Roadmap 2050 en bedrijvigheid in Nederland voor ... · Oil Gas Coal 1860 -… B1 A1T B2 A1B A2 A1FI...

40

Roadmap 2050 en bedrijvigheid in Nederland voor hernieuwbare energie Remko Ybema www.ecn.nl Ambassadeursconferentie - 20 januari 2011

Transcript of Roadmap 2050 en bedrijvigheid in Nederland voor ... · Oil Gas Coal 1860 -… B1 A1T B2 A1B A2 A1FI...

Roadmap 2050 en bedrijvigheid in Nederland voor hernieuwbare energie

Remko Ybema

www.ecn.nl

Ambassadeursconferentie - 20 januari 2011

Onderzoek van ECN

Zonne-energie WindenergieBiomassa, Locaties

2 21-1-2011

Zonne-energie Windenergie

BeleidsstudiesEfficiency & Infrastructure

Biomassa, kolen, milieu

Locaties• Petten• Amsterdam• Eindhoven (2011)• China (2011)

Inhoud

• Roadmap 2050• Bedrijvigheid op gebied van hernieuwbare energie

3 21-1-2011

Roadmap 2050

4 21-1-2011

Waarom energievisies (en –scenario’s) voor 2050?

• Voorbereiden op toekomstige uitdagingen• Aansprekend beeld creëren om naar toe te werken

5 21-1-2011

Roadmap 2050

• Initiatief van European Climate Foundation (ECF)• Uitgevoerd door ECF, McKinsey, Kema, Imperial

College London, Oxford Economics, E3G, ECN en OMAOMA

• Bedoeld om geloofwaardige paden te laten zien naar een Europese energievoorziening waar de CO2-uitstoot in 2050 met 80% is verminderd- Inzoomen op de elektriciteitssector- Strategische lessen trekken- Beleidsopties voor de volgende 5 jaar

6 21-1-2011

Wat is echt nieuw aan ECF Roadmap 2050?

• Groot aangepakt met een brede groep van instituten en bedrijven

• Consequenties van elektriciteitsvoorziening met veel hernieuwbare energie goed uitgezochtveel hernieuwbare energie goed uitgezocht

• Eerste analyse van fundamentele beleidsissues• High level presentatie en professioneel

PR-offensief

7 21-1-2011

Hoofdboodschappen Roadmap 2050 (1)

• Het is voor Europa mogelijk om in 2050 de CO2-uitstoot met 80% te verminderen

• Er is een sleutelrol voor besparing en elektriciteit• Elektriciteitsproductie moet ‘zero carbon’ worden • Elektriciteitsproductie moet ‘zero carbon’ worden

en dat is mogelijk met verschillende soorten brandstofmix met hernieuwbare energie, kernenergie en kolen/gas-centrales met CCS

8 21-1-2011

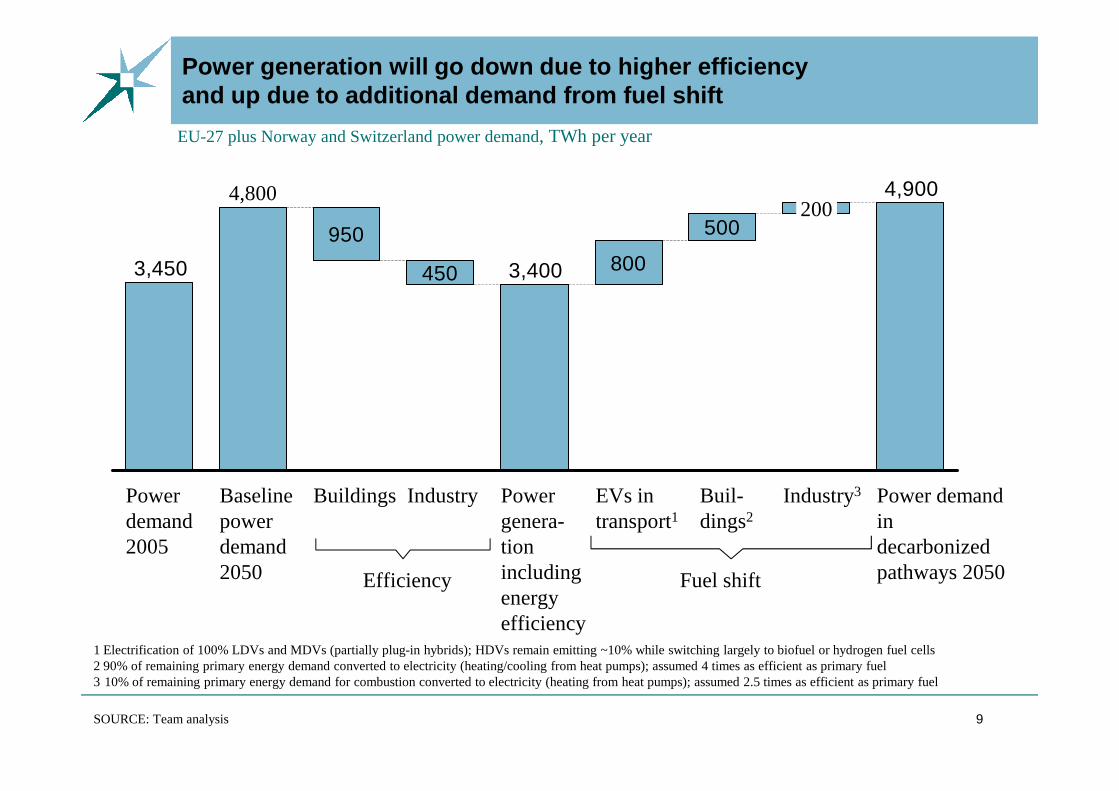

Power generation will go down due to higher efficie ncy and up due to additional demand from fuel shift

EU-27 plus Norway and Switzerland power demand, TWh per year

950

450 800

500

4,900

3,4003,450

4,800200

9

1 Electrification of 100% LDVs and MDVs (partially plug-in hybrids); HDVs remain emitting ~10% while switching largely to biofuel or hydrogen fuel cells2 90% of remaining primary energy demand converted to electricity (heating/cooling from heat pumps); assumed 4 times as efficient as primary fuel3 10% of remaining primary energy demand for combustion converted to electricity (heating from heat pumps); assumed 2.5 times as efficient as primary fuel

SOURCE: Team analysis

Baseline power demand 2050

BuildingsPower demand 2005

Power demand in decarbonized pathways 2050

Industry3Buil-dings2

EVs in transport1

Power genera-tion including energy efficiency

Industry

Efficiency Fuel shift

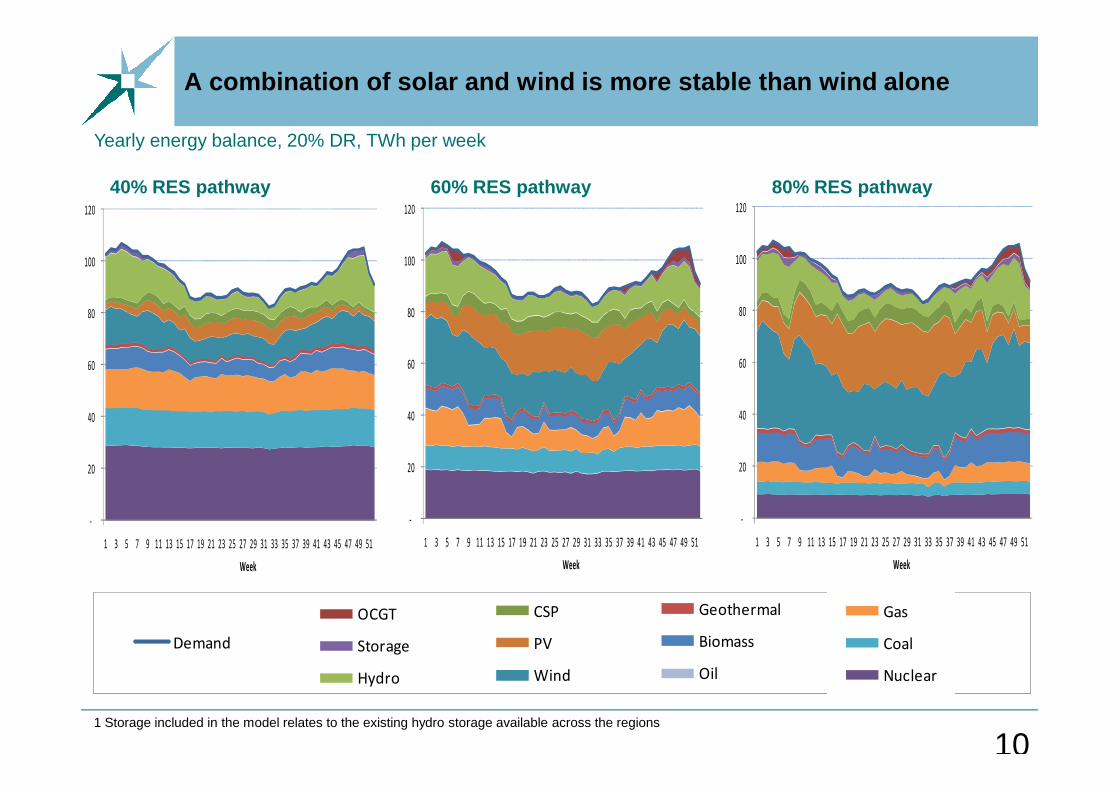

A combination of solar and wind is more stable than wind alone

1

Yearly energy balance, 20% DR, TWh per week

60

80

100

120

60

80

100

120

60

80

100

120

40% RES pathway 60% RES pathway 80% RES pathway

10

Gas

Coal

Nuclear

1 Storage included in the model relates to the existing hydro storage available across the regions

-

20

40

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Week

Geothermal

Biomass

Oil

CSP

PV

Wind

OCGT

Storage

Hydro

Demand

-

20

40

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Week

-

20

40

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Week

Hoofdboodschappen Roadmap 2050 (2)

