The Management Accountant · 2012-12-22 · by Dr. K. V. Ramana Murthy & Dr. K. V. Achalapathi 134...

80

PRESIDENT G. N. Venkataraman email : [email protected] VICE PRESIDENT B. M. Sharma email : [email protected] CENTRAL COUNCIL MEMBERS A. N. Raman, A. S. Durga Prasad, Ashwin G. Dalwadi, Balwinder Singh, Chandra Wadhwa, Hari Krishan Goel, Kunal Banerjee, M. Gopalakrishnan, Dr. Sanjiban Bandyopadhyaya, S. R. Bhargave, Somnath Mukherjee, Suresh Chandra Mohanty, V. C. Kothari, GOVERNMENT NOMINEES Jaikant Singh, P. K. Sharma, R. K. Jain, S. C. Vasudeva, T. S. Rangan CHIEF EXECUTIVE OFFICER Sudhir Galande [email protected] Senior Director (Examinations) Chandana Bose [email protected] Senior Director (Administration & Finance) R N Pal [email protected] Director (Technical) J. P. Singh [email protected] Director (Studies) Arnab Chakraborty [email protected] Director (CAT) L. Gurumurthy [email protected] Director (PDD and Training & Placement) J. K. Budhiraja [email protected]. Additional Director (CEP) D. Chandru [email protected] Additional Director (Membership) cum Joint Secretary Kaushik Banerjee [email protected] Additional Director (International Affairs) S. C. Gupta [email protected] EDITOR Sudhir Galande Editorial Office & Headquarters 12, Sudder Street, Kolkata-700 016 Phone : (033) 2252-1031/34/35, Fax : (033) 2252-1602/1492 Website : www.icwai.org Delhi Office ICWAI Bhawan 3, Institutional Area, Lodi Road New Delhi-110003 Phone : (011) 24622156, 24618645, Fax: (011) 24622156, 24631532, 24618645 The Management Accountant « Official Organ of The Institute of Cost and Works Accountants of India established in year 1944 (Founder member of IFAC, SAFA and CAPA) Volume 45 No. 2 February 2010 the management accountant, February, 2010 91 Editorial 93 President’s Communique 94 Cover Features New Pension System - An Effort towards an Inclusive Safety Net for Old Age by Dr. Netra Apte 96 IAS 26, Accounting and Reporting by Retirement Benefit Plans - A Closer Look by K. S. Muthupandian 101 AS(15)-Accounting for Retirement Benefits in the financial statements of employer-Review and comparative study of AS-15 with IAS-19 and FAS-36 (USA) by S. Murugan 106 Life Insurance by A. L. Prasad 114 Accounting Issues Accrual Accounting in Government: An Analytical View by Dr. T. Satyanarayana Chary & K. Vara Prasad 116 Costing Matters Throughput Accounting–A Tool to Manage Inventory During Recession by Atul Shiva & Monica Sethi 123 Recent developments in finance Maintenance Spares Management : Cost Reduction Approach by B. C. Patel 126 Global Financial Crisis, Risk Management & Financial Stability by Dr. A. Srivastava & Sheetal Kumar 139 IDEALS THE INSTITUTE STANDS FOR q to develop the Cost and Manage- ment Accountancy profession q to develop the body of members and properly equip them for functions q to ensure sound professional ethics q to keep abreast of new developments. The views expressed by contributors or reviewers in this Journal do not necessarily reflect the opinion of The Institute of Cost and Works Accountants of India nor can the Institute by any way be held responsible for them. The contents of this journal are the copyright of The Institute of Cost and Works Accountants of India, whose permission is necessary for reproduction in whole or in part. Marketing Matters Avenues and Revenues-A Study on the Pricing Strategies of Telugu TV Channels by Dr. K. V. Ramana Murthy & Dr. K. V. Achalapathi 134 Taxation Updates Latest Arrivals-ACES (Automation of Central Excise & Service Tax) by R. Gopal 163 IFRS 129 51 st National Convention 130 Admission to Membership 146 Announcement 153 Legal Updates 154 Regions & Chapter 164

Transcript of The Management Accountant · 2012-12-22 · by Dr. K. V. Ramana Murthy & Dr. K. V. Achalapathi 134...

PRESIDENTG. N. Venkataraman

email : [email protected] PRESIDENT

B. M. Sharmaemail : [email protected] COUNCIL MEMBERS

A. N. Raman, A. S. Durga Prasad,Ashwin G. Dalwadi, Balwinder Singh,Chandra Wadhwa, Hari Krishan Goel,Kunal Banerjee, M. Gopalakrishnan,

Dr. Sanjiban Bandyopadhyaya,S. R. Bhargave, Somnath Mukherjee,

Suresh Chandra Mohanty, V. C. Kothari,GOVERNMENT NOMINEES

Jaikant Singh, P. K. Sharma, R. K. Jain,S. C. Vasudeva, T. S. Rangan

CHIEF EXECUTIVE OFFICERSudhir [email protected]

Senior Director (Examinations)Chandana Bose

[email protected] Director

(Administration & Finance)R N Pal

[email protected] (Technical)

J. P. [email protected]

Director (Studies)Arnab Chakraborty

[email protected] (CAT)L. Gurumurthy

[email protected] (PDD and Training & Placement)

J. K. [email protected].

Additional Director (CEP)D. Chandru

[email protected] Director (Membership) cum

Joint SecretaryKaushik Banerjee

[email protected] Director (International Affairs)

S. C. [email protected]

EDITORSudhir Galande

Editorial Office & Headquarters12, Sudder Street, Kolkata-700 016Phone : (033) 2252-1031/34/35,

Fax : (033) 2252-1602/1492Website : www.icwai.org

Delhi OfficeICWAI Bhawan

3, Institutional Area, Lodi RoadNew Delhi-110003

Phone : (011) 24622156, 24618645,Fax: (011) 24622156, 24631532, 24618645

TheManagementAccountan t

« Official Organ of The Institute of Cost and Works Accountants of India

established in year 1944 (Founder member of IFAC, SAFA and CAPA)

Volume 45 No. 2 February 2010

the management accountant, February, 2010 91

Editorial 93

President’s Communique 94

Cover Features

New Pension System - An Efforttowards an Inclusive Safety Net forOld Age

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by Dr. Netra Apte 96

IAS 26, Accounting and Reporting byRetirement Benefit Plans - A CloserLook

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by K. S. Muthupandian 101

AS(15)-Accounting for RetirementBenefits in the financial statements ofemployer-Review and comparativestudy of AS-15 with IAS-19 andFAS-36 (USA)

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by S. Murugan 106

Life Insuranceby A. L. Prasad 114

Accounting Issues

Accrual Accounting in Government:An Analytical View

by Dr. T. Satyanarayana Chary &K. Vara Prasad 116

Costing MattersThroughput Accounting–A Tool toManage Inventory During Recessionby Atul Shiva & Monica Sethi123

Recent developments in financeMaintenance Spares Management :Cost Reduction Approach

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by B. C. Patel 126

Global Financial Crisis, RiskManagement & Financial Stabilityby Dr. A. Srivastava &Sheetal Kumar 139

IDEALSTHE INSTITUTE STANDS FOR

q to develop the Cost and Manage-ment Accountancy profession q todevelop the body of members andproperly equip them for functionsq to ensure sound professionalethics q to keep abreast of newdevelopments.

The views expressed bycontributors or reviewers in thisJournal do not necessarily reflect theopinion of The Institute of Costand Works Accountants of India nor can the Institute by any way beheld responsible for them. Thecontents of this journal are thecopyright of The Institute of Costand Works Accountants of India,whose permission is necessary forreproduction in whole or in part.

Marketing MattersAvenues and Revenues-A Study on thePricing Strategies of Telugu TVChannelsby Dr. K. V. Ramana Murthy &Dr. K. V. Achalapathi 134

Taxation UpdatesLatest Arrivals-ACES (Automation ofCentral Excise & Service Tax)by R. Gopal 163

IFRS 129

51st National Convention 130

Admission to Membership 146

Announcement 153

Legal Updates 154

Regions & Chapter 164

The Management AccountantTechnical Data

Periodicity MonthlyLanguage English

Overall size - 26.5 cm. x 19.5 cm.Printed Area - 24 cm. x 17 cm.

Screens - up to 130

Subscription

Rs. 300/- (Inland) p.a.Single Copy : Rs. 30/-

Overseas

US $ 150 for AirmailUS $ 100 for Surface Mail

Concessional Subscription Rates for RegisteredStudents & Grad CWAs of the Institute

Rs. 150/- p.a.Single Copy : Rs. 15/- (for ICWAI

Students & Grad CWAs)

Subscription rate and price ofThe Management Accountant

(Student Edition)Annual Subscription rate : Rs. 50Price of Single copy : Rs. 5

Revised Rates for AdvertisementThe Management Accountant

Rs. (US $)Back Cover (colour only) 50,000 2,500

Inside Cover (colour only) 35,000 2,000

Ordy. Full page (B/W only) 20,000 1,500

Ordy. Half page (B/W only) 12,000 1,250

Ordy. Qrtr. page (B/W only) 7,500 750

Revised Rates for AdvertisementStudent Edition

Full Page Rs. 12,000

Back Page Rs. 10,000

(Always Half Page only)

Inside Half Page Rs. 7,500

Inside Quarter Page Rs. 5,000

The Institute reserves the right to refuse anymatter of advertisement detrimental to theinterest of the Institute. The decision of theEditor in this regard will be final.

