WELFARE, THE EARNED INCOME TAX CREDIT, AND …scholz/Teaching_742/Meyer...WELFARE, THE EARNED INCOME...

52

WELFARE, THE EARNED INCOME TAX CREDIT, AND THE LABOR SUPPLY OF SINGLE MOTHERS* BRUCE D. MEYER AND DAN T. ROSENBAUM During 1984 –1996, welfare and tax policy were changed to encourage work by single mothers. The Earned Income Tax Credit was expanded, welfare bene ts were cut, welfare time limits were added, and welfare cases were terminated. Medicaid for the working poor was expanded, as were training programs and child care. During this same time period there were unprecedented increases in the employment and hours of single mothers. We show that a large share of the increase in work by single mothers can be attributed to the EITC and other tax changes, with smaller shares for welfare bene t cuts, welfare waivers, training programs and child care programs. I. INTRODUCTION Between 1984 and 1996, changes in tax and transfer pro- grams sharply increased the incentive for single mothers to work. During this same period, single mothers began to work more as their weekly employment increased by about six percentage points and their annual employment increased by nearly nine percentage points. Other groups, such as single women without children, married mothers, and black men, did not experience similar gains in employment over this period (see Meyer and Rosenbaum [2000a]). These facts lead us to examine whether the changes in tax and transfer programs were responsible for single mothers working more and what changes were the most important. * We thank Joseph Altonji, Timothy Bartik, Rebecca Blank, Janet Currie, Steven Davis, Jeffrey Liebman, Thomas MaCurdy, Leslie Moscow, Derek Neal, Julie Rosenbaum, Christopher Ruhm, John Karl Scholz, seminar participants at the Association for Public Policy Analysis and Management Annual Meetings, University of California at San Diego, the Federal Reserve Board, the Institute for Research on Poverty, the Manpower Demonstration Research Corporation, the University of Maryland, the National Association for Welfare Research and Sta- tistics Annual Meetings, the National Bureau of Economic Research, the National Tax Association annual meetings, Northwestern University, Syracuse University, Texas A & M University, the Urban Institute, and the University of Wisconsin and many others for comments. We have been greatly aided by help with data and program details by Daniel Feenberg, Linda Giannarelli, Laura Guy, Phillip Le- vine, Robert McIntire, Steve Savner, Jill Schield, and Aaron Yelowitz. Brian Jenn and Christopher Jepsen provided excellent research assistance. This research has been partly supported by the Northwestern University/University of Chicago Joint Poverty Center, the Household International, Inc. Chair in Economics and the National Science Foundation (Meyer), and a Research Training Fellowship in Urban Poverty funded by the National Science Foundation and Northwestern University (Rosenbaum). © 2001 by the President and Fellows of Harvard College and the Massachusetts Institute of Technology. The Quarterly Journal of Economics, August 2001 1063

Transcript of WELFARE, THE EARNED INCOME TAX CREDIT, AND …scholz/Teaching_742/Meyer...WELFARE, THE EARNED INCOME...

WELFARE THE EARNED INCOME TAX CREDIT ANDTHE LABOR SUPPLY OF SINGLE MOTHERS

BRUCE D MEYER AND DAN T ROSENBAUM

During 1984ndash1996 welfare and tax policy were changed to encourage work bysingle mothers The Earned Income Tax Credit was expanded welfare benetswere cut welfare time limits were added and welfare cases were terminatedMedicaid for the working poor was expanded as were training programs and childcare During this same time period there were unprecedented increases in theemployment and hours of single mothers We show that a large share of theincrease in work by single mothers can be attributed to the EITC and other taxchanges with smaller shares for welfare benet cuts welfare waivers trainingprograms and child care programs

I INTRODUCTION

Between 1984 and 1996 changes in tax and transfer pro-grams sharply increased the incentive for single mothers to workDuring this same period single mothers began to work more astheir weekly employment increased by about six percentagepoints and their annual employment increased by nearly ninepercentage points Other groups such as single women withoutchildren married mothers and black men did not experiencesimilar gains in employment over this period (see Meyer andRosenbaum [2000a]) These facts lead us to examine whether thechanges in tax and transfer programs were responsible for singlemothers working more and what changes were the mostimportant

We thank Joseph Altonji Timothy Bartik Rebecca Blank Janet CurrieSteven Davis Jeffrey Liebman Thomas MaCurdy Leslie Moscow Derek NealJulie Rosenbaum Christopher Ruhm John Karl Scholz seminar participants atthe Association for Public Policy Analysis and Management Annual MeetingsUniversity of California at San Diego the Federal Reserve Board the Institute forResearch on Poverty the Manpower Demonstration Research Corporation theUniversity of Maryland the National Association for Welfare Research and Sta-tistics Annual Meetings the National Bureau of Economic Research the NationalTax Association annual meetings Northwestern University Syracuse UniversityTexas A amp M University the Urban Institute and the University of Wisconsinand many others for comments We have been greatly aided by help with data andprogram details by Daniel Feenberg Linda Giannarelli Laura Guy Phillip Le-vine Robert McIntire Steve Savner Jill Schield and Aaron Yelowitz Brian Jennand Christopher Jepsen provided excellent research assistance This research hasbeen partly supported by the Northwestern UniversityUniversity of ChicagoJoint Poverty Center the Household International Inc Chair in Economics andthe National Science Foundation (Meyer) and a Research Training Fellowship inUrban Poverty funded by the National Science Foundation and NorthwesternUniversity (Rosenbaum)

copy 2001 by the President and Fellows of Harvard College and the Massachusetts Institute ofTechnologyThe Quarterly Journal of Economics August 2001

1063

The largest change in the work incentives of single mothersbetween 1984 and 1996 was a tenfold increase in credits throughthe Earned Income Tax Credit (EITC) Only working families(primarily those with children) receive the EITC so its expansionincreased the incentive for single mothers to work We analyzenot only the federal EITC but other federal income tax changesstate income taxes and state EITCs as well The Medicaid pro-gram also greatly expanded during this period Between 1984 and1994 the number of children receiving health coverage throughMedicaid increased 77 percent while the number of coveredadults with dependent children increased 35 percent The expan-sions increased coverage for nonwelfare families with incomesnear the poverty line thus making work more attractive forlow-income single mothers Cash assistance to single parentsthrough Aid to Families with Dependent Children (AFDC) alsochanged quite dramatically over this period Nearly every stateexperimented with changes often under federal waivers of theexisting AFDC rules These changes typically imposed work re-quirements time limits or other measures to encourage singlemothers to work We also investigate the effects of other changesto the AFDC and Food Stamp programs including changes inbenet levels earnings disregards and benet reduction ratesFinally we examine the effects of changes in child care andtraining programs during this period

Our main research strategy identies the effects of thesepolicies on single mothersrsquo labor supply through the differentialtreatment of single mothers and single women without childrenunder welfare and tax laws However the richness of these policychanges allows us to consider additional specications that focuson narrower sources of variation including differences amongsingle mothers in their numbers and ages of children and differ-ences across states in their taxes benets and living costs Thesesources of variation are likely to be unrelated to underlyingdifferences across individuals in their desire to work and thusare likely to be exogenous to labor supply decisions We alsodevelop a new methodology for summarizing the key features ofthe complex nonlinear budget sets created by policies such as theEITC Medicaid and AFDC

Understanding the relationship between the changes in gov-ernment policies and the increases in the labor supply of singlemothers during this period is important for several reasons Firstthese changes in policies provide a plausible source of exogenous

1064 QUARTERLY JOURNAL OF ECONOMICS

variation with which to identify the effects of tax and welfareparameters on labor supply The magnitudes of these effects arekey determinants of the gains or losses from changes in incomeredistribution and social insurance policies

Second understanding the effects of government policiesduring the 1984 ndash1996 period has taken on more importance dueto the passage of the Personal Responsibility and Work Opportu-nity Reconciliation Act of 1996 (PRWORA) In 1997 PRWORAreplaced the main cash assistance program for single mothersAFDC with Temporary Assistance for Needy Families (TANF)The increased state discretion under the new law combined withpolitical changes has led to welfare reform which discourageswelfare receipt and often diverts potential welfare recipients fromtraditional programs These reforms are difcult if not impossibleto characterize using a few variables It is likely that many of thepolicies examined in this paper will be harder and more problem-atic to analyze using post-PRWORA data1

Third there is surprisingly little previous work that esti-mates the effects of the EITC Medicaid or welfare changes onwhether single mothers work The only paper that directly exam-ines how the EITC affects single mothersrsquo labor supply is Eissaand Liebman [1996] which examines the effect of the Tax ReformAct of 19862 In his discussion of the labor supply effects ofMedicaid Moftt [1992] argues that there has been too little workto draw reliable conclusions3 Moftt describes the labor supplyeffect of AFDC as being subject to considerable uncertainty andnotes that the broader labor supply literature has examinedsingle mothers ldquoonly rarelyrdquo4 Dickert Houser and Scholz [1995]argue that this literature provides little guidance as to how theEITC will affect labor market participation and that this omis-sion is especially important because past work suggests that most

1 See Ellwood [2000] National Research Council [1999] and Jencks andSwingle [2000] for related arguments

2 Several papers use labor supply parameters estimated from the negativeincome tax experiments and other sources to simulate the effects of the EITCincluding Hoffman and Seidman [1990] Holtzblatt McCubbin and Gillette[1994] Browning [1995] and Dickert Houser and Scholz [1995] Dickert Houserand Scholz estimate the effect of the after-tax wage and welfare programs onparticipation using a cross section of data from the 1990 panel of the Survey ofIncome and Program Participation (SIPP) They then apply these results tosimulate the effects of the EITC on participation Eissa and Hoynes [1998]examine the effects of the EITC on the labor supply of married couples

3 See Blank [1989] Winkler [1991] and Moftt and Wolfe [1992] in particu-lar The more recent work of Yelowitz [1995] examines the 1988 to 1991 period