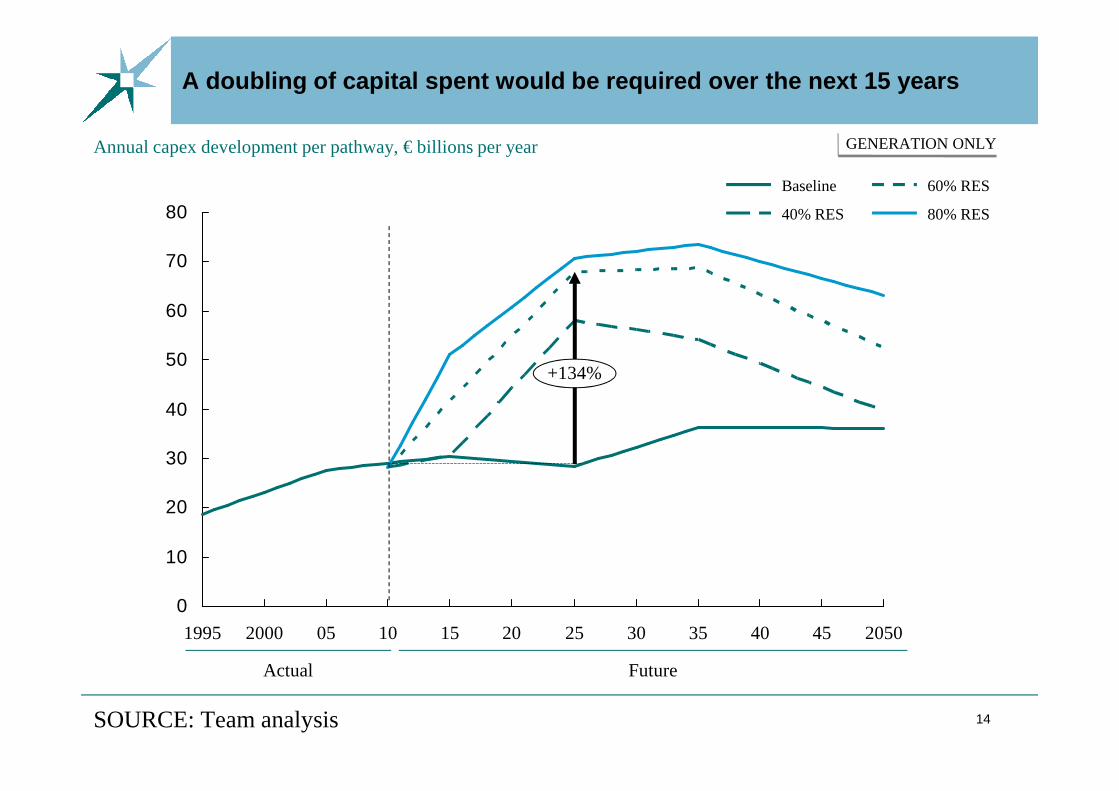

• Met veel hernieuwbare energie is er een intermittency issue- Veel meer trans-Europese transmissie is nodig

in Europa en vraagsturingin Europa en vraagsturing• De extra kosten vallen mee• De kapitaalskosten van de energiesector zullen

fors toenemen• Nu beginnen, anders hogere kosten

11 21-1-2011

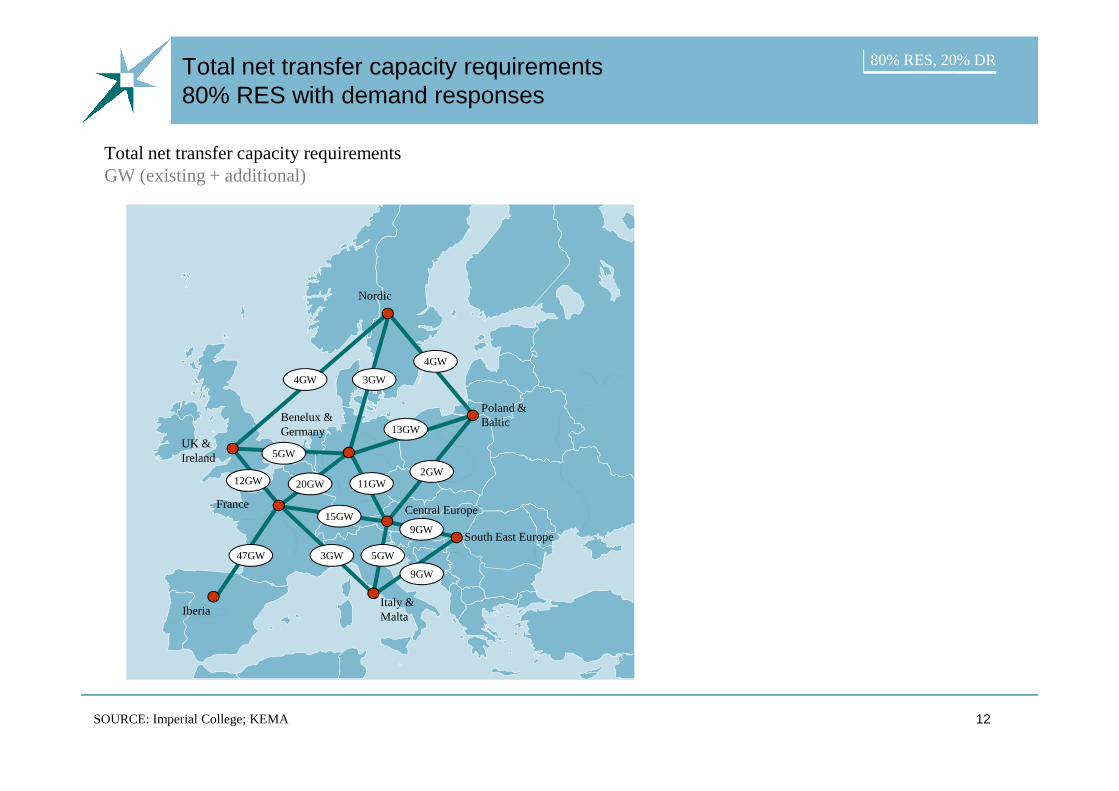

Total net transfer capacity requirements 80% RES with demand responses

80% RES, 20% DR

Nordic

4GW

4GW 3GW

Total net transfer capacity requirements GW (existing + additional)

