Kamal Kant Project

38

HISTORY Life Insurance Corporation of India set up LIC Mutual Fund on 19th June 1989 and contributed Rs. 2 Crores towards the corpus of the Fund. LIC Mutual F und was constituted as a Trust in accordance with the provisions of the Indian Trust Act, 1882. The settlor is not responsible for the management of the Trust. The settlor is also not responsible or liable for any loss or shortfall resulting in any of the schemes of LIC Mutual Fund. The Trustees of the LIC Mutual Fund have exclusive ownership of Trust Fund and are vested with general power of superintendence, discretion and management of the affairs of the Trust. LIC Mutal Fund Asset Management Company Ltd. was formed on 20th April 1994 in compliance with the S ecurities and Exchange Board of India (Mutual Funds) Regulations, 1993. The Company commenced business on 29th April 1994. The Trustees of LI C Mutual Fund have appointed LIC Mutual Fund Asset Management Company Ltd. as the I nvestment Managers for LIC Mutual Fund. The Trustees are responsible for appointing a Custodian. The Trustees should also ensure that the activities of the Trust and the Asset Management Company are in accordance with the Trust Deed and the SEBI Mutual Fund Regulations as amended from time to time. The Trustees have also to report periodically to SEBI on the functioning of the Fund. The investors under the schemes can obtain a copy of the Trust Deed, the text of the concerned Scheme as also a copy of the Annual Report, on a written r equest made to the LIC Mutual Fund Asset Management Company Ltd. at a nominal price of Rs. 10/-.

-

Upload

kamalkantshukla -

Category

Documents

-

view

220 -

download

0

Transcript of Kamal Kant Project

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 1/38

HISTORY

Life Insurance Corporation of India set up LIC Mutual Fund on 19th June 1989 and

contributed Rs. 2 Crores towards the corpus of the Fund. LIC Mutual Fund was

constituted as a Trust in accordance with the provisions of the Indian Trust Act,

1882. The settlor is not responsible for the management of the Trust. The settlor is

also not responsible or liable for any loss or shortfall resulting in any of the

schemes of LIC Mutual Fund.

The Trustees of the LIC Mutual Fund have exclusive ownership of Trust Fund and

are vested with general power of superintendence, discretion and management of

the affairs of the Trust. LIC Mutal Fund Asset Management Company Ltd. was

formed on 20th April 1994 in compliance with the Securities and Exchange Board

of India (Mutual Funds) Regulations, 1993. The Company commenced business on

29th April 1994. The Trustees of LIC Mutual Fund have appointed LIC Mutual

Fund Asset Management Company Ltd. as the Investment Managers for LIC

Mutual Fund. The Trustees are responsible for appointing a Custodian. The

Trustees should also ensure that the activities of the Trust and the AssetManagement Company are in accordance with the Trust Deed and the SEBI Mutual

Fund Regulations as amended from time to time. The Trustees have also to report

periodically to SEBI on the functioning of the Fund.

The investors under the schemes can obtain a copy of the Trust Deed, the text of the

concerned Scheme as also a copy of the Annual Report, on a written request made

to the LIC Mutual Fund Asset Management Company Ltd. at a nominal price of Rs.10/-.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 2/38

LIC MUTUAL FUND TRUSTEE COMPANY

PRIVATE LIMITED

NAME OF THE DIRECTOR

SHRI THOMAS MATHEW T. (Chairman)

SHRI P. N. MEHTA (Indepedent Director)

SHRI P. N. SHAH (Indepedent Director)

SHRI V.G. SUBRAMANIAN (Indepedent Director)

SHRI T. C. VENKAT SUBRAMANIAN (Indepedent Director)

SHRI M. RAGHAVENDRA (Indepedent Director)

Definition

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 3/38

SEBI (Mutual Fund) Regulations 1993 defines Mutual Fund as “a fund established

in the form of a trust by a sponsor to raise money by the trustees through the sale

of units to the public under one or more schemes for investing securities in

accordance with these regulations” The rationale behind a mutual fund is that there

a large number of investors who lack the time and or the skills to manage their

money.

Hence, professional fund managers, acting on behalf of the Mutual Fund, manage

the investments (investor’s money) for their benefit in return for a management

fee. The organization that manages the investment is called the Asset Management

Company (AMC). Thus, a Mutual Fund is the most suitable investment for thecommon person as it offers an opportunity to invest in a diversified, professionally

managed basket of securities at a relatively low cost. Anybody with an investible

surplus of as little as a few thousand rupees can invest in mutual fund .Each mutual

fund scheme has defined investment objective and strategy.

A Draft offer documents is to be prepared for launching a fund. Typically, itspecifies the investment objectives of the fund, the risk associated, the cost

involved in the process and the broad rules for entry into and exit from funds and

others areas of operation. As you probably know, mutual funds have become

extremely popular over the last couple of decades what was once just another

obscure instrument is now part of daily lives. More than 80 million people or one

half of the household in America invest in mutual funds. That means that, in the

United States alone, trillions of dollars alone are invested in mutual fund. In fact,

too many people, investing means buying mutual funds After all, its common

knowledge that investing in mutual fund is (or at least should be) better than

simply letting cash waste away in a saving account but for most people, that’swhere the understanding of fund ends.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 4/38

Mutual fund is a mechanism for pooling the resources by issuing unit to the

investors and investing funds in securities in accordance with the objective as

disclosed in offer document. Investment in securities is spread across a wide

section of industry and sector and the risk is reduced. Diversification reduces the

risk because all stock may or may not move in the same direction in the same

proportion to their proportion at the same time. Mutual fund issues units to the

investors in accordance with quantum of money invested by them. Investor of

mutual are called unit holders.The profit or losses are shared by the investors in

proportion to their investment. The mutual fund usually comes out with a number

of schemes with different investment objectives which are launched from time to

time. A mutual fund is required to be registered with the SEBI, which regulates

securities markets before it can collect fund from the public.

A mutual fund is nothing more than a collective stock and /or bonds. You can think

of a mutual fund as a company that brings together a group of people and invests

their money in stock, bonds and other securities Each investors owns shares which

represent a portion of holding of the fund.

In India, SEBI (Mutual Fund) Regulations, 1996 regulates the structure of mutualfunds. Mutual funds in India are constituted in the form of a Public Trust created

under The Indian Trusts Act, 1882.

History of mutual funds

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 5/38

The origin of mutual fund industry in India is with the introduction of the concept

of mutual fund by UTI in the year 1963. Though the growth was slow, but it

accelerated from the year 1987 when non-UTI players entered the industry. In the past decade, Indian mutual fund industry had seen dramatic improvements, both

quality wise as well as quantity wise. The mutual fund industry in India started in

1963 with the formation of unit Trust of India, at the initiative of the government if

India and reserve bank.

1. First phase (1964-1987)

• The Unit Trust if India (UTI) was established in the year 1963 by passing anact in the parliament.

• In 1978 UTI was de-linked from the RBI and the Industrial Development

Bank of India (IDBI) took over the regulatory and administrative control in

place of RBI.

• The first scheme launched by UTI was Unit Scheme 1964, which is

popularly known as US-64.

• At the end of 1988 UTI had Rs.6, 700 crores of assets under management.

2. Second phase (1987-1993)

• In the year 1987, public sector mutual funds setup by public sector banks,

life insurance Corporation of India and general insurance of India are came

in to existence.

• The end of 1993 marked Rs.47, 004 as assets under management

• The following are the non-UTI mutual funds at initial stages.

1. SBI mutual fund in June 1987.

2. Can bank mutual fund in December 1987.

3. LIC mutual fund in June 1989.

4. GIC mutual fund in June 19905. Punjab National Bank mutual fund in august 1989.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 6/38

3. Third phase (1993-2003)

• Entry of private sector funds- a wide choice to Indian investors in mutual

fund.

• 1993 was the year in which the first Mutual Fund Regulations came into

being, under which all mutual funds, except UTI were to be registered and

governed

• The 1993 SEBI (Mutual Fund) Regulations were substituted by a more

comprehensive and revised Mutual Fund Regulations in 1996. The industry

now functions under the SEBI (Mutual Fund) Regulations 1996.

• As at the end of January 2003, there were 33 mutual funds with total assets

of Rs. 1,21,805 crores.

4. Fourth phase (since 2003 February)

Following the repeal of the UTI act in February 2003, it was UTI bifurcated into 2

separate entities.

• One is the specified undertaking of the UTI with asset under management of

Rs.29835/- crass at the end of January 2003

• The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and

LIC. It is registered with SEBI and functions under the Mutual Fund

Regulations.