4 See Danziger Haveman and Plotnick [1981] and Moftt [1992]

1065THE LABOR SUPPLY OF SINGLE MOTHERS

of the labor supply response is in the work decision rather thanthe hours decision Furthermore there is no work that we areaware of that assesses the overall effect of recent changes intraining and child care programs5 The work on the effects ofwelfare waivers has examined program caseloads rather thanemployment and has reached conicting results6

We examine the major policies affecting the labor supply ofsingle mothers during the 1984 to 1996 period using two datasets the Current Population Survey (CPS) Outgoing RotationGroup Files and the March CPS Files By investigating severalprograms at once using thirteen years of individual data weaccount for their separate effects and we can directly comparethe programs using the same sample time period and methodsOur approach improves on the common past research strategy ofexamining changes in one of these policies in isolation over ashort time period or with a single cross section of data

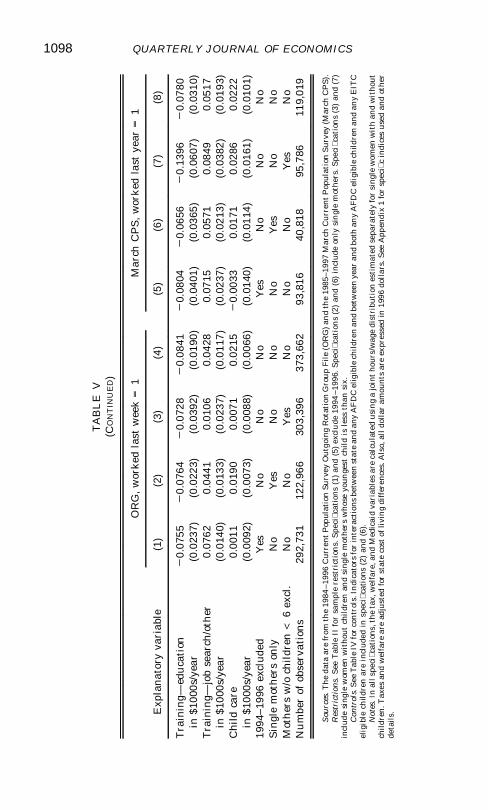

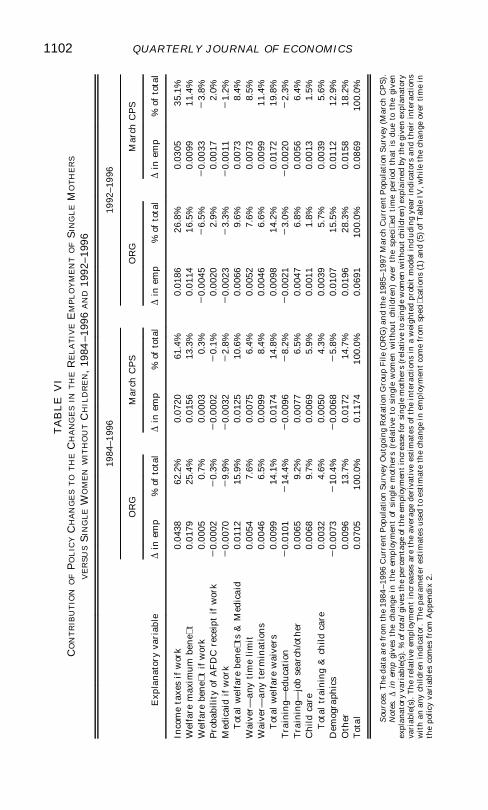

The estimates from our main specications suggest that theEITC and other tax changes account for over 60 percent of the1984 ndash1996 increase in the weekly and annual employment ofsingle mothers (relative to single women without children) Wel-fare waivers and other changes in AFDC account for smaller butstill large shares of the increase for both employment measuresChanges in Medicaid training and child care programs play asmaller role Our estimated effects of tax and EITC changes arefairly robust across time periods and specications We ndlarger effects for less educated women and smaller but stillsubstantial effects when we compare changes for single motherswith different numbers of children Some of these identicationstrategies result in much weaker AFDC effects The effects ofother policies on employment tend not to vary much by specica-tion Additionally we nd that the effects of the policies on totalhours worked are very similar to the employment results

The structure of the paper is as follows Section II provides atheory of the decision to work and states our main modelingchoices We describe the two data sets used in the empirical workin Section III Section IV describes the main program changes

5 See Gueron and Pauly [1991] for a review of training programs for welfarerecipients and Council of Economic Advisers [1997] for a review of work on theeffects of child care

6 See Levine and Whitmore [1998] Martini and Wiseman [1997] Blank[1997] and Ziliak et al [1997] for differing views of the relative importance ofwelfare waivers economic conditions and benet cuts in the recent decline inwelfare receipt

1066 QUARTERLY JOURNAL OF ECONOMICS

over the 1984 to 1996 period that affected the labor supply ofsingle mothers We also provide summary statistics on programchanges discuss their theoretical impacts on labor supply andintroduce variables that measure particular policies Section Vcompares the employment rates and other characteristics of sin-gle mothers and single women without children Section VI in-vestigates how the employment of single mothers was affected bythe policies we study We also examine alternative explanationsfor our results and briey examine hours worked Section VIIprovides an accounting of the contribution of different policychanges to the overall increase in employment of single mothersin recent years We then offer conclusions in Section VIII

II MODELING THE WORK DECISION

Our modeling approach combines some of the best aspects ofstructural methods and quasi-experimental or natural experi-ment type approaches Beginning from a structural approachclaries which variables should enter the work decision and theform in which they should enter Our simple structural modelalso allows us to test some fundamental economic predictions andmore convincingly simulate policy changes7 The quasi-experi-mental methods make transparent the assumptions that allowthe identication of our key coefcients By the appropriate use ofcontrol variables and simplifying assumptions we identify ourkey parameters using only the sources of variation in our ex-planatory variables that we believe are exogenous

We focus on employment because previous work has foundthat women are more responsive to wages and income in thedecision to work than in the hours decision (see Heckman [1993])The probability that a single woman works is just the probabilitythat the expected utility when working Uw exceeds the expectedutility when not working Un w ie Pr[Uw gt Unw ] We takeutility to be a function of income Y nonmarket time L an indi-cator for welfare participation P (which captures transactioncosts or stigma) other demographic and other control variablesX and an additive stochastic term e Thus the probability ofwork is just

7 Because of the simplications we make to improve the modelrsquos tractabilityone may not want to consider our approach fully structural As with any struc-tural model simulations that rely heavily on simplifying assumptions may givemisleading results

1067THE LABOR SUPPLY OF SINGLE MOTHERS

(1) Pr[U(Yw Lw Pw X) U(Ynw Lnw Pnw X)]where the randomness in this event comes from the stochasticterm e

Income when working is pretax earnings minus taxes plusAFDC and Food Stamps plus Medicaid benets Income whennot working is the maximum AFDCFood Stamp benet andMedicaid benets In each case we calculate the earnings taxesand benets for a given individual incorporating family composi-tion (number and ages of children) and characteristics of stateand federal policies at the time We calculate real income andbenets across states using a cost of living index that depends onstate housing costs The decision to work should depend on thereal return to work not the nominal return8

A key issue in implementing this approach is the form of theuncertainty about a womanrsquos wage and hours should she work Inthe estimates reported here we take a woman to have no moreknowledge of her potential wage and hours than we do as re-searchers9 Thus we take her wage to be a random draw from adistribution (to be specied below) and her hours worked to be arandom draw from a distribution (also to be specied below) thatis conditional on the wage realization Then the probability ofworking is just

(2) PrE[Uw] Unwwhere the expectation here is over the joint wage and hoursdistribution

To estimate equation (2) we take the distribution of e to benormal and take U to be linear in income and nonmarket time (wehave relaxed this latter assumption in other work) In the linearcase (2) has a very simple form

(3) Pra (E[Yw] 2 Ynw) 1 b (E[Lw] 2 Lnw)

2 r (E[Pw] 2 Pnw) 1 X 9 g e nw 2 e wwhere X is other variables that may affect the work decision such

8 Our base specication includes a state cost of living adjustment followingthe approach of National Research Council [1995] One can argue that housingcosts largely reect local amenities However to the extent that these amenitiesare largely xed benets of an area one would still want to account for statedifferences in housing costs when calculating the value of additional income

9 We have also considered two alternatives 1) a woman knows her wage andhours before choosing to work and 2) a woman knows her wage but not her hoursbefore choosing to work Our experiments with these alternatives yielded resultsqualitatively similar to our main results

1068 QUARTERLY JOURNAL OF ECONOMICS

as demographic variables and characteristics of state welfarewaivers training programs and child care programs This speci-cation also allows xed costs of work which vary across demo-graphic groups Under the normality assumption (3) can be re-written as

(4) F a (E[Yw] 2 Ynw) 1 b (E[Lw] 2 Lnw) 2 r (E[Pw] 2 Pnw) 1 X 9 g We make the simplifying assumption that nonworking singlemothers participate in welfare and that working single mothersparticipate if their earnings are low enough to qualify them foraid This assumption is clearly a simplication as some womenwho qualify for aid will not participate because of the transactioncosts or stigma of doing so Past work on program takeup sug-gests that about 75 percent of those eligible for AFDC and about50 percent of those eligible for Food Stamps participate (for arecent review of past work see Blank and Ruggles [1996]) How-ever AFDC takeup rates between 80 and 90 percent are probablycloser to the truth given the underreporting of welfare receipt instandard data sets (see Bavier [1999]) We also assume that allsingle women without children do not participate in welfare pro-grams10

We generalize (4) by allowing the coefcients on the differentcomponents of income to differ since income from differentsources may be valued differently For example we allow theeffect of welfare income (AFDC plus Food Stamps) to differ fromthat of labor income taxes paid and Medicaid coverage Welfareincome may be valued less than labor income because of a vari-able component to the transaction costs or stigma of welfareparticipation (see Moftt [1983]) Medicaid may be valued at lessthan our calculated cost because it is an in-kind transfer or morethan cost because of its insurance component These separatecoefcients on different income terms allow for additional tests ofthe hypothesis that increases in the return to work make workmore likely and they allow an approach that is less restrictiveie less likely to yield biased estimates