92 the management accountant, February, 2010

MISSION STMISSION STMISSION STMISSION STMISSION ST AAAAATEMENTTEMENTTEMENTTEMENTTEMENT

�ICWAI Professionals would ethically driveenterprises globally by creating value to stakeholdersin the socio-economic context through competenciesdrawn from the integration of strategy, managementand accounting.�

VISION STVISION STVISION STVISION STVISION ST AAAAATEMENTTEMENTTEMENTTEMENTTEMENT

�ICWAI would be the preferred source of resourcesand professionals for the financial leadership ofenterprises globally.�

DISCLAIMER

The views expressed by the authors are personaland do not necessarily represent the views andshould not be attributed to ICWAI.

NOTIFICA TION

Ref. No. DS-3/1/1/10 January 12, 2010

Finance (No.2) Act 2009, involving Assessment Year2010-2011 will be applicable for the subjects BusinessTaxation (Intermediate) and Strategic Tax Management(Final) under Syllabus 2002 for the purpose of June 2010term of Examination.

Arnab ChakrabortyDirector-Studies

NOTIFICA TION

Ref. No. DS-3/2/1/10 January 12, 2010

Finance (No.2) Act 2009, involving Assessment Year2010-2011 will be applicable for the subjects Applied DirectTaxation (Intermediate), Applied Indirect Taxation(Intermediate) and Indirect & Direct-Tax Management (Final)for the purpose of June 2010 term of Examination underRevised Syllabus 2008.

Arnab ChakrabortyDirector-Studies

Editorial

the management accountant, February, 2010 93

"Old age is the most unexpected of all things thathappen to man."--Leon Trotsky

An age bomb is ticking in India with the current elderlypopulation of nearly 75 million expected to increaseto 160 million by 2020. Around one-eight of the world'selderly population lives in India. Caring for the agedis part of our social tradition and ethos with explicitrecognition of Vanaprastha or 'retirement stage' andaction taken by family and community to facilitatethe same. Unfortunately, in India, Old Age seems tobe most unanticipated and consequently groundworkfor it is quite inadequate. With globalization andmigration, the joint family system is on the decline (atleast in urban areas) and to that extent the challengeof caring for the aged has become greater for societyand the government. The traditional and informalmethods of old age income security are not able tocope with the trends of increased life span andenhanced medical expenses during old age.

Pension savings are the primary source of securityfor retirement. Pensions are expected to achieve thegoals of minimizing poverty in old age; smootheninginter temporal life consumption, which fluctuatessignificantly and ensuring that retirees do not outlivetheir pension benefits. This has been achieved indifferent countries and different sectors by followingspecific retirement benefit schemes like pay-as-yougo, which are Defined Benefit plans and publiclyfunded. However there is an increase in the greyingpopulation on account of increased life expectancydue to advances in medicine, decline in populationgrowth and improved lifestyle requirements at old age.All these factors are putting pressure on the socialsecurity system and also impacting the corporate'sbalance sheets due to greater pension outlays. In sucha scenario, corporates would like to move away fromDefined Benefit to Defined Contribution schemes butare being met with substantial opposition fromemployees due to fall in the benefits.

India has to grapple with an additional problem oflarger coverage of the population under the social

security net especially the unorganized sector (AnOASIS report estimates that nearly 90% of theworkforce is not covered by any of the mandatoryschemes and they depend on other financial savings,investment in gold or on family support) and the abilityof the state to sustain its current schemes forgovernment employees, owing to the fact that pensionpayments constitute a major share of the government'sexpenditure and thus any increase in pension paymentwill add to the already woeful fiscal deficit of thecountry.

The existing schemes like Provident Fund schemesare characterized by under performance and areviewed more as modes of tax evasion by the salariedincome earners rather than as a fund that would coverexpenditure during the lifetime after retirement.Investment restrictions owing to archaic regulations;under developed annuity markets, which result inlimited returns and inadequate development of theinsurance sector that has a symbiotic relationship withthe pensions sector, have hindered pension reformsin our country. Apart from addressing the commercialand economic considerations of pensions; reducingthe wide chasm between the pension benefits of thepublic and private sectors and linking health care issuewith retirement benefits are also required to take careof the social aspect of pensions.

The Old Age Social and Income Security (OASIS)report has led to the formulation of the New PensionScheme (NPS) in India from 2009. The NPS is afirst of its kind social security scheme and is proposedto remove the many ills that plague the current pensionsector in India.

In the current issue we focus on the salient featuresof the NPS and examine the accounting standardsrelating to retirement plans. Cost AccountingStandard- 7 on Employee Cost released by ICWAIalso considers the aspect of retirement plans. Asadvisors/ consultants, Cost & ManagementAccountants have an important role in recommendingthe most suitable and cost effective pension plans fortheir clients.

Pension Ponderables

94 the management accountant, February, 2010

lPresident�s Communique l

Dear Professional Friends,

SEASON'S GREETINGS TO ALL OF YOU.

I am happy to note that the year 2010 has been a good start for ICWAI with thefollowing events:-

ICWAI elected to Vice Presidentship of South Asian Federation of Accountants (SAFA):

After 14 years, our Institute has got the turn of occupying the Vice Presidentship ofSAFA and this has happened on 23rd January 2010 when SAFA Assembly electedICWAI Council Member, Shri A.N. Raman as its Vice President for the year 2010 withan overwhelming unanimous support. While sharing this glad news, I have to informthat many of our members are not thinking about the contribution by our Institutethrough this body and hence I am specifically requesting all the members to understandthe functioning of SAFA, Confederation of Pacific and Asian Accountants (CAPA)and International Federation of Accountants. These are the bodies, which are monitoring the good Cost andManagement Accountant Practice at SAARC Regional level, at the Asia Pacific level and at the world level. Ifour good Cost and Management Accountant practices are shared with these bodies, which we are doing, itcould bring ICWAI to high reckoning. This enables ICWAI to earn a place to have a say in all the matters ofSAFA, including Cost and Management Accountancy.

I congratulate Shri A.N. Raman on my behalf and on behalf of the ICWAI Council and other ProfessionalMembers of ICWAI for having occupied the seat, and wish him the best tenure of 2010 as Vice President ofSAFA. Several opportunities are getting opened to the Cost and Management Accountants and we are takingthe lead to spread these first to the SAARC regional body and then to the other higher levels. I am sure the newVice President of SAFA will be able to achieve the above professional aspirations and bring laurels to ourprofession and the Institute. The job will continue further till 2011 when ICWAI occupies the seat of Presidentship of SAFA in the beginning of year 2011 when we can continue the 2010 achievements and contributefurther in the coming years.

Shri Komal Chitrakar of Nepal elected as President of SAFA for the year 2010:On behalf of ICWAI, I congratulate Shri Komal Chitrakar for taking over the Presidentship of SAFA for theyear 2010.

Emerging Professional Matters:I am getting several suggestions and advices relating to many professional matters which are in the pipe line likeCompany Law Bill 2009, Introduction of GST, Direct Tax Code, Adoption of International Financial ReportingStandards (IFRS), the name change and Expert Group recommendations to MCA, etc. Since these matters arein several stages of follow-up, I can only assure the members that all the suggestions given by our friends arebeing taken care of and we are continuously monitoring and following up on all these matters to get our duerecognition and we are hopeful of the same.

Co-ordination Committee meeting with the Institute of Chartered Accountants of India:I am glad to inform you that a Co-ordination Committee meeting was held recently with the Institute ofChartered Accountants of India (ICAI) and the dialogue has started with the understanding of points on bothsides wherever we can work together to arrive at a consensus for giving relief to some of the problems arisingfor students and members of both the Institutes. I am sure in the coming months, when we come out withcertain recommendations, the students and members should be very happy and this dialogue will continuefurther also.

Visits to the Regions and Chapters during December 2009 and January 2010:It was a record admission to ICWA Courses in the current batch at SIRC, Chennai. Over 1,000 students hadassembled for the inaugural function along with their parents. The Principal Secretary of Tamil Nadu Governmentinaugurated the classes. Other Office-bearers who spoke on the occasion, highlighted the importance of

the management accountant, February, 2010 95

education in Cost and Management Accountancy. The students and parents were happy to react to the suggestionsgive by the Chief Guest and other people and were happy about the scope for Cost and Management Accountants,which the Institute is working for. Some faculties also gave advice to the students and suggestions to theparents to see that students who take the initial registration for ICWAI Course should have a zeal to completethe Final examination for which all infrastructure are provided by the Regional Council and the Institute.

I was also happy to share some details with the officials on clarifications asked by Media. A good coveragecame from Chennai Media.

The Nagpur Chapter of Cost Accountants had arranged a very educative seminar on GST and Indirect Taxesbringing the knowledgeable Resource Persons including top officials from Central Excise and Customs. Thevalue addition of the seminar is that members were suggesting for conduct of number of such seminars andwork-shops on the above topics so that our students and members will be able to take the lead in the mattersof Service Tax, Excise Duty, Customs Duty, VAT and future GST with the Corporate world.

I was happy to attend along with few Central Council colleagues, a function of Surat Chapter of CostAccountants. An excellent programme of recognizing the top achievers in the Institute examination was heldand this will go a long way in propagating the quality additions to our studentship registration as well asenhancing the quality and quantity of members. Chairman-WIRC was present along with WIRC Councilcolleagues.

The Surat Chapter of Cost Accountants also arranged an "Investor Awareness Programme" with the participationof Resource Persons from the respective fields like Stock-Brokers, Mutual Fund Executives, Investors, Banksand Insurance Companies. Members are aware that the Investor Awareness Programme conducted by ICWAIin co-ordination with MCA is attracting good number of participants and we are confident of achieving thedesired goal of MCA in corporatising India, particularly in formation of LLPs, etc., which the Government iskeen to encourage. ICWAI will be conducting this programme for another one year in various cities in thecountry and I once again appeal to all the Chapters and the four Regional Councils to make this InvestorAwareness Programme a big success and this will add visibility of ICWAI which is necessary for our futuregrowth.

