qualitative asset transformation. Banks fulfill this by simply the issuing of loans

in a liquid asset which are provided for to the bank by depositors in the form of a liquid asset

deposit. This is a very simple and straight forward process with a limited number of parties

11 Id.

7

involved. Shadow banking involves a much more complicated process to achieve the same goal,

which is with many benefits as well as cautions.

The depositors in shadow banking are wholesale investors who in turn sell to individual

investors and who provide the funds like a traditional depositor would. They provide an analogous

short term funds as a depositor through the use of repurchase markets(more commonly known as

repo markets) and most commonly through money market funds(such funds are also known as

money market mutual funds). On the other end of the process is the loan originator which in the

traditional model would be the bank. Here we find the "shadow bank" which is a financial

institution or can also be a traditional bank engaging in the shadow banking system.

The repurchase market where repo transactions take place. Repo transaction are whereby

commercial entities with surplus case buy a security for cash only for an issuer and then resell them

back to the issue after a short period of time, or term. This functions like a loan to the seller, issuer,

of the security. The security itself is the collateral to the loan made by the purchaser to the seller of

the security. These transaction can be very open ended and are often rolled over with frequency.

This, in turn, functions just like a deposit at a traditional bank. So analogous in fact that a repo

transaction is withdrawable on demand just like a depositor can withdraw funds on demand from a

traditional bank. However, the analogy stops there. There is no deposit insurance on a repo

transaction. The security to the "deposit" is inherent to the collateral. In the event that the issuer is

unable to repay the buyer, the buyer is entitled to sell the repo on the open market and collect the

proceeds from the open market sale, thus passing the obligation to pay to the new owner from the

original buyer. In addition, repo transaction are over collateralized. This overcollateralization results

in a haircut on the repo transaction and is dependent specifically on the level of risk involved with

the repo transaction. The loan amount is typically less than the face value of the security used as

8

collateral. Suppose the lender lends $9 million and receives $10 million of bonds at market value,

then there is a ten percent haircut.

Money Market Funds are a second method by which shadow banking is initiated. In money

market funds investors pool funds together in order to invest in a high-quality and short-term

security. Generally, such investments are issued by governments, central banks, or major well

established corporations who are financially stable. These investments in money market funds are

also withdrawable on demand just like repo transaction which is why they are nearly analogous to

traditional deposits at a bank. Due to the type of security these investment seek, they are regarded as

with no credit risk or very low credit risk. This demands on if it is a US Treasury bill which is most

common, or some other form of commercial paper which is asset backed. Such asset backed

commercial paper is highly regulated in order to ensure the genuine high quality of the security.

Asset banked commercial paper is typically backed by loan receivables or credit card receivables as

the underlying collateral.

Repo transactions and money market funds are attractive and useful in shadow banking

activities because they are safe investments and are withdrawable on demand. This makes them

function like deposits. Although they are similar in that aspect, both do function different in that

investments in money market funds are in the form of a continuing contract where as a repo

transaction is a one-time contract with fixed terms and returns. As stated previously, money market

mutual funds investment shares can be redeemed on demand. Repo transaction use securities that

are typically of a longer maturity as collateral and for short-term borrowing of cash. Both cases have

liability formed which is theoretically withdrawable on demand and of shorter maturities than that of

the assets financed. This is the mechanics of by which shadow banking systems are typically

resemblance of the functions of traditional banks.

9

Historically, traditional banks originate a loan, or issue a loan, with the intention of then

holding on to the loan. However, in modern banking this model has become unprofitable as the

result of increased competition and a changing regulatory regime. In modern banking, origination of

loans is done with the intent and purpose of then converting the issued loan into a security. This is

done by a process known as securitization. Securitization can often be a very complex process with

multiple layers, but the basics of securitization can be explained and is fundamental to the operation

of shadow banking because securitization is how bank deposit funds are used to finance repo

transactions or investments in money market funds.

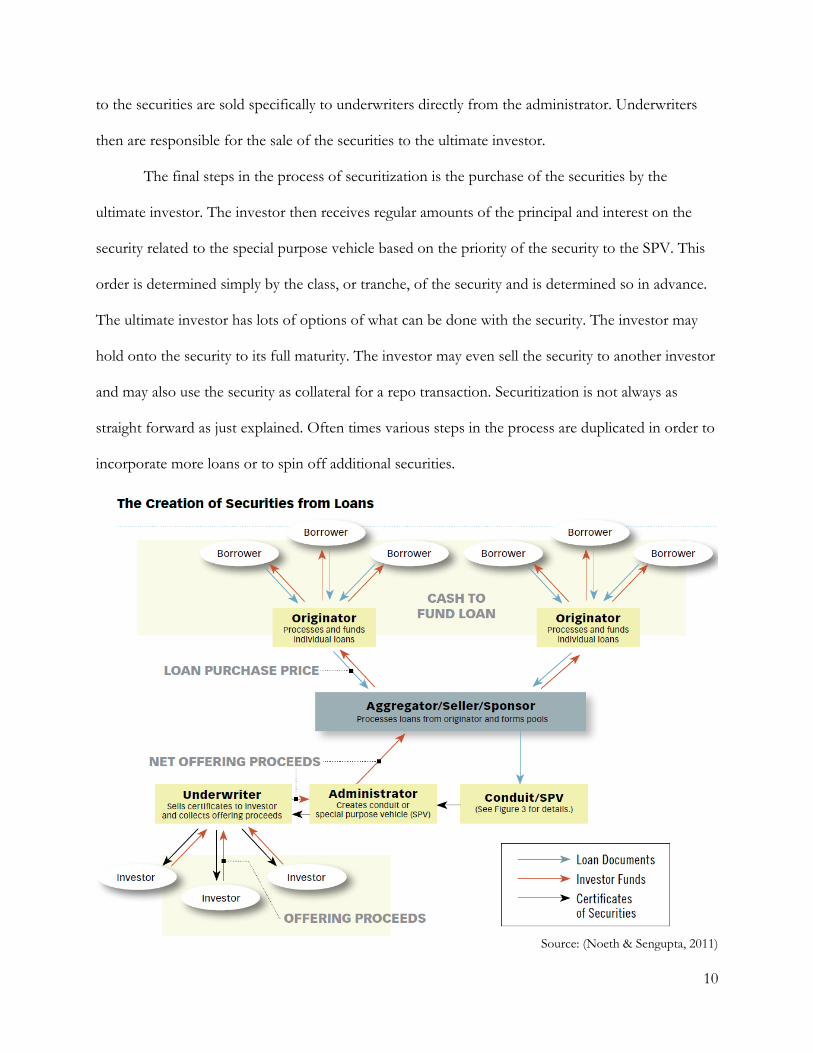

The starting point to securitization is the originating bank of a loan, whether it is a home

loan or auto loan or student loan, arranges for the loan to be sold to what is known as a warehouse

bank. Warehouse banks purchase loans from a variety of banks much like a warehouse holds a

variety of goods. These warehouse banks are also known as aggregators, sellers, or sponsors. The

financing to this process is that the warehouse bank will issue a line of credit to the originator of the

loan who can then close on the loan and then pass the loan documents back to the warehouse in

exchange for the line of credit funds to be disbursed so the originator can pay out the loan.

Warehouse banks then collect large amounts of loan documents from multiple sources on a large

number of loans. These loan documents serve as collateral on the lines of credit issued to each

originating bank for each loan.