We assume that all single mothers face the same pretax wage

10 The primary program for which single women without children would beeligible is Food Stamps Single adults with children are more than ten times aslikely to receive Food Stamps as single adults without children (authorsrsquo calcula-tions and U S Department of Agriculture [1995]) Furthermore since the FoodStamp program has not changed much over time and does not differ much by stateexcept for interactions with AFDC our control variables below (particularly yearand number of children dummies) should account for most of these differences

1069THE LABOR SUPPLY OF SINGLE MOTHERS

and hours distribution and we make the same assumption forsingle childless women We estimated some specications thatused a wagehours distribution that varied with demographicsalthough these results are not reported here (see Meyer andRosenbaum [1999]) Thus expected earnings if working only varywith the controls and are absorbed by X which includes variablesfor the presence and number of children age education stateyear and other variables described fully below Similarly non-market time when working and not working E[Lw ] and Lnw respectively are taken to be constant or to vary with X and thusare absorbed by X Pn w which identically equals 1 is absorbedinto the constant We then obtain the employment probability

(5) F a 1E[taxes] 1 a 2E[AFDC and Food Stamp benefits if work]

1 a 3E[Medicaid coverage if work valued at cost]

2 a 4maximum AFDCFood Stamp benefit

2 a 5Medicaid coverage if do not work valued at cost

1 r E[Pw] 1 X 9 g

We allow the tax and welfare variables in (5) to vary withyear state and the number and ages of children To implementthis approach we discretize the wage and hours distribution andperform the numerical integration required in (5) allowing thehours distribution to vary with the wage level because of thepronounced dependence between the two distributions To calcu-late the wage and hours distribution we pool 1984 ndash1996 MarchCPS data and estimate one distribution that we use for all yearsWe do this separately for single mothers and single childlesswomen We approximate these distributions using cells denedby 50 intervals of the joint wage and hours distribution (seeAppendix 1 for details) Our approach is both tractable and yetable to capture the fairly complex and highly nonlinear budgetconstraints of low income single mothers These complexities aredescribed in detail in Section IV

III DATA

The data used in this paper come from the Current Popula-tion Survey (CPS) a nationally representative monthly survey ofapproximately 60000 households We use two types of the CPSdata the March CPS Files and the merged Outgoing Rotation

1070 QUARTERLY JOURNAL OF ECONOMICS

Group (ORG) data During each interview household membersare asked whether they worked last week and their hoursworked as well as many other questions In the March inter-views individuals are asked to provide detailed retrospectiveinformation including hours earnings and weeks worked duringthe previous year The ORG les come from all twelve months ofthe year but only include the same person once in a given yearThe March CPS data are from the 1985ndash1997 interviews andtherefore provide information on the years 1984 ndash1996 The ORGdata are from 1984 ndash1996 We limit the sample to single women(widowed divorced and never married) who are between 19 and44 years old and not in school In the March CPS women whowere ill or disabled during the previous year or who had positiveearned income but zero hours of work are also excluded Theresulting samples sizes are 373662 for the ORG and 119019 forthe March CPS

IV THE POLICY CHANGES AND LABOR SUPPLY

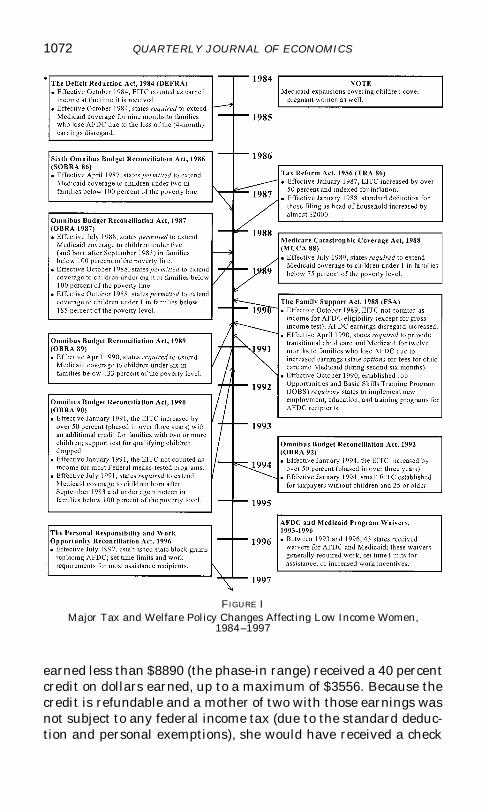

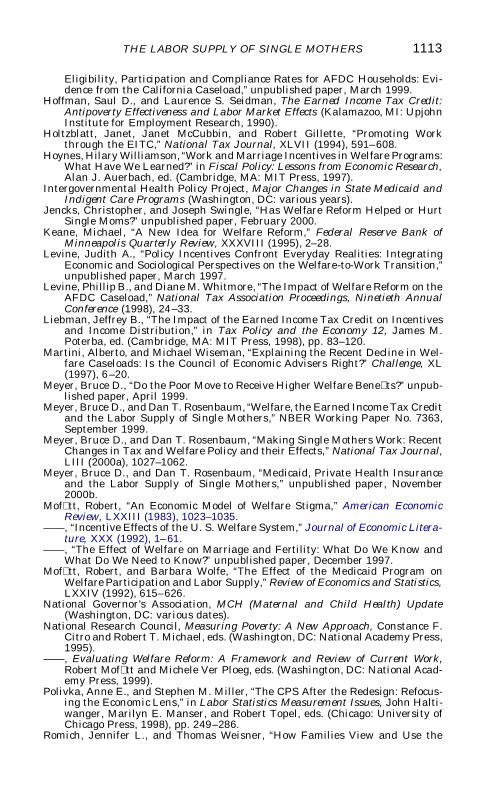

In this section we describe the major policy changes between1984 and 1996 that affected the labor supply of single mothersFor each policy or program we rst provide some brief back-ground information and outline the major changes between 1984and 1996 (see Figure I for a time line depicting these changes)Next we describe the policy variables used in the empirical workto summarize the incentive effects of these programs Finally weanalyze the theoretical effects of these changes on labor supplyespecially on the choice of whether or not to work An in-depthdiscussion of the policy changes is in Meyer and Rosenbaum[2000a]

A The EITC and Federal and State Income Taxes

In our period the most important changes in work incentivesfor single mothers probably came from the Earned Income TaxCredit11 EITC credits increased fteenfold from $16 billion in1984 to a projected $251 billion in 1996 Single parents receivedabout two-thirds of these EITC dollars (see U S House of Rep-resentatives Green Book [1996] U S Department of the Trea-sury SOI [1999]) In 1996 a single woman with two children who

11 See Liebman [1998] for a history of the EITC and a survey of many of thekey economic issues

1071THE LABOR SUPPLY OF SINGLE MOTHERS

earned less than $8890 (the phase-in range) received a 40 percentcredit on dollars earned up to a maximum of $3556 Because thecredit is refundable and a mother of two with those earnings wasnot subject to any federal income tax (due to the standard deduc-tion and personal exemptions) she would have received a check

FIGURE IMajor Tax and Welfare Policy Changes Affecting Low Income Women

1984ndash1997

1072 QUARTERLY JOURNAL OF ECONOMICS

from the IRS for the credit amount With additional earnings upto $11610 the credit amount did not change Additional earningsbeyond $11610 and up to $28495 (the phase-out range) resultedin a reduction in the credit by 2106 percent of the additionalearnings until the credit was reduced to zero This credit sched-ule meant that a woman with two children earning between$5000 and just under $19000 received at least a $2000 credit

The current EITC is the result of several legislative changes(summarized in Figure I) which greatly expanded the EITC after1984 Between its beginning in 1975 and the passage of the TaxReform Act of 1986 (TRA86) the EITC was small and the creditamounts did not keep up with ination Beginning with theTRA86 the EITC was expanded in a number of dimensions Firstcredit rates phase-in ranges and phase-out ranges were in-creased considerably Second in 1991 the credit was expanded toprovide a larger credit for families with two or more children12

The increment to the maximum credit for a second child wassmall through 1993 but beginning in 1994 the difference began torise sharply it rose to $490 in 1994 $1016 in 1995 and $1404 in1996 Third in 1991 the requirements for qualifying childrenwere changed in a way that tended to increase eligibility

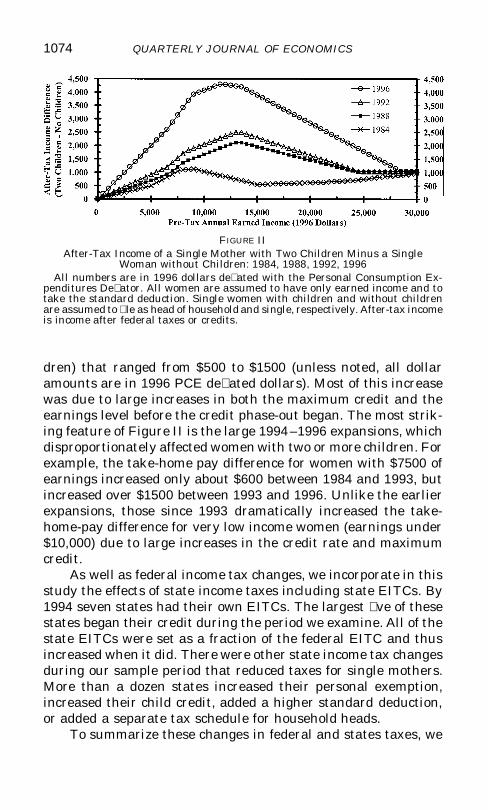

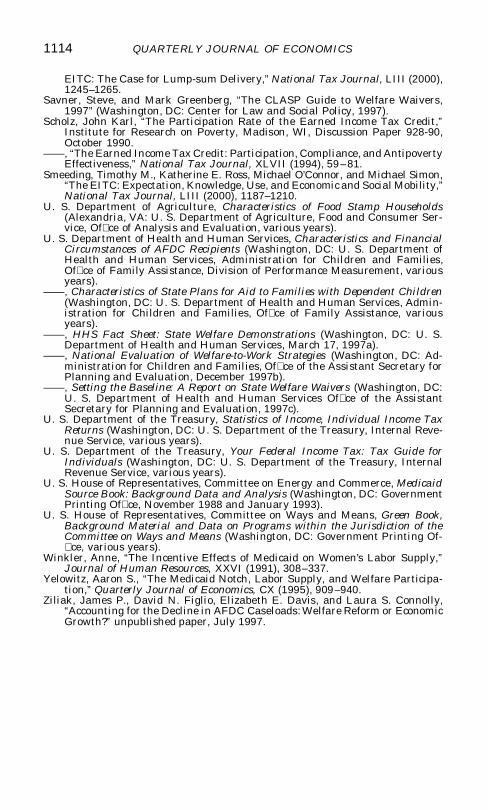

The after-tax incomes of single women were affected by otherchanges in federal income taxes during this period such as the1987 increase in the personal exemption and the 1988 increase inthe standard deduction for household heads To illustrate theoverall changes in after-tax incomes we plot in Figure II thedifference in after-tax income (earnings minus federal incometaxes plus the EITC) between a woman with two children and awoman with no children for various pretax earnings levels in1984 1988 1992 and 199613