• At the end March 2000 UTI had more than Rs.76,000 crores of AUM.

As at the end of September, 2004, there were 29 funds, which manage assets of

Rs.153108 crores under 421 schemes

SWOT ANALYSIS

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 7/38

A type of fundamental analysis of the health of a company by examining its

strengths(S), weakness (W), business opportunity (O), and any threat (T) or

dangers it might be exposed to.

1. I. STRENGTHS

• Brand strategy: LIC mutual fund is GOVT. company.

• Low price: LIC mutual fund there products is low price for other

company.

• Distribution channel strategy: LIC is continuously improving the

distribution of its products. Its online and Internet-based access offers a

combination of excellent growth prospects.

• Various sources of income: LIC has many sources of income throughout

the group, and this diversity within the group makes the company more

flexible and resistant to economic and environmental changes.

• Large pool of installed capacities.

• Experienced managers for large number of Generics.

• Large pool of skilled and knowledgeable manpower.

1.

2. II. WEAKNESS

• Mutual funds are like many other investments without a guaranteed return:

there is always the possibility that the value of your mutual fund will

depreciate. Unlike fixed-income products, such as bonds and Treasury bills,

• mutual funds experience price fluctuations along with the stocks that make

up the fund. When deciding on a particular fund to buy, you need to research

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 8/38

the risks involved – just because a professional manager is looking after the

fund, that doesn’t mean the performance will be stellar.

• Fees: In mutual funds, the fees are classified into two categories:

shareholder fees and annual operating fees. The shareholder fees, in the

forms of loads and redemption fees are paid directly by shareholders

purchasing or selling the funds. The annual fund operating fees are charged

as an annual percentage – usually ranging from 1-3%. These fees are

assessed to mutual fund investors regardless of the performance of the fund.

As you can imagine, in years when the fund doesn’t make money, these fees

only magnify losses.

1. III. OPPORTUNITIES

•

Potential markets: The Indian rural market has great potential. All themajor market leaders consider the segments and real markets for their

products. A senior official in a one of the leading company says foray into

rural India already started and there has been realization that the rural market

is both price and quantity conscious.

1. IV. THREATS

• Increased Competition: With intense competition by so many local players

causing headache to the current marketers. In addition to this though

multinational brands are not yet established but still they will soon hit themark. Almost 60 to 70% of the revenue is spending on the management and

services.

• Hedge funds : sometimes referred to as ‘hot money’, are also causing a

threat for mutual funds have gained worldwide notoriety for bringing

the markets down. Be it a crash in the currency, stock or bond

market, usually a hedge fund prominently figures somewhere in the picture.

TYPE OF MUTUAL FUND SCHEMES

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 9/38

Wide variety of mutual fund schemes exists to cater to the needs such as financial

position, risk tolerance and return expectations etc. the table below gives an

overview into the existing types of schemes in the industry.

By structure

• Open-Ended schemes

• Close-Ended schemes

• Interval schemes

By investment objectives

• Growth/Equity schemes

• General purpose

• Money market

• Guilt funds

• Balanced schemes

Other schemes

• Tax saving schemes

• Sector specific schemes

• Index schemes

Open-ended schemes

A type of mutual fund where there are no restrictions on the amount of shares the

fund will issue. If demand is high enough the fund will continue to issue shares no

matter how many investors there are. Open-end funds also buy back shares when

investors wish to sell. Most of the funds available in the marketplace are open-end

funds. Open-end funds are generally managed actively and are priced according to

their net assets value (NAV). Open-end funds are wide ranging. Some open-end

funds are more conservative and provide consistent returns with low risk, and some

are more aggressive in seeking to make capital gains through constant trading.

Close-ended schemes

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 10/38

Under this scheme the corpus of the fund and its duration are prefixed. In other

words the corpus of the fund and the number of units are determined in advance.

Once the subscription reaches the pre-determined level, the entry of investors is

closed. After the expiry of the fixed period, the entire corpus is disinvested and the

proceeds are distributed to the various unit holders in proportion to their holdings.

Thus, the fund ceases to be a fund, after the final distribution. Close end schemes

are usually more illiquid as compared to open-end schemes and hence trade at a

discount to the NAV. This discount towards the NAV closer to the maturity date of

the scheme.

Interval schemes

These schemes combine the features of open ended schemes. They may be tradedon the stock exchange or may be open for sale or redemption during predetermined

intervals at NAV based prices.

Growth/Equity schemes

These schemes also commonly called growth schemes, seek to invest a majority of

their funds in equities and a small portion in money market instruments. Such

schemes have the potential to deliver superior returns over the long term. However, because they invest in equities, these schemes are exposed to fluctuations in value

especially in the short term.

Equity schemes are hence not suitable for investors seeking regular income or

needing to use their investments in the short term. They are ideal for investors who

have a long term investment horizon. The NAV prices of equity fund fluctuates

with market value of the underlying stock which are influenced by external factors

such as social, political as well as economic.

General Purpose Equity Schemes

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 11/38

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 12/38

These primarily invest in government debts. Hence, the investor usually does not

have to worry about credit risk since government debt is generally credit risk free.

Reliance Gilt Securities Fund – Short Term Gilt Plan & Long Term Gilt Plan are

best example of such scheme.

Balanced Schemes

These schemes invest in both equities as well as debt. By investing in a mix of this

nature, balanced schemes seek to attain the objective of income and moderate

capital appreciation. Such schemes are ideal for investors with a conservative long

term orientation. Reliance balanced fund is an example of such schemes.

Tax Saving Schemes

Investors (Individuals and Hindu undivided families (HUFs)) are being encouraged

to invest in equity markets through equity linked savings scheme (ELSS) by

offering them a tax rebate. Units purchased cannot be assigned/ transferred/

pledged/ redeemed/ switched-out until completion of 3years from the date of

allotment of the respective units. The scheme is subject to securities and exchange

board of India (Mutual Funds) regulations 1996 and the notifications issued by the

Ministry of Finance (Department of economic Affairs), government of India

regarding ELSS. Subject to such conditions and limitations, as prescribed under

section 88 of the income tax act, 1961, subscriptions to the units not exceeding

Rs.10000 would be eligible to a deduction, from income tax an amount equal to

20% of the amount subscribed. Reliance Tax Saver (ELSS) Fund is an example of such fund.

Sector specific equity schemes:

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 13/38

These schemes restrict their investing to one or more pre defined sectors e.g.

technology sector. They depend upon the performance of these select sectors only

and are hence inherently more risky than general purpose equity schemes. These

schemes are ideally suited for informed investors who wish to take a view and risk

on the concerned sector. Reliance Banking Fund, Reliance Diversified Power

Sector Fund, Reliance Pharma Fund, Reliance Media & Entertainment Fund are

perfect examples of sector specific funds.

Index schemes:

An index is used as a measure of performance of the market as a whole, or a

specific sector of the market. It also serves as a relevant benchmark to evaluate the

performance of mutual funds. Some investors are interested in investing in themarket in general rather than investing in any specific fund. Such investors are

happy to receive the returns posted by the markets. As it not practical to invest in

each and every stock in the market in proportion to its size, these investor s are

comfortable investing in a fund that they believe is a good representative of the

entire market. Index funds are launched and managed for such investors. An

example to such a fund is the Reliance index fund.

Advantages of investing in a Mutual Fund are:

• Diversification: The best mutual funds design their portfolios so individual

investments will react differently to the same economic conditions. For

example, economic conditions like a rise in interest rates may cause certain

securities in a diversified portfolio to decrease in value. Other securities in

the portfolio will respond to the same economic conditions by increasing in

value. When a portfolio is balanced in this way, the value of the overall

portfolio should gradually increase over time, even if some securities lose

value.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 14/38

• Professional Management: Most mutual funds pay topflight professionals

to manage their investments. These managers decide what securities the fund

will buy and sell.

• Regulatory oversight: Mutual funds are subject to many government

regulations that protect investors from fraud.

• Liquidity: It’s easy to get your money out of a mutual fund. Write a check,

make a call, and you’ve got the cash.

• Convenience: You can usually buy mutual fund shares by mail, phone, or

over the Internet.

• Low cost: Mutual fund expenses are often no more than 1.5 percent of your

investment. Expenses for Index Funds are less than that, because index

funds are not actively managed. Instead, they automatically buy stock in

companies that are listed on a specific index

• Flexibility: currently most funds have regular investment plans, regular

withdrawal plans and dividend reinvestment scheme. A great deal of

flexibility is assured in the process.