The next step in the process is the sale of these pooled loans at the warehouse bank to what

is known as an administrator. The administrator purchases the loans and then creates a special

purpose vehicle (commonly referred to as a SPV) to then hold the loans. The special purpose vehicle

then issues securities against the loans held by the special purpose vehicle. It is important to note

that the administrator’s purpose is to only purchase loans from a warehouse/aggregator and place

the loans in a SPV. The administrator does not openly sell the securities, generally. The certificates

10

to the securities are sold specifically to underwriters directly from the administrator. Underwriters

then are responsible for the sale of the securities to the ultimate investor.

The final steps in the process of securitization is the purchase of the securities by the

ultimate investor. The investor then receives regular amounts of the principal and interest on the

security related to the special purpose vehicle based on the priority of the security to the SPV. This

order is determined simply by the class, or tranche, of the security and is determined so in advance.

The ultimate investor has lots of options of what can be done with the security. The investor may

hold onto the security to its full maturity. The investor may even sell the security to another investor

and may also use the security as collateral for a repo transaction. Securitization is not always as

straight forward as just explained. Often times various steps in the process are duplicated in order to

incorporate more loans or to spin off additional securities.

Source: (Noeth & Sengupta, 2011)

11

The creation of this securities establishes the passing of the proceeds from the sale of the

securities upstream to all of the participating entities in the chain of intermediation. That being the

administrator, the aggregator and the originators of the loans. More simply, the creator of the SPV,

the warehouse bank, and then the originating bank of the loan. This also create a necessity of short-

term funding at each step of the process. This is for two possible reasons. First, the maturity is

mismatched being that the maturity of the securities is of a shorter term than the maturity on the

loan which requires the entity to "roll over:" the securities or use short term funds to pay the

investors. The second is that at each step in the securitization process the short term funding need

arises between the purchase of the loans and their subsequent sale downstream which is arguably the

most common scenario. This short term funding is where the repo transaction, money market funds

become heavily relied upon. Each time an entity utilizes the use of a repo transaction or money

market mutual fund they are performing the function of a bank because they are acquiring funding.

Each step in the securitization process is funded by a "shadow lending" activity to complete the

shadow banking process. The securitization process thus transforms longer term loans, like

mortgages and student loans, which can carry a varying degree to risk levels into financial

instruments of a shorter maturity and can considerably lower the risk. This process as a whole

mimics the function of a bank.

Shadow banking has been criticized as being redundant to traditional banks. Traditional

banking activities and shadow banking activities do achieve the same general purpose of qualitative

asset transformation, however shadow banking achieves this goal in a manner that a traditional bank

cannot. Shadow banking utilizes securitization. Securitization allows for risk diversification across

multiple borrowers, financial products, and physical geographical locations- i.e. different financial

markets. Securitization takes advantage of the economies of scale and scope by segmenting various

different activities of credit intermediation which in turn reduces over call to lending. By providing

12

such a variety of securities that differ in relation to risk and maturity, a better opportunity to

manage portfolios is provides than would normally be considered possible in the traditional banking

model. The most important difference, when securitization is done properly, is an increase of

transparency and disclosure because banks now sell assets that are then scrutinized during

securitization that they would otherwise just hold on in their rather opaque balance sheets.

a. Alternative payment forms12

Payment systems around the world have generally been operated and maintained by banks.

The processing of retail payments is another important core function of the financial system. The

way in which payment systems are developing as a result of innovative new technologies and

demand for increased convenience is leading payment systems to move outside of traditional bank.

This shift results in lower revenues for traditional banks which have in the past been very reliant on

such fees. These shadow banks which participate in the payment process have created secure

methods which mimic and can complete entire transaction without the need of a traditional bank.

Traditional banks role as the intermediary for payments is a product of these entities have

large deposits of liquid assets from depositors as well as the interconnectedness of traditional banks

throughout the financial system. Banks can transfer funds between each other in order to satisfy the

transactions between buyers and sellers with ease. As technology continues to advance, shadow

banks are beginning to fill in some, if not all, of those roles. "Most non-banks have specific and

limited functions in retail payment systems, such as providing customer interface or back-office

12 Although alternative payment forms are not a source of lending, they are important as a demonstration of how shadow banking is advancing on all fronts on the model of traditional banking.

13

services for payment networks run by banks. Some non-banks also provide clearing and settlement

services to banks, thus playing a much larger role as an integral part of payment processing."13

Over the last several decades, electronic noncash payments have grown rapidly. The scale of

non-cash payments is enormous with an estimated 334 billion transactions globally in 2012.14 Bank

cards accounted for 61% of total number of non-cash transactions.15 Credit transfers and direct

debits together accounted for 30% of non-cash transactions.16 The remainder of transactions

consisted of checks, which continue to decline as a share of total transactions.

Electronic payments generally consist of three basic steps: authorization, clearing, and finally

settlement. The initiating step, authorization, consists of the transmission of data to the processor of

the payment for the confirmation of the identity as well as the permission to facilitate the

transaction. The second step, the clearing, involves the aggregating of the transaction. This is the

transmission of the values requested for disbursement and the final "net amount" for the

transaction. The final step, the settlement, is the electronic transfer of the funds to complete the

transaction. It is the "hand shake" between the accounts of the buyer and seller.

Shadow banks are providing similar services. Through the use of online services, shadow

banks are able to complete the entire transaction and can even do so, sometimes, without the need

for a traditional banks involvement. Some of these shadow bank payment companies have created

"closed-loop payments" in which virtual online accounts for buyers and sellers within the online

system are credited and debited without the involvement of traditional banks. Such entities and

services are becoming increasingly popular around the world. In the United States alone, in 2012,

there were over 2 billion of these sort of transaction.17 Not all shadow bank payment systems do by

13 (Borst, 2015) 14 (World Payment Reports, 2014) 15 Id. 16 Id. 17 (Federal Reserve Bank, 2014)

14

pass traditional banks, however. Many systems, such as PayPal, require account settlement with a

bank account or credit card. This does still have an effect on the payment system. For example,

several dozen purchases can be made on PayPal, but when the settlement between PayPal and a

traditional bank occurs there is only one transaction for the total amount of all purchases executed

using PayPal's payment service. One transaction which is the total of dozens of transactions.

This results in lower revenues from transaction fees for the bank. There are currently a variety of

other shadow bank payment services that are similar or identical to the model by which PayPal has

come to function and become widely used and embraced around the world

The growth of these shadow bank payment services helps fosters innovation as well as

improve efficiency in the current market place for transactions. Traditional banks view these new

alternatives as a challenge to their well-established structure of fees by which large sums of revenue

are generated. Without absolute regulation, traditional banks will have to adopt in terms of

technology as well as re-evaluating the manner and method by which fees are assessed for electronic

transactions.

b. P2P Lending

As a result of banks restructuring and focus on conforming to new regulatory standards

since the financial crisis new alternatives have percolated which also contributes to the shadow

banking sector. These smaller shadow bank entities take the forms as payday lenders, pawnbrokers

and even loan sharks as well as other similar "institutions". Nobody is too worried by competition to

banks in their ancillary businesses: if, say, Google can help people manage their money more

efficiently, that is to be welcomed.18 The most important and potentially revolutionizing for the

18 (The Economist, 2014)

15

financial sector is a form of "grassroots finance" known as peer-to-peer (P2P) lending. The worry is

in the creation of credit intermediation, which P2P does not do. It is a good thing that lending

outside the banking system is expanding.