The Noida Chapter of Cost Accountants organized a Members' Meet and the inauguration of first Oral CoachingBatch for ICWAI Courses to cater to the needs of students around Noida and particularly the interior parts ofU.P. I have taken the opportunity to advise all members and students that we should propagate the CAT courseto the nook and corner of India and to reach this to village level 10+2 students so that they can be brought intothe mainstream for achieving inclusive growth. It is our desire that all of us should take steps whatever isnecessary in propagating the admission of rural students for this course. The Institute has assured all thefacilities to all the colleges wherever they start this course and see to it that ICWAI will be a partner of theGovernment in its revolution of achieving inclusive growth.

It is my appeal from now onwards till 31st March 2010 to all our members to bring more and more non-members who have passed ICWAI examination into our fold by applying for our Membership. I am happy toinform that for the last six months, addition to our Associates and Fellowships is on the increase. However, wehave to achieve quite a lot if we have to be regarded as a sizeable number to work and contribute in propagatingthe Cost and Management Accountancy to the whole of India, if not to the world community.

With regards,

Yours sincerely

(GN Venkataraman)PresidentDate : 1st February, 2010

lPresident�s Communique l

96 the management accountant, February, 2010

New Pension System -An Effort towards anInclusive Safety Net forOld AgeDr. Netra Apte*

B.Com, AICWAI, MMS, Ph.D

H uman race is blessed withintelligence. The variousscientific and medical

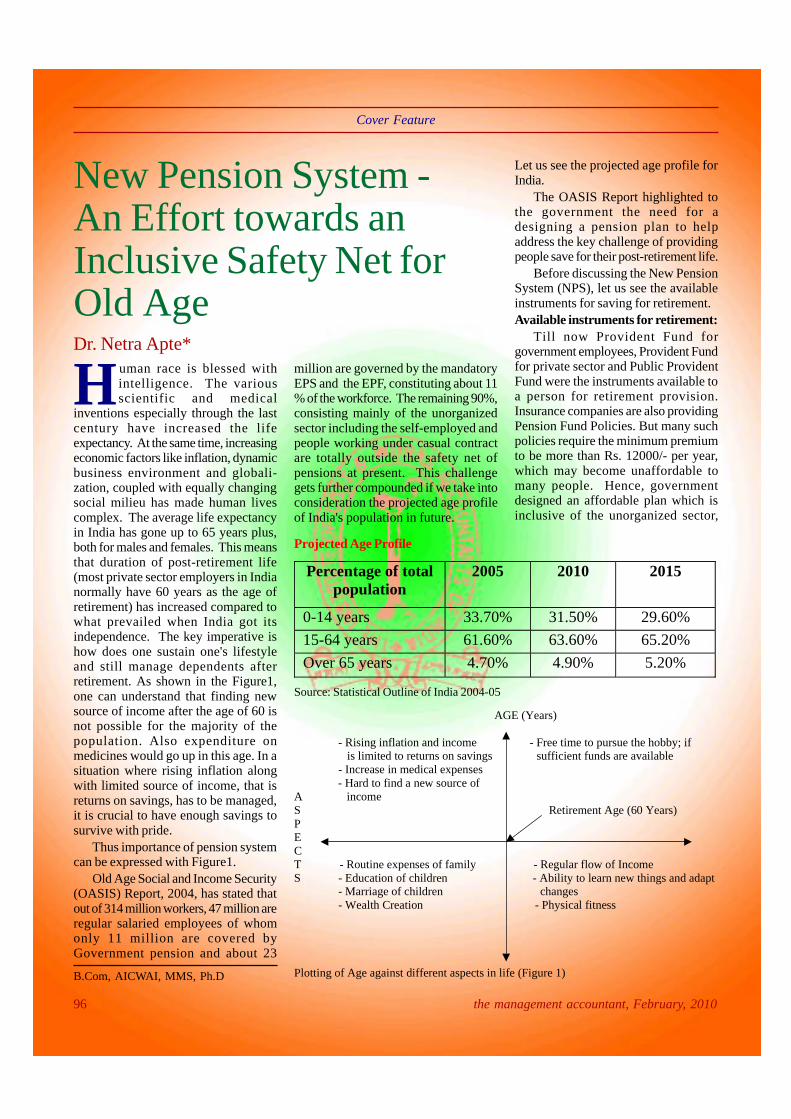

inventions especially through the lastcentury have increased the lifeexpectancy. At the same time, increasingeconomic factors like inflation, dynamicbusiness environment and globali-zation, coupled with equally changingsocial milieu has made human livescomplex. The average life expectancyin India has gone up to 65 years plus,both for males and females. This meansthat duration of post-retirement life(most private sector employers in Indianormally have 60 years as the age ofretirement) has increased compared towhat prevailed when India got itsindependence. The key imperative ishow does one sustain one's lifestyleand still manage dependents afterretirement. As shown in the Figure1,one can understand that finding newsource of income after the age of 60 isnot possible for the majority of thepopulation. Also expenditure onmedicines would go up in this age. In asituation where rising inflation alongwith limited source of income, that isreturns on savings, has to be managed,it is crucial to have enough savings tosurvive with pride.

Thus importance of pension systemcan be expressed with Figure1.

Old Age Social and Income Security(OASIS) Report, 2004, has stated thatout of 314 million workers, 47 million areregular salaried employees of whomonly 11 million are covered byGovernment pension and about 23

million are governed by the mandatoryEPS and the EPF, constituting about 11% of the workforce. The remaining 90%,consisting mainly of the unorganizedsector including the self-employed andpeople working under casual contractare totally outside the safety net ofpensions at present. This challengegets further compounded if we take intoconsideration the projected age profileof India's population in future.

Percentage of total population

2005 2010 2015

0-14 years 33.70% 31.50% 29.60%

15-64 years 61.60% 63.60% 65.20%

Over 65 years 4.70% 4.90% 5.20%

Projected Age Profile

Source: Statistical Outline of India 2004-05

AGE (Years)

- Rising inflation and income - Free time to pursue the hobby; if is limited to returns on savings sufficient funds are available - Increase in medical expenses - Hard to find a new source of A income S Retirement Age (60 Years) P E C T - Routine expenses of family - Regular flow of Income S - Education of children - Ability to learn new things and adapt - Marriage of children changes - Wealth Creation - Physical fitness

Plotting of Age against different aspects in life (Figure 1)

Let us see the projected age profile forIndia.

The OASIS Report highlighted tothe government the need for adesigning a pension plan to helpaddress the key challenge of providingpeople save for their post-retirement life.

Before discussing the New PensionSystem (NPS), let us see the availableinstruments for saving for retirement.Available instruments for retirement:

Till now Provident Fund forgovernment employees, Provident Fundfor private sector and Public ProvidentFund were the instruments available toa person for retirement provision.Insurance companies are also providingPension Fund Policies. But many suchpolicies require the minimum premiumto be more than Rs. 12000/- per year,which may become unaffordable tomany people. Hence, governmentdesigned an affordable plan which isinclusive of the unorganized sector,

Cover Feature

the management accountant, February, 2010 97

agricultural workers and large sectionof people, the New Pension System(NPS). With changes in socio-economicenvironment, the government has alsocarried out a major change beforeintroducing NPS. That is, from earlierschemes which offered "Defined Benefit(DB)", now it has been shifted to"Defined Contribution (DC)".Provident Fund for governmentemployees, for private sector and PublicProvident Fund, all are defined benefitscheme. That means, benefit to bereceived by the person is assured.

1All over the world there has been atendency to switch over from DB to DCsystem. It has certain key reasons. Theforces of globalization have causedchanges in job frequently; peoplemoving from one organization toanother, from one country to another,making it almost impossible to run a DBsystem. Other reason includes theweakening of trade unions across theglobe and the decreasing rate of interestwhich has led to employers finding itincreasingly difficult to sustain thefunding required to build up thebenefits on the DB system. Sinceenvironment now has become toodynamic to afford defined benefitsystem, the concept of definedcontribution has evolved. Under thissystem, returns are market driven. Theyare not fixed or assured. A person whowishes to make a provision for the oldage can contribute as per his or her wishand ability. Hence, Pension FundRegulatory and Development Authority(PFRDA) has been established by theGovernment of India, Ministry ofFinance to promote old age security.NPS is now available to all citizens ofIndia with effect from May 1, 2009 otherthan government employees alreadycovered under NPS.2Under NPS, two types of accounts willbe available to the account holder:1. Tier I account: Account holder can

contribute the savings for retirementinto this non- withdrawableaccount.

2. Tier II Account: This is a voluntarysavings facility. An account holderwill be free to withdraw the savingsas per his or her wish.

1R. Vaidyanathan, Pension Business InIndia, IIMB Management Review,September 20042New Pension System , Offer Document

But, at present only Tier I accountsystem is available. Tier II system willstart as per PFRDA's decision andsubsequent notification.

Let us see the procedure for openingthis account and various aspects ofworking of NPS.Who can join?

A citizen of India, whether residentor non resident, subject to the followingconditions:1. Person should be between 18 -55

years of age as on the date of thesubmission of the application form.

2. Person should comply with KnowYour Customer (KYC) norms.

Who cannot join?1. Undischarged insolvent2. Individuals of unsound mind3. Pre - existing account holders underNPS.How to enroll in NPS?

To enroll in the NPS, person needsto submit the registration form to thepoint of presence service provider (POP-SP) of his or her choice. There arecurrently 22 POP - SP'S. ICICI Bank Ltd,LIC of India, State Bank of India are fewof them.

After the account is opened, CentralRecord Keeping Agency (CRA), shallmail a welcome kit to the account holdercontaining the subscriber's uniquePermanent Retirement Account NumberCard. This account number will be theprimary means of identifying andoperating the account.