• Choice of schemes: mutual funds offer a variety of schemes to suit varying

needs of investors.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 15/38

• Tax benefits: Tax Benefit under 80C

• Well regulated: The funds are registered with the Securities and Exchange

Board of India and their operations are continuously monitored.

Mutual funds have their drawbacks and may not be for everyone:

• No Guarantees: No investment is risk free. If the entire stock market

declines in value, the value of mutual fund shares will go down as well, no

matter how balanced the portfolio. Investors encounter fewer risks when

they invest in mutual funds than when they buy and sell stocks on their own.

However, anyone who invests through a mutual fund runs the risk of losing

money.

• Fees and commissions: All funds charge administrative fees to cover their

day-to-day expenses. Some funds also charge sales commissions or “loads”

to compensate brokers, financial consultants, or financial planners. Even if

you don’t use a broker or other financial adviser, you will pay a sales

commission if you buy shares in a Load Fund.

• Taxes: During a typical year, most actively managed mutual funds sell

anywhere from 20 to 70 percent of the securities in their portfolios. If your fund makes a profit on its sales, you will pay taxes on the income you

receive, even if you reinvest the money you made.

• Management risk: When you invest in a mutual fund, you depend on the

fund’s manager to make the right decisions regarding the fund’s portfolio. If

the manager does not perform as well as you had hoped, you might not make

as much money on your investment as you expected. Of course, if you invest

in Index Funds, you forego management risk, because these funds do not

employ managers.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 16/38

Structure of the Indian mutual fund industry

The Indian mutual fund industry is dominated by the Unit Trust of India and which

has a total corpus of Rs 700bn collected from more than 20 million investors .The

UTI has many fund /schemes in all categories i.e. equity, balanced, income etc

with some being open ended and some being closed ended. The United Scheme

1964 commonly referred to as US64, which is a balanced fund, is the biggest

scheme with a corpus of about Rs 200bn URI was floated by financial institution

and is governed by a special act of the parliament. Most of its investors believe that

the UTI is government owned and controlled, which, while legally incorrect, is true

for all practical purposes.The second largest categories of mutual funds are the

ones floated by nationalized banks. Can bank Asset management floated by Canara

Bank and SBI Funds Management floated by the State Bank of India are the largest

of these. GIC AMC floated by General Insurance Corporation and Jeevan Bima

Sahayog AMC floated by the LIC are some of the prominent ones. The aggregatecorpus of funds managed by this category of AMC’s is about Rs 150 billion The

third largest categories of the mutual funds are the once floated by the private

sector and by the foreign asset management companies. The largest of these are

Prudential ICICI AMC and Birla SUN LIFE AMC. The aggregate corpus of the

asset managed by this category of AMC s is in excess of Rs 250bn.

Recent trends in the mutual fund industry

The most important in the mutual fund industry is the aggressive expansion of the

foreign owned mutual fund companies and the decline of the companies floated by

the nationalized bank and smaller private sector players.Many nationalized banks

got into the mutual fund business in the early nineties and go off to a good start due

to the stock market boom prevailing then. These banks did not really understand

the mutual fund business and they just viewed it as another kind of bankingactivity. Few hired specialized staff and generally choose to transfer staff from the

parent organization. Some schemes had offered guaranteed returns and their patent

organization had to bail out these AMCs by paying large amount of money the

difference between the guaranteed and actual returns. The service level was also

bad. Most of these AMCs have not been able to retain staffs, float, and new

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 17/38

schemes etc.and it is doubtful whether barring a few expectations, they have

serious plans of continuing the activity in a major way.

The experience of some of the AMCs floated by private sector Indian companies

was also very similar. They quickly realized that the AMCs business is a business,

which makes money in the long term and requires deep pocketed support in the

intermediate years. Some have sold out to foreign owned companies, some have

merged with the others and there is general restructuring going on.

The foreign owned companies have deep pockets and have come in here with the

expectation of a long haul. They can be credited with introducing many new

practices such as new product innovation, sharp improvement in the service

standards and disclosure, usage of technology, broker education etc.In fact, they

have forced the industry to upgrade itself and service levels of the organization like

UTI have improved dramatically in the last few years in response to thecompetition provided by these.

Future scenario

The asset base will continue to grow at an annual rate of about 30 to 35% over the

next few years as investor’s shift their asset from banks and other traditional

avenues. Some of the older public and private sector players will either close or be

taken over.Out of ten public sectors players five will sell out, close down or mergewith strong players in three to four years. In the private sector this trend has

already started with two mergers and one takeover. Here too some of them will

down their shutter in the near future to come.But this does not mean there is no

room for other players. The market will witness a flurry of new players entering

the area. There will be a large number of offers from various asset management

companies in times to come. Some big names like Fidelity, Principal and Old

Mutual etc. are looking at Indian market seriously.

The mutual fund industry is awaiting the derivation in India as this would enable it

to hedge its risk and this in turn would be reflected in its Net Asset Value (NAV).

SEBI is working out the norms for enabling the existing mutual fund scheme to

trade in derivatives. Importantly, many market players have called on the

Regulator to initiate the process immediately, so that the mutual funds can

implement the changes that are required to trade in derivates.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 18/38

Role of SEBI in mutual fund

In the year 1992 SEBI act was passed. The objectives of SEBI are – to protect the

interest of investors in securities, to promote the development of, and to regulate

the securities market. As far as mutual are concerned, SEBI formulates policies

and regulation the mutual fund to protect the interest of the investors. SEBI

notified regulation for mutual funds in 1993. Thereafter mutual fund sponsored by

private sector entities were allowed to enter the capital market. The regulations

were fully revised in 1996 and been amended. Therefore, from time to time SEBI

has also issued guidelines to the mutual fund from time to time to protect the

interest of the investors.

All mutual funds whether promoted by public sector or private sector entities

including those promoted by foreign entities are governed by the same set of

regulation. There is no distinction in regulatory requirement of the mutual fund and

all are subject to monitoring and inspecting by SEBI. The risks associated with the