P2P Lending is a process by which any range of entities in search of funds are matched,

generally by an online electronic intermediary, to entities which are seeking to lend. Lending entities

earn a higher interest rate than what is currently possible on a deposit at a bank while the borrowers

generally will pay less than they would have to pay for a loan from a bank.

Peer-to-peer lending is developing around the world at a fast pace. Growth is seen in large

volumes. In Britain, loan volumes are doubling every six months. They have just passed the £1

billion mark ($1.7 billion), though this is tiny against the country’s £1.2 trillion in retail deposits.19 In

America, the two largest P2P lenders, Lending Club and Prosper, have 98% of the market.20 They

issued $2.4 billion in loans in 2013, up from $871m in 2012.21

The scale of P2P is still modest in size. The two largest P2P lending firms in the United

States have thus far lent only $5 billion combined.22 This is small in comparison to the total

personal-loan market of $1.8 trillion in the United States.23 But the rate of growth is rapid. At the

smaller of the two, Prosper, the value of new loans agreed in March totaled $77million, which was

more than four times that a year earlier.24 Its lending has grown by 3,000% in eight years. Such

exponential growth is a common theme in this sector.25 Another common theme, for now, is that

default are low.

19 (The Economist, 2014) 20 Id. 21 Id. 22 (The Economist, 2014) 23 Id. 24 Id. 25 Id.

16

These P2P loans are generally an unsecured personal loan regardless if it is a business or a

private individual. Some P2P intermediaries even allow the investor to decide the loans to which

they ultimately underwrite. Additionally, P2P intermediaries can also bundle the loans for investors,

or multiple investors, in a securitized fashion in order to give a dynamic return with inherent

security.

Regulators are also taking note of P2P lending. The new worry about P2P lending is that a

poorly managed platform might collapse and take all of the investors’ money in the collapse. Funds

placed with P2P lenders are not covered by the state-backed guarantees that protect retail deposits in

banks. At a conference organized by the P2P Finance Association executives were worried about the

risks of a “Bitcoin-style bust” that could rattle confidence in the new and fragile lending sector. New

regulatory rules are likely to insist that P2P businesses create separate funds gathered from savers

and coordinate for third parties to manage outstanding loans if they cease trading. Some platforms

offer something of a substitute. Zopa and most other British companies have started “provision

funds”, which aim (but do not promise) to make good on loans that sour.26 These smooth the risk

for lenders, but blunt the original P2P concept. Purists fear such arrangements could recreate the

moral hazard that has plagued conventional banking.

The promising aspect to P2P intermediaries in the shadow banking sector is that in the event

of a default on a loan the loss is passed directly to the lender. The reason why this is important is

because it does not place traditional deposits at risk at a traditional bank nor does it place any

burden on central bank deposit insurance. P2P intermediary lending allows for access to liquidity

and assets in a manner in which that does not ultimately put any adverse risk to the tax payer. In

addition, P2P lending also ends the worrisome and dangerous mismatches often seen in other areas

of shadow banking between short-term deposits and long-term loans inherent in conventional

26 (The Economist, 2014)

17

banking but generally by locking lenders in for the loan’s duration.27 It is a system of "lender

beware" which is in conformity to the new modern idea of investments and investing.

c. Inter-connectedness

Inter-connectedness between shadow banks and traditional banks poses a significant threat

to the viability and sustainability of financial systems in specific countries and the greater global

financial system. As what was discovered in the financial crisis, traditional banks and shadow banks

were significantly inter-connected to such an extent that failures and runs that occurred outside of

the traditional banking sector caused great stress and strain on traditional banks by a phenomenon

known as contagion.

Inter-connectedness takes two main forms. These forms are direct and indirect links. Direct

links are established when shadow banks are either forming part of a traditional banks credit

intermediation process, or are directly owned by a traditional bank, or are benefiting from direct

support from a traditional bank. Indirect linkages are established when both shadow banks and

traditional banks have invested in similar assets or are exposed to common entities.

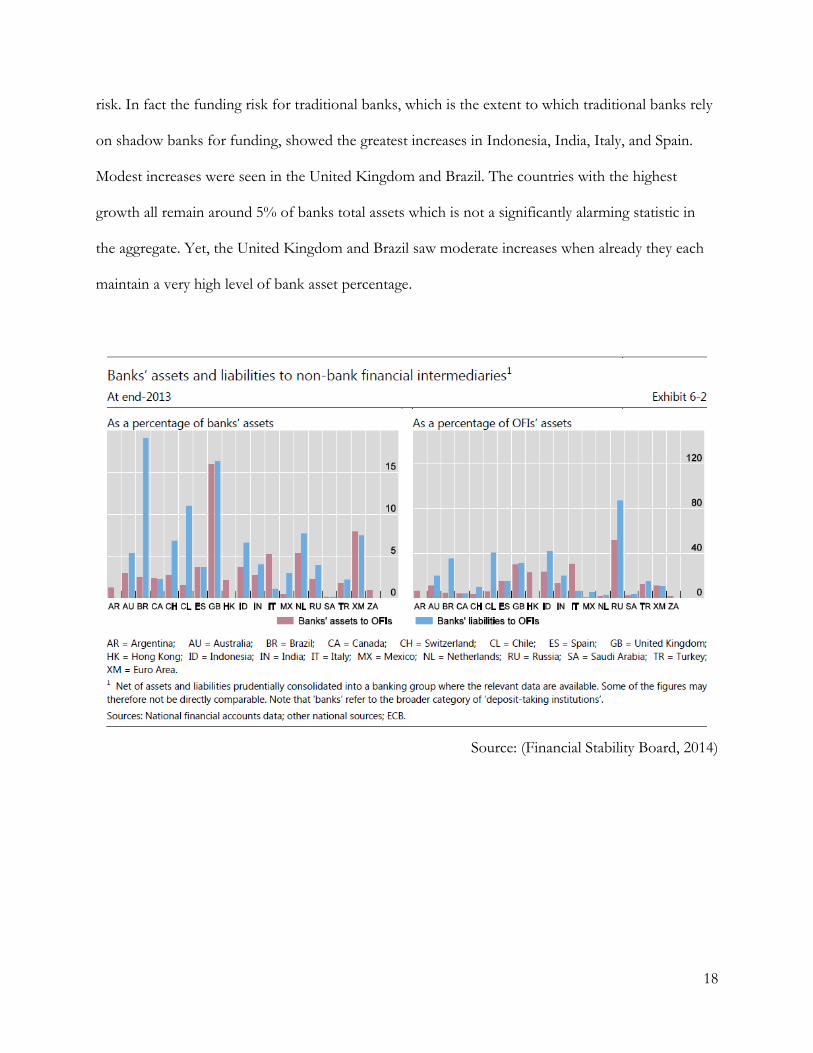

According to the FSB report on global shadow banking, interconnectedness has declined on

a year over year basis.28 Traditional banks assets to OFI's(shadow bank entities) declined from $4.3

trillion at the end of 2012 to #$3.9 trillion at the end of 2013.29 Traditional banks liabilities to OFIs

declined as well from $4.7 trillion to $4.4 trillion.30 Additionally, Australia and Chile experienced the

most decrease in the exposure of their traditional banking system to shadow bank entities. Not all

countries have experienced the same results. Spain as well as the Netherlands have seen increases of

27 Id. 28 (Financial Stability Board, 2014) 29 Id. 30 Id.

18

risk. In fact the funding risk for traditional banks, which is the extent to which traditional banks rely

on shadow banks for funding, showed the greatest increases in Indonesia, India, Italy, and Spain.