Figure II illustrates several important aspects of the EITCexpansions First between 1984 and 1988 single mothers of twowith earnings between $10000 and $20000 experienced in-creases in take-home pay (relative to single women without chil-

12 There were other small program changes From 1991 through 1993 therewere small refundable credits for child health insurance premiums and for chil-dren under one Beginning in January 1991 the EITC was not counted as incomein most means-tested programs increasing its value for very low income women

13 Changes over time in this difference were almost entirely due to changesin the taxes paid (or credits received) by single mothers as can be seen in panel 1of Table I The taxes paid by single women without children hardly changedbetween 1984 and 1996 especially for earnings levels between $10000 and$20000

1073THE LABOR SUPPLY OF SINGLE MOTHERS

dren) that ranged from $500 to $1500 (unless noted all dollaramounts are in 1996 PCE deated dollars) Most of this increasewas due to large increases in both the maximum credit and theearnings level before the credit phase-out began The most strik-ing feature of Figure II is the large 1994 ndash1996 expansions whichdisproportionately affected women with two or more children Forexample the take-home pay difference for women with $7500 ofearnings increased only about $600 between 1984 and 1993 butincreased over $1500 between 1993 and 1996 Unlike the earlierexpansions those since 1993 dramatically increased the take-home-pay difference for very low income women (earnings under$10000) due to large increases in the credit rate and maximumcredit

As well as federal income tax changes we incorporate in thisstudy the effects of state income taxes including state EITCs By1994 seven states had their own EITCs The largest ve of thesestates began their credit during the period we examine All of thestate EITCs were set as a fraction of the federal EITC and thusincreased when it did There were other state income tax changesduring our sample period that reduced taxes for single mothersMore than a dozen states increased their personal exemptionincreased their child credit added a higher standard deductionor added a separate tax schedule for household heads

To summarize these changes in federal and states taxes we

FIGURE IIAfter-Tax Income of a Single Mother with Two Children Minus a Single

Woman without Children 1984 1988 1992 1996All numbers are in 1996 dollars deated with the Personal Consumption Ex-

penditures Deator All women are assumed to have only earned income and totake the standard deduction Single women with children and without childrenare assumed to le as head of household and single respectively After-tax incomeis income after federal taxes or credits

1074 QUARTERLY JOURNAL OF ECONOMICS

calculate a variable called Income Taxes if Work This variable isthe expected taxes a woman would pay in a given state and yearwith a given family composition and ages of children The expec-tation is calculated by integrating over the wage and hours dis-tribution of single women as described in Section II Appendix 2reports the mean of this variable for single mothers and singlewomen without children for various years Over the years 1984 ndash1996 taxes paid by single mothers relative to single women with-out children fell by $1607 Thirty-nine percent of the relative fallin taxes (increase in credits) occurred in the last three years(1993ndash1996) About 43 percent occurred in 1987 and 1988 with18 percent occurring between 1991 and 1993 Almost all of the fallin relative taxes was due to federal tax changes Only $37 wasdue to state taxes with all but $7 of this due to state EITCsHowever in the seven states with state EITCs the role of statetaxes was much greater In these jurisdictions state EITCs ac-counted for a $215 drop in the taxes of single mothers relative tosingle women without children

The theoretical effect of the EITC expansions on the annualparticipation decision of single parents is unambiguously posi-tive Since the EITC expansions have increased the after-taxreturn to work at all earnings levels work is unambiguouslymore attractive The effect of the EITC and its expansions on thehours of work among those working is much less clear and de-pends on where a person would choose to work on the pre- andpostcredit budget sets Overall the income effect of the creditcombined with the negative substitution effect that people face onthe phase-out portion of the credit is expected to reduce the hoursof those who work14

B AFDC Food Stamps and Waivers

The two programs that have been most commonly thought ofas welfare are Aid to Families with Dependent Children (AFDC)and Food Stamps We discuss Food Stamps along with AFDC

14 One might wonder whether households are aware of these tax incentivesand bother to le tax returns Awareness appears to be high [Romich and Weisner2000 Smeeding et al 2000] and EITC takeup appears to be high and risingScholz [1990 1994] estimates takeup to be 75 percent in 1988 and between 80 and86 percent in 1990 With the increases in the EITC after 1990 that raised thevalue of ling and disproportionately made eligible moderate income people whoare likely to le one might expect that the participation rate rose further Inaddition EITC awareness and outreach has increased in recent years On theother hand recent compliance efforts may have discouraged some potential lers

1075THE LABOR SUPPLY OF SINGLE MOTHERS

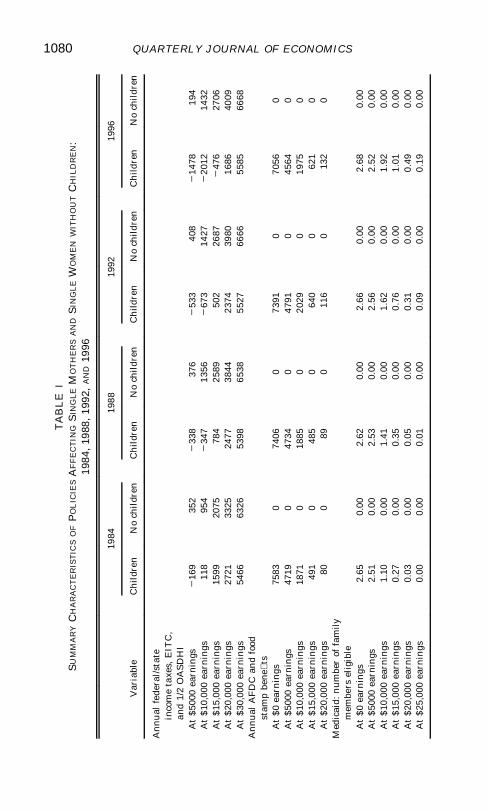

because nearly 90 percent of AFDC recipients also received FoodStamps [U S House of Representatives 1996] The AFDC pro-gram provided cash payments to families with children who havebeen deprived of support due to the absence or unemployment ofa parent The Food Stamp program provides low-income house-holds with coupons to purchase food AFDC program parameterswere set by the states while most Food Stamp parameters are thesame in all states Nevertheless because of the interaction of theeligibility and benet calculations of the two programs there areinterstate differences in the Food Stamps received for people insimilar situations Both of these programs are large relative toother means-tested programs with 1996 AFDC and Food Stampexpenditures totaling $237 billion and $255 billion respectivelyBoth had growing expenditures and caseloads in the late 1980sand early 1990s with peaks in scal year 1994

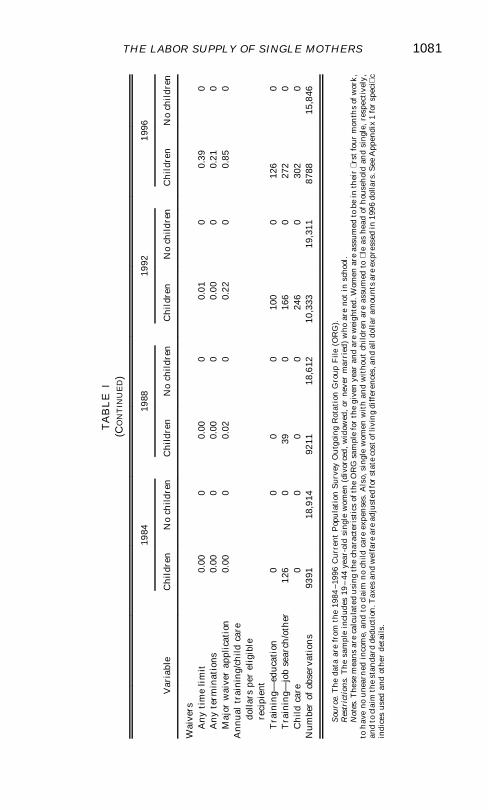

While much past work has summarized the AFDC and FoodStamp programs using the combined maximum benet this mea-sure ignores the large interstate differences and changes overtime in earnings exemptions and implicit tax rates By 1996fteen states had exemptions and tax rates that differed from thestandard $120 earnings exemption and the two-thirds implicittax rate We summarize AFDC and Food Stamps with threevariables implied by our theoretical model the maximum com-bined benet expected benets if a person works and the prob-ability of AFDC receipt (which captures transaction costs orstigma) Due to cuts in AFDC the mean maximum combinedAFDC and Food Stamp benet fell about 7 percent over thesample period Over the same period mean benets for a workingsingle mother remained roughly constant as implicit tax rateswere reduced

Theory predicts that the AFDC and Food Stamp programsdecrease labor supply for two reasons First the income effect ofthe guarantee amount (maximum benet) should make employ-ment less likely and reduce hours worked if a woman worksSecond the implicit tax rate resulting from reductions in benetsas earnings increase (captured by reductions in the benets ifwork variable) also reduces the incentive to work Thus AFDCshould decrease both the likelihood of working and hours condi-tional on working However in interpreting our estimates belowone should bear in mind that substantial research indicates thatactual exemptions and implicit tax rates differ from the statutory