scheme launched by mutual funds sponsored by these entities are of similar type

COMPETITOR

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 19/38

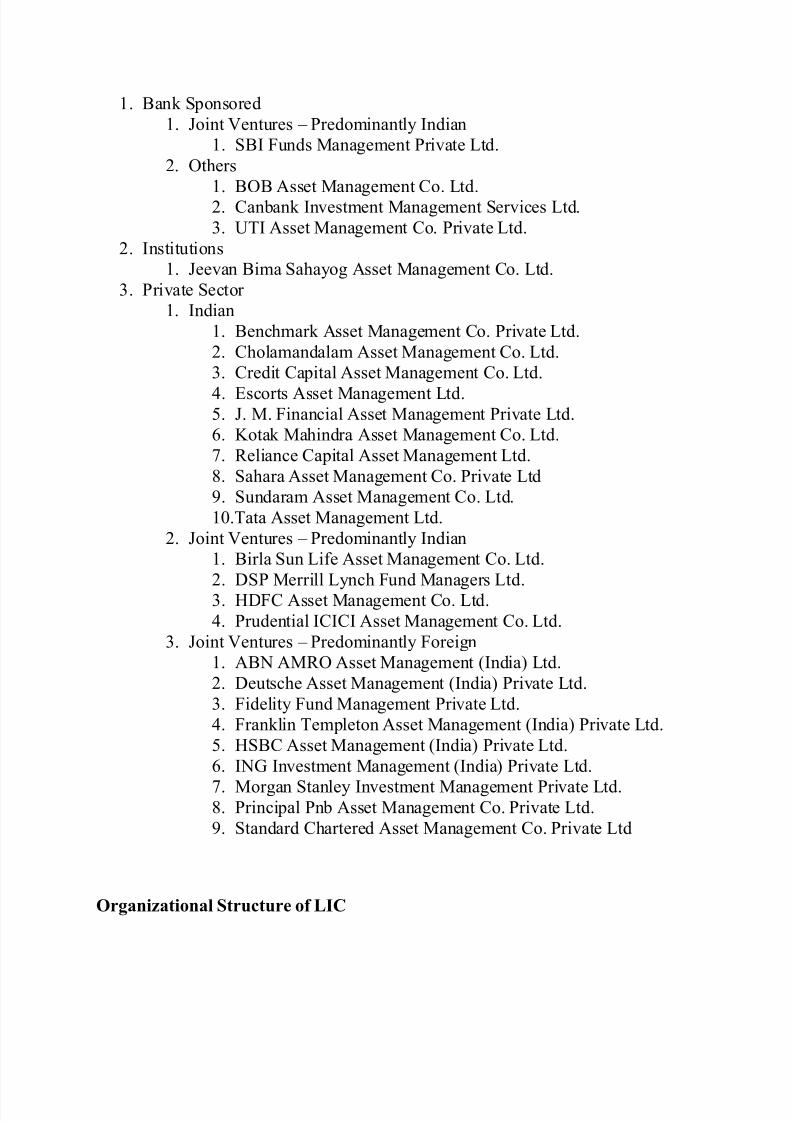

1. Bank Sponsored

1. Joint Ventures – Predominantly Indian

1. SBI Funds Management Private Ltd.

2. Others

1. BOB Asset Management Co. Ltd.

2. Canbank Investment Management Services Ltd.

3. UTI Asset Management Co. Private Ltd.

2. Institutions

1. Jeevan Bima Sahayog Asset Management Co. Ltd.

3. Private Sector

1. Indian

1. Benchmark Asset Management Co. Private Ltd.

2. Cholamandalam Asset Management Co. Ltd.

3. Credit Capital Asset Management Co. Ltd.

4. Escorts Asset Management Ltd.5. J. M. Financial Asset Management Private Ltd.

6. Kotak Mahindra Asset Management Co. Ltd.

7. Reliance Capital Asset Management Ltd.

8. Sahara Asset Management Co. Private Ltd

9. Sundaram Asset Management Co. Ltd.

10.Tata Asset Management Ltd.

2. Joint Ventures – Predominantly Indian

1. Birla Sun Life Asset Management Co. Ltd.

2. DSP Merrill Lynch Fund Managers Ltd.

3. HDFC Asset Management Co. Ltd.

4. Prudential ICICI Asset Management Co. Ltd.

3. Joint Ventures – Predominantly Foreign

1. ABN AMRO Asset Management (India) Ltd.

2. Deutsche Asset Management (India) Private Ltd.

3. Fidelity Fund Management Private Ltd.

4. Franklin Templeton Asset Management (India) Private Ltd.

5. HSBC Asset Management (India) Private Ltd.

6. ING Investment Management (India) Private Ltd.

7. Morgan Stanley Investment Management Private Ltd.8. Principal Pnb Asset Management Co. Private Ltd.

9. Standard Chartered Asset Management Co. Private Ltd

Organizational Structure of LIC

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 20/38

The organization is the form having independent or co-ordinated parts for unit

action for the accomplishment of common objectives. As such the organization

relating to insurance business is a form having different functional divisional units

with the ultimate aim of providing effective services to the customers of the

insurance products. An effective organization is essential to share information and

effectively execute the managerial decisions. The organizational structure differs

for different types of business.The organization structure is based on the objectives

or mission of the business organization. The organization should be structured with

an aim to coordinate, not only with internal managers or groups, but also with the

external world, the customers, authorities and other persons directly or indirectly

interested in it.

The insurance business is concerned with the functions of marketing of insurance

products and its related functions like premium collections and premium fixings,

accepting the insurance proposals, issuing policy documents, maintain recordsrelating t the policies issued everyday in chronological order, and also payment of

claims.

The claims department is associated with the receipt of claims and arrangement of

claims investigations. After it is decided whether to make payment to the assured

or to defer it, the insurance company may seek guidance from the panel of

advocates. The insurance company needs to protect the company from the claims

litigations of the clients by defending the claims in the courts and supervise other

alternative dispute resolutions. Thus the insurance organization is associated with

the marketing of policies, underwriting of policies, claims payment, claimsdefending and stiff matters. The delegation of duties to each unit with well-defined

limitations, responsibilities and decision making are all related to the

organizational structure and management.

Basic structure of LIC

Today, most of functions, nearly 90%, related to the marketing and other related

activities of the insurance consumers are dealt and handled at the branch level. The

branch office, depending upon its business, is headed by a manager and each

function of insurance business like marketing, underwriting of policies, accounts,

claims payments, staff and administration matters are identified as departments of

the branch office with responsible officials such as Administration and Accounts

Officers (AAO).

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 21/38

The managerial decisions are based on the information supplied by the AAO, the

functional head at root level. All the functions of claims will be settled at the

branch level. The AAO of life insurance business will deal with maturity and death

claims. If the branch is smaller, all the types of claims will be dealt by one AAO

and if the branch is bigger with good number of claims, they will be settled by,

separate officials. At branch level, these officials have to maintain cordial relations

and establish a system of sharing information with the other departments, relating

to the policy documents, payment of premium and using the staff or the agents for

the settlement of claims disputes. The branches maintain records relating to the

claims payment and claims rejections. They wiill submit the reports to the Zonal

Officer, who in turn will forward it to the Head Office or Corporate Office.

The branches report to their respective divisional office. If any branch gets a claimand there is a problem in identifying the correct claimant among the claimants, or

otherwise, a dispute of risk crops up, which will be forwarded to the divisional

office with its comments. The divisional office after receiving the papers, verifies

them, applies legal knowledge and skills, or seeks advice from skilled persons and

tries to solve the problems. The divisional office is responsible to settle the claims

referred by the branch office and also report the same to the zonal office, which in

turn will consolidate the data and submit the same as required by the statute or

otherwise under any law to the government. The government will put the same for

the approval of the both the houses.

At the division office level, the claims department generally deals with the claims,

which are pending with the branches because of some disputes, or some claims

which are of high value. The investment portfolio and establishment and

maintenance of reserves for the purpose of claims payment or otherwise required

under the law is the important function of the central office. Thus the

organizational structure of the insurance business is most flexible and decided,

based on the above said factors.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 22/38

MUTUAL FUND

CONCEPT

A Mutual Fund is a trust that pools the savings of a number of investors who share

a common financial goal. The money thus collected is then invested in capital

market instruments such as shares, debentures and other securities. The income

earned through these investments and the capital appreciation realised are shared

by its unit holders in proportion to the number of units owned by them. Thus a

Mutual Fund is the most suitable investment for the common man as it offers anopportunity to invest in a diversified, professionally managed basket of securities

at a relatively low cost. The flow chart below describes broadly the working of a

mutual fund:

Mutual fund is a mechanism for pooling the resources by issuing units to the

investors and investing funds in securities in accordance with objectives as

disclosed in offer document.

Investments in securities are spread across a wide cross-section of industries andsectors and thus the risk is reduced. Diversification reduces the risk because all

stocks may not move in the same direction in the same proportion at the same

time. Mutual fund issues units to the investors in accordance with quantum of

money invested by them. Investors of mutual funds are known as unitholders.

The profits or losses are shared by the investors in proportion to their investments.

The mutual funds normally come out with a number of schemes with different

investment objectives which are launched from time to time. A mutual fund is

required to be registered with Securities and Exchange Board of India (SEBI)

which regulates securities markets before it can collect funds from the public.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 23/38

Mutual Fund Operation Flow Chart

OBJECTIVE:

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 24/38

“To know the various factors considered by customer while going for investment in

mutual fund”.

To study the working of mutual fund.

To study the characteristics of mutual fund which attracts the investor

What an investor should consider for safe investment and better returns.

RESEARCH METHODOLOGY

RESEARCH DESIGN: -

DESCRIPTIVE (Cross sectional) it is the deliberate manner to collect the

information and it describes the phenomena without establishing the association

between the factors. This is most commonly used when we want to know about

the preferences of the customer. The design is cross-sectional because it is suited

and the respondent is interviewed once.

METHOD OF ACCESSING THE DATA: -• PRIMARY: - Through the structured questionnaire and the personal interview

which are interviewer administrated

• SECONDARY: -it will be from the websites, books.

DATA COLLECTION FORM: -

STRUCTURED form will be used in which open ended and close ended both type

of question would be asked.