Modest increases were seen in the United Kingdom and Brazil. The countries with the highest

growth all remain around 5% of banks total assets which is not a significantly alarming statistic in

the aggregate. Yet, the United Kingdom and Brazil saw moderate increases when already they each

maintain a very high level of bank asset percentage.

Source: (Financial Stability Board, 2014)

19

III. Global reality of shadow banking

Shadow banking is a global reality. Shadow banking has become the single greatest

alternative to traditional banking activity. This is made apparent by the absolute enormity of the

shadow banking sector. Using data from the Financial Stability Board's Global Shadow Banking

Monitoring Report (GSBMR) an analysis of the global shadow banking sector as well as the shadow

banking sectors in key financial jurisdictions and financial regions can help better understand the

current state of the shadow banking sector and it's future. The total coverage of the monitoring

report accounts for nearly 80% of global GDP as well as roughly 90% of the global financial

system.31

Shadow banking is a complement and a valuable addition to traditional banking in that it

expands access to credit as well as spreading risk and providing more liquidity to the markets. In

developing economies finance companies and microcredit lenders often provide credit and

investments to underbanked communities. In advanced economies, various types of financial

intermediaries have been stepping in to provide long-term credit to the private sector while banks

have been reorganizing their balance sheets in order to be compliant with new regulatory structures

(see: April 2014 Global Financial Stability Report). Lending activities by shadow bank entities is a

significant portion of total lending activity in the United States economy and is rising in many

countries as well, notably in the European Union.

Although there are many obvious and valuable benefits to the shadow banking sector, the

global financial crisis exposed that without proper regulation shadow banking can put the stability of

the financial system at a serious risk. In advanced economies, some shadow bank entities, like money

31 Id.

20

market funds and SPVs, were highly leveraged or had large holdings of illiquid assets leading up to

the crisis. As a result they were fatally vulnerable to ensuing "runs" when investors withdrew massive

quantities of assets with hardly any notice. This led to a fire sales of assets which in turn intensified

the financial fallout by depressing the value of assets and resulted in traditional banks feeling the

heat and stress of the collapse. Since the crisis, economies and government around the world have

undergone regulatory reforms in cooperation with each other and the FSB. The FSB has been

instrumental in these reforms because the FSB has recommended greater transparency on asset

values, governance improvements, reforms on ownership of assets, stricter oversight and most

importantly improved regulation of shadow banks.

In advanced economies, shadow banking appears to be shifting to less-well-monitored

activities in the wake of new regulations. Only investment funds, especially bond funds, country

specific entities, and “other” entities continued to grow after 2008.32 The growth of the “other”

entities signals a shift in risk to financial stability toward the newer and less understood activities and

could perhaps suggests that these may comprise new forms of direct lending and over-the-counter

derivatives trading.

In emerging market economies, overall growth of shadow banking remains strong. Shadow

banking assets as a proportion of GDP expanded from 6 percent to 35 percent between 2002 and

2012, while banking sector assets grew from 30 percent to 70 percent of GDP over the same

period.33 This growth, however, can be characterized as a normal part of an emerging economy

continuing to develop its financial markets. The growth of shadow banking has been led by the

growth of activities and financial companies that operate financial instruments similar to that of

MMFs. In some countries, including Brazil and South Africa, mutual funds have also been growing

32 (International Monetary Fund, October 2014) 33 Id.

21

strongly; in others, including Mexico and Turkey, real estate investment trusts have expanded

especially fast (albeit from a low base). In dollar terms, China’s shadow banking sector became the

fifth largest among FSB jurisdictions in 2012.34

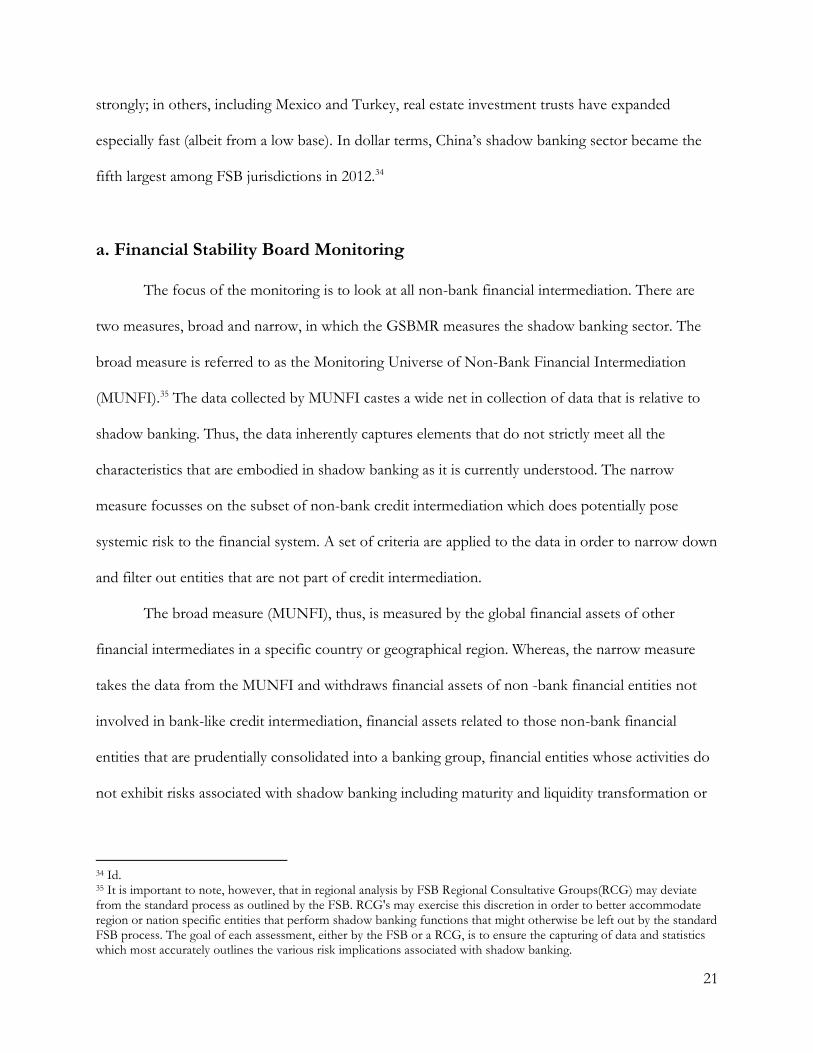

a. Financial Stability Board Monitoring

The focus of the monitoring is to look at all non-bank financial intermediation. There are

two measures, broad and narrow, in which the GSBMR measures the shadow banking sector. The

broad measure is referred to as the Monitoring Universe of Non-Bank Financial Intermediation

(MUNFI).35 The data collected by MUNFI castes a wide net in collection of data that is relative to

shadow banking. Thus, the data inherently captures elements that do not strictly meet all the

characteristics that are embodied in shadow banking as it is currently understood. The narrow

measure focusses on the subset of non-bank credit intermediation which does potentially pose

systemic risk to the financial system. A set of criteria are applied to the data in order to narrow down

and filter out entities that are not part of credit intermediation.