12SOURCE: Imperial College; KEMA

Iberia

France

UK & Ireland

Benelux & Germany

Italy & Malta

South East Europe

Central Europe

Poland & Baltic

5GW

11GW20GW

47GW

9GW

9GW

12GW

13GW

15GW

3GW 5GW

2GW

60

70

80

90

100

110

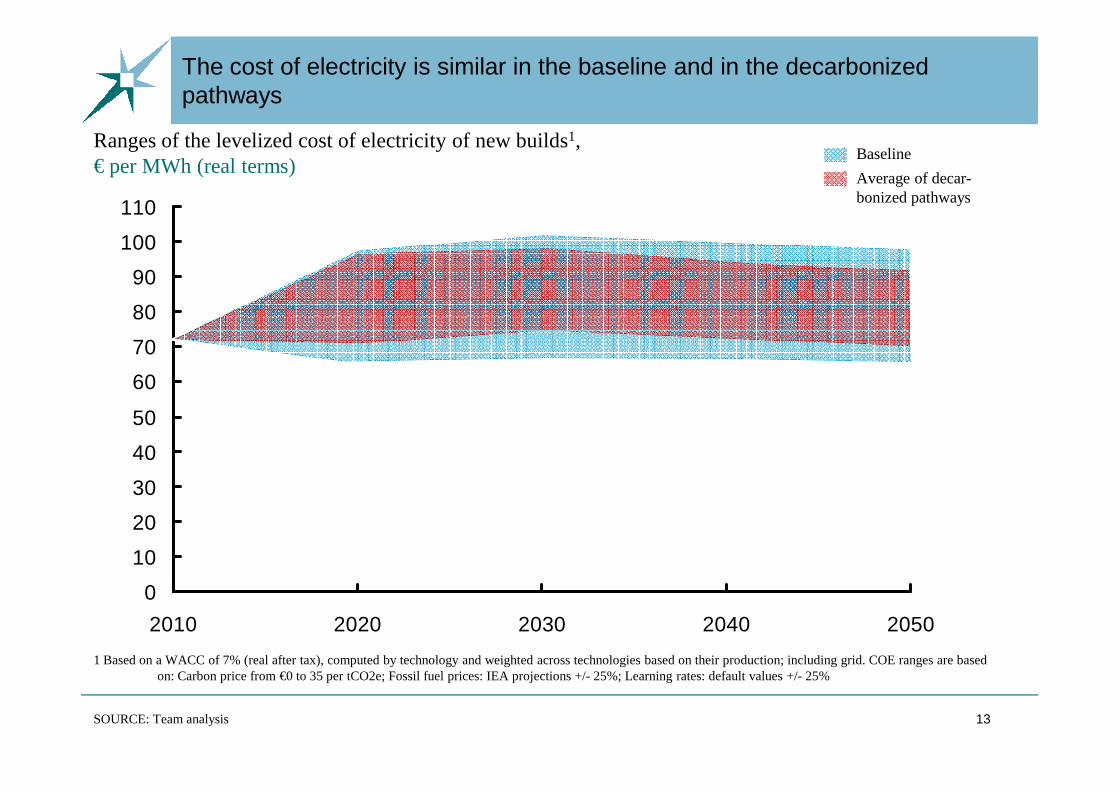

The cost of electricity is similar in the baseline and in the decarbonized pathways

Baseline

Average of decar-bonized pathways

Ranges of the levelized cost of electricity of new builds1, € per MWh (real terms)

13

0

10

20

30

40

50

2010 2020 2030 2040 2050

SOURCE: Team analysis

1 Based on a WACC of 7% (real after tax), computed by technology and weighted across technologies based on their production; including grid. COE ranges are based on: Carbon price from €0 to 35 per tCO2e; Fossil fuel prices: IEA projections +/- 25%; Learning rates: default values +/- 25%

50

60

70

80

+134%

80% RES

60% RES

40% RES

Baseline

Annual capex development per pathway, € billions per year GENERATION ONLY

A doubling of capital spent would be required over the next 15 years

14

0

10

20

30

40

205045403530252015100520001995

Actual Future

SOURCE: Team analysis

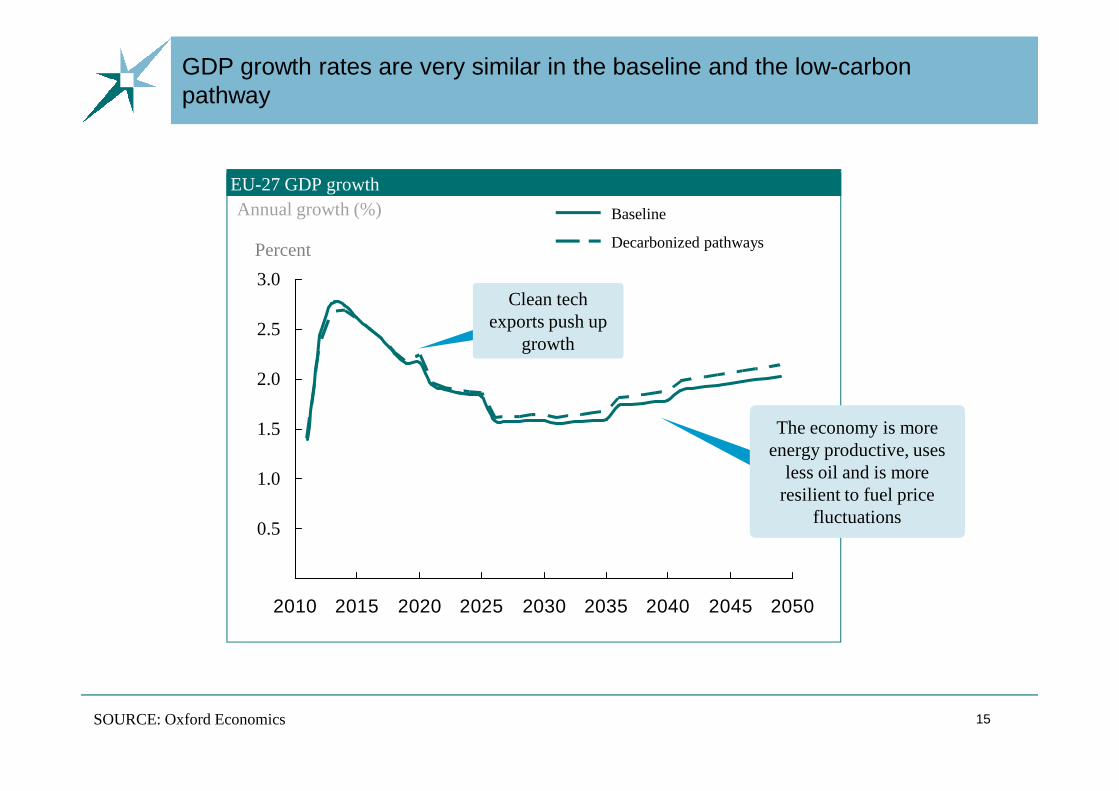

EU-27 GDP growth

Percent

3.0

2.5

2.0

GDP growth rates are very similar in the baseline and the low-carbon pathway

Baseline

Decarbonized pathways

Clean tech exports push up

growth

Annual growth (%)

15SOURCE: Oxford Economics

2010 2015 2020 2025 2030 2035 2040 2045 2050

0.5

1.5

1.0

The economy is more energy productive, uses

less oil and is more resilient to fuel price

fluctuations

Wat is nodig om de Roadmap 2050 te realiseren? (1) – een breed pakket

• Tempo energiebesparing moet sterk toenemen- Maak EU van doelstelling energiebesparing een verplichting- Scherp ESD aan en versterk Eco-Design richtlijn richting BAT- EPBD toepassen op alle gebouwen- EPBD toepassen op alle gebouwen- Hoge CO2-prijs

• Nieuwe technieken volwassen en commercieel laten worden: SET-plan uitvoeren en markt stimuleren

• Pas het ETS aan: een hogere en stabiele CO2-prijs- Aanscherpen van CO2-plafond 2020 en duidelijkheid over

plafond na 2020, minder CDM- Maatregelen voor meer prijsstabiliteit

16 21-1-2011

Wat is nodig om de Roadmap 2050 te realiseren? (2)

• Duidelijkheid voor de elektriciteitssector bieden- Financiële prikkels voor o.a. CCS- Regulering

• Ontwikkel regionale roadmaps voor de power sector samen •met de belanghebbenden

• Ontwikkel capaciteitsmarkten of andere manieren om elektriciteitsmarkt te verbeteren

• Zorg dat de transitie gefinancierd kan worden• Introduceer een Climate and Resource Directive

17 21-1-2011

Kanttekeningen bij visiedocumenten

• Veronderstellen voorspoedige technische innovaties• Weinig aandacht voor andere belangen, voorkeuren

en weerstand tegen verandering- Kosten gaan voor de baten uit- Kosten gaan voor de baten uit- Prisoners dilemma