1076 QUARTERLY JOURNAL OF ECONOMICS

ones15 Consequently our calculations of AFDC benets for thosewho work may be fairly rough We will return to this issue inSection VI

Under AFDC the Secretary of Health and Human Services(HHS) was authorized to waive specied program requirementsto allow states to experiment This waiver authority was rarelyused prior to the late 1980s but its use accelerated under Presi-dents Bush and Clinton Between January 1993 and August1996 HHS approved welfare waivers in 43 states While statesexperimented with changes in nearly every aspect of AFDCmany provisions applied to small parts of states or would not beexpected to have a substantial effect on the employment of singlemothers We focus on a few types of waiver provisions that weretried in many states Our main welfare waiver variables are AnyTime Limit which equals one for single mothers in states thatimposed work requirements or benet reductions on those whoreached time limits and Any Terminations which equals one forany single mother in a state in which a welfare case had beenterminated under a welfare waiver Some common types of pro-visions such as expanded income disregards have been incorpo-rated in our coding of the AFDC program Others such as familycaps (which limited the benets for additional children) or in-creased resource limits (which loosened the asset restrictions forAFDC eligibility) likely have small or ambiguous effects on em-ployment and are therefore not included

In this paper we focus on implementation dates and actualbeginning dates of terminations instead of application or ap-proval dates We also examine a dummy variable for states thatapplied for a major statewide waiver in case this indicates atightening of administrative requirements in a state These vari-ables are interacted with an indicator for whether a woman haschildren In Table I we report the fraction of single women livingin states that have applied for or implemented various types ofwaivers Very few women were in states that had implementedsignicant waivers through at least 1994 The fraction of womenin states that had made a major waiver application was muchhigher 022 in 1992 and 085 in 1996

15 See Fraker Moftt and Wolf [1985] and Levine [1997] Other researchindicates that few AFDC recipients report their income to welfare ofces [Edinand Lein 1997 Hill et al 1999]

1077THE LABOR SUPPLY OF SINGLE MOTHERS

C Medicaid

Medicaid is the biggest and most costly program that aidssingle mothers and their children In 1994 $309 billion wasspent on 248 million nonaged nondisabled Medicaid recipients agroup that was predominantly single mothers and their children[U S House of Representatives Green Book 1996 pp 897ndash902]Unlike the Food Stamp program and especially AFDC Medicaideligibility has expanded dramatically since 1984 resulting in amore than threefold increase between 1984 and 1994 in Medicaidexpenditures on families with dependent children (and a 60 per-cent increase in the caseload) Prior to 1987 Medicaid eligibilityfor single mothers and their children generally required receipt ofAFDC In a series of expansions Medicaid coverage was extendedto low-income pregnant women and children (again see Figure I)The differences across states in the extent to which they tookadvantage of the permitted coverage options generated largedifferences in who was covered in different years in differentstates Moreover state AFDC income limits interacted with theMedicaid expansions to determine the additional families covered(see Meyer and Rosenbaum [2000b] for more details)

We measure Medicaid benets by rst calculating the num-ber of adults and children in the family that would be covered ifa woman works We then convert these numbers to dollar valuesusing Medicaid expenditures per child and adult averaged overall states and years16 As can be seen in Table I there was a fairlysteady increase over our sample period in the number of familymembers covered under Medicaid if a single mother works

The theoretical effect of Medicaid expansions on the decisionto work is positive since those newly covered are those withearnings that would make them ineligible for AFDC The Med-icaid expansions also could result in some working women in-creasing their hours if pre-expansion earnings limits resulted inthem reducing their hours of work in order to qualify for Medicaidcoverage Overall the effect on hours conditional on working isambiguous since the expansions also could result in hours de-creases for women who choose to reduce their hours in order toqualify for Medicaid coverage for their children

16 Note that in our specications Medicaid coverage for the nonworking iscollinear with family size and number of children controls so a 5 is not estimated

1078 QUARTERLY JOURNAL OF ECONOMICS

D Training and Child Care Programs

To capture the effect of training programs on the probabilityof work by single mothers we focus on the programs specicallyfor AFDC applicants and recipients rst the Work Incentives(WIN) program and then the Job Opportunities and Basic Skills(JOBS) program Total expenditures as well as the emphasis ofthese programs changed sharply over our period (see Table I) Weconstruct two variables that measure the character and extent ofthe JOBS and WIN programs in a state and year Because edu-cational spending is likely to have a different effect than otherspending we split expenditures into education and job searchother We scale state expenditures by the size of the AFDCmandatory population These variables are interacted with anindicator for whether a woman would be required to participate inJOBS or WIN (based on the age of her youngest child these rulesdiffered across states and over time) so that these variables equalzero for single women without children or with children under theage cutoff

The effects of these training programs on labor supply likelydepends on the mix of services provided and the stringency of theparticipation requirements Job search assistance job place-ments and improving job skills and readiness should lower jobsearch costs thereby increasing the level of work for womentrainees On the other hand even with a benecial long-termeffect on wages or employment secondary or postsecondary edu-cation may delay entry into the workforce while women takeclasses leading to a short-term negative employment effect Inany case there is much stronger evidence of employment effectsfrom job search assistance than from education at least in theshort run17

The cost and quality of child care is likely to have an impor-tant effect on whether a woman works The federal role in childcare for low-income women expanded greatly following the Fam-ily Support Act of 1988 and the Omnibus Budget ReconciliationAct of 1990 Four large programs started during this periodAFDC Child Care Transitional Child Care At-Risk Child Careand Child Care and Development Block Grants We focus onthese programs because they are particularly important for singlemothers and they were the main changes over our period Total

17 See Gueron and Pauly [1991] and U S Department of Health andHuman Services [1997b]

1079THE LABOR SUPPLY OF SINGLE MOTHERS

TA

BL

EI

SU

MM

AR

YC

HA

RA

CT

ER

IST

ICS

OF

PO

LIC

IES

AF

FE

CT

ING

SIN

GL

EM

OT

HE

RS

AN

DS

ING

LE

WO

ME

NW

ITH

OU

TC

HIL

DR

EN

19

841

988

1992

A

ND

1996

Var

iabl

e

1984

1988

1992

1996

Ch

ildr

enN

och

ildr

enC

hil

dren

No

chil

dren

Ch

ildr

enN

och

ildr

enC

hil

dren

No

chil

dren

An

nu

alfe

dera

lst

ate

inco

me

taxe

sE

ITC

an

d1

2O

AS

DH

IA

t$5

000

earn

ings

216

935

22

338

376

253

340

82

1478

194

At

$10

000

earn

ings

118

954

234

713

562

673

1427

220

1214

32A

t$1

500

0ea

rnin

gs15

9920

7578

425

8950

226

872

476

2706

At

$20

000

earn

ings

2721

3325

2477

3844

2374

3980

1686

4009

At

$30

000

earn

ings

5466

6326

5398

6538

5527

6666

5585

6668

An

nu

alA

FD

Can

dfo

odst

amp

bene

ts

At

$0ea

rnin

gs75

830

7406

073

910

7056

0A

t$5

000

earn

ings

4719

047

340

4791

045

640

At

$10

000

earn

ings

1871

018

850

2029

019

750

At

$15

000

earn

ings

491

048

50

640

062

10

At

$20

000

earn

ings

800

890

116

013

20

Med

icai

dn

um

ber

offa

mil

ym

embe

rsel

igib

leA

t$0

earn

ings

265

000

262

000

266

000

268

000

At

$500

0ea

rnin

gs2

510

002

530

002

560

002

520

00A

t$1

000

0ea

rnin

gs1

100

001

410

001

620

001

920

00A

t$1

500

0ea

rnin

gs0

270

000

350

000

760

001

010

00A

t$2

000

0ea

rnin

gs0

030

000

050

000

310

000

490

00A

t$2

500

0ea

rnin

gs0

000

000

010

000

090

000

190

00

1080 QUARTERLY JOURNAL OF ECONOMICS

TA

BL

EI

(CO

NT

INU

ED

)

Var

iabl

e

1984

1988

1992

1996

Ch

ildr

enN

och

ildr

enC

hil

dren

No

chil

dren

Ch

ildr

enN

och

ildr

enC

hil

dren

No

chil

dren

Wai

vers

An

yti

me

lim

it0

000

000

00

010

039

0A

ny

term

inat

ions

000

00

000

000

00

210

Maj

orw

aive

rap

plic

atio

n0

000

002

00

220

085

0A

nn

ual

trai

nin

gch

ild

care

doll

ars

per

elig

ible

reci

pien

tT

rain

ingmdash

edu

cati

on0

00

010

00

126

0T

rain

ingmdash

job

sear

cho

ther

126

039

016

60

272

0C

hil

dca

re0

00

024

60

302

0N

um

ber

ofob

serv

atio

ns

9391

189

1492

1118

612

103

3319

311

8788

158

46

Sou

rce

The

data

are

from

the

1984

ndash199

6C

urre

ntP

opu

lati

onS

urve

yO

utg

oing

Rot

atio

nG

roup

File

(OR

G)

Res

tric

tion

sT

hesa

mpl

ein

clud

es19

ndash44

year

-old

sing

lew

omen

(div

orce

dw

idow

ed

orne

ver

mar

ried

)w

hoar

eno

tin

scho

ol

Not

esT

hese

mea

nsar

eca

lcu

late

du

sing

the

char

acte

rist

ics

ofth

eO

RG

sam

ple

for

the

give

nye

aran

dar

ew

eigh

ted

Wom

enar

eas

sum

edto

bein

thei

rr

stfo

urm

onth

sof

wor

kto

hav

eno

une

arn

edin

com

ean

dto

clai

mn

och

ildca

reex

pen

ses

Als

osi

ngle

wom

enw

ith

and

wit

hout

chil

dren

are

assu

med

tol

eas

head

ofh

ouse

hol

dan

dsi

ngle

res

pect

ivel

yan

dto

clai

mth

est

anda

rdde

duct

ion

Tax

esan

dw

elfa

rear

ead

just

edfo

rst

ate

cost

ofli

vin

gdi

ffer

ence

san

dal

ldol

lar

amou

nts

are

expr

esse

din

1996

dolla

rsS

eeA

ppen

dix

1fo

rsp

eci

cin

dice

sus

edan

dot

her

deta

ils

1081THE LABOR SUPPLY OF SINGLE MOTHERS

state and federal expenditures on these four new federal pro-grams by state and year are scaled by the number of singlemothers with children under six These numbers can be seen inTable I which shows a steep rise in child care expendituresbetween 1988 and 1992 followed by a slower rise in later yearsFor more detail on training and child care programs see Meyerand Rosenbaum [1999]