• OPEN ENDED OUESTION

• CLOSE ENDED QUESTION: - Multiple choice, scales will be used,

dichotomous question.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 25/38

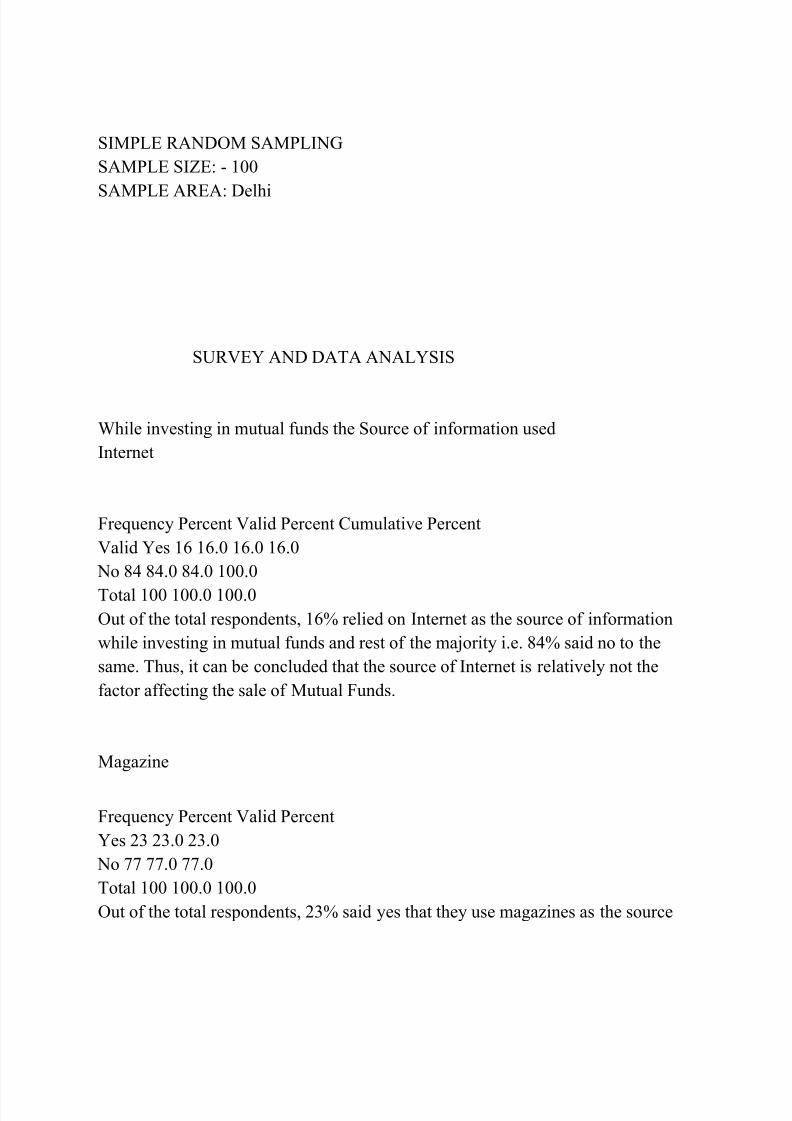

SIMPLE RANDOM SAMPLING

SAMPLE SIZE: - 100

SAMPLE AREA: Delhi

SURVEY AND DATA ANALYSIS

While investing in mutual funds the Source of information used

Internet

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 16 16.0 16.0 16.0

No 84 84.0 84.0 100.0

Total 100 100.0 100.0

Out of the total respondents, 16% relied on Internet as the source of information

while investing in mutual funds and rest of the majority i.e. 84% said no to the

same. Thus, it can be concluded that the source of Internet is relatively not the

factor affecting the sale of Mutual Funds.

Magazine

Frequency Percent Valid Percent

Yes 23 23.0 23.0

No 77 77.0 77.0

Total 100 100.0 100.0

Out of the total respondents, 23% said yes that they use magazines as the source

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 26/38

of information while investing in mutual funds and rest 77% said no to the same.

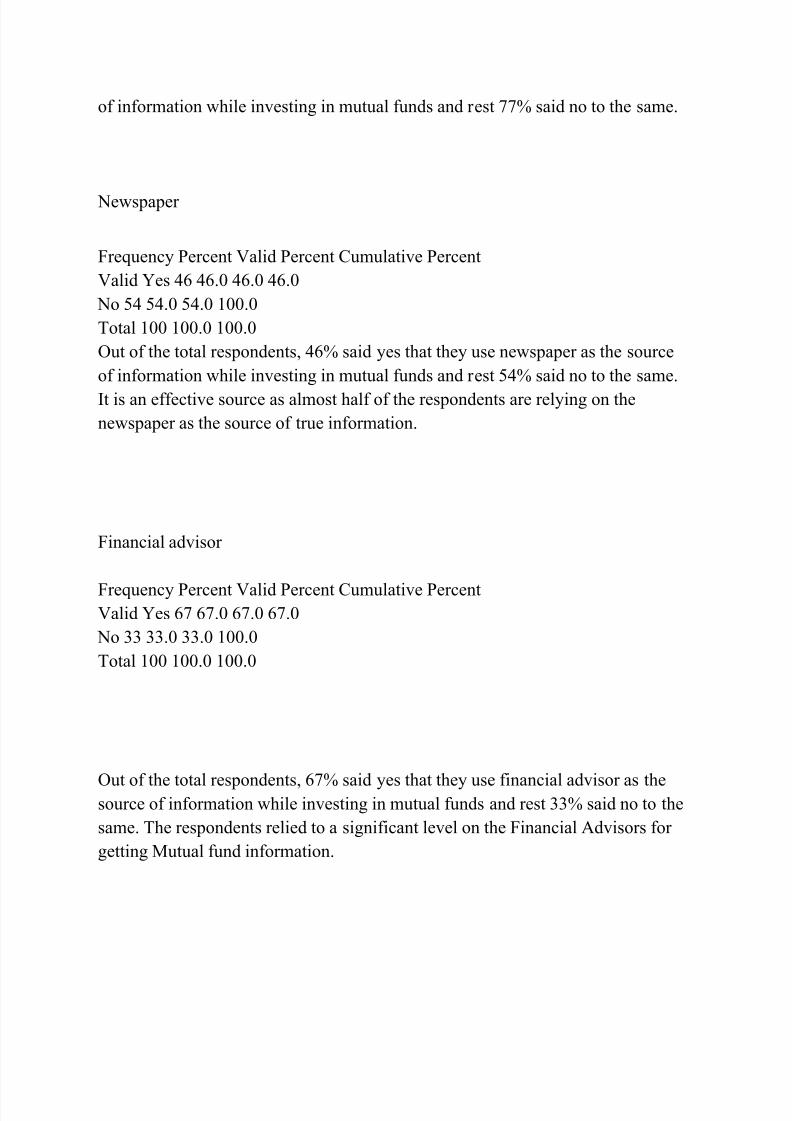

Newspaper

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 46 46.0 46.0 46.0

No 54 54.0 54.0 100.0

Total 100 100.0 100.0

Out of the total respondents, 46% said yes that they use newspaper as the source

of information while investing in mutual funds and rest 54% said no to the same.

It is an effective source as almost half of the respondents are relying on the

newspaper as the source of true information.

Financial advisor

Frequency Percent Valid Percent Cumulative PercentValid Yes 67 67.0 67.0 67.0

No 33 33.0 33.0 100.0

Total 100 100.0 100.0

Out of the total respondents, 67% said yes that they use financial advisor as thesource of information while investing in mutual funds and rest 33% said no to the

same. The respondents relied to a significant level on the Financial Advisors for

getting Mutual fund information.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 27/38