• Grote mate van optimaliteit bij de realisatie verondersteld - In de praktijk vaak gebrek aan coördinatie, trage

besluitvorming, etc.• Benodigde nationale beleid nauwelijks uitgewerkt

18 21-1-2011

Bedrijvigheid op gebied van hernieuwbare energie

19 21-1-2011

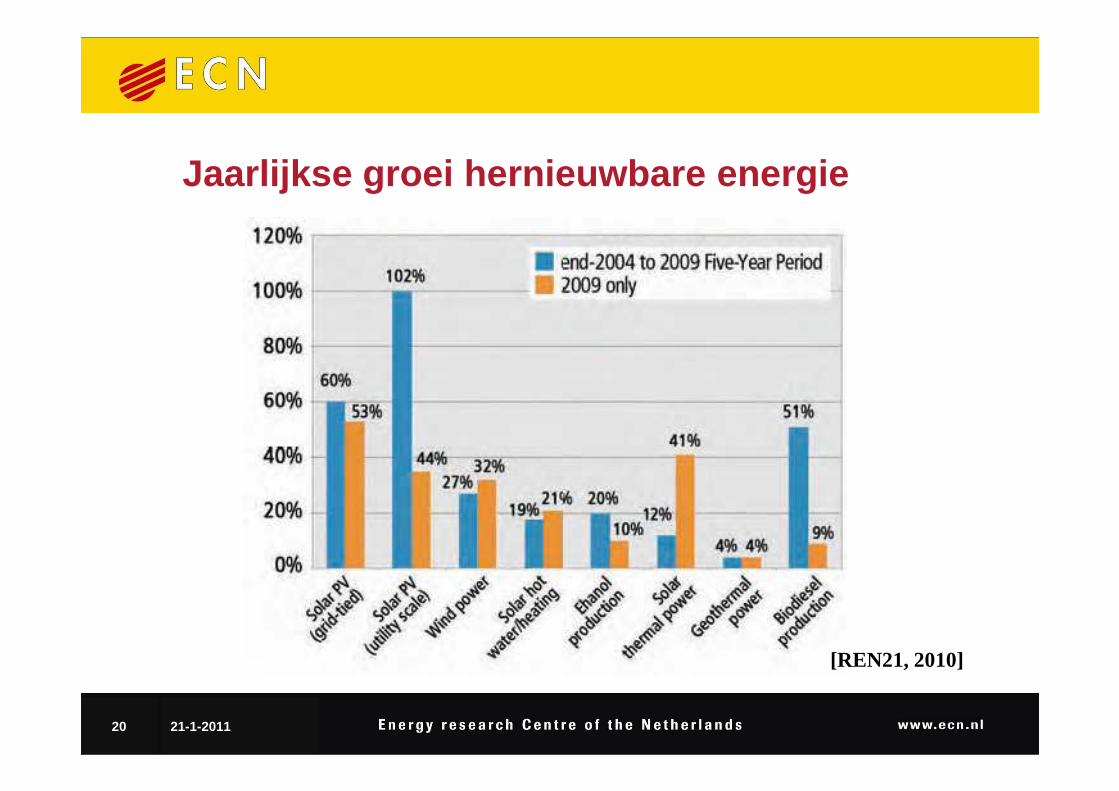

Jaarlijkse groei hernieuwbare energie

20 21-1-2011

[REN21, 2010]

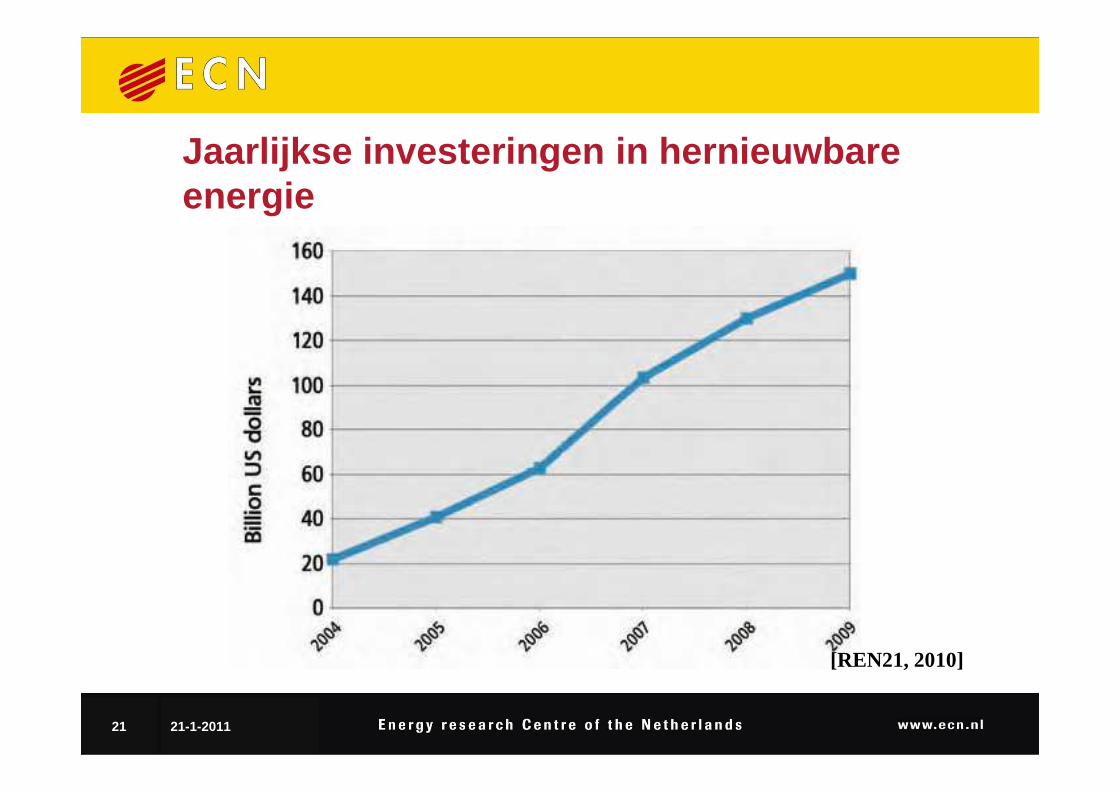

Jaarlijkse investeringen in hernieuwbare energie

21 21-1-2011

[REN21, 2010]

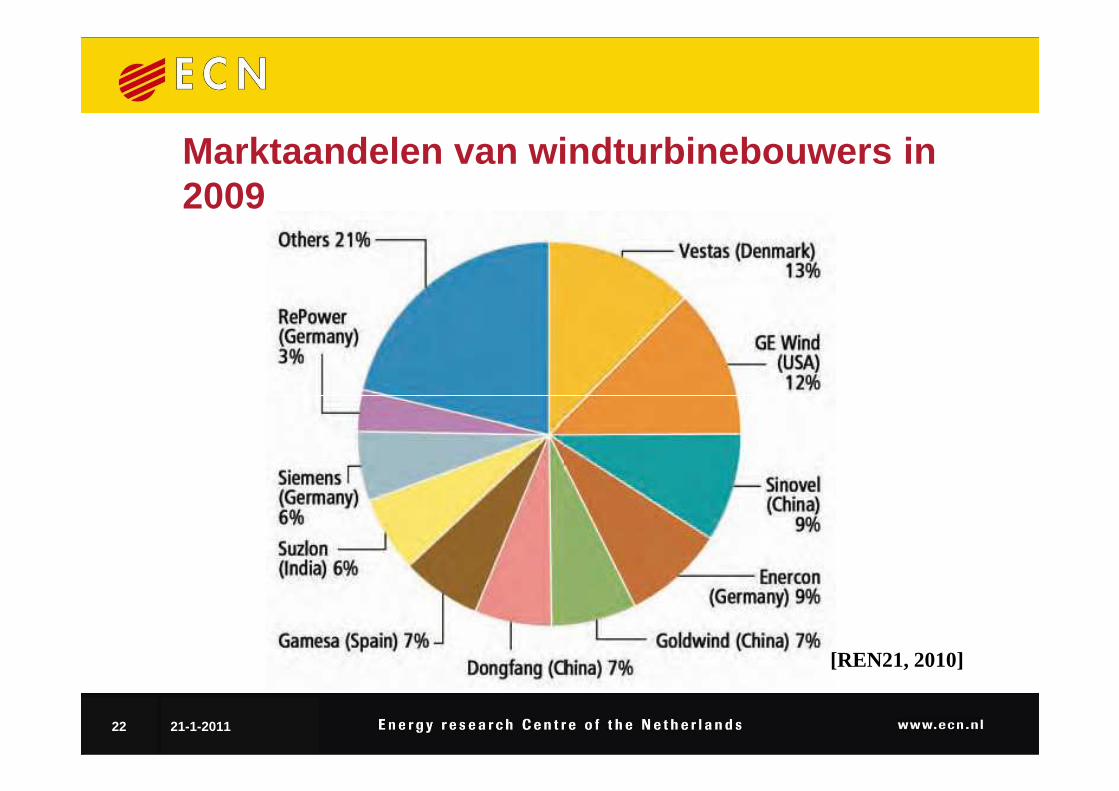

Marktaandelen van windturbinebouwers in 2009

22 21-1-2011

[REN21, 2010]

