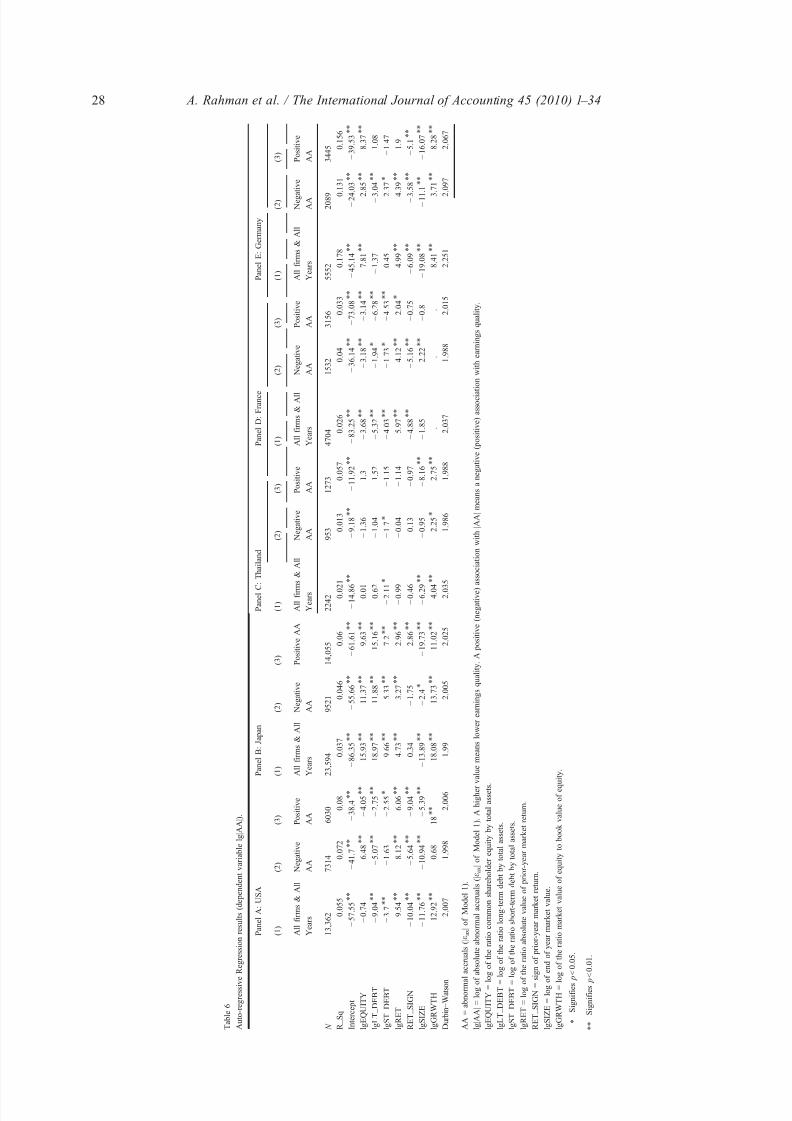

Rahman et al 2010.pdf

35

Financial reporting quality in international settings: A comparative study of the USA, Japan, Thailand, France and Germany Asheq Rahman a , ⁎ , Jira Yammeesri b , Hector Perera c a School of Accountancy, Massey University, Auckland, New Zealand b School of Accountancy, University of the Thai Chamber of Commerce, Bangkok, Thailand c Department of Accounting and Finance, Macquarie University, Sydney, Australia Abstract The purpose of this study is to show the importance of the business contexts of individual countri es to underst and corporate accounting practi ces in international settings. Using data from five countri es, we show that while age ncy theo ry constr ucts are effective in explaining acc ount ing practices in corporate set tings that have a strong agency orientat ion, such as that of the United States, it is necessary to go beyond such constructs to understand accounting practices in other corporate settings. Given the variety of international business settings, we use a generic theory, institutional theo ry. To conduc t this exa minatio n into cross-coun try acc ount ing pra ctices, we foc us on an earnings quality measure based on accrual accounting practices, the abnormal accruals component of accoun ting earnings. We provide evidence to support the view that with varying business settings we are likely to see diversity in accounting practices that result in different levels of accruals or accruals based earnings quality. © 2010 University of Illinois. All rights reserved. Keywords: Agency theory; Financial reporting quality; USA; Japan; Thailand; France; Germany 1. Introduction Agency theory is frequently used by researchers to explain accounting practices in country-specific studies. It explains accounting practices in corporate settings that have a Available online at www.sciencedirect.com The International Journal of Accounting 45 (2010) 1 – 34 ⁎ Corresponding author. Tel.: +64 9 414 0800. E-mail address: a.r.rahman@massey .ac.nz (A. Rahman). 0020-7063/$ - see front matter © 2010 University of Illinois. All rights reserved. doi:10.1016/j.intacc.2010.01.001