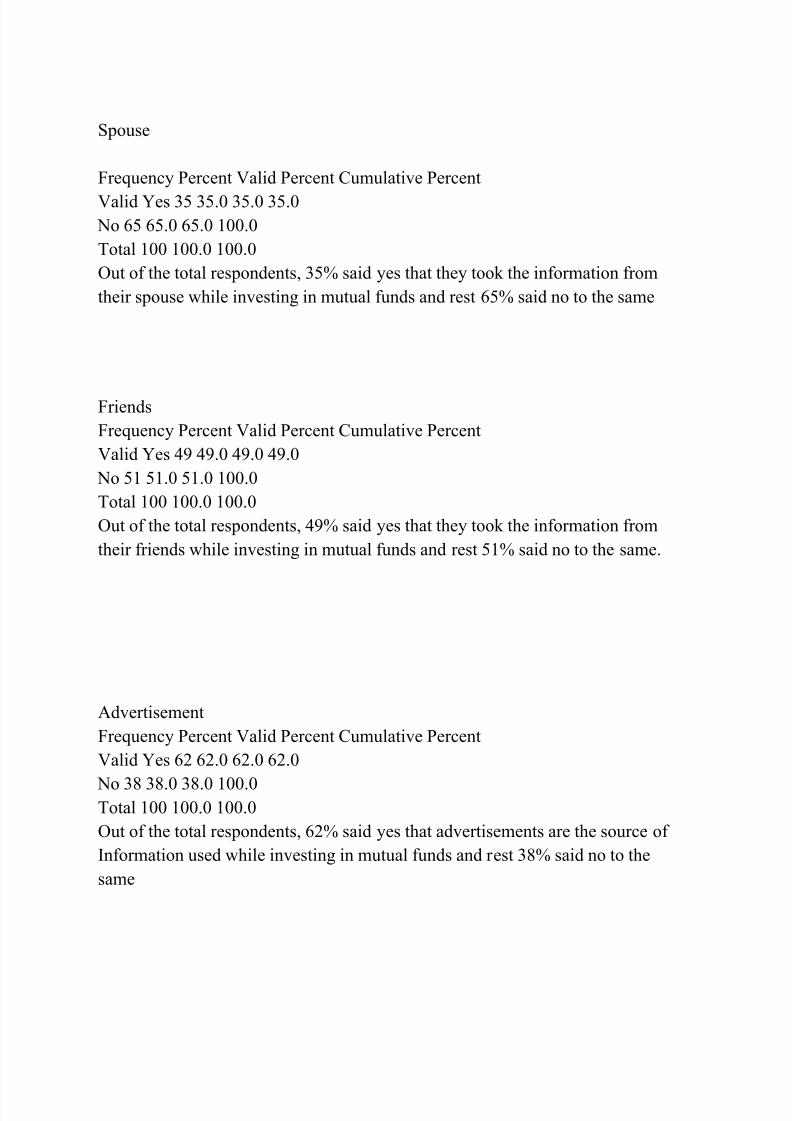

Spouse

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 35 35.0 35.0 35.0

No 65 65.0 65.0 100.0

Total 100 100.0 100.0

Out of the total respondents, 35% said yes that they took the information from

their spouse while investing in mutual funds and rest 65% said no to the same

Friends

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 49 49.0 49.0 49.0

No 51 51.0 51.0 100.0

Total 100 100.0 100.0

Out of the total respondents, 49% said yes that they took the information from

their friends while investing in mutual funds and rest 51% said no to the same.

Advertisement

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 62 62.0 62.0 62.0

No 38 38.0 38.0 100.0Total 100 100.0 100.0

Out of the total respondents, 62% said yes that advertisements are the source of

Information used while investing in mutual funds and rest 38% said no to the

same

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 28/38

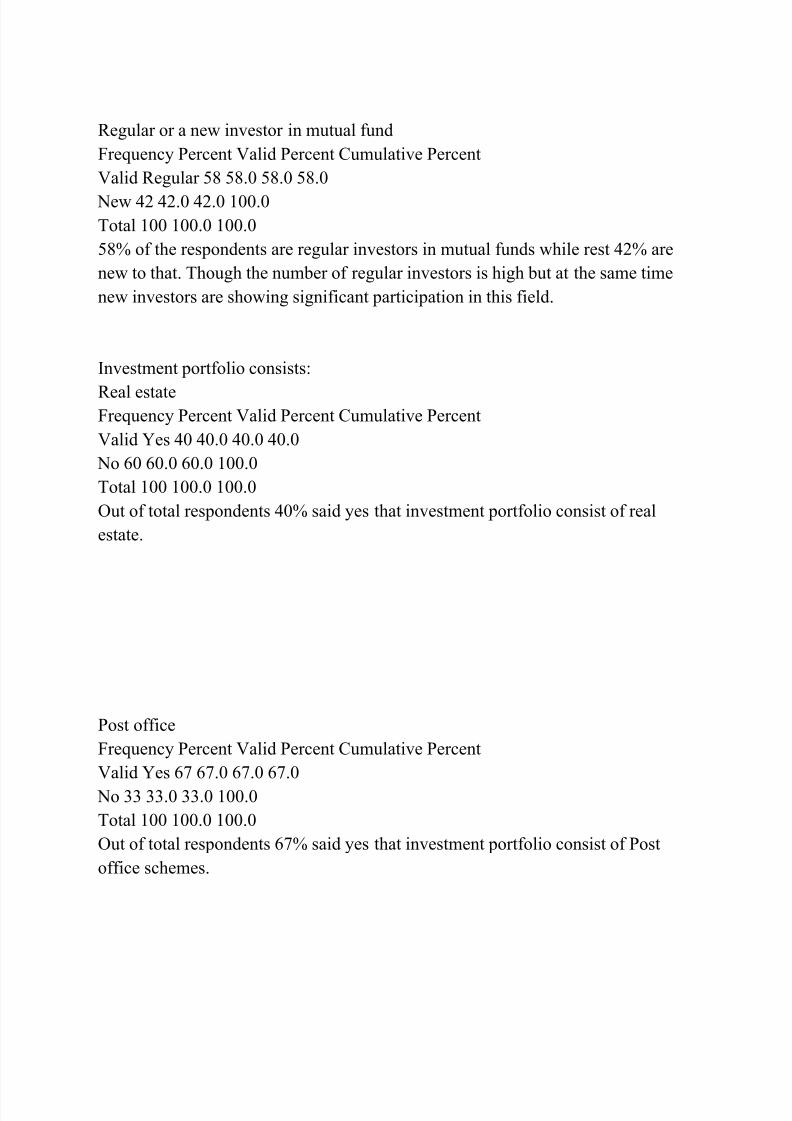

Regular or a new investor in mutual fund

Frequency Percent Valid Percent Cumulative Percent

Valid Regular 58 58.0 58.0 58.0

New 42 42.0 42.0 100.0

Total 100 100.0 100.0

58% of the respondents are regular investors in mutual funds while rest 42% are

new to that. Though the number of regular investors is high but at the same time

new investors are showing significant participation in this field.

Investment portfolio consists:

Real estateFrequency Percent Valid Percent Cumulative Percent

Valid Yes 40 40.0 40.0 40.0

No 60 60.0 60.0 100.0

Total 100 100.0 100.0

Out of total respondents 40% said yes that investment portfolio consist of real

estate.

Post office

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 67 67.0 67.0 67.0

No 33 33.0 33.0 100.0

Total 100 100.0 100.0

Out of total respondents 67% said yes that investment portfolio consist of Post

office schemes.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 29/38

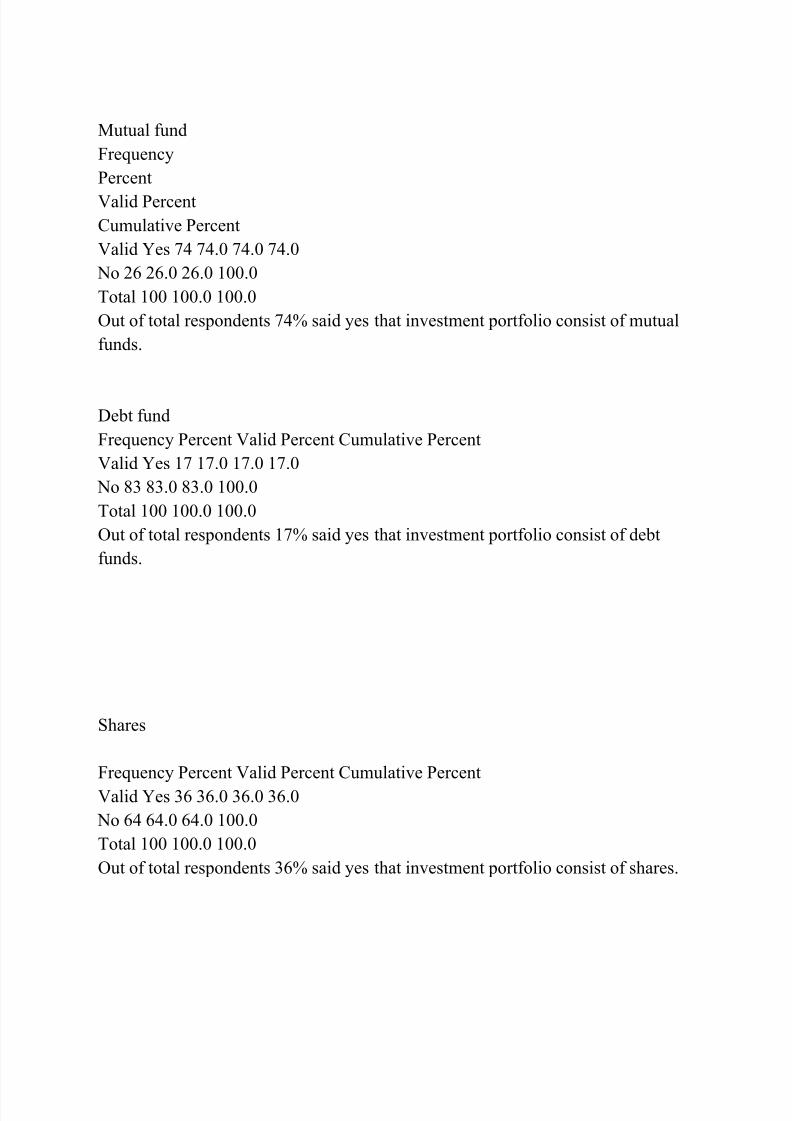

Mutual fund

Frequency

Percent

Valid Percent

Cumulative Percent

Valid Yes 74 74.0 74.0 74.0

No 26 26.0 26.0 100.0

Total 100 100.0 100.0

Out of total respondents 74% said yes that investment portfolio consist of mutual

funds.