Fund Managers: The subscriber ofNPS need to choose a pension fundfrom the following list:1. ICICI Prudential Pension Funds

Management Company Ltd.2. IDFC Pension Funds Management

Company Ltd.3. Kotak Mahindra Pension Fund Ltd.4. Reliance Capital Pension Fund Ltd.5. SBI Pension Funds Private Ltd.6. UTI Retirement solutions Ltd.How much does the subscriber needsto contribute?Minimum contribution per year -Rs. 6,000/-Minimum amount per contribution -

Rs. 500 (12 installments minimum perannum)Minimum number of contributions - 4per yearWhat are the benefits of joining theNPS?l It is voluntary.l It is simple.l It is flexible: One can choose his/

her own investment option andpension fund and see money grow.

l It is portable: One can operate youraccount from anywhere in thecountry, even if one changes thejob, city or pension funds manager.

l It is regulated: NPS is regulated byPFRDA, with transparent invest-ment norms and regular monitoringand performance review of fundmanagers by NPS Trust.

What investment choices thesubscribers have?

The NPS offers you two approachesto invest your money:l Active choice: Individual fundsl Auto choice: Lifecycle fundActive choice: Individual funds

The account holder has choice toactively decide as to how your NPSpension wealth is to be invested in thefollowing three options.Asset class E:Investments in predominantly equitymarket instruments.

The investment in this class of assetwould be a subject to a cap of 50 %, asit bears high risk.Asset class C:Investments in fixed income instrumentsother than Government Securities.Asset class G :Investments in Government securities.Auto choice - Lifecycle Fund

Those account holders who cannotdecide the allocation of funds in theabove mentioned three classes, theycan go for this option. Here, the fractionof funds invested across the three

Cover Feature

98 the management accountant, February, 2010

assets classes will be determined by apredefined portfolio, which is decidedon the basis of the age of the accountholder.It is important to note that neither theActive choice nor the Auto choiceprovide assured returns.When can a subscriber withdraw theamount?Tax Benefits

Tax benefits would be applicable asper the Income Tax Act, 1961 asamended from time to time.Charges:Contributors have to pay two types ofcharges.Fixed charges1. Rs. 50 /- (One time charge for issuing

permanent retirement accountnumber)

2. Rs.40 (initial subscriber registrationand Rs. 20 for any subsequenttransactions)

3. Rs.350/- (Annual maintenancecharge)

4. Rs. 10/- for every transaction fromfund value.

Variable charges1. 0.0075 - 0.05 % of fund value per

annum as custodian charge.2. 0.0009% of the fund value per

annum as investment managementfees.

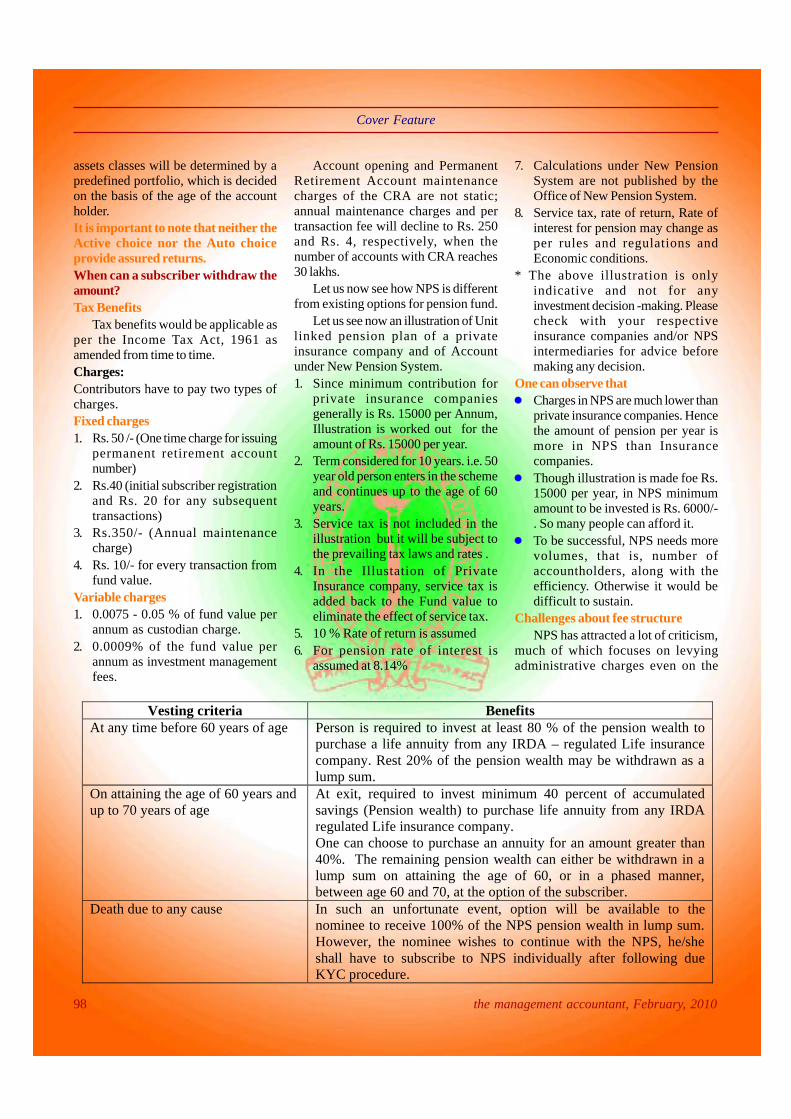

Vesting criteria Benefits At any time before 60 years of age

Person is required to invest at least 80 % of the pension wealth to purchase a life annuity from any IRDA – regulated Life insurance company. Rest 20% of the pension wealth may be withdrawn as a lump sum.

On attaining the age of 60 years and up to 70 years of age

At exit, required to invest minimum 40 percent of accumulated savings (Pension wealth) to purchase life annuity from any IRDA regulated Life insurance company. One can choose to purchase an annuity for an amount greater than 40%. The remaining pension wealth can either be withdrawn in a lump sum on attaining the age of 60, or in a phased manner, between age 60 and 70, at the option of the subscriber.

Death due to any cause In such an unfortunate event, option will be available to the nominee to receive 100% of the NPS pension wealth in lump sum. However, the nominee wishes to continue with the NPS, he/she shall have to subscribe to NPS individually after following due KYC procedure.

Account opening and PermanentRetirement Account maintenancecharges of the CRA are not static;annual maintenance charges and pertransaction fee will decline to Rs. 250and Rs. 4, respectively, when thenumber of accounts with CRA reaches30 lakhs.

Let us now see how NPS is differentfrom existing options for pension fund.

Let us see now an illustration of Unitlinked pension plan of a privateinsurance company and of Accountunder New Pension System.1. Since minimum contribution for

private insurance companiesgenerally is Rs. 15000 per Annum,Illustration is worked out for theamount of Rs. 15000 per year.

2. Term considered for 10 years. i.e. 50year old person enters in the schemeand continues up to the age of 60years.

3. Service tax is not included in theillustration but it will be subject tothe prevailing tax laws and rates .

4. In the Illustation of PrivateInsurance company, service tax isadded back to the Fund value toeliminate the effect of service tax.

5. 10 % Rate of return is assumed6. For pension rate of interest is

assumed at 8.14%

7. Calculations under New PensionSystem are not published by theOffice of New Pension System.

8. Service tax, rate of return, Rate ofinterest for pension may change asper rules and regulations andEconomic conditions.

* The above illustration is onlyindicative and not for anyinvestment decision -making. Pleasecheck with your respectiveinsurance companies and/or NPSintermediaries for advice beforemaking any decision.

One can observe thatl Charges in NPS are much lower than

private insurance companies. Hencethe amount of pension per year ismore in NPS than Insurancecompanies.

l Though illustration is made foe Rs.15000 per year, in NPS minimumamount to be invested is Rs. 6000/-. So many people can afford it.

l To be successful, NPS needs morevolumes, that is, number ofaccountholders, along with theefficiency. Otherwise it would bedifficult to sustain.

Challenges about fee structureNPS has attracted a lot of criticism,

much of which focuses on levyingadministrative charges even on the

Cover Feature

the management accountant, February, 2010 99

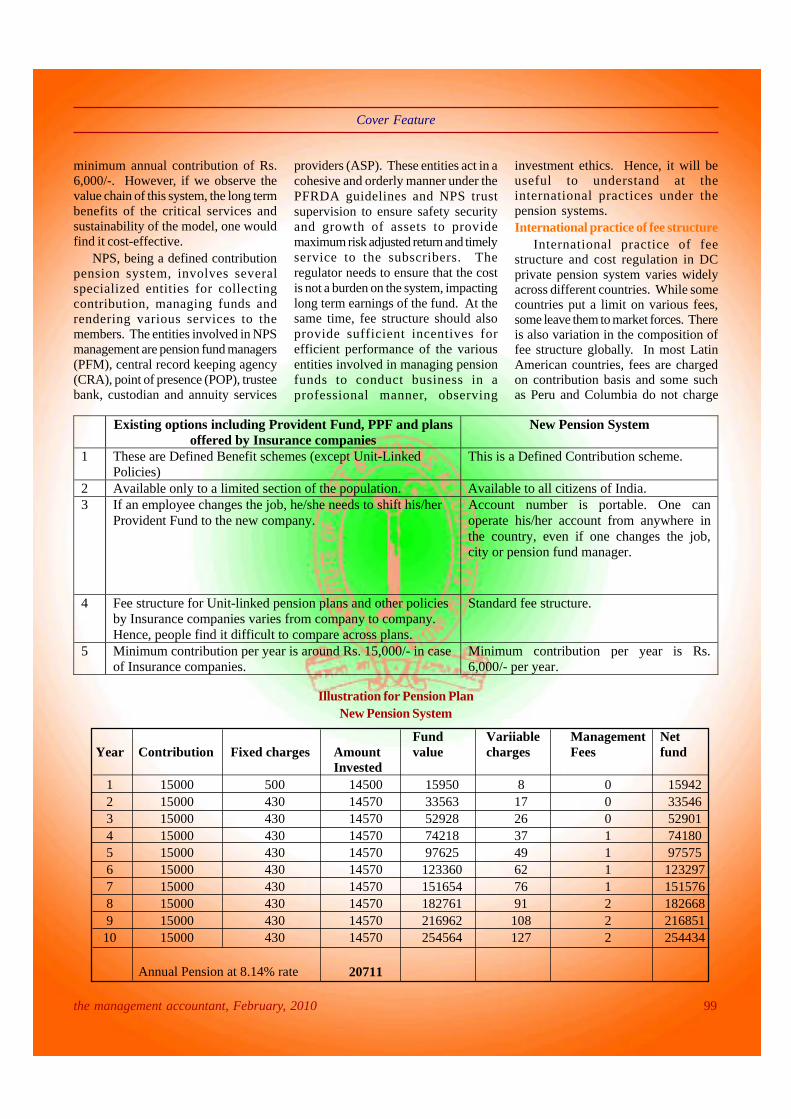

Existing options including Provident Fund, PPF and plans offered by Insurance companies

New Pension System

1 These are Defined Benefit schemes (except Unit-Linked Policies)

This is a Defined Contribution scheme.