Transcript of Rahman et al 2010.pdf

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 1/34

Financial reporting quality in international settings: A

comparative study of the USA, Japan, Thailand,

France and Germany

Asheq Rahman a,⁎, Jira Yammeesri b, Hector Perera c

a School of Accountancy, Massey University, Auckland, New Zealand b School of Accountancy, University of the Thai Chamber of Commerce, Bangkok, Thailand

c Department of Accounting and Finance, Macquarie University, Sydney, Australia

Abstract

The purpose of this study is to show the importance of the business contexts of individual

countries to understand corporate accounting practices in international settings. Using data from five

countries, we show that while agency theory constructs are effective in explaining accounting

practices in corporate settings that have a strong agency orientation, such as that of the United States,it is necessary to go beyond such constructs to understand accounting practices in other corporate

settings. Given the variety of international business settings, we use a generic theory, institutional

theory. To conduct this examination into cross-country accounting practices, we focus on an

earnings quality measure based on accrual accounting practices, the abnormal accruals component of

accounting earnings. We provide evidence to support the view that with varying business settings we

are likely to see diversity in accounting practices that result in different levels of accruals or accruals

based earnings quality.

© 2010 University of Illinois. All rights reserved.

Keywords: Agency theory; Financial reporting quality; USA; Japan; Thailand; France; Germany

1. Introduction

Agency theory is frequently used by researchers to explain accounting practices in

country-specific studies. It explains accounting practices in corporate settings that have a

Available online at www.sciencedirect.com

The International Journal of Accounting 45 (2010) 1–34

⁎ Corresponding author. Tel.: +64 9 414 0800.

E-mail address: [email protected] (A. Rahman).

0020-7063/$ - see front matter © 2010 University of Illinois. All rights reserved.

doi:10.1016/j.intacc.2010.01.001

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 2/34

strong agency orientation as it is based on the notion of separation among ownership, debt,

and management. For example, studies focused on the United States usually support the

agency argument that certain firm and board features, and good quality accounting1 and

auditing are the bases for better firm performance. However, in international settings,similar studies have often produced contradictory results. For example, Gabrielsen,

Gramlich, and Plenborg (2002) find that managerial ownership (an agency variable) has

different effects on the information content of earnings and discretionary accruals in

Denmark from that in the United States. Further, in a review of audit independence,

discretionary accruals, and earnings-informativeness studies, Rainsbury (2007) finds that in

many non-U.S. settings agency monitoring mechanisms such as board of directors,

accounting arrangements, and audit quality do not relate to discretionary accruals and

earnings informativeness in the same manner as they do in the US setting.

Agency theory originated in the environment of growth of large modern corporations in

Anglo-American countries. It mainly focuses on exogenous factors that relate to financing.

However, the business settings internationally are diverse in characteristics. The purpose of

this study is to emphasize the need to go beyond the agency theory constructs to explain

accounting practices in international settings and to propose the use of a generic and all-

encompassing theory, institutional theory, which is applicable to all international settings,

with or without strong agency orientation. Institutional theory allows for the examination of

all exogenous and endogenous factors that affect corporate practices.