Debt fund

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 17 17.0 17.0 17.0

No 83 83.0 83.0 100.0

Total 100 100.0 100.0

Out of total respondents 17% said yes that investment portfolio consist of debt

funds.

Shares

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 36 36.0 36.0 36.0

No 64 64.0 64.0 100.0

Total 100 100.0 100.0

Out of total respondents 36% said yes that investment portfolio consist of shares.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 30/38

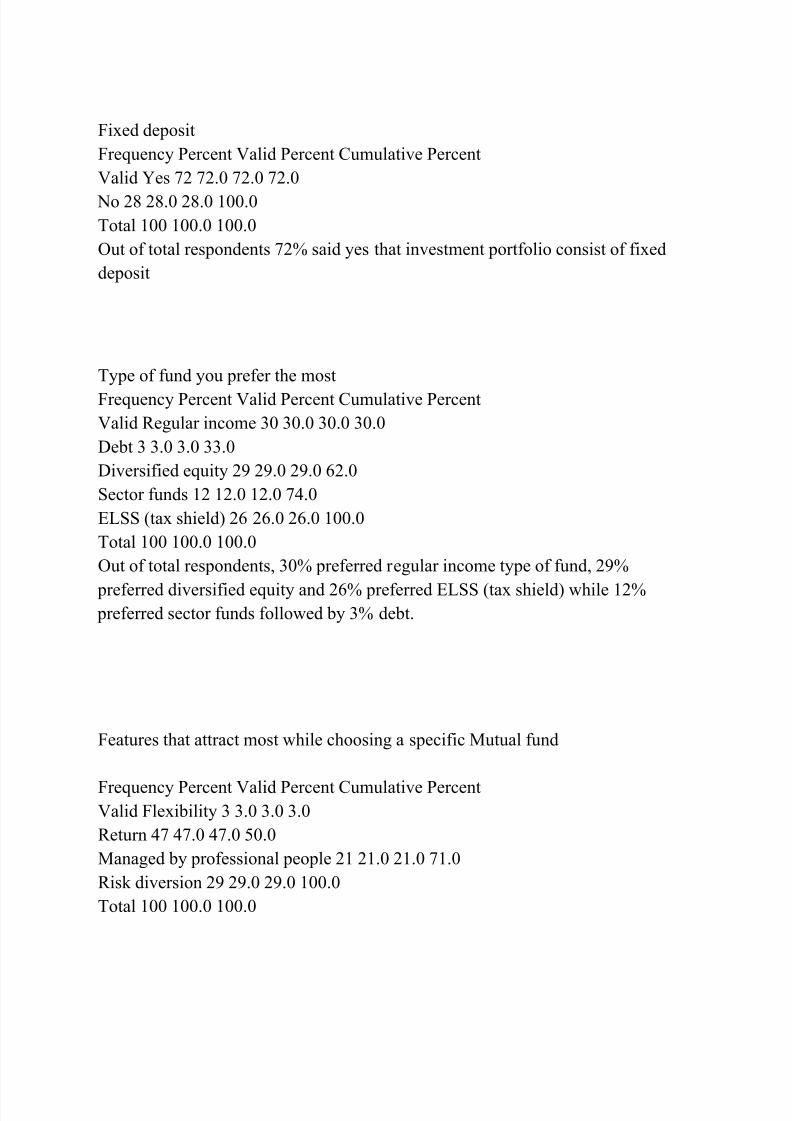

Fixed deposit

Frequency Percent Valid Percent Cumulative Percent

Valid Yes 72 72.0 72.0 72.0

No 28 28.0 28.0 100.0

Total 100 100.0 100.0

Out of total respondents 72% said yes that investment portfolio consist of fixed

deposit

Type of fund you prefer the most

Frequency Percent Valid Percent Cumulative Percent

Valid Regular income 30 30.0 30.0 30.0

Debt 3 3.0 3.0 33.0

Diversified equity 29 29.0 29.0 62.0

Sector funds 12 12.0 12.0 74.0

ELSS (tax shield) 26 26.0 26.0 100.0

Total 100 100.0 100.0

Out of total respondents, 30% preferred regular income type of fund, 29%

preferred diversified equity and 26% preferred ELSS (tax shield) while 12% preferred sector funds followed by 3% debt.

Features that attract most while choosing a specific Mutual fund

Frequency Percent Valid Percent Cumulative PercentValid Flexibility 3 3.0 3.0 3.0

Return 47 47.0 47.0 50.0

Managed by professional people 21 21.0 21.0 71.0

Risk diversion 29 29.0 29.0 100.0

Total 100 100.0 100.0

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 31/38

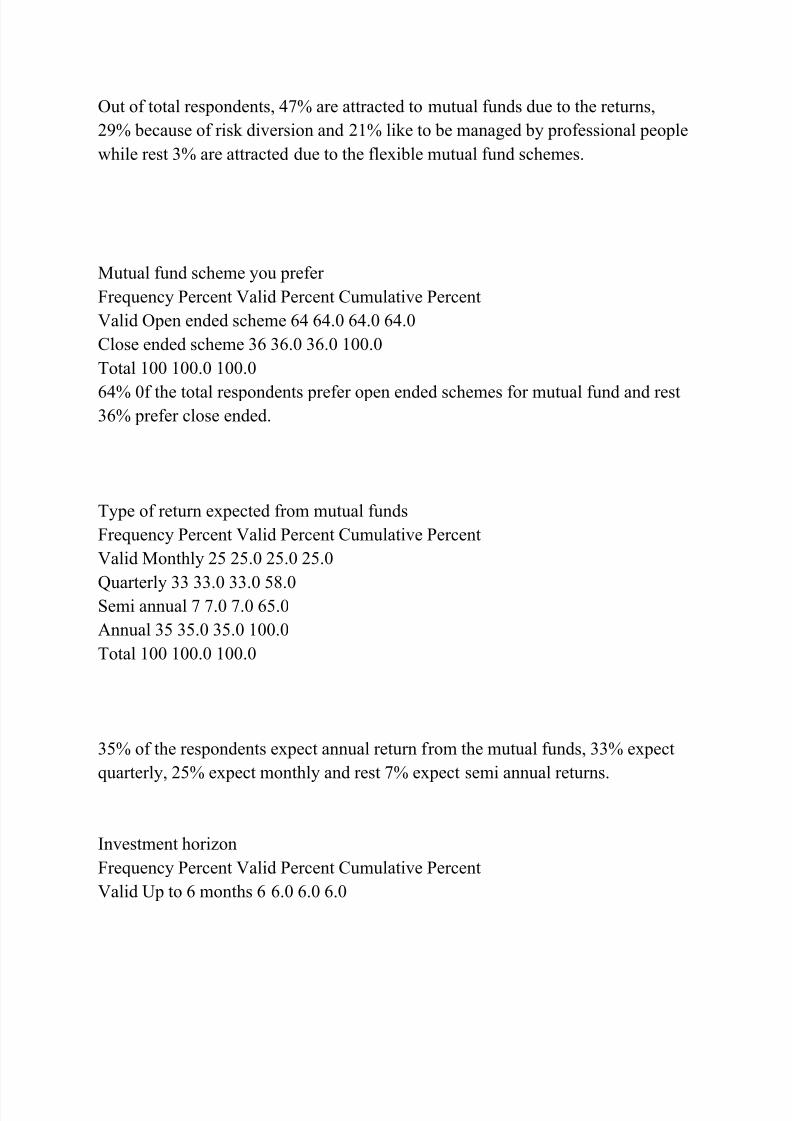

Out of total respondents, 47% are attracted to mutual funds due to the returns,

29% because of risk diversion and 21% like to be managed by professional people

while rest 3% are attracted due to the flexible mutual fund schemes.

Mutual fund scheme you prefer

Frequency Percent Valid Percent Cumulative Percent

Valid Open ended scheme 64 64.0 64.0 64.0

Close ended scheme 36 36.0 36.0 100.0

Total 100 100.0 100.0

64% 0f the total respondents prefer open ended schemes for mutual fund and rest36% prefer close ended.