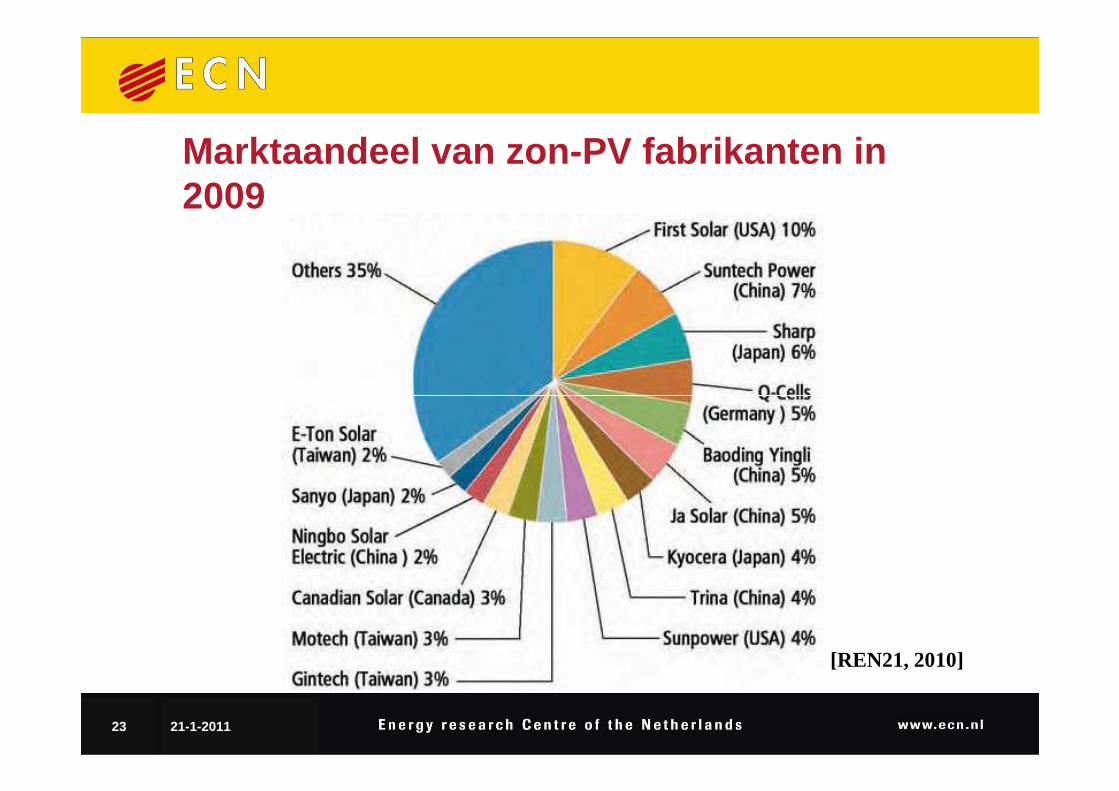

Marktaandeel van zon-PV fabrikanten in 2009

23 21-1-2011

[REN21, 2010]

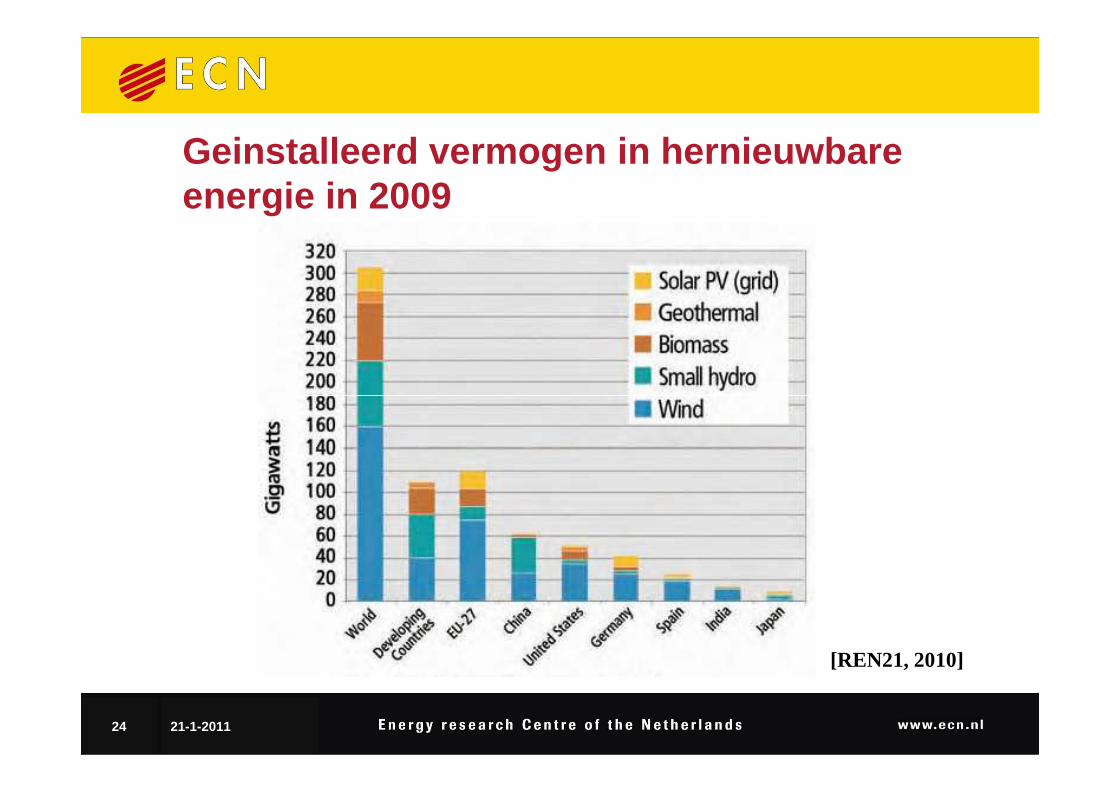

Geinstalleerd vermogen in hernieuwbare energie in 2009

24 21-1-2011

[REN21, 2010]

Bedrijvigheid op gebied van energie in Nederland

• Aardgas: meer dan 10 mrd baten, 11000 banen• Energiebesparing: 20.000 tot 30.000 banen• Hernieuwbare energie: 11.000 banen, omzet van

5,5 mrd5,5 mrd

• En energiebedrijven, raffinaderijen, ….

25 21-1-2011

Nederlandse duurzame energiesector

• Geen grote Nederlandse spelers (kleine thuismarkt)• Vooral R&D en consultancy en toelevering en

assemblage• Veel kleine bedrijven• Veel kleine bedrijven• Vooral afvalketen, zon-PV, zon-thermisch, wind en

biogas• Exportpositie het sterkst bij zon-PV (270 mln), wind

op zee (270 mln) en biobrandstoffen (80 mln)

26 21-1-2011

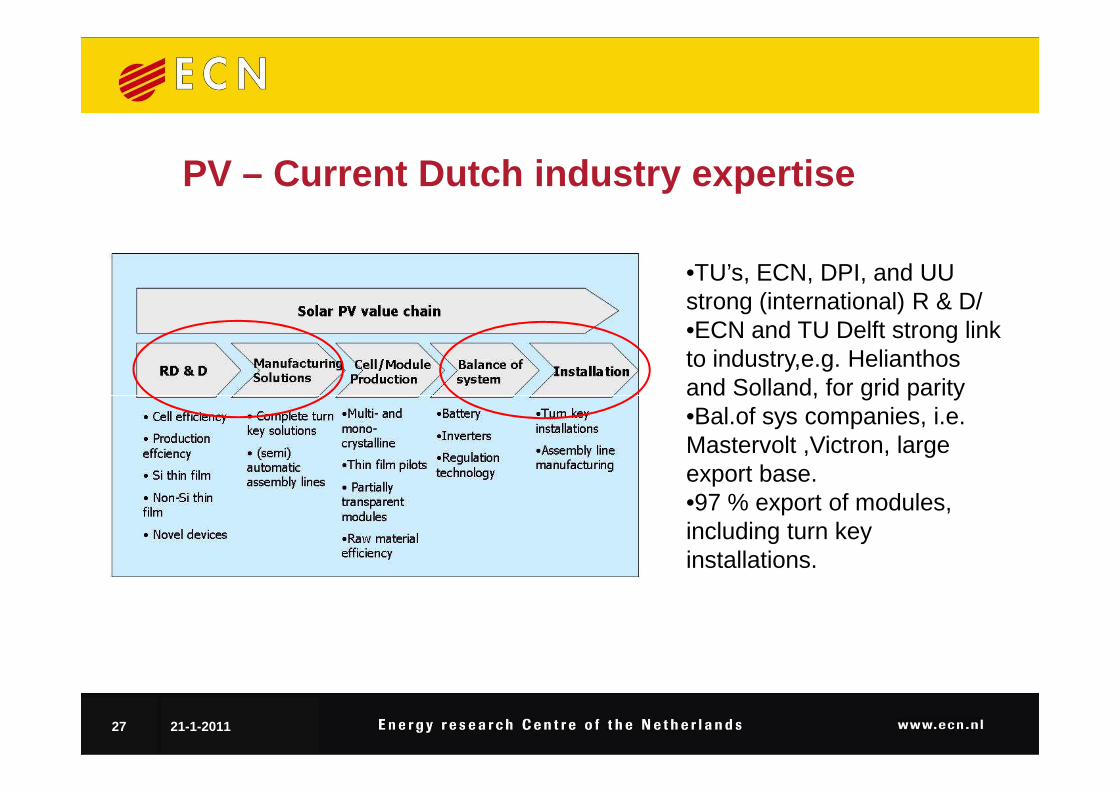

PV – Current Dutch industry expertise

•TU’s, ECN, DPI, and UU strong (international) R & D/•ECN and TU Delft strong link to industry,e.g. Helianthos and Solland, for grid parity

27 21-1-2011

and Solland, for grid parity•Bal.of sys companies, i.e. Mastervolt ,Victron, large export base.•97 % export of modules, including turn key installations.