The broad measure (MUNFI), thus, is measured by the global financial assets of other

financial intermediates in a specific country or geographical region. Whereas, the narrow measure

takes the data from the MUNFI and withdraws financial assets of non -bank financial entities not

involved in bank-like credit intermediation, financial assets related to those non-bank financial

entities that are prudentially consolidated into a banking group, financial entities whose activities do

not exhibit risks associated with shadow banking including maturity and liquidity transformation or

34 Id. 35 It is important to note, however, that in regional analysis by FSB Regional Consultative Groups(RCG) may deviate from the standard process as outlined by the FSB. RCG's may exercise this discretion in order to better accommodate region or nation specific entities that perform shadow banking functions that might otherwise be left out by the standard FSB process. The goal of each assessment, either by the FSB or a RCG, is to ensure the capturing of data and statistics which most accurately outlines the various risk implications associated with shadow banking.

22

leverage. The broad measure as well as the narrow measure of shadow banking are both important

indicators of the size, composition and growth trends of non-bank financial intermediaries.

Source: (Financial Stability Board, 2014)

FSB broad estimates shows an increase in shadow banking activity in the euro area, the

United Kingdom, and the United States, while narrower gauges of shadow banking might suggest

stagnation at first glance. After a mild drop around 2008, the FSB measures show varying degrees of

recovery in the United States, the euro area, and the United Kingdom. In contrast, the flow of funds

and noncore liabilities measures remain broadly constant, which reflects two opposing forces: the

decline in the role of certain activities after the crisis, such as securitization and lending via repos and

securities, and a concomitant rise in other activities, including those of country-specific entities. The

pickup in the FSB measures can be partly explained by positive valuation effects from the growth in

the investment fund industry. The large difference between broad and narrow measures reflects

significant activity within the financial system that is not fully captured by other shadow banking

measures.

The goal of the new regulation is to replace a shadow banking system which was prone to

failure due to excess with a shadow banking system that contribute to strong, sustainable balanced

23

growth in the global economy.36 The time is coming now where shadow banking is coming out of

the “shadows” and is to become a sustainable and contributing market based financial competent of

the greater financial sector in the world.

b. Shadow Banking in the United States

Shadow banking in the United States can trace its origins back to securitization in the 1970s,

when Ginnie Mae, a Government Sponsored Enterprise(GSE), began to guarantee mortgage pass-

through securities, as a way to foster the secondary mortgage market and promote

homeownership.37 Fannie Mae and Freddie Mac, both GSE's as well, followed shortly thereafter.

From there securitization quickly spread to other areas and in the 1980s the first "asset backed

security" was created. The growth in shadow bank activity continued to grow and in 1989 began to

outpace the activity of traditional banks. Shadow banking has continued to do so through 2007.38

Despite the serious losses and new regulatory framework which is requiring banks in the US

to reorganize, total shadow bank liabilities still measure in size nearly in equal amounts to traditional

banks. Although the past five years of shadow banking activity in the United States has been on the

decline, this trend is now seen to be reversing. As the American economy continues to grow and

improve, so does the growth in demand for access to credit. The increase in regulatory requirements

in the United States gives shadow banks a competitive advantage against their traditional counter

parts.

36 (Carney, 2014) 37 (TD Bank Group, 2014) 38 Id.

24

Source: (Adrian & Ashcraft, Shadow Banking Regulation, 2014)

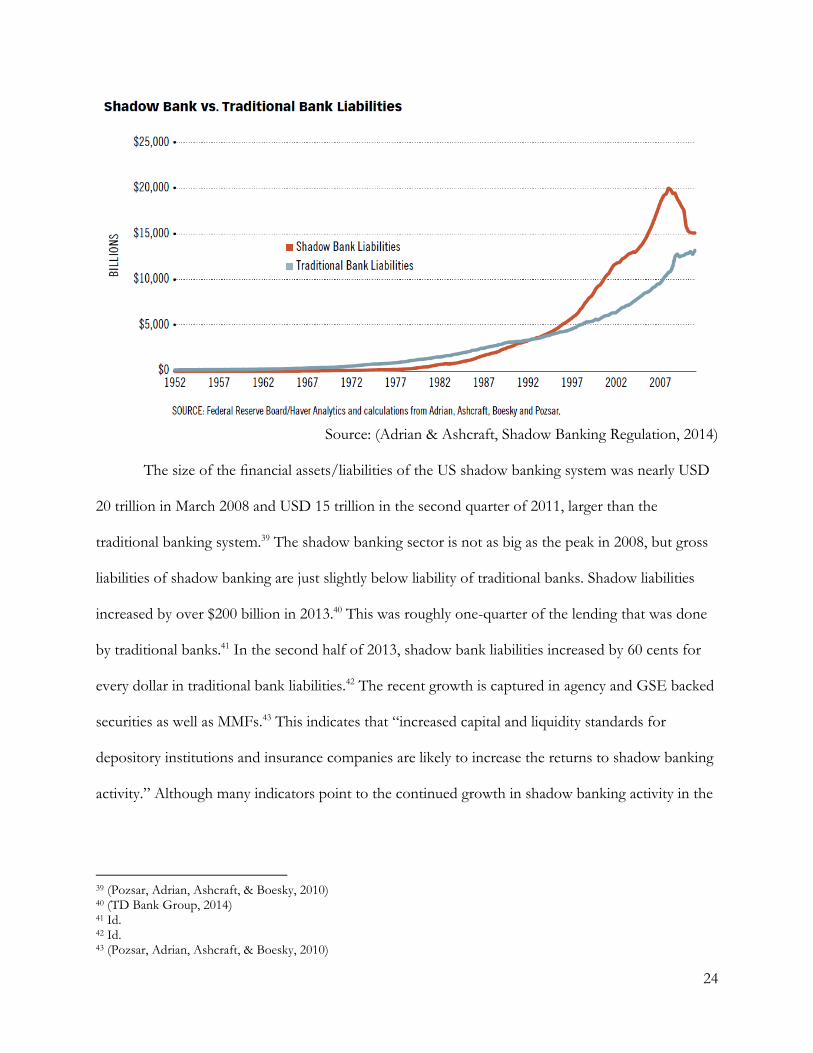

The size of the financial assets/liabilities of the US shadow banking system was nearly USD

20 trillion in March 2008 and USD 15 trillion in the second quarter of 2011, larger than the

traditional banking system.39 The shadow banking sector is not as big as the peak in 2008, but gross

liabilities of shadow banking are just slightly below liability of traditional banks. Shadow liabilities

increased by over $200 billion in 2013.40 This was roughly one-quarter of the lending that was done

by traditional banks.41 In the second half of 2013, shadow bank liabilities increased by 60 cents for

every dollar in traditional bank liabilities.42 The recent growth is captured in agency and GSE backed

securities as well as MMFs.43 This indicates that “increased capital and liquidity standards for

depository institutions and insurance companies are likely to increase the returns to shadow banking

activity.” Although many indicators point to the continued growth in shadow banking activity in the

39 (Pozsar, Adrian, Ashcraft, & Boesky, 2010) 40 (TD Bank Group, 2014) 41 Id. 42 Id. 43 (Pozsar, Adrian, Ashcraft, & Boesky, 2010)

25

United States, regulators are keen to implement regulation on shadow banking as to strength the

entirety of the financial sector to prevent previous errors and gaps in regulation in 2008.