V THE DETERMINANTS OF EMPLOYMENT

We use several different econometric methods to identify theimpact of the recent policy changes on the employment of singlemothers We begin with the familiar difference in differencesestimator This approach compares employment rates over timefor single mothers with those for single women without childrenThis approach is the one taken by Eissa and Liebman [1996] intheir study of the EITC over the 1984 to 1990 period We waituntil Section VI to discuss the estimates from our simple struc-tural model

A Employment Rates of Single Mothers and Single ChildlessWomen

The top panel of Table II reports the employment rates ofsingle mothers and single women without children along withthe difference in employment rates between these two groups ofsingle women We report this difference because many determi-nants of employment that change over time especially wages andmacroeconomic conditions might be expected to affect all singlewomen similarly Other determinants of employment particu-larly the tax and transfer programs that we examine specicallyaffect single mothers The bottom panel of Table II focuses on thesubsample of single mothers with children under six (again rela-tive to single women without children) a group we expect to bemore responsive to changes in the rewards to work Also employ-ment changes are likely to have greater effects on children forbetter or worse when they are young and their mother likelyplays a larger role in their care and education

We report two different measures of employment whether awoman worked last week (from the ORG data) and whether awoman worked at all last year (from the March data) Eachmeasure has its advantages Whether a woman worked last weekis probably a better measure of labor supply to use as an input to

1082 QUARTERLY JOURNAL OF ECONOMICS

policy decisions since its average captures the fraction of womenworking in a given week This variable will be especially useful ifthose who move in or out of the workforce on the margin workonly a few weeks during the year On the other hand as discussedearlier the EITC unequivocally increases the probability of work-

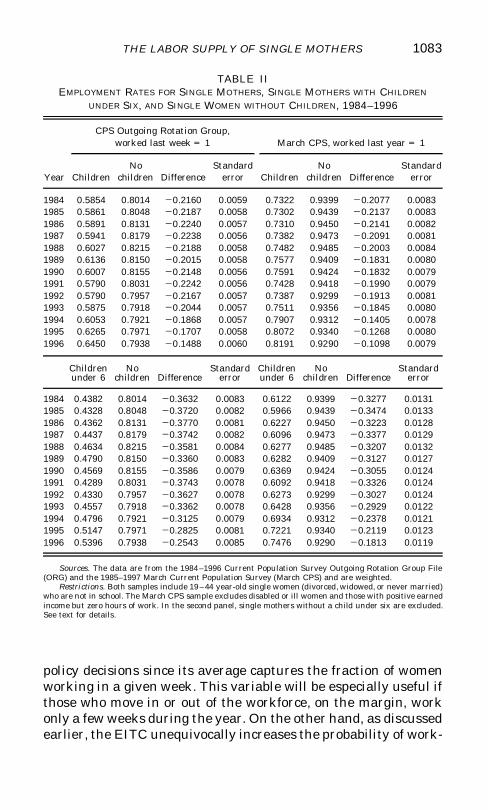

TABLE IIEMPLOYMENT RATES FOR SINGLE MOTHERS SINGLE MOTHERS WITH CHILDREN

UNDER SIX AND SINGLE WOMEN WITHOUT CHILDREN 1984ndash1996

Year

CPS Outgoing Rotation Groupworked last week = 1 March CPS worked last year = 1

ChildrenNo

children DifferenceStandard

error ChildrenNo

children DifferenceStandard

error

1984 05854 08014 2 02160 00059 07322 09399 2 02077 000831985 05861 08048 2 02187 00058 07302 09439 2 02137 000831986 05891 08131 2 02240 00057 07310 09450 2 02141 000821987 05941 08179 2 02238 00056 07382 09473 2 02091 000811988 06027 08215 2 02188 00058 07482 09485 2 02003 000841989 06136 08150 2 02015 00058 07577 09409 2 01831 000801990 06007 08155 2 02148 00056 07591 09424 2 01832 000791991 05790 08031 2 02242 00056 07428 09418 2 01990 000791992 05790 07957 2 02167 00057 07387 09299 2 01913 000811993 05875 07918 2 02044 00057 07511 09356 2 01845 000801994 06053 07921 2 01868 00057 07907 09312 2 01405 000781995 06265 07971 2 01707 00058 08072 09340 2 01268 000801996 06450 07938 2 01488 00060 08191 09290 2 01098 00079

Childrenunder 6

Nochildren Difference

Standarderror

Childrenunder 6

Nochildren Difference

Standarderror

1984 04382 08014 2 03632 00083 06122 09399 2 03277 001311985 04328 08048 2 03720 00082 05966 09439 2 03474 001331986 04362 08131 2 03770 00081 06227 09450 2 03223 001281987 04437 08179 2 03742 00082 06096 09473 2 03377 001291988 04634 08215 2 03581 00084 06277 09485 2 03207 001321989 04790 08150 2 03360 00083 06282 09409 2 03127 001271990 04569 08155 2 03586 00079 06369 09424 2 03055 001241991 04289 08031 2 03743 00078 06092 09418 2 03326 001241992 04330 07957 2 03627 00078 06273 09299 2 03027 001241993 04557 07918 2 03362 00078 06428 09356 2 02929 001221994 04796 07921 2 03125 00079 06934 09312 2 02378 001211995 05147 07971 2 02825 00081 07221 09340 2 02119 001231996 05396 07938 2 02543 00085 07476 09290 2 01813 00119

Sources The data are from the 1984ndash1996 Current Population Survey Outgoing Rotation Group File(ORG) and the 1985ndash1997 March Current Population Survey (March CPS) and are weighted

Restrictions Both samples include 19ndash44 year-old single women (divorced widowed or never married)who are not in school The March CPS sample excludes disabled or ill women and those with positive earnedincome but zero hours of work In the second panel single mothers without a child under six are excludedSee text for details

1083THE LABOR SUPPLY OF SINGLE MOTHERS

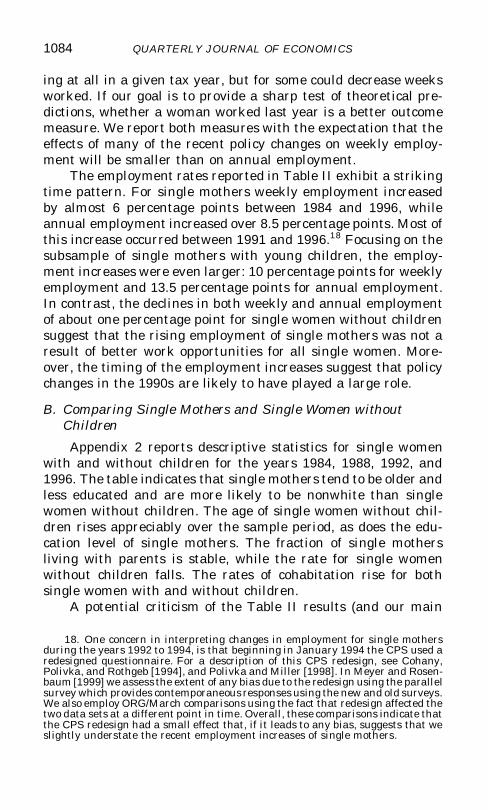

ing at all in a given tax year but for some could decrease weeksworked If our goal is to provide a sharp test of theoretical pre-dictions whether a woman worked last year is a better outcomemeasure We report both measures with the expectation that theeffects of many of the recent policy changes on weekly employ-ment will be smaller than on annual employment

The employment rates reported in Table II exhibit a strikingtime pattern For single mothers weekly employment increasedby almost 6 percentage points between 1984 and 1996 whileannual employment increased over 85 percentage points Most ofthis increase occurred between 1991 and 199618 Focusing on thesubsample of single mothers with young children the employ-ment increases were even larger 10 percentage points for weeklyemployment and 135 percentage points for annual employmentIn contrast the declines in both weekly and annual employmentof about one percentage point for single women without childrensuggest that the rising employment of single mothers was not aresult of better work opportunities for all single women More-over the timing of the employment increases suggest that policychanges in the 1990s are likely to have played a large role

B Comparing Single Mothers and Single Women withoutChildren

Appendix 2 reports descriptive statistics for single womenwith and without children for the years 1984 1988 1992 and1996 The table indicates that single mothers tend to be older andless educated and are more likely to be nonwhite than singlewomen without children The age of single women without chil-dren rises appreciably over the sample period as does the edu-cation level of single mothers The fraction of single mothersliving with parents is stable while the rate for single womenwithout children falls The rates of cohabitation rise for bothsingle women with and without children

A potential criticism of the Table II results (and our main

18 One concern in interpreting changes in employment for single mothersduring the years 1992 to 1994 is that beginning in January 1994 the CPS used aredesigned questionnaire For a description of this CPS redesign see CohanyPolivka and Rothgeb [1994] and Polivka and Miller [1998] In Meyer and Rosen-baum [1999] we assess the extent of any bias due to the redesign using the parallelsurvey which provides contemporaneous responses using the new and old surveysWe also employ ORGMarch comparisons using the fact that redesign affected thetwo data sets at a different point in time Overall these comparisons indicate thatthe CPS redesign had a small effect that if it leads to any bias suggests that weslightly understate the recent employment increases of single mothers

1084 QUARTERLY JOURNAL OF ECONOMICS

regression results below) is that single women without childrenare not a good comparison group for single mothers The means inAppendix 2 suggest the possibility that changes in the character-istics of single mothers versus single women without childrencould explain the two groupsrsquo differing employment rate trendsIn our regression results we condition on observable characteris-tics such as race and education in order to make the two groupsmore comparable It is also interesting to note that single womenwith and without children are quite similar in an importantdimension hourly earnings The mean hourly earnings of womenwith and without children are fairly similar (and they are muchcloser if one controls for education)