2 Available only to a limited section of the population. Available to all citizens of India. 3 If an employee changes the job, he/she needs to shift his/her

Provident Fund to the new company. Account number is portable. One can operate his/her account from anywhere in the country, even if one changes the job, city or pension fund manager.

4 Fee structure for Unit-linked pension plans and other policies by Insurance companies varies from company to company. Hence, people find it difficult to compare across plans.

Standard fee structure.

5 Minimum contribution per year is around Rs. 15,000/- in case of Insurance companies.

Minimum contribution per year is Rs. 6,000/- per year.

minimum annual contribution of Rs.6,000/-. However, if we observe thevalue chain of this system, the long termbenefits of the critical services andsustainability of the model, one wouldfind it cost-effective.

NPS, being a defined contributionpension system, involves severalspecialized entities for collectingcontribution, managing funds andrendering various services to themembers. The entities involved in NPSmanagement are pension fund managers(PFM), central record keeping agency(CRA), point of presence (POP), trusteebank, custodian and annuity services

Illustration for Pension PlanNew Pension System

Year Contribution Fixed charges Amount Fund value

Variiable charges

Management Fees

Net fund

Invested 1 15000 500 14500 15950 8 0 15942 2 15000 430 14570 33563 17 0 33546 3 15000 430 14570 52928 26 0 52901 4 15000 430 14570 74218 37 1 74180 5 15000 430 14570 97625 49 1 97575 6 15000 430 14570 123360 62 1 123297 7 15000 430 14570 151654 76 1 151576 8 15000 430 14570 182761 91 2 182668 9 15000 430 14570 216962 108 2 216851 10 15000 430 14570 254564 127 2 254434

Annual Pension at 8.14% rate 20711

providers (ASP). These entities act in acohesive and orderly manner under thePFRDA guidelines and NPS trustsupervision to ensure safety securityand growth of assets to providemaximum risk adjusted return and timelyservice to the subscribers. Theregulator needs to ensure that the costis not a burden on the system, impactinglong term earnings of the fund. At thesame time, fee structure should alsoprovide sufficient incentives forefficient performance of the variousentities involved in managing pensionfunds to conduct business in aprofessional manner, observing

investment ethics. Hence, it will beuseful to understand at theinternational practices under thepension systems.International practice of fee structure

International practice of feestructure and cost regulation in DCprivate pension system varies widelyacross different countries. While somecountries put a limit on various fees,some leave them to market forces. Thereis also variation in the composition offee structure globally. In most LatinAmerican countries, fees are chargedon contribution basis and some suchas Peru and Columbia do not charge

Cover Feature

100 the management accountant, February, 2010

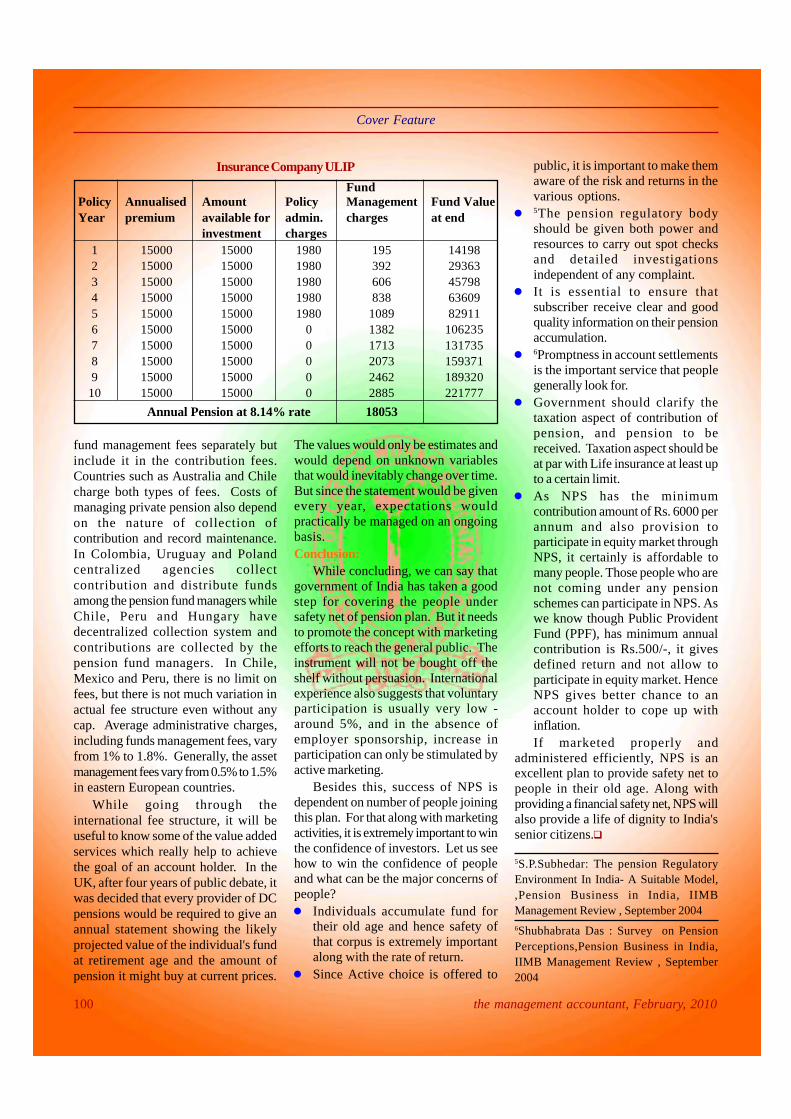

Insurance Company ULIP

Policy Annualised Amount Policy Fund Management Fund Value

Year premium available for admin. charges at end investment charges

1 15000 15000 1980 195 14198 2 15000 15000 1980 392 29363 3 15000 15000 1980 606 45798 4 15000 15000 1980 838 63609 5 15000 15000 1980 1089 82911 6 15000 15000 0 1382 106235 7 15000 15000 0 1713 131735 8 15000 15000 0 2073 159371 9 15000 15000 0 2462 189320 10 15000 15000 0 2885 221777

Annual Pension at 8.14% rate 18053

fund management fees separately butinclude it in the contribution fees.Countries such as Australia and Chilecharge both types of fees. Costs ofmanaging private pension also dependon the nature of collection ofcontribution and record maintenance.In Colombia, Uruguay and Polandcentralized agencies collectcontribution and distribute fundsamong the pension fund managers whileChile, Peru and Hungary havedecentralized collection system andcontributions are collected by thepension fund managers. In Chile,Mexico and Peru, there is no limit onfees, but there is not much variation inactual fee structure even without anycap. Average administrative charges,including funds management fees, varyfrom 1% to 1.8%. Generally, the assetmanagement fees vary from 0.5% to 1.5%in eastern European countries.

While going through theinternational fee structure, it will beuseful to know some of the value addedservices which really help to achievethe goal of an account holder. In theUK, after four years of public debate, itwas decided that every provider of DCpensions would be required to give anannual statement showing the likelyprojected value of the individual's fundat retirement age and the amount ofpension it might buy at current prices.

The values would only be estimates andwould depend on unknown variablesthat would inevitably change over time.But since the statement would be givenevery year, expectations wouldpractically be managed on an ongoingbasis.Conclusion:

While concluding, we can say thatgovernment of India has taken a goodstep for covering the people undersafety net of pension plan. But it needsto promote the concept with marketingefforts to reach the general public. Theinstrument will not be bought off theshelf without persuasion. Internationalexperience also suggests that voluntaryparticipation is usually very low -around 5%, and in the absence ofemployer sponsorship, increase inparticipation can only be stimulated byactive marketing.