The Dodd-Frank Wall Street Reform and Consumer Protection Act substantially changed

the nature of shadow banking in the United States, among many of its implementations throughout

the financial sector. Dodd-Frank now requires issuers of ABS and ABCP to maintain a portion of

the issuance on balance sheet. This makes issuance of such instruments more expensive and impacts

the commercial viability of the products as well because of the new capital liquidity standards as

established by Basel III. At the same time, these regulations have also fostered improved

transparency of the instruments. Furthermore, the SEC has placed restrictions on the amount of

maturity and the amount of liquidity transformation that may take place with a MMF.

Even with the greater regulatory oversight, the growth in shadow banking remains

significant. Continued innovation in the future of financial products creates new opportunities for

substantial growth potential in a perpetually dynamic financial sector. Economists at the Federal

Reserve Bank of New York expect “shadow banking to adapt to these new regulations” and “new

forms of regulatory arbitrage and shadow banking to emerge.”44

Shadow banking declined significantly during the crisis and subsequent recession in the

United States. The recovery has been slow. As stronger more resilient balance sheet for traditional

banks has improved competition among traditional banks, the recovery and growth in the economy

is fueling growth in shadow banking. The recovery in shadow banking will continue to garner much

attention as investors are looking to see how a newly regulated shadow banking system will continue

to enhance credit intermediation in the financial sector after its disastrous contribute to the financial

crisis.

44 (Adrian & Ashcraft, Shadow Banking Regulation, 2014)

26

c. Shadow Banking in the European Union

Shadow banking is also finding its place in the European Union. Although overall shadow

banking in the EU is smaller than that of the activity in the United States, it is still significant. The

shadow banking sector in the EU is roughly valued at €10.8 trillion in 2011. This accounts for

around 38% of total bank activity in the euro area. The shadow banking sector in the EU also differs

greatly from that of the United States. The sector is very stable in terms of growth and traditional

banks continue to be the main source of credit intermediation in Europe. Roughly three times the

amount of assets are intermediated by traditional banks than shadow banks in the euro area.

It is worth noting that, in the second quarter of 2011, almost 70% of the assets of the “other

intermediaries” grouping (€7.6 trillion) were held by miscellaneous financial institutions. A stock-

taking exercise carried out by the European System of Central Banks (ESCB) in 2009 revealed that

around 19% of the residual “other miscellaneous intermediaries” correspond to financial holding

companies, captive institutions (i.e. those providing financial services to a limited group of

companies) and money lenders.45 Moreover, 15% is constituted by non-deposit taking institutions

engaging in lending (factoring, leasing and other forms) and 10% by securities and derivatives

dealers.46 A remaining 52% is made up of unidentified miscellaneous financial institutions. An

important part of the euro area financial sector remains therefore relatively unexplored by official

statistics.47

Securitization is smaller in volume in the euro area than in the United States. However, the

euro area is not a homogenous group—witness the strength of shadow banking in a country like the

Netherlands where non-financial banking institutions (NFBI) have the largest percentage of total

45 (Bakk-Simon, Borgioli, & Giron, 2012) 46 Id. 47 Id.

27

assets (45%) compared to the US (35%), the euro area (30%), and the UK (25%)48. In fact, euro area

banks have increasingly been relying on funding from other financial institutions, including

securitization vehicles.49

In order to identify the possible systemic relevance of shadow banking, it is important to

understand the interconnections with the regulated banking system. Over the recent past, the

interconnectedness between traditional banks and shadow banks has increased, which has also

increased Europe's exposure to contagion from runs in the shadow banking sector.

The British proportion of shadow banking operations relative to traditional banking is much

greater than in continental Europe. This may be explained by the strong connections of British

banks with the City. Another characteristic of British banks, but also of French and Spanish banks,

is the development of their activities at the international level, much more so than most US banks.

The move into the international financial area is largely due to the response to increased competition

and increased globalized standards among traditional banks. Although the response is to new

financial stimuli, this is not necessarily a new phenomenon. For the United Kingdom, France and

Spain, the internationalization of banking activity is a compliment and parallel to those countries as

colonial powers. Another factor which encouraged the expansion of banks abroad more recently

was European integration. Due to the creation of the European area and the Eurozone, banks are

much more internationalized and convene business on a scale that is unique to most of the world.50

Overall, shadow banking activities in Europe have the pedigree to become a serious threat to

the economy. However, due to the current climate of the European economy and regulation already

established, the majority of financial activity is currently taking place in the traditional banking

sector. However, there is room for growth to be made in the shadow banking sector which can help

48 (Jeffers & Plihon, 2014) 49 Id. 50 Id.

28

grow the European economy as a whole similar to how the shadow banking sector is making

improvements in the American economy. Despite the potential room for growth, regulators and

bankers alike need to be keenly aware of the interconnectedness not only between traditional banks

and shadow banks in Europe, but also between banks in the euro area and banks in the United

States. Close interconnectedness is what helped spread the crisis in its infancy. Regulators need to

take steps to curb this potential threat.

d. Shadow Banking in China

While shadow banking in the United States and European Union has seen somewhat of a

decline or stagnation since the financial crisis, China's shadow banking sector continues to flourish

and grow. Shadow banks, which barely existed before China’s credit surge in 2009, now have assets

of at least 30 trillion yuan ($4.9 trillion), or more than 50% of GDP, according to estimates by ANZ

Bank.51 This is alarming. This growth in the shadow banking sector of China has been fueled by

concerns of traditional bank credit intermediation as well as concerns over growing inflation. The

Chinese government, in 2010, established strategic restrictions on the traditional banking system

through the implementation of increasing interest rates and increased reserve requirements.52 These

new regulations slowed the growth rate of the credit intermediation that was of concern. Very

quickly traditional banks found ways to keep originating credit by the use of off balance sheet

entities. Now, the fastest growing source of credit origination comes from the shadow banking

sector. Non-bank financial institutions accounted for nearly half of the growth in credit in China in

2013. Concerns now fall on one specific type of financial entity, trusts.

51 (The Economist, 2014) 52 (Adrian, Ashcraft, & Cetorelli, Shadow Bank Monitoring, 2013)

29

Trusts are created when bank loans are bought by trust companies. These trust companies

then sell to retail depositors various wealth management products. Banks earn fees on the

origination of loans and management of these products, but since they are off balance sheet, they do

not have to hold capital against them.53 These product also lack any form of a guarantee, generally.

More often than not, the perception is that these products carry an implicit official sector support

via a state bank. Trusts have grown very quickly in part because the central bank has limited the

traditional banks' ability to lend to economic sectors in which there is an observable overinvestment,

for example coalmining and real property. Trusts raise money by offering an attractive returns that

traditional banks could not and then lend to sectors that the regulator have prohibit traditional

banks from lending. As a result, commercial businesses in these economic sector have few

alternatives or options other than seeking funding from the shadow banking sector. Additionally,

China's central bank has placed a cap on interest for deposits which reduces Chinese savers’ return

on deposit. As a result, savings accounts produce a meager 0.35% a year and a one-year fixed deposit

earns 3.3%, which is hardly incentivizing.54 That makes trust products attractive for investors. Much

like other parts of the world, shadow banking is an opportunistic alternative of last resort for

financial mobility and success.