Perhaps more importantly one might argue that employ-ment rates are so high for single women without children that itis unreasonable to expect this group to respond to changes ineconomic conditions in the same way that single mothers do Yetemployment rates are not particularly high for low-educated sin-gle women particularly when examining employment last weekOnly 33 percent of high school dropout single mothers workedand 48 percent of high school dropout single women withoutchildren worked last week Nevertheless in our later regressionsderivative estimates for our key policy variables tend to be thelargest and most statistically signicant for high school dropouts

One might also wonder whether the large increases in em-ployment that we nd for single mothers but not for singlewomen without children also occur for other demographicgroups In Meyer and Rosenbaum [2000a] we examine whetherthere are similar employment increases for two other groups withhistorically low employment rates black males 19ndash44 and mar-ried mothers 19ndash44 We nd that the large increases in employ-ment of single mothers over 1984 ndash1996 and particularly since1991ndash1996 are not mirrored by other demographic groups

Another potential criticism of our approach is that usingvariation across women in their marital status number of chil-dren and state of residence implicitly assumes that marriagefertility and migration decisions are exogenous to the policychanges that we examine The evidence on the effects of policychanges on these decisions is mixed making the exogeneity as-sumption more plausible For example in her recent reviewHoynes [1997] concludes ldquoTogether this evidence suggests thatmarriage decisions are not sensitive to nancial incentivesrdquo Shealso argues that ldquoOverall [the effects of welfare on out-of-wedlock

1085THE LABOR SUPPLY OF SINGLE MOTHERS

births] are often insignicant and when they are not they aresmall [pp 129ndash130]rdquo On the other hand another recent reviewMoftt [1997] suggests that the weight of the evidence impliessome effect of welfare benets on marriage and fertility As tolocation Meyer [1999] concludes that there is a signicant butsmall effect of welfare on migration Overall it is likely thatendogenous single motherhood and location exert a small bias onour results

C Accounting for Individual and State Characteristics

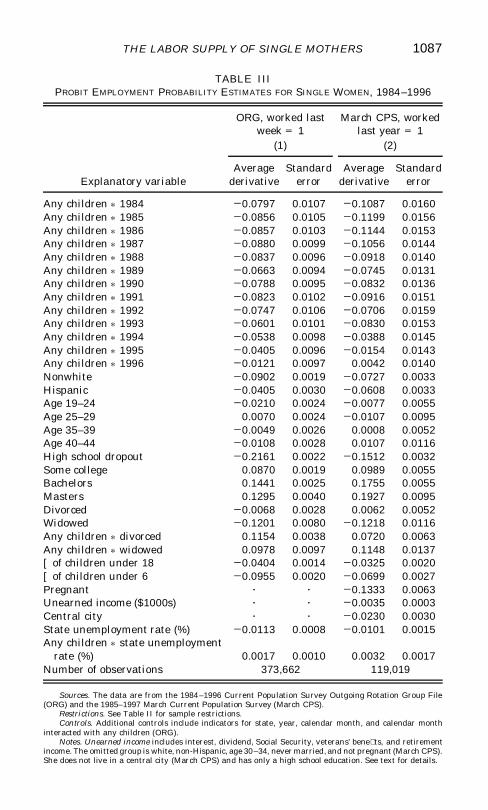

As mentioned above the results in Table II could be partlyexplained by differential changes over time in characteristicssuch as age and education for single women with and withoutchildren Moreover business cycles may differentially affect sin-gle women with and without children thereby leading to employ-ment shifts unrelated to policy changes Consequently Table IIIpresents probit employment estimates for single women control-ling for demographic and business cycle changes We include alarge number of controls for differences between the two groupsand we include the unemployment rate as well as its interactionwith whether or not a woman has children The specication thatwe estimate is

(6) Pr(Eit 5 1) 5 F a Xit 1 b tYEARt

1 g t(YEARt p ANYCHILDRENi)

where Eit equals one if woman i from year t reports positive hoursworked in the reference week for the ORG (or the previous yearfor the March CPS) Xit is a vector that includes demographic andbusiness cycle variables YEARt is an indicator variable for yeart and ANYCHILDRENi equals one for a woman with childrenThe year dummies control for labor market trends in overallfemale employment and the X vector controls for demographicand business cycle effect differences between the groups espe-cially compositional shifts over time Thus differences between g t

coefcients give difference-in-differences estimates controlling forthese other factors These differences can be interpreted as esti-mates of the combined effect of changes in all factors affecting theemployment of single mothers relative to single women withoutchildren

The demographic and business cycle variables accounted forin Table III include controls for state race ethnicity age educa-

1086 QUARTERLY JOURNAL OF ECONOMICS

TABLE IIIPROBIT EMPLOYMENT PROBABILITY ESTIMATES FOR SINGLE WOMEN 1984ndash1996

Explanatory variable

ORG worked lastweek = 1

March CPS workedlast year = 1

(1) (2)

Averagederivative

Standarderror

Averagederivative

Standarderror

Any children p 1984 2 00797 00107 2 01087 00160Any children p 1985 2 00856 00105 2 01199 00156Any children p 1986 2 00857 00103 2 01144 00153Any children p 1987 2 00880 00099 2 01056 00144Any children p 1988 2 00837 00096 2 00918 00140Any children p 1989 2 00663 00094 2 00745 00131Any children p 1990 2 00788 00095 2 00832 00136Any children p 1991 2 00823 00102 2 00916 00151Any children p 1992 2 00747 00106 2 00706 00159Any children p 1993 2 00601 00101 2 00830 00153Any children p 1994 2 00538 00098 2 00388 00145Any children p 1995 2 00405 00096 2 00154 00143Any children p 1996 2 00121 00097 00042 00140Nonwhite 2 00902 00019 2 00727 00033Hispanic 2 00405 00030 2 00608 00033Age 19ndash24 2 00210 00024 2 00077 00055Age 25ndash29 00070 00024 2 00107 00095Age 35ndash39 2 00049 00026 00008 00052Age 40ndash44 2 00108 00028 00107 00116High school dropout 2 02161 00022 2 01512 00032Some college 00870 00019 00989 00055Bachelors 01441 00025 01755 00055Masters 01295 00040 01927 00095Divorced 2 00068 00028 00062 00052Widowed 2 01201 00080 2 01218 00116Any children p divorced 01154 00038 00720 00063Any children p widowed 00978 00097 01148 00137[ of children under 18 2 00404 00014 2 00325 00020[ of children under 6 2 00955 00020 2 00699 00027Pregnant z z 2 01333 00063Unearned income ($1000s) z z 2 00035 00003Central city z z 2 00230 00030State unemployment rate () 2 00113 00008 2 00101 00015Any children p state unemployment

rate () 00017 00010 00032 00017Number of observations 373662 119019

Sources The data are from the 1984ndash1996 Current Population Survey Outgoing Rotation Group File(ORG) and the 1985ndash1997 March Current Population Survey (March CPS)

Restrictions See Table II for sample restrictionsControls Additional controls include indicators for state year calendar month and calendar month

interacted with any children (ORG)Notes Unearned income includes interest dividend Social Security veteransrsquo benets and retirement

income The omitted group is white non-Hispanic age 30ndash34 never married and not pregnant (March CPS)She does not live in a central city (March CPS) and has only a high school education See text for details

1087THE LABOR SUPPLY OF SINGLE MOTHERS

tion marital status marital status interacted with a childrenindicator the number of children under six and eighteen thestate unemployment rate the state unemployment rate inter-acted with a children indicator (for the March CPS only) controlsfor pregnancy central city and unearned income and (for theORG only) controls for month and month interacted with a chil-dren indicator Note that the difference-in-differences calculatedby subtracting one YEAR p ANYCHILDREN coefcient fromanother are hardly affected by including the controls19 For ex-ample between 1984 and 1996 the weekly employment of singlemothers relative to single women without children rises 71 per-centage points without controls and 68 percentage points withcontrols20 For annual employment the difference-in-differencesestimator for 1984 to 1996 suggests an 117 percentage pointincrease in the relative annual employment of single motherswithout controls and an 113 percentage point increase withcontrols Again most of the increase occurs between 1991 and1996 Therefore these difference-in-difference estimates suggesta potential role for policy changes especially since 1991

VI POLICY VARIABLES AND EMPLOYMENT USING OUR SIMPLE

STRUCTURAL MODEL

We now move on to our main approach that uses our simplestructural model to distinguish between the different policies andto provide estimates that have a clearer interpretation Whilesome of the estimates rely on comparisons of single mothers andsingle women with children over time other estimates use avariety of other sources of identifying variation in our key explana-tory variables In some specications the identifying variationcomes from differences in taxes and benets for families of dif-ferent sizes and in different states as well as changes in thesetaxes and benets over time and differences in state living costs

Table IV reports estimates of our structural model of the

19 Due to the difculty in gauging the magnitude of probit coefcient esti-mates instead we report derivatives of the probability of working with respect toeach of the explanatory variables averaged over the single mothers in the sampleThus differences in the average derivatives for the YEAR p ANYCHILDRENvariables give changes over time in the difference in employment between singlewomen with and without children analogous to the changes that can be calculatedfrom Table II

20 The ldquowithout controlsrdquo results come from a weighted probit including onlythe year dummies and YEAR p ANYCHILDREN interactions