Besides this, success of NPS isdependent on number of people joiningthis plan. For that along with marketingactivities, it is extremely important to winthe confidence of investors. Let us seehow to win the confidence of peopleand what can be the major concerns ofpeople?l Individuals accumulate fund for

their old age and hence safety ofthat corpus is extremely importantalong with the rate of return.

l Since Active choice is offered to

public, it is important to make themaware of the risk and returns in thevarious options.

l 5The pension regulatory bodyshould be given both power andresources to carry out spot checksand detailed investigationsindependent of any complaint.

l It is essential to ensure thatsubscriber receive clear and goodquality information on their pensionaccumulation.

l 6Promptness in account settlementsis the important service that peoplegenerally look for.

l Government should clarify thetaxation aspect of contribution ofpension, and pension to bereceived. Taxation aspect should beat par with Life insurance at least upto a certain limit.

l As NPS has the minimumcontribution amount of Rs. 6000 perannum and also provision toparticipate in equity market throughNPS, it certainly is affordable tomany people. Those people who arenot coming under any pensionschemes can participate in NPS. Aswe know though Public ProvidentFund (PPF), has minimum annualcontribution is Rs.500/-, it givesdefined return and not allow toparticipate in equity market. HenceNPS gives better chance to anaccount holder to cope up withinflation.If marketed properly and

administered efficiently, NPS is anexcellent plan to provide safety net topeople in their old age. Along withproviding a financial safety net, NPS willalso provide a life of dignity to India'ssenior citizens.q

5S.P.Subhedar: The pension RegulatoryEnvironment In India- A Suitable Model,,Pension Business in India, IIMBManagement Review , September 20046Shubhabrata Das : Survey on PensionPerceptions,Pension Business in India,IIMB Management Review , September2004

Cover Feature

the management accountant, February, 2010 101

IAS 26,Accounting and Reportingby Retirement Benefit Plans- A Closer LookK.S.Muthupandian*

I nternational Accounting Standard(IAS) 26, Accounting andReporting by Retirement Benefit

Plans, prescribes the principles forreporting of retirement benefit plans.Retirement benefit plans are sometimesreferred to by various other names, suchas 'pension schemes', 'superannuationschemes' or 'retirement benefitschemes'. In July 1985, the InternationalAccounting Standards Committee(IASC) issued the Exposure Draft E27,Accounting and Reporting byRetirement Benefit Plans. In January1987, the IASC issued IAS 26,Accounting and Reporting byRetirement Benefit Plans, operative forfinancial statements of retirementbenefit plans covering periodsbeginning on or after January 1, 1988.In 1994, the IASC reformatted IAS 26.In April 2001, the InternationalAccounting Standards Board (IASB)resolved that all Standards andInterpretation issued under previousConstitutions continued to beapplicable unless and until they wereamended or withdrawn.

ObjectiveThe objective of IAS 26 is to specify

measurement and disclosure principlesfor the reports of retirement benefitplans. All plans should include in theirreports a statement of changes in netassets available for benefits, a summaryof significant accounting policies and a

description of the plan and the effect ofany changes in the plan during theperiod.

Retirement benefit plans are normallydescribed as either defined contributionplans or defined benefit plans, eachhaving their own distinctivecharacteristics. Occasionally plans existthat contain characteristics of both.Such hybrid plans are considered to bedefined benefit plans for the purposesof IAS 26.

For defined contribution plans, theobjective of reporting is to provideinformation about the plan and theperformance of its investments.

For defined benefit plans, theobjective of reporting is to provideinformation about the financialresources and activities of the plan thatwill facilitate an assessment of therelationships between the accumulationof resources and plan benefits over time.

Scope and Application

IAS 26 applies for financialstatements of retirement benefit plans,where such financial statements areprepared. It deals with reporting to allparticipants as a group, and specificallydoes not deal with reports to individualsabout their retirement benefits. IAS 26does not deal with other forms ofemployment benefits such asemployment termination indemnities,deferred compensation arrangements,long service leave benefits special earlyretirement or redundancy plans, healthand welfare plans or bonus plans. It also

does not deal with government socialsecurity type arrangements.

IAS 26 regards a retirement benefitplan as a reporting entity separate fromthe employers of the participants in theplan. All other standards apply tofinancial statements of retirementbenefit plans to the extent that they arenot superseded by IAS 26. Note thatIAS 19, Employee Benefits is concernedwith the determination of the cost ofretirement benefits in the financialstatements of employers having plans.Hence IAS 26 complements IAS 19.

Retirement benefit plans with assetsinvested with insurance companies aresubject to the same accounting andfunding requirements as privatelyinvested arrangements. Accordingly,they are within the scope of IAS 26unless the contract with the insurancecompany is in the name of a specifiedparticipant or a group of participantsand the retirement benefit obligation issolely the responsibility of theinsurance company.

Many require the creation ofseparate funds, which may or may nothave separate legal identity and may ormay not have trustees, to whichcontributions are made and from whichretirement benefits are paid. IAS 26applies regardless of whether such afund is created and regardless ofwhether there are trustees.

Some retirement benefit plans havesponsors other than employers; IAS 26also applies to the financial statementsof such plans.

Key Definitions

Retirement benefit plans arearrangements whereby an entityprovides benefits for employees on orafter termination of service (either in theform of an annual income or as a lumpsum) when such benefits, or thecontributions towards them, can bedetermined or estimated in advance ofretirement from the provisions of adocument or from the entity's practices.

Cover Feature

*M.Com., FICWA, and Member of TamilNadu State Treasuries and Accounts Service,presently working as Treasury Officer,Ramanathapuram District, Tamil Nadu.

102 the management accountant, February, 2010

Defined contribution plans areretirement benefit plans for which theamounts to be paid as retirementbenefits are determined bycontributions to a fund together withinvestment earnings thereon.

Defined benefit plans are retirementbenefit plans under which amounts tobe paid as retirement benefits aredetermined by reference to a formulausually based on employees' earningsand / or years of service.

Funding is the transfer of assets toan entity (the fund) separate from theemployer's entity to meet futureobligations for the payment ofretirement benefits.

Participants are the members of aretirement benefit plan and others whoare entitled to benefits under the plan.

Net assets available for benefits arethe assets of a plan less liabilities otherthan the actuarial present value ofpromised retirement benefits.

Actuarial present value of promisedretirement benefits is the present valueof the expected payments by aretirement benefit plan to existing andpast employees, attributable to theservice already rendered.

Vested benefits are benefits, therights to which, under the conditionsof a retirement benefit plan, are notconditional on continued employment.

Prescribed Accounting TreatmentDefined contribution plans

The financial statements of adefined contribution plan shall containa statement of net assets available forbenefits and a description of thefunding policy.

Under a defined contribution plan,the amount of a participant's futurebenefits is determined by thecontributions paid by the employer, theparticipant, or both, and the operatingefficiency and investment earnings ofthe fund. An employer's obligation isusually discharged by contributions tothe fund. An actuary's advice is not

normally required although such adviceis sometimes used to estimate futurebenefits that may be achievable basedon present contributions and varyinglevels of future contributions andinvestment earnings.

The participants are interested inthe activities of the plan because theydirectly affect the level of their futurebenefits. Participants are interested inknowing whether contributions havebeen received and proper control hasbeen exercised to protect the rights ofbeneficiaries. An employer is interestedin the efficient and fair operation of theplan.

The objective of reporting by adefined contribution plan is periodicallyto provide information about the planand the performance of its investments.That objective is usually achieved byproviding financial statementsincluding the following:

(a) a description of significant activitiesfor the period and the effect of anychanges relating to the plan, and itsmembership and terms andconditions;

(b) statements reporting on thetransactions and investmentperformance for the period and thefinancial position of the plan at theend of the period; and

(c) a description of the investmentpolicies.

Defined benefit plans

The financial statements of adefined benefit plan shall contain either:

(a) a statement that shows:

(i) net assets available for benefits,

(ii) actuarial present value of promisedretirement benefits, distinguishingbetween vested benefits and non-vested benefits, and

(iii) resulting excess or deficit

(b) a statement of net assets availablefor benefits including either

(i) note disclosing actuarial present

value of promised retirementbenefits, distinguishing betweenvested benefits and non-vestedbenefits, or

(ii) a reference to this information in anaccompanying actuarial report

The actuarial present value ofpromised retirement benefits shall bebased on the benefits promised underthe terms of the plan of service renderedto date based on either current salarylevels or projected salaries. Disclosureof the basis is necessary. Changes inactuarial assumptions with significanteffect on the actuarial present value ofpromised retirement benefits shall alsobe disclosed.

The financial statements shallexplain the relationship between theactuarial present value of promisedretirement benefits and the net assetsavailable for benefits, and the policy forthe funding of promised benefits.

Under a defined benefit plan, thepayment of promised retirement benefitsdepends on the financial position of theplan and the ability of contributors tomake future contributions to the planas well as the investment performanceand operating efficiency of the plan.

A defined benefit plan needs theperiodic advice of an actuary to assessthe financial condition of the plan,review the assumptions and recommendfuture contribution levels.

The objective of reporting by adefined benefit plan is periodically toprovide information about the financialresources and activities of the plan thatis useful in assessing the relationshipsbetween the accumulation of resourcesand plan benefits over time. Thisobjective is usually achieved byproviding financial statementsincluding the following:

(a) a description of significant activitiesfor the period and the effect of anychanges relating to the plan, and itsmembership and terms andconditions;

Cover Feature

the management accountant, February, 2010 103

(b) statements reporting on thetransactions and investmentperformance for the period and thefinancial position of the plan at theend of the period;

(c) actuarial information either as partof the statements or by way of aseparate report; and

(d) a description of the investmentpolicies.

Actuarial present value of promisedretirement benefits

The present value of the expectedpayments by a retirement benefit planmay be calculated and reported usingcurrent salary levels or projected salarylevels up to the time of retirement ofparticipants.

The reasons given for adopting acurrent salary approach include:

(a) the actuarial present value ofpromised retirement benefits, beingthe sum of the amounts presentlyattributable to each participant in theplan, can be calculated moreobjectively than with projectedsalary levels because it involvesfewer assumptions;

(b) increases in benefits attributable toa salary increase become anobligation of the plan at the time ofthe salary increase; and

(c) the amount of the actuarial presentvalue of promised retirementbenefits using current salary levelsis generally more closely related tothe amount payable in the event oftermination or discontinuance of theplan.

The reasons given for adopting aprojected salary approach include:

(a) financial information should beprepared on a going concern basis,irrespective of the assumptions andestimates that must be made;

(b) under final pay plans, benefits aredetermined by reference to salariesat or near retirement date; hencesalaries, contribution levels and

rates of return must be projected;and

(c) failure to incorporate salaryprojections, when most funding isbased on salary projections, mayresult in the reporting of anapparent over funding when theplan is not over funded, or inreporting adequate funding whenthe plan is under funded.