In addition to trust loans, there also exists entrusted loans. These are loans originated by

non-banks which are cash-rich companies that desire to lend to other companies in order to put

their capital to work. These non-bank loans are sold to trust companies and serviced by banks.

Banks also use entrusted loans as a mechanism to continue originating loan to circumvent the loan

quota restrictions, which funds the off balance sheet entity. Banks, as a result of these shadow

53 Id. 54 (The Economist, 2014)

30

activities, have increased their stake of ownership in various trust companies to better facilitate

distribution channel.

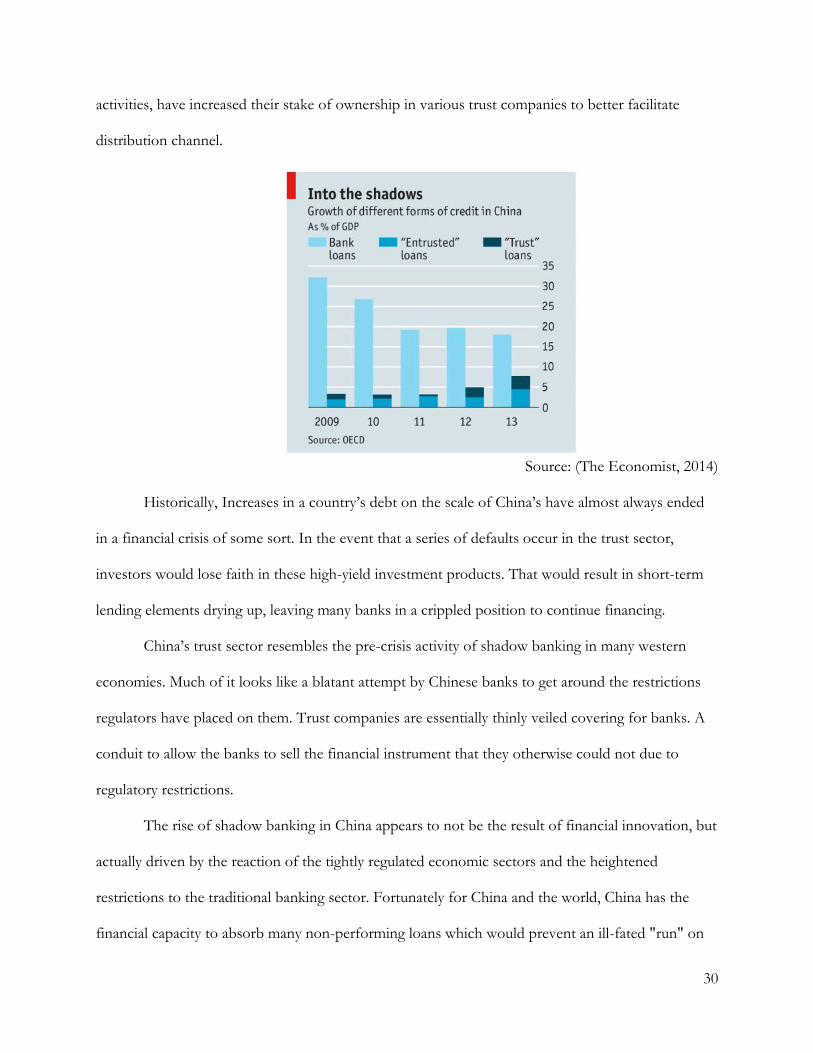

Source: (The Economist, 2014)

Historically, Increases in a country’s debt on the scale of China’s have almost always ended

in a financial crisis of some sort. In the event that a series of defaults occur in the trust sector,

investors would lose faith in these high-yield investment products. That would result in short-term

lending elements drying up, leaving many banks in a crippled position to continue financing.

China’s trust sector resembles the pre-crisis activity of shadow banking in many western

economies. Much of it looks like a blatant attempt by Chinese banks to get around the restrictions

regulators have placed on them. Trust companies are essentially thinly veiled covering for banks. A

conduit to allow the banks to sell the financial instrument that they otherwise could not due to

regulatory restrictions.

The rise of shadow banking in China appears to not be the result of financial innovation, but

actually driven by the reaction of the tightly regulated economic sectors and the heightened

restrictions to the traditional banking sector. Fortunately for China and the world, China has the

financial capacity to absorb many non-performing loans which would prevent an ill-fated "run" on

31

the banks. Standard & Poor’s, a ratings agency, argues that reforms could lead to “a turbulent period

in which funding could dry up as the domestic market struggles to re-price risk”.55 In addition,

combined debts (shadow and traditional) in China are smaller in relation to China's GDP than many

combined debts in western economies leading up to the financial crisis.

e. Shadow Banking in Asia

The Working Group on Shadow Banking of the FSB Regional Consultative Group for Asia

(RCGA) conducted a study on shadow banking in Asia. The Working Group conducted a survey

among RCGA members to examine the profile of non-bank financial intermediaries (NBFIs), the

regulations governing these entities, the definition of shadow banking applied by members, the

distinction between shadow banking and NBFIs, the potential risks emanating from NBFIs and the

applicability of FSB’s recommendations on shadow banking to Asia.

The RCGA is comprised of Australia, Cambodia, China, Hong Kong SAR, India, Indonesia,

Japan, Korea, Malaysia, New Zealand, Pakistan, Philippines, Singapore, Sri Lanka, Thailand and

Vietnam.5657 Ten of the 16 members of this group are classified as emerging economies based on

standard economic indicators.58 In the emerging economies, shadow banking provides commercial

entities and individual’s access to credit where traditional banks could not or are absent from the

local market.59 This has allowed for greater liquidity and economic inclusion to a larger audience who

would otherwise be forgotten. Shadow banking activity in Asia is not a systemic threat nor does it

account for a significant portion of total finance. In addition, the vast majority of the shadow

55 (The Economist, 2014) 56 (Financial Stability Board, February 2015) 57 Analysis for China is markedly different than the rest of the region due to the national specific entities in the shadow banking sector and due to the enormous size and growth of the Chinese economy. 58 (Financial Stability Board, 2014) 59 Id.

32

banking activity is domestic with minimal risk from cross-border transaction. The financial systems

in the Asian economies remains "traditional bank" dominant.60 Shadow banking activities account

for less than half of total assets in the financial system.61 However, the amount of shadow banking

activity in each country does vary greatly. China and Japan have large and intricate shadow banking

sectors. Total OFI assets in Japan comprise roughly half of all OFI assets in Asia.62 Furthermore,

Hong Kong and Singapore are major financial centers in Asia and as a result have a large OFI asset

amount in relation to the size of their economies.