PV – Dutch position in global market

• Comparative advantage in cell manufacturing machines, assembly lines. Strong ties with China.

• Substantial expertise in novel devices, thin-film and building integrated R & D.

•

28 21-1-2011

• Scheuten, OTB, Mastervolt, Eurotron, Solland, TU’s and ECN main players.

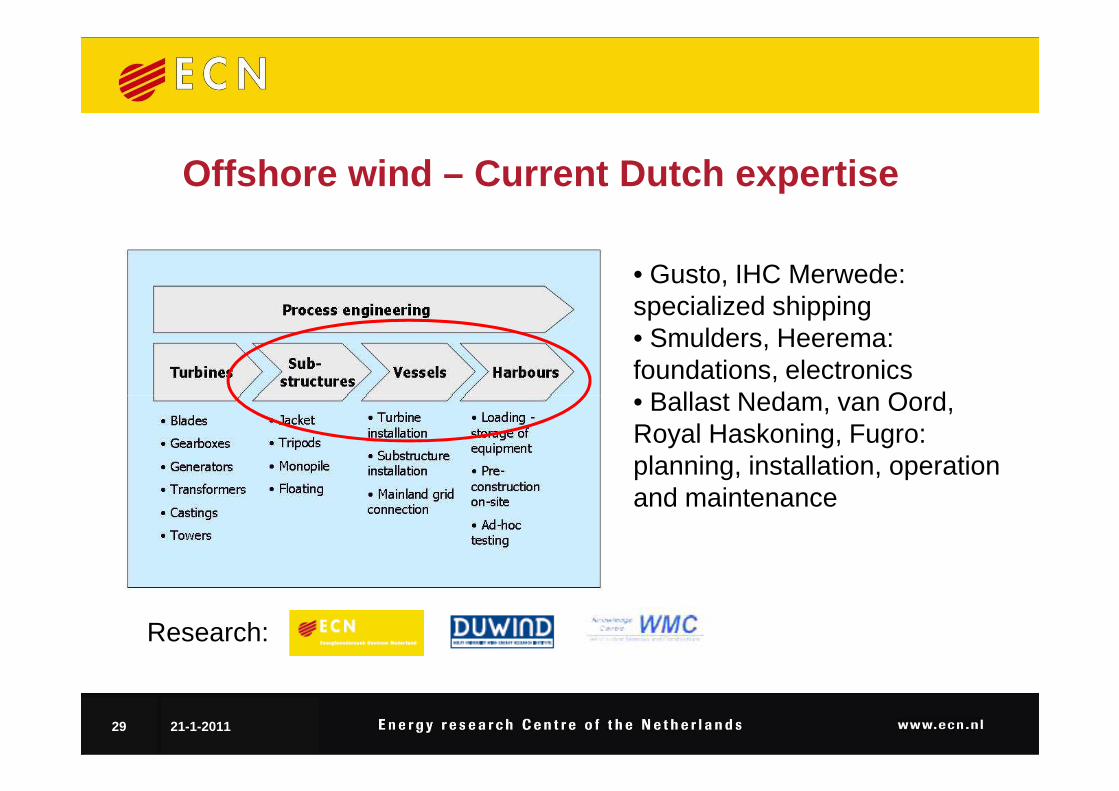

Offshore wind – Current Dutch expertise

• Gusto, IHC Merwede: specialized shipping• Smulders, Heerema: foundations, electronics• Ballast Nedam, van Oord,

29 21-1-2011

• Ballast Nedam, van Oord, Royal Haskoning, Fugro: planning, installation, operation and maintenance

Research:

Offshore wind – Global position of Dutch industry

• Highly specialized knowledge, benefit from oil& gas exploration experiences • In the future, 1/3 cost for wind turbine, 2/3 operation

30 21-1-2011

wind turbine, 2/3 operation & maintenance• Netherlands is well positioned in the ‘process engineering’• Also others with oil & gas expertise could benefit: UK, Norway

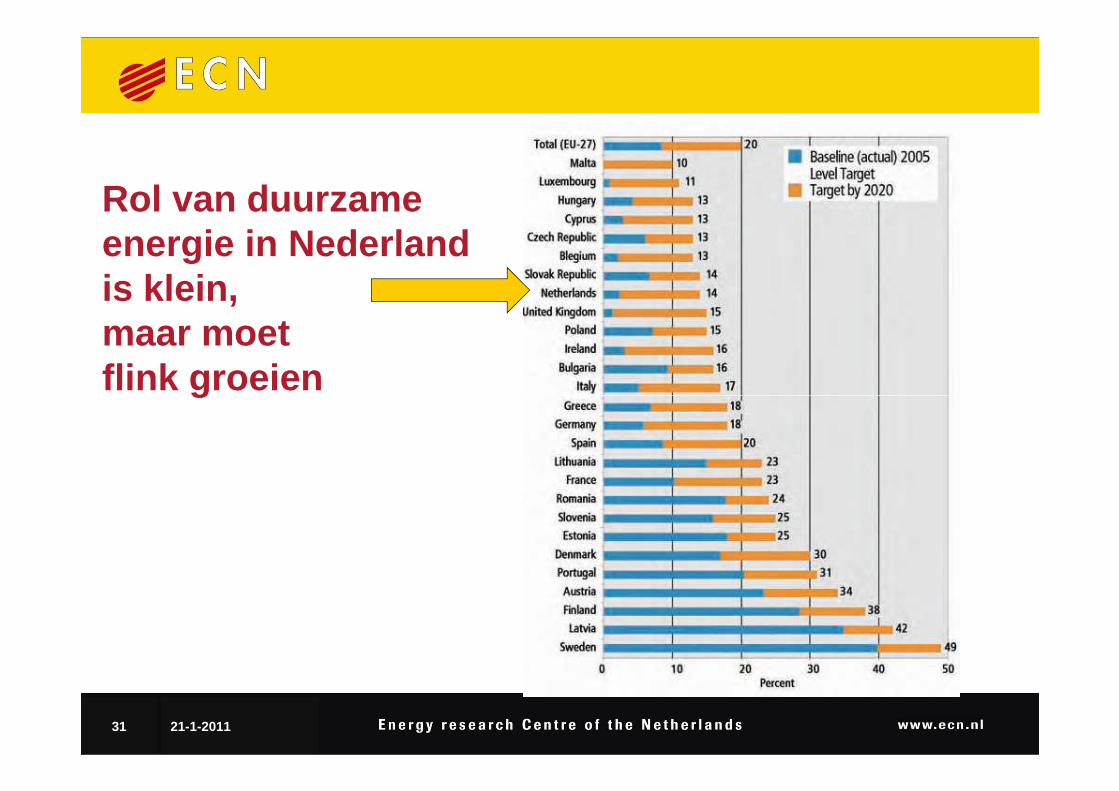

Rol van duurzameenergie in Nederlandis klein,maar moet flink groeienflink groeien

31 21-1-2011

Conclusies

• Een duurzame energievoorziening is mogelijk, maar dit vergt een grote tranistie, veel beleid en een goede coördinatie

• Nederland is nog vooral een gas- en olieland met • Nederland is nog vooral een gas- en olieland met een kleine thuismarkt hernieuwbare energie

• Er bestaan nog volop kansen voor Nederlandse bedrijven op gebied van hernieuwbare energie, vooal bij zon-PV, wind offshore en bio-energie

32 21-1-2011

Vragen?