The actuarial present value ofpromised retirement benefits based oncurrent salaries is disclosed in thefinancial statements of a plan to indicatethe obligation for benefits earned to thedate of the financial statements. Theactuarial present value of promisedretirement benefits based on projectedsalaries is disclosed to indicate themagnitude of the potential obligationon a going concern basis which isgenerally the basis for funding. Inaddition to disclosure of the actuarialpresent value of promised retirementbenefits, sufficient explanation mayneed to be given so as to indicate clearlythe context in which the actuarialpresent value of promised retirementbenefits should be read. Suchexplanation may be in the form ofinformation about the adequacy of theplanned future funding and of thefunding policy based on salaryprojections. This may be included in thefinancial statements or in the actuary'sreport.

Frequency of actuarial valuations

In many countries, actuarialvaluations are not obtained morefrequently than every three years.Where actuarial valuation has not beenprepared at the date of the financialstatements, the most recent valuationshall be used as a base and the date ofthe valuation shall be disclosed.

Financial statement content

For defined benefit plans,information is presented in one of thefollowing formats which reflect different

practices in the disclosure andpresentation of actuarial information:

(a) a statement is included in thefinancial statements that shows thenet assets available for benefits, theactuarial present value of promisedretirement benefits, and the resultingexcess or deficit. The financialstatements of the plan also containstatements of changes in net assetsavailable for benefits and changesin the actuarial present value ofpromised retirement benefits. Thefinancial statements may beaccompanied by a separateactuary's report supporting theactuarial present value of promisedretirement benefits;

(b) financial statements that include astatement of net assets available forbenefits and a statement of changesin net assets available for benefits.The actuarial present value ofpromised retirement benefits isdisclosed in a note to thestatements. The financialstatements may also beaccompanied by a report from anactuary supporting the actuarialpresent value of promisedretirement benefits; and

(c) financial statements that include astatement of net assets available forbenefits and a statement of changesin net assets available for benefitswith the actuarial present value ofpromised retirement benefitscontained in a separate actuarialreport.

In each format a trustees' report inthe nature of a management or directors'report and an investment report may alsoaccompany the financial statements.

Those in favour of the formatsdescribed in (a) and (b) believe that thequantification of promised retirementbenefits and other information providedunder those approaches help users toassess the current status of the planand the likelihood of the plan's

Cover Feature

104 the management accountant, February, 2010

obligations being met. They alsobelieve that financial statements shouldbe complete in themselves and not relyon accompanying statements. However,some believe that the format describedin (a) could give the impression that aliability exists, whereas the actuarialpresent value of promised retirementbenefits does not in their opinion haveall the characteristics of a liability.

Those who favour the formatdescribed in (c) believe that theactuarial present value of promisedretirement benefits should not beincluded in a statement of net assetsavailable for benefits as in the formatdescribed in (a) or even be disclosed ina note as in (b), because it will becompared directly with plan assets andsuch a comparison may not be valid.They contend that actuaries do notnecessarily compare actuarial presentvalue of promised retirement benefitswith market values of investments butmay instead assess the present valueof cash flows expected from theinvestments. Therefore, those in favourof this format believe that such acomparison is unlikely to reflect theactuary's overall assessment of the planand that it may be misunderstood. Also,some believe that, regardless of whetherquantified, the information aboutpromised retirement benefits should becontained solely in the separateactuarial report where a properexplanation can be provided.

IAS 26 accepts the views in favourof permitting disclosure of theinformation concerning promisedretirement benefits in a separate actuarialreport. It rejects arguments against thequantification of the actuarial presentvalue of promised retirement benefits.Accordingly, the formats described in(a) and (b) are considered acceptableunder IAS 26, as is the format describedin (c) so long as the financial statementscontain a reference to, and areaccompanied by, an actuarial report thatincludes the actuarial present value ofpromised retirement benefits.

Valuation of plan assets

Retirement benefit plan investmentsshall be carried at fair value. Formarketable securities, the fair value isthe market value. Where planinvestments are held for which anestimate of fair value is not possible(e.g. reliable measurement cannot beachieved), a disclosure explaining thereason for not using fair value isrequired. Where some investments arecarried at amounts other than marketvalue or fair value (e.g. market valueobtained from a thinly traded market),fair value (e.g. valuation technique) isgenerally disclosed, if not carried in thebooks.

Prescribed Disclosures

Financial statements of a retirementbenefit plan (either defined benefit ordefined contribution) shall contain thefollowing information:

1. a statement of changes in net assetsavailable for benefits

2. a summary of significant accountingpolicies

3. a description of the plan and theeffect of any changes in the planduring the period

Financial statements provided byretirement benefit plans include thefollowing, if applicable:

(a) a statement of net assets availablefor benefits disclosing:

(i) assets at the end of the periodsuitably classified;

(ii) the basis of valuation of assets;

(iii) details of any single investmentexceeding either 5% of the netassets available for benefits or 5%of any class or type of security;

(iv)details of any investment in theemployer; and

(v) liabilities other than the actuarialpresent value of promisedretirement benefits;

(b) a statement of changes in net assetsavailable for benefits showing thefollowing:

(i) employer contributions;

(ii) employee contributions;

(iii) investment income such as interestand dividends;

(iv)other income;

(v) benefits paid or payable (analysed,for example, as retirement, death anddisability benefits, and lump sumpayments);

(vi)administrative expenses;

(vii) other expenses;

(viii) taxes on income;

(ix) profits and losses on disposal ofinvestments and changes in valueof investments; and

(x) transfers from and to other plans;

(c) a description of the funding policy;

(d) for defined benefit plans, theactuarial present value of promisedretirement benefits (which maydistinguish between vested benefitsand non-vested benefits) based onthe benefits promised under theterms of the plan, on servicerendered to date and using eithercurrent salary levels or projectedsalary levels; this information maybe included in an accompanyingactuarial report to be read inconjunction with the relatedfinancial statements; and

(e) for defined benefit plans, adescription of the significantactuarial assumptions made and themethod used to calculate theactuarial present value of promisedretirement benefits.

The report of a retirement benefitplan contains a description of the plan,either as part of the financial statementsor in a separate report. It may containthe following:

(a) the names of the employers and theemployee groups covered;

(b) the number of participants receivingbenefits and the number of otherparticipants, classified asappropriate;

Cover Feature

the management accountant, February, 2010 105

(c) the type of plan-definedcontribution or defined benefit;

(d) a note as to whether participantscontribute to the plan;

(e) a description of the retirementbenefits promised to participants;

(f) a description of any plan terminationterms; and

(g) changes in items (a) to (f) during theperiod covered by the report.

It is not uncommon to refer to otherdocuments that are readily available tousers and in which the plan is described,and to include only information onsubsequent changes.

Notwithstanding the items whichare listed above, any information thatsupports the objective of reporting oris relevant to all participants as a groupshall be disclosed.

Comparative Indian Standard

The Accounting Standardcomparative to IAS 26 is underpreparation by the Institute of CharteredAccountants of India (ICAI).

Conclusion

Many retirement benefit plansprovide for the establishment ofseparate funds into which contributions

are made and out of which benefits arepaid. Such funds may be administeredby parties who act independently inmanaging fund assets. In India, thePension Fund Regulatory andDevelopment Authority (PFRDA) wasestablished in 2003 by Government ofIndia to act as a regulator for the pensionsector. As a first step towards institutingpensionary reforms, Government of Indiaand the State Governments moved froma defined benefit pension to a definedcontribution based pension system bymaking it mandatory for its newrecruits.q

CANCELLATION OF REGISTRATION UNDERREGULATION 25(1) OF CWA ACT, 1959

REGISTRATION NUMBERS CANCELLEDFOR JUNE-2010 EXAMINATION

UPTOERS/000904

NRS/001818 (EXCEPT 96, 119, 127, 140-145,488-499, 533-600, 901-923, 937-950)SRS/002191 (EXCEPT 2062–2104)

WRS/001818RSW/075376RAF/005824

RE-REGISTRATION

The students whose Registration Numbers have been cancelled (inclusive ofthe students registered upto 31st December-2002) as above but desire to takethe Institute’s Examination in June-2010 must apply for DE-NOVO Registrationand on being Registered DE-NOVO, Exemption from individual subject(s) atIntermediate/Final Examination of the Institute secured under their formerRegistration, if any, shall remain valid as per prevalent Rules.

For DE-NOVO Registration, a candidate shall have to apply to Director ofStudies in prescribed Form (which can be had either from the Institute’s H.Q.at Kolkata or from the concerned Regional Offices on payment of Rs. 5/-)along with a remittance of Rs. 2000/- only as Registration Fee through DemandDraft drawn in favour of THE ICWA OF INDIA, payble at KOLKATA.

Wishing you a very happy and Prosperous New Year.

Date: 27th January, 2010 Arnab Chakraborty,Director of Studies

Cover Feature

106 the management accountant, February, 2010

AS (15) - Accounting forRetirement Benefits in thefinancial statements ofemployer - Review andcomparative study ofAS- 15 with IAS-19 andFAS-36 (USA)S. Murugan*

Recently the audit findings ofnationalized banks revealed thatthe annual charge to the profits

towards future employees benefits wereinadequate so as to meet the committedlevel of employee benefits. The resultantaccumulated shortfall was found to bebeyond the reach of the banks torecoup from the normal businessoperation and sought permission torecoup in a distributed manner over theperiod of 3 to 5 years.

If this kind of blunder of grossnegligence could happen in aprofessionally managed organizedsectors, then the reliability of thedefined employee benefits is to bequestioned and the matter deserves athorough research. Applicability of theStandard

The enterprises which fall in anyone or more of the following categories,at any time during the accountingperiod:

(i) Enterprises whose equity or debtsecurities are listed whether in Indiaor outside India.