Asian markets should continue to move towards more innovative and sophisticated financial

markets in order to ensure economic development by increasing the efficiency of the allocated

savings available and the financial stability of the region.63 This is also important for the global

economy to help alleviate the global imbalances and the associated reserves accumulated in the

Asian region which is partly to blame for a lack of financial sophistication in the region.64

As a whole Asia is not at risk from shadow banking like other major economies, United

States and European Union for example, due to the fact that the financial markets in Asia are not as

wholly developed as their western counterparts nor are the products they offer at the same level of

complexity like they are offered in America and Europe.65 Financial products originating from non-

banks is just not complex nor enormous enough to pose a serious risk to the financial stability of

Asia as a whole. This is a very positive statistic because it allows for the Asian economies to

continue to grow and develop and use shadow banking in a manner that helps promote economic

growth and financial stability. The future for Asia's financial sectors, both shadow and traditional,

60 Id. 61 NBFIs comprise 33%, OFIs comprise 15% 62 (Financial Stability Board, 2014) 63 (Hannoun, 2008) 64 Id. 65 (Financial Stability Board, 2014)

33

are very bright so long as shadow banking is use responsibly while traditional banks are regulated in

accordance with the high quality international standard.

f. Shadow Banking in Switzerland

Switzerland has long been known as a majorly important financial, and more importantly,

banking hub in the world. According to data collected by the MUNFI and after the implementation

of the narrowing down criteria, Switzerland's shadow banking sector is roughly USD $502 billion

(CHF 481 billion).6667 This corresponds to roughly 81% of Swiss GDP.68 When applying the shadow

banking activities as defined by the FSB, Switzerland's shadow banking sector reduces to (CHF 315

billion) which accounts for 53% of Swiss GDP.69

Switzerland maintains a relatively low risk to financial stability issues related to shadow

banking. This can be attributed to three reasons. First, the size of Switzerland's shadow banking

sector is significantly smaller than its traditional banking sector unlike many other countries and

regions. Second, the assets that are in existence in the shadow banking sector are believed to be of

low to moderate bank-like systemic risk. This means that even in the event of a disruption in the

shadow banking sector, the resulting issues would be minor and very well manageable. Third, bond

funds are other investment funds, which make up 60% of shadow banking assets in Switzerland are

supervised by the Swiss Financial Market Supervisory Authority (FINMA).70

66 (Financial Stability Board, 2014) 67 CHF1.00 = $1.017 USD, XE Currency Conversion 68 (Financial Stability Board, 2014) 69 Id. 70 Id.

34

IV. Financial Stability Board Policy and Regulations

The FSB71 monitors and assesses vulnerabilities affecting the global financial system and

proposes actions needed to address them. In addition, it monitors and advises on market and

systemic developments, and their implications for regulatory policy.72

Transforming shadow banking into resilient market-based financing has been one of the

core elements of the FSB’s regulatory reform agenda to address the fault lines that contributed to

the global financial crisis and to build safer, more sustainable sources of financing for the real

economy.73 Two major issues were made apparent in the aftermath of the financial crisis that were

contributory to the crisis itself. These two issues centered on a heavy reliance of short-term

wholesale funding, a variety of incentive problems in securitized and structured finance markets that

weakened lending standards, and a general lack of transparency that hid growing amounts of

leverage and maturity mismatch, as well as the ultimate bearer of the associated risks.74 As the prices

dropped for securitized assets, the terms for collateralized financing constricted, which then

triggered a fire sales particularly by investors who were significantly mismatched and leveraged. As

the markets grinded up to a halt, several investment vehicles became insolvent and failed, MMMFs

experienced quick panic runs, and the entire shadow banking system came to a screeching halt. The

viability of the banking system was also threatened and the supply of credit to the real economy was

drastically restricted.

The FSB has adopted a two-pronged strategy to deal with these issues, which they call "fault

lines." First, the FSB has created a system-wide monitoring framework to track developments in the

shadow banking system with a view to identifying the build-up of systemic risks and initiating

71 The FSB was established in April 2009 as the successor to the Financial Stability Forum (FSF) 72 (Financial Stability Board, 2015) 73 (Financial Stability Board, November 2014) 74 Id.

35

corrective actions where necessary.75 Second, the FSB is coordinating and contributing to the

development of policy measures in five areas where oversight and regulation needs to be

strengthened to reduce excessive build-up of leverage, as well as maturity and liquidity mismatching

in the system: (i) mitigating risks in banks’ interactions with shadow banking entities; (ii) reducing

the susceptibility of MMFs to “runs”; (iii) improving transparency and aligning incentives in

securitization; (iv) dampening pro-cyclicality and other financial stability risks in securities financing

transactions such as repos and securities lending; and (v) assessing and mitigating financial stability

risks posed by other shadow banking entities and activities.76

a. System wide monitoring

The first prong of the approach to address the issues from the financial crisis as established

by the FSB is the implementation of system wide monitoring. This monitoring assess sources of

systemic risks. The FSB has thus begun conducting annual monitoring exercises to assess global

trends and risks in the shadow banking system. These exercises have prompted an increasing

number of national and regional authorities to regularly assess the risks of their own shadow banking

sectors. The system wide monitoring now covers a total of 25 jurisdictions which represents 80% of

global GDP and 90% of global financial system assets.77 In addition, the FSB’s Regional

Consultative Groups (RCGs) of the Americas and Asia (which include non-FSB member

authorities) have recently started to conduct their own monitoring based on the annual FSB

monitoring exercises.78

75 Id. 76 Id. 77 Several jurisdictions (e.g. Australia, Canada, Germany and the Netherlands) and the European Central Bank (ECB) have also published analyses of their respective shadow banking system, leveraging on the FSB annual monitoring exercises. The International Monetary Fund has conducted some analysis using the data collected in the FSB annual monitoring exercise in their October 2014 Global Financial Stability Report (http://www.imf.org/external/pubs/ft/gfsr/2014/02/pdf/ c2.pdf). 78 (Financial Stability Board, November 2014)

36

The increase in monitoring on a national and regional scale better covers jurisdictions where

shadow banking entities are often located which helps increase the understanding of their operations

and the risks they might contain as well as the benefits to which are applied. As monitoring

continues and improves it is expected that these exercises will continue to benefit from further

improvements in collecting data by jurisdictions and rectify identified data gap inconsistencies.

b. Improved oversight

The second issue the FSB is addressing through its policy recommendations is the improvement of

oversight.79 In coordinating and contributing to the development of policy measures, the FSB has

addressed five areas where oversight and regulation needs to be strengthened to reduce excessive

build-up of leverage, as well as maturity and liquidity mismatching in the system.

i. Mitigating risk in banks’ interactions with shadow banking activities

The financial crisis revealed that both the shadow banking sector and the traditional banking

sector were both intertwined with each other leading to heavy risk exposures. The FSB requested

the Basel Committee on Banking Supervision (BCBS) to develop the policy recommendations to

ensure that future risk spill-over to traditional banks from shadow bank are mitigated.

The BCBS put forth the following recommendations: (i) risk-sensitive capital requirements

for banks’ investments in the equity of funds; and (ii) the supervisory framework for measuring and

controlling banks’ large exposures.80 The first requirement establishes a more consistent and risk-

sensitive approach for computing regulatory capital requirements for banks’ investments in equity of

79 Id. 80 Id.

37

funds, by appropriately reflecting both the risk of the fund’s underlying investments and its leverage.

Implementation goes into effect on 1 January 2017.

The supervisory framework for limiting banks’ large exposures to single counterparties seeks

to protect the traditional banking sector from the risk of default of shadow bank entities. In order to

meet the goal of this framework, the definition of a large exposure is now strengthened to limit

carve outs and exemptions which shadow banks were previously able to take advantage of and to

more clearly and consistently capture exposures to funds, securitization structures and other

vehicles.81 Banks will also be subject to a hard limit on large exposures of 25% of Tier 1 capital (15%