33 21-1-2011

Reserve sheetsExterne ontwikkelingen

34 21-1-2011

Betaalbaar, betrouwbaar, schoon

• Betaalbaarheid: gaat goed, nog wel• Betrouwbaarheid: gaat goed, in veel regio’s • Schoon: Internationaal zwak klimaatbeleid,

lage CO prijslage CO2 prijs• Breed besef bij bedrijven en burgers dat

verduurzaming nodig is• Hernieuwbare energie groeit sterk, de maakindustrie

verschuift naar China en India

35 21-1-2011

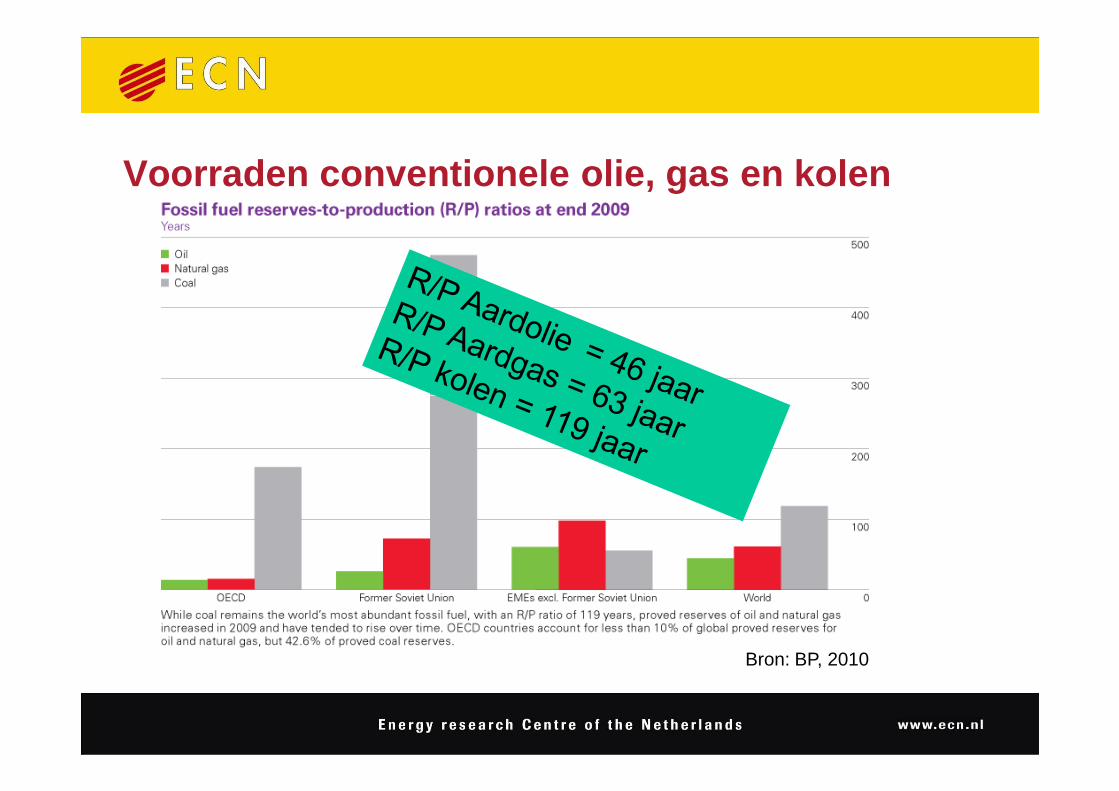

Voorraden conventionele olie, gas en kolen

Bron: BP, 2010

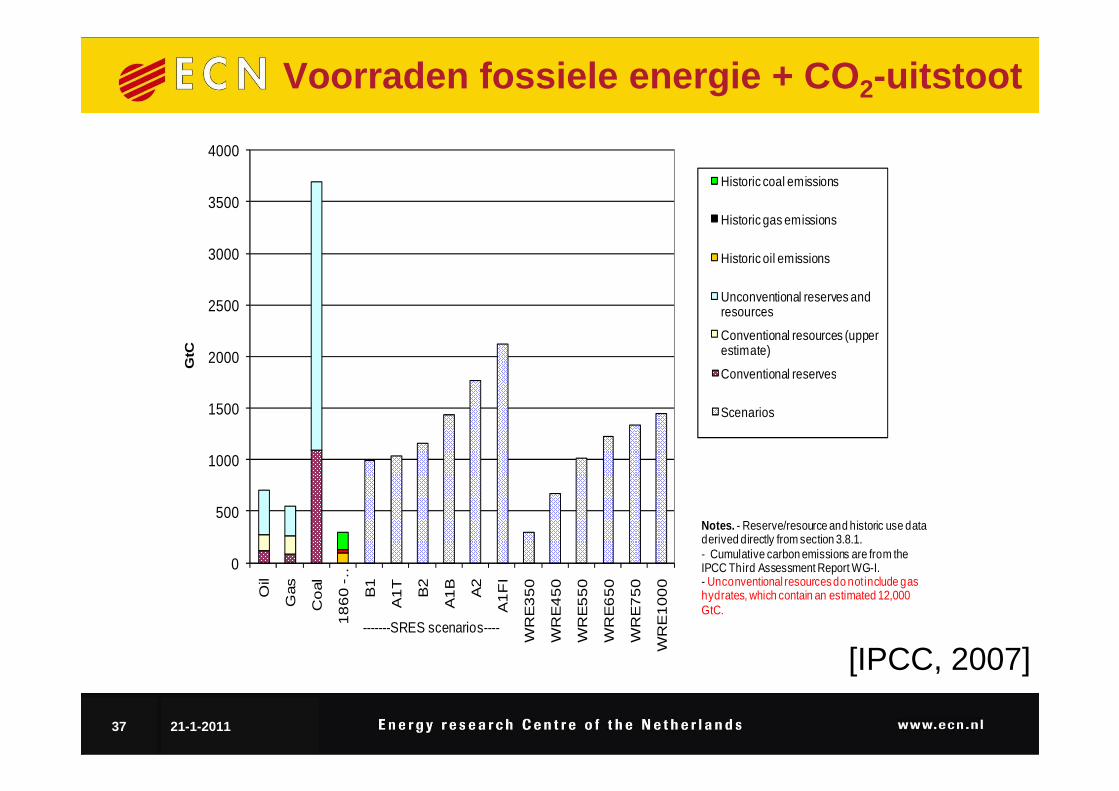

Voorraden fossiele energie + CO 2-uitstoot

2000

2500

3000

3500

4000

GtC

Historic coal emissions

Historic gas emissions

Historic oil emissions

Unconventional reserves and resources

Conventional resources (upper estimate)

Conventional reserves

37 21-1-2011

0

500

1000

1500

Oil

Gas

Co

al

18

60

-…

B1

A1

T

B2

A1

B

A2

A1

FI

WR

E3

50

WR

E4

50

WR

E5

50

WR

E6

50

WR

E7

50

WR

E1

00

0

Scenarios

Notes. - Reserve/resource and historic use data derived directly from section 3.8.1.- Cumulative carbon emissions are from the IPCC Third Assessment Report WG-I.- Unconventional resources do not include gas hydrates, which contain an estimated 12,000 GtC.

-------SRES scenarios----

[IPCC, 2007]

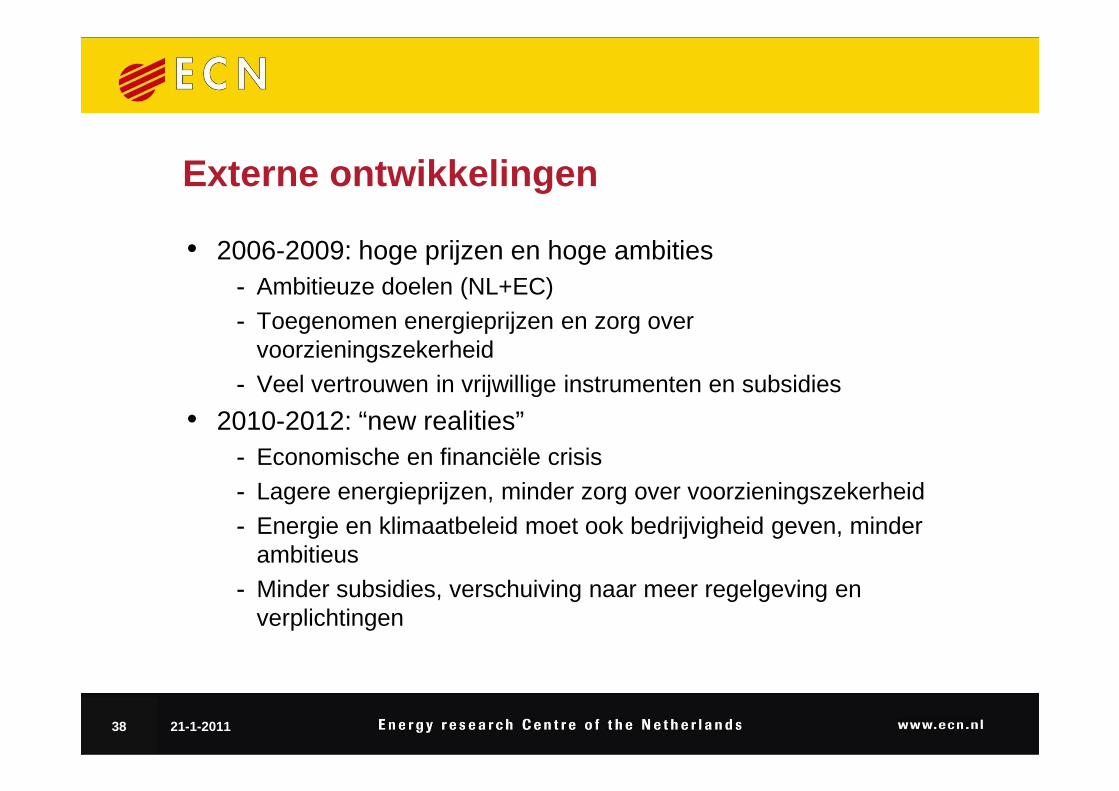

Externe ontwikkelingen

• 2006-2009: hoge prijzen en hoge ambities- Ambitieuze doelen (NL+EC)- Toegenomen energieprijzen en zorg over

voorzieningszekerheid- Veel vertrouwen in vrijwillige instrumenten en subsidies- Veel vertrouwen in vrijwillige instrumenten en subsidies