(ii) Enterprises which are in the processof listing their equity or debtsecurities as evidenced by the boardof directors’ resolution in thisregard.

(iii) Banks including co-operativebanks.

(iv)Financial institutions.

(v) Enterprises carrying on insurancebusiness.

(vi)All commercial, industrial andbusiness reporting enterprises,whose turnover for the immediatelypreceding accounting period on thebasis of audited financial statementsexceeds Rs. 50 crore. Turnover doesnot include ‘other income’.

Objective

The objective of this Statement isto prescribe the accounting anddisclosure for employee benefits. TheStatement requires an enterprise torecognize:

(a) a liability when an employee hasprovided service in exchange foremployee benefits to be paid in thefuture; and

(b) an expense when the enterpriseconsumes the economic benefit

*Deputy Manager/Finance, Bharat HeavyElectricals Ltd., Trichy Dt. Tamil Nadu.

arising from service provided by anemployee in exchange for employeebenefits.

Scope

1. This Statement should be appliedby an employer in accounting for allemployee benefits, except employeeshare-based payments.

2. This Statement does not deal withaccounting and reporting byemployee benefit plans.

3. The employee benefits to which thisStatement applies include thoseprovided:

(a) under formal plans or other formalagreements between an enterpriseand individual employees, groupsof employees or their represen-tatives;

(b) under legislative requirements, orthrough industry arrangements,whereby enterprises are required tocontribute to state, industry or othermulti-employer plans; or

(c) by those informal practices that giverise to an obligation. Informalpractices give rise to an obligationwhere the enterprise has no realisticalternative but to pay employeebenefits. An example of such anobligation is where a change in theenterprise's informal practices wouldcause unacceptable damage to itsrelationship with employees.

4. Employee benefits include :

(a) short-term employee benefits, suchas wages, salaries and socialsecurity contributions (e.g.,contribution to an insurancecompany by an employer to pay formedical care of its employees), paidannual leave, profit-sharing andbonuses (if payable within twelvemonths of the end of the period) andnon-monetary benefits (such asmedical care, housing, cars and freeor subsidised goods or services) forcurrent employees;

Cover Feature

the management accountant, February, 2010 107

(b) post-employment benefits such asgratuity, pension, other retirementbenefits, post-employment lifeinsurance and post-employmentmedical care;

(c) other long-term employee benefits,including long-service leave orsabbatical leave, jubilee or otherlong-service benefits, long-termdisability benefits and, if they arenot payable wholly within twelvemonths after the end of the period,profit-sharing, bonuses anddeferred compensation; and theaccounting for such benefits is dealtwith in the Guidance Note onAccounting for Employee Share-based Payments issued by theInstitute of Chartered Accountantsof India. 8 (d) termination benefits.Because each category identified in(a) to (d) above has differentcharacteristics, this Statementestablishes separate requirementsfor each category.

5. Employee benefits include benefitsprovided to either employees or theirspouses, children or otherdependants and may be settled bypayments (or the provision ofgoods or services) made either:

(a) directly to the employees, to theirspouses, children or otherdependants, or to their legal heirsor nominees; or

(b) to others, such as trusts, insurancecompanies.

6. An employee may provide servicesto an enterprise on a full-time, part-time, permanent, casual ortemporary basis. For the purpose ofthis Statement, employees includewhole-time directors and othermanagement personnel.

7. The following terms are used in thisStatement with the meaningsspecified: Employee benefits are allforms of consideration given by anenterprise in exchange for servicerendered by employees

Appraisal of Accounting Standard (15)

Employer - Employee relationship

The Standard does not define theterm " employee". Paragraph 6 of theStandard states that an employee mayprovide services to an enterprise to anenterprise on a full-time, part-time,permanent, casual or temporary basisand the term would also include hewhole-time directors and othersmanagement personnel. The Standardis applicable to all forms of employer-employee relationships. There is norequirement for a formal employeremployee relationship.

Employee benefits from informalrelationship

Paragraph 3 (c) of the Standarddefines employee benefits to includethose informal practices that give riseto an obligation where the enterprisehas no realistic alternative but to payemployee benefits.

Carried forward for Earned leave

Paragraph 7.2 of the Standarddefines 'Short-term' benefits asemployee benefits (other thantermination benefit) which fall duewholly within twelve months after theend of the period in which the employeerender the related service. Paragraph 8(b) of the Standard illustrates the term'Short-term benefits' to include "shortterm compensated absences (such aspaid annual leave) where he absencesare expected to occur within twelvemonths after the end of the period inwhich the employees render the relatedemployee service".

Measurement of cost of compensatedabsence

The cost of compensated absencesshould be measured as the additionalamount the enterprise expects to payas a result of the used entitlement.When an employee avails the leave at afuture date the cost of such leave wouldbe the compensation and otherbenefits, which the employee would e

paid for the period of his absence. Insome enterprises the amount payableto an employee on encashment wouldbe paid in case the leave is availed. Forinstance, an enterprise could have apractice of paying only basic wagewhen leave is enchased whereas heemployee would be entitled to basicwage, allowances and other benefitswhen the leave is availed. Suchsituations would require estimation forthe additional amount the enterpriseexpects to pay.

Carried forward of sick leave upto thetime of retirement

Sick leave is one of the types ofcompensated absences. Sick leave isconditional on the future event of anemployee reporting sick. An obligationarises as the employee renders service,which in creases the employee'sentitlement (Conditional orunconditional) to future compensatedabsences. Accumulating paid sick leavecreates an obligation because anyunused entitlement increases theemployee's entitlement to sick leave infuture periods. The probability that theemployee will be sick in those futureperiods affects the measurement of thatobligation, but does not determinewhether that obligation exists.

Concessional loan given to employees- Employee benefit

There granting of a loan by anenterprise to an employee at aconcessional rate of interest results ina benefit to an employee. At presentthe value of such benefit is recognizedover he period of the loan by accountingfor the interest income at the stipulatedrate instead of at the market rate.

Interest from Provident Fund - Definedbenefit plan or defined contributionplan

Section 17 of the EmployeeProvident Funds (EPF) Act, 1952empowers the Government to exemptany establishment from the provisions

Cover Feature

108 the management accountant, February, 2010

of the Employees' Provident Scheme,1952 provided that the rules of theprovident fund set up by theestablishment are not less favorablethan those specified in section 6 of theEPF Act and the employees are also inenjoyment of other provident fundbenefits which on the whole are not lessfavorable to the employees than thebenefits provided under the Act.

Accordingly, provident funds set upby employers, which require interestshortfall to be met by the employerwould be in effect defined benefit plansin accordance with the requirements ofparagraph 26(b) of AS 15.

Gratuity benefit scheme covered undergroup insurance scheme

A key distinction between definedcontribution plans and defined benefitplan is that in the case of defined benefitplans the actuarial risk (that benefit willcost more than expected) andinvestment risk fall, in substance, on theenterprise. If actuarial or investmentexperience are worse than expected, theenterprise's obligation may beincreased. Where a gratuity scheme iscovered under an insurance policy, thepayments to the insurance companyunder the policy would not beconsidered a defined contributions if theactuarial risk and investment risk isborne by the enterprise.

Separate trust created by enterprise toadminister a defined benefit plan

Where an enterprise has created aseparate trust to administer a definedbenefit plan, the fair value of the trustassets (net of liabilities) out of whichthe obligations are to be settled directlywould be deduced from the presentvalue of the defined benefit obligationand the net total would be recognizedin the Balance Sheet.

Defined benefit scheme covered undera Group Gratuity scheme

In the case of defined benefitschemes covered under a Group

Gratuity or other defined benefit schemewith an insurance company where theactuarial risk and investment risk havenot been transferred from theenterprise, the actuarial valuationcertificate provided by the insurancecompany can be relied upon by theenterprise.

Treatment of under provisioning madeunder pre-revised AS-15

Enterprise to which the pre-revisedAS 15 was applicable, were required tocomply with the provisions of theStandard in the preparation andpresentation of the financial statements.In case an enterprise had not created aprovision for retirement benefits as perthe earlier Standard, the amount ofbenefit as at the commencement of thefinancial year when the revisedStandard is first applied would be priorperiod item as it represents an omissionin the preparation of the financialstatements of earlier periods.

Disclosure requirements in respect ofaccounting policies on revised standard

Accounting policies refer to the specificaccounting principles and othermethods of applying those principlesin the preparation and presentation offinancial statements. Accordingly, anychange in the application for theprinciples of accounting for employeebenefits based on the revised AS 15 ascompared to the pre-revised Standardincluding the methods of applyingthose principles would be a change inaccounting policy and should be dealtwith as per the requirements ofparagraph 32 AS 5.

Gratuity

l Contribution by the employer to thefund may be own fund created undertrust or to any insurance company.

l Contributions to be calculated onthe basis of acturial valuation forboth of above cases.

l Contributions to be based onestimated salary at the time ofretirement.

l The difference between theestimated provision made every yearand actual gratuity paid at the timeof retirement to be booked in Profitand Loss account of the year ofretirement.

l As there is possible to have hugedifference between provisions andactual gratuity, the estimate shouldmore accurate

l The provisions of the earlier yearsmay have to be adjusted due toretrospective effect of wagerevision, changes in Govt. policiesetc.

l But, the standard is silent about suchprior period adjustment of provisionin the current year which result inhuge amount of booking expensesin the year retirement andunnecessarily lowering the profit ofthe enterprises.

Encashment of Earned Leave and sickleave

l Contributions are made out of ownfunds

l Contributions / provisions are madebased on actuarial valuation and

l On the basis of pattern/ ratio ofavailing and encashment of leaves

l Provisions are based on estimatedwages at the time of retirement.