1088 QUARTERLY JOURNAL OF ECONOMICS

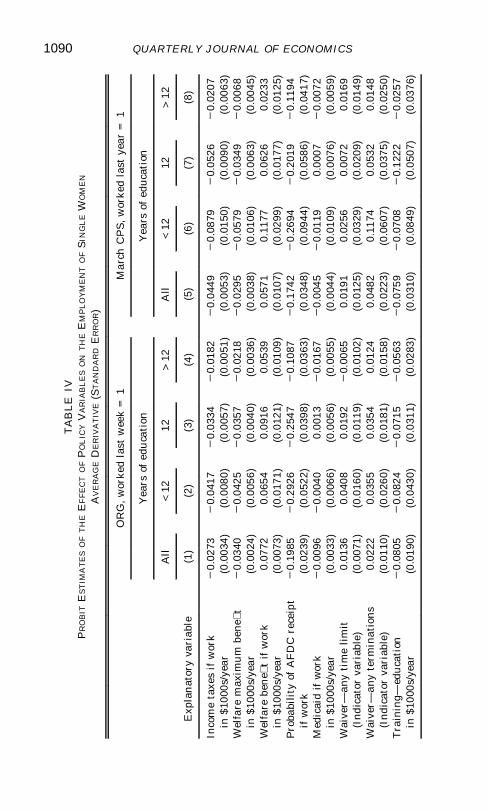

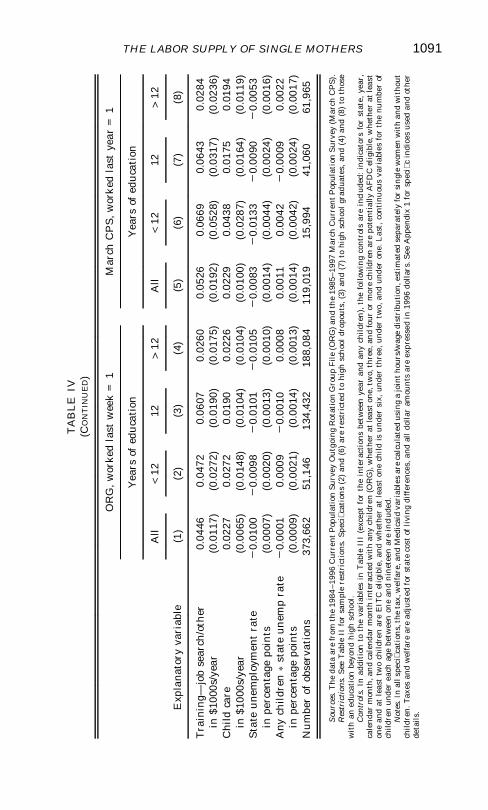

effects of tax and welfare policy on the probability that a womanworks These specications provide estimates of the parametersin expression (5) of Section II and can be used to obtain estimatesof the effects of the different policy changes during the 1984 ndash1996period These specications also provide coefcients that can beused to summarize the effects of a wide range of policies and thatcan be used to simulate other policies In addition to the variablesshown in Table IV each of these probits include the controlvariables reported in Table III (except for the YEAR p ANY-CHILDREN interactions) along with a large number of familycomposition variables listed in the table notes These controlvariables imply that we are not using simple differences acrossfamily types to identify our coefcients We are using changesover time or differences across states in how different families aretreated We focus rst on the full sample specications in columns(1) and (5)

All of the coefcients on the income variables have the signsthat are implied by our simple structural model and are signi-cantly different from zero21 Lower taxes and maximum welfarebenets increase employment while higher welfare benets if awoman works (due to lower implicit taxes on earnings) increaseemployment Rather than restricting the income variables toenter the worknonwork decision as a single expected incomevariable we have allowed the coefcients on the different compo-nents of income to differ It is thus encouraging that the coef-cients on the income tax and welfare variables have roughly thesame magnitude as expected The one exception to this rule isthat the coefcient on Welfare Benets if Work in the weeklyemployment equation is substantially larger than the other in-come coefcients

A Taxes

The Income Taxes if Work coefcient implies that a onethousand dollar reduction in income taxes if a woman worksincreases employment last week by 27 percentage points andincreases employment last year by 45 percentage points Both ofthese effects are strongly signicant These coefcients indicateelasticities of the participation rate with respect to the return to

21 We examined the importance of allowing for correlation among the errorterms at the level of state p year p ANYCHILDREN using STATA These standarderrors are very close to those without this correction for clustering

1089THE LABOR SUPPLY OF SINGLE MOTHERS

TA

BL

EIV

PR

OB

ITE

ST

IMA

TE

SO

FT

HE

EF

FE

CT

OF

PO

LIC

YV

AR

IAB

LE

SO

NT

HE

EM

PL

OY

ME

NT

OF

SIN

GL

EW

OM

EN

AV

ER

AG

ED

ER

IVA

TIV

E(S

TA

ND

AR

DE

RR

OR)

Exp

lan

ator

yva

riab

le

OR

Gw

orke

dla

stw

eek

=1

Mar

chC

PS

wor

ked

last

year

=1

Yea

rsof

edu

cati

onY

ears

ofed

ucat

ion

All

lt12

12gt

12A

lllt

1212

gt12

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Inco

me

taxe

sif

wor

k2

002

732

004

172

003

342

001

822

004

492

008

792

005

262

002

07in

$100

0sy

ear

(00

034)

(00

080)

(00

057)

(00

051)

(00

053)

(00

150)

(00

090)

(00

063)

Wel

fare

max

imu

mbe

net

20

0340

20

0425

20

0357

20

0218

20

0295

20

0579

20

0349

20

0068

in$1

000s

yea

r(0

002

4)(0

005

6)(0

004

0)(0

003

6)(0

003

8)(0

010

6)(0

006

3)(0

004

5)W

elfa

rebe

ne

tif

wor

k0

0772

006

540

0916

005

390

0571

011

770

0626

002

33in

$100

0sy

ear

(00

073)

(00

171)

(00

121)

(00

109)

(00

107)

(00

299)

(00

177)

(00

125)

Pro

babi

lity

ofA

FD

Cre

ceip

t2

019

852

029

262

025

472

010

872

017

422

026

942

020

192

011

94if

wor

k(0

023

9)(0

052

2)(0

039

8)(0

036

3)(0

034

8)(0

094

4)(0

058

6)(0

041

7)M

edic

aid

ifw

ork

20

0096

20

0040

000

132

001

672

000

452

001

190

0007

20

0072

in$1

000s

yea

r(0

003

3)(0

006

6)(0

005

6)(0

005

5)(0

004

4)(0

010

9)(0

007

6)(0

005

9)W

aive

rmdashan

yti

me

lim

it0

0136

004

080

0192

20

0065

001

910

0256

000

720

0169

(Ind

icat

orva

riab

le)

(00

071)

(00

160)

(00

119)

(00

102)

(00

125)

(00

329)

(00

209)

(00

149)

Wai

vermdash

any

term

inat

ions

002

220

0355

003

540

0124

004

820

1174

005

320

0148

(Ind

icat

orva

riab

le)

(00

110)

(00

260)

(00

181)

(00

158)

(00

223)

(00

607)

(00

375)

(00

250)

Tra

inin

gmdashed

uca

tion

20

0805

20

0824

20

0715

20

0563

20

0759

20

0708

20

1222

20

0257

in$1

000s

yea

r(0

019

0)(0

043

0)(0

031

1)(0

028

3)(0

031

0)(0

084

9)(0

050

7)(0

037

6)

1090 QUARTERLY JOURNAL OF ECONOMICS

TA

BL

EIV

(CO

NT

INU

ED

)

Exp

lana

tory

vari

able

OR

Gw

orke

dla

stw

eek

=1

Mar

chC

PS

wor

ked

last

year

=1

Yea

rsof

edu

cati

onY

ears

ofed

uca

tion

All

lt12

12gt

12A

lllt

1212

gt12

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Tra

inin

gmdashjo

bse

arch

oth

er0

0446

004

720

0607

002

600

0526

006

690

0643

002

84in

$100

0sy

ear

(00

117)

(00

272)

(00

190)

(00

175)

(00

192)

(00

528)

(00

317)

(00

236)

Chi

ldca

re0

0227

002

720

0190

002

260

0229

004

380

0175

001

94in

$100

0sy

ear

(00

065)

(00

148)

(00

104)

(00

104)

(00

100)

(00

287)

(00

164)

(00

119)

Sta

teu

nem

ploy

men

tra

te2

001

002

000

982

001

012

001

052

000

832

001

332

000

902

000

53in

perc

enta

gepo

ints

(00

007)

(00

020)

(00

013)

(00

010)

(00

014)

(00

044)

(00

024)

(00

016)

Any

chil

dren

pst

ate

unem

pra

te2

000

010

0009

20

0010

000

080

0011

000

422

000

090

0022

inpe

rcen

tage

poin

ts(0

000

9)(0

002

1)(0

001

4)(0

001

3)(0

001

4)(0

004

2)(0

002

4)(0

001

7)N

um

ber

ofob

serv

atio

ns37

366

251

146

134

432

188

084

119

019

159

9441

060

619

65

Sou

rces

The

data

are

from

the

1984

ndash199

6C

urre

ntP

opul

atio

nSu

rvey

Out

goin

gR

otat

ion

Gro

up

Fil

e(O

RG

)an

dth

e19

85ndash1

997

Mar

chC

urre

ntP

opul

atio

nS

urve

y(M

arch

CP

S)

Res

tric

tion

sS

eeT

able

IIfo

rsa

mpl

ere

stri

ctio

ns

Spec

ica

tion

s(2

)an

d(6

)ar

ere

stri

cted

tohi

ghsc

hoo

ldr

opou

ts(

3)an

d(7

)to

high

sch

ool

grad

uate

san

d(4

)an

d(8

)to

thos

ew

ith

aned

ucat

ion

beyo

nd

hig

hsc

hool

C

ontr

ols

Inad

diti

onto

the

vari

able

sin

Tab

leII

I(e

xcep

tfo

rth

ein

tera

ctio

nsbe

twee

nye

aran

dan

ych

ildr

en)

the

foll

owin

gco

ntro

lsar

ein

clud

ed

indi

cato

rsfo

rst

ate

year

ca

len

dar

mon

tha

nd

cale

ndar

mon

thin

tera

cted

wit

han

ych

ildr

en(O

RG

)w

heth

erat

leas

ton

etw

oth

ree

and

four

orm

ore

child

ren

are

pote

ntia

llyA

FD

Cel

igib

lew

heth

erat

leas

ton

ean

dat

leas

ttw

och

ildr

enar

eE

ITC

elig

ible

and