Type of return expected from mutual funds

Frequency Percent Valid Percent Cumulative Percent

Valid Monthly 25 25.0 25.0 25.0

Quarterly 33 33.0 33.0 58.0Semi annual 7 7.0 7.0 65.0

Annual 35 35.0 35.0 100.0

Total 100 100.0 100.0

35% of the respondents expect annual return from the mutual funds, 33% expect

quarterly, 25% expect monthly and rest 7% expect semi annual returns.

Investment horizon

Frequency Percent Valid Percent Cumulative Percent

Valid Up to 6 months 6 6.0 6.0 6.0

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 32/38

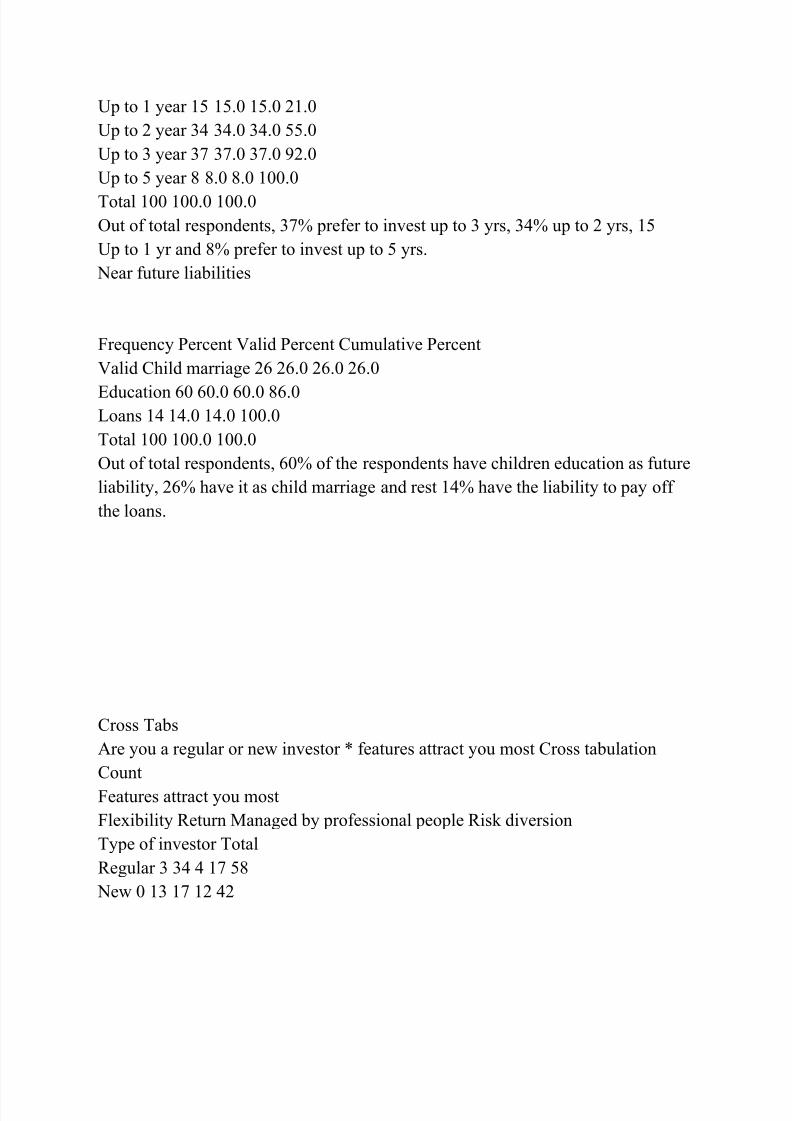

Up to 1 year 15 15.0 15.0 21.0

Up to 2 year 34 34.0 34.0 55.0

Up to 3 year 37 37.0 37.0 92.0

Up to 5 year 8 8.0 8.0 100.0

Total 100 100.0 100.0

Out of total respondents, 37% prefer to invest up to 3 yrs, 34% up to 2 yrs, 15

Up to 1 yr and 8% prefer to invest up to 5 yrs.

Near future liabilities

Frequency Percent Valid Percent Cumulative Percent

Valid Child marriage 26 26.0 26.0 26.0

Education 60 60.0 60.0 86.0Loans 14 14.0 14.0 100.0

Total 100 100.0 100.0

Out of total respondents, 60% of the respondents have children education as future

liability, 26% have it as child marriage and rest 14% have the liability to pay off

the loans.

Cross Tabs

Are you a regular or new investor * features attract you most Cross tabulation

Count

Features attract you most

Flexibility Return Managed by professional people Risk diversion

Type of investor Total

Regular 3 34 4 17 58

New 0 13 17 12 42

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 33/38

Total 3 47 21 29 100

This table tells us that maximum number of investors i.e. 47 invest because of

return they get from the mutual fund schemes. It also tells us that the regular

investors i.e. 34 invest on the basis of returns they get and the new ones i.e. 13 are

investing because of the people those who are managing the fund schemes.

FINDINGS

1. The investors give more preference to regular income funds besides the

considerations of 1) Diversified Equity 2) Tax Saving Schemes. Thus if the

government encourages the investment in mutual funds in the current budget, thenmore people will be investing in the MFs for tax saving. However people are also

not compliant to risk aversion. They are willing to invest in risky equity funds.

2. Another significant finding of the project is that investors are lured by the

returns MFs are showing. However at the same time they also want to minimize

their risk.

3. Investors desire or opt open-ended schemes than close-ended schemes. This

means that they want flexibility in the inflow and outflow of their funds.

4. The investment horizon, which is most liked by the investors, is 2-3 yrs.

5. The source of information the investors most rely is on advertisement. However they also require the detailed information, which they take from Financial

Advisors. On other sources the investors are quite apprehensive.

6. Investor’s portfolio consists mainly of Fixed Deposits and Post Office schemes.

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 34/38

However portfolio of regular investors do contain significant proportion of Mutual

Funds.

RECOMMENDATIONS

• There is lack of awareness among people about mutual funds so there should be

more advertising and other promotional campaigns to make them aware.

• People are more interested in investing in equity funds rather than debt funds

because companies are promoting more for equity funds. Companies shouldequally promote debt funds also as the provide security to customers.

• Companies should give knowledge to its customer about its computerized

operations to save their time and to make the operations more easy.

CONCLUSION

The Mutual fund industry is growing at a tremendous pace. A large number of

plans have come up from different financial resources. With the Stock marketssoaring the investors are attracted towards these schemes.

Only a small segment of the investors still invest in Mutual funds and the main

sources of information still are the financial advisors followed by advertisements

in different media. The Indian investor generally investors over a period of 2 to

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 35/38

three years. Also there is a greater tendency to invest in fixed deposits due to the

security attached with it.

In order to excel and make mutual funds a success, companies still need to create

awareness and understand the Psyche of the Indian customer.

QUESTIONNAIRE ON MUTUAL FUNDS

NAME:…………………………………………

AGE:……………………….

MONTHLY INCOME:…………………………. OCCUPATION:

………………………

1. What is your source of information while investing in mutual funds?

a) Internet [ ]

b) Magazine [ ]

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 36/38

c) Newspaper [ ]

d) Financial Advisor [ ]

e) Spouse [ ]

f) Friends [ ]

g) Advertisements [ ]

2. Are you a regular or a new investor in mutual fund?

REGULAR [ ] NEW [ ]

3. Your investment portfolio consists in %)

a) Real Estate [ ] b) Post office schemes [ ]

c) Mutual Funds [ ]

d) Debt [ ]

e) Shares [ ]

f) Fixed Deposits [ ]

4. Which type of fund you prefer the most?

a) Regular income [ ]

b) Debt [ ]

c) Diversified Equity [ ]

d) Sector funds [ ]

e) ELSS (tax shield) [ ]

5 . Which Features attract you the most while choosing a specific Mutual Fund?

a) Flexibility [ ]

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 37/38

b) Return [ ]

c) Managed by professional people [ ]

d) Risk Diversion [ ]

e) Less Expenses [ ]

6. What type of Mutual Fund Scheme you prefer?

a) Open Ended Scheme [ ]

b) Close Ended Scheme [ ]

7. What type of return you expect?

Monthly [ ] Quarterly [ ]

Semi annual [ ] Annual [ ]

8. What is your investment horizon?

Up to 6 months [ ]

Up to 1 year [ ]

Up to 2 years [ ]

Up to 3 years [ ]

Up to 5 years [ ]Up to 10 years [ ]

9. What are your near future liabilities?

8/8/2019 Kamal Kant Project

http://slidepdf.com/reader/full/kamal-kant-project 38/38

Child marriage [ ]

Education [ ]

Any other please specify………………………….