• 2010-2012: “new realities”- Economische en financiële crisis- Lagere energieprijzen, minder zorg over voorzieningszekerheid- Energie en klimaatbeleid moet ook bedrijvigheid geven, minder

ambitieus- Minder subsidies, verschuiving naar meer regelgeving en

verplichtingen

38 21-1-2011

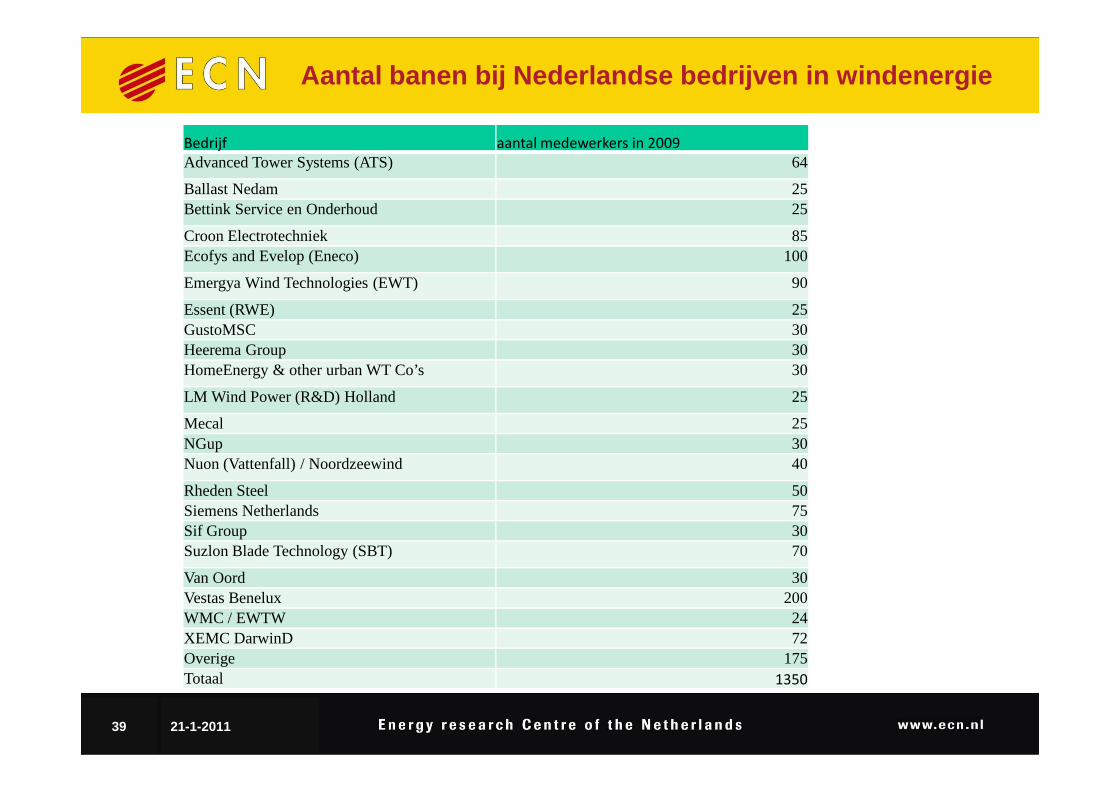

Aantal banen bij Nederlandse bedrijven in windenerg ie

Bedrijf aantal medewerkers in 2009

Advanced Tower Systems (ATS) 64

Ballast Nedam 25Bettink Service en Onderhoud 25

Croon Electrotechniek 85Ecofys and Evelop (Eneco) 100

Emergya Wind Technologies (EWT) 90

Essent (RWE) 25GustoMSC 30Heerema Group 30HomeEnergy & other urban WT Co’s 30

LM Wind Power (R&D) Holland 25LM Wind Power (R&D) Holland 25

Mecal 25NGup 30Nuon (Vattenfall) / Noordzeewind 40

Rheden Steel 50Siemens Netherlands 75Sif Group 30Suzlon Blade Technology (SBT) 70

Van Oord 30Vestas Benelux 200WMC / EWTW 24XEMC DarwinD 72Overige 175Totaal 1350

39 21-1-2011

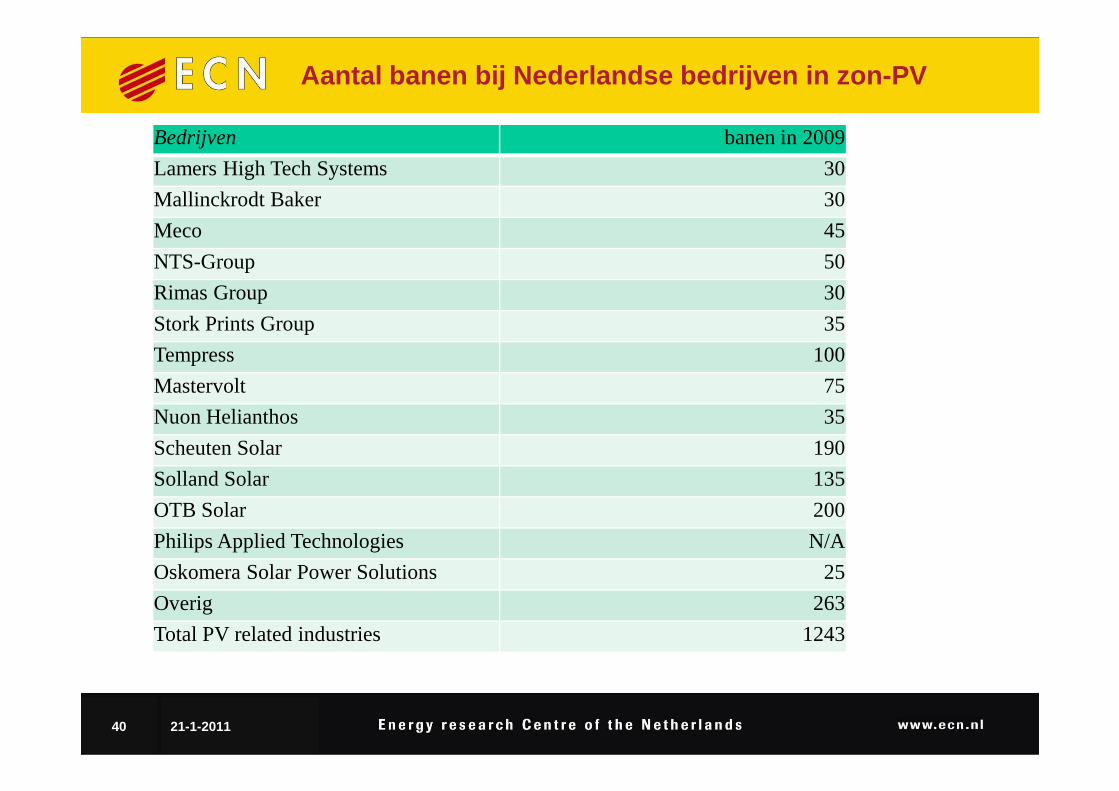

Bedrijven banen in 2009

Lamers High Tech Systems 30

Mallinckrodt Baker 30

Meco 45

NTS-Group 50

Rimas Group 30

Stork Prints Group 35

Tempress 100

Mastervolt 75

Aantal banen bij Nederlandse bedrijven in zon-PV

Mastervolt 75

Nuon Helianthos 35

Scheuten Solar 190

Solland Solar 135

OTB Solar 200

Philips Applied Technologies N/A

Oskomera Solar Power Solutions 25

Overig 263

Total PV related industries 1243

40 21-1-2011