We do not see, however, agency theory and institutional theory as mutually exclusive.

Rather, we see agency theory as a theory that is applicable to an institutional setting where

the agency relationships among ownership, debt, and management are clearly explicable. Inother words, agency theory constructs are better applicable to explaining corporate actions

in settings where there is clear separation among ownership, debt, and management. On the

other hand, institutional theory is a more general theory that calls for an appreciation of any

form of institutional arrangement prevailing in business.

Institutional influences on accounting have been observed in the extant literature. For

example, Ball (1995) and Nobes (1998) contend that accounting systems and the level of

market transparency are functions of the nature of the legal systems and financing of firms

in a country. This view has been broadly assessed in terms of whether a country has a code-

law or a common-law legal origin, or whether a country has a debt-based or an equity-based

capital market (Ball, Kothari, & Robin, 2000; Ali & Hwang, 2000; Ball, Robin, & Wu,2003). However, it only provides a general understanding of how accounting is related to

law and finance and lacks appreciation of the specific nature of country settings and their

influence on accounting practices in international settings. For example, Ball et al. (2003)

find that the timeliness of accounting income in four East Asian common-law countries is

similar to the timeliness of accounting income in code-law countries, suggesting that there

are other factors affecting accounting income.

The financial and organizational settings of countries are far more complex than what the

legal and financing dichotomies reflect. For East Asian countries, Fan and Wong (2002)

find that concentrated ownership and the associated pyramidal and cross-holding structures

1 For the purposes of this study, accounting quality is defined as the extent to which accounting indicators are

reliable measures of firm performance.

2 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 3/34

create agency conflicts between controlling owners (insiders) and outside investors,

whereby, controlling owners report accounting information for self-interest purposes. Their

explanations of high concentration and tightly controlled hierarchies suggest that firms in

East Asia do not display separation of ownership and control. In addition, finance andmanagement literatures suggest that there are systematic variations between countries with

regard to organization of firms, which in turn affect managerial and market behavior

(Gilson & Roe, 1993; Shishido, 1999). These firm-level idiosyncrasies that exist across

many firms in a country often arise from country level institutional idiosyncrasies. For

example, in the case of countries with weak shareholder protection, major shareholders tend

to attempt to protect their own interests at the expense of other shareholders through

majority ownership or other control measures.

Using samples of firm-year observations from the United States, Japan, Thailand,

France, and Germany, we show that because institutional variables such as organizational

structures, ownership structures, nature of debt, and regulations vary systematically

between countries, the agency variables of equity and debt affect accounting quality in each

country differently. In this regard, we find that the agency expectations of how financing

affects accounting quality hold only in certain settings. In other settings, the effects of

financing variables depend on the nature of the institutional variables. We use a broad

accounting-practice variable, the level of abnormal accruals, to assess accounting quality in

each country. We partition debt into long-term and short-term components, as these

components are likely to have different influences on abnormal accruals.

The United States is chosen as one of the sample countries because the institutional

setting of its firms resembles the setting depicted in agency theory, which suggests a clear demarcation between the interests of equity providers, creditors and managers. Most of the

prior literature dealing with financing and accounting issues is based on the agency

framework. Japan is chosen because its business setting is dominated by a unique business

form called the keiretsu. The keiretsu is a group of firms interrelated through debt and

equity financing by a central keiretsu bank, cross-shareholdings between keiretsu member

firms and operating links between the keiretsu firms. Thailand also provides a unique

business setting with its family-owned businesses and high short-term debt dependence.

France has its own idiosyncrasies with firms having high blockholder concentration and

high debt financing complemented by regulations that require better disclosure when debt

levels are higher. Germany also has high block ownership in firms, but has less debt financing than France, and its debt financiers participate in the governance of firms and are

heavily protected by bankruptcy laws.

An important contribution of this study is that it provides insights into how organi-

zational, financial, and regulatory factors that are peculiar to a country interact and affect

accounting practices. Such insights can help policy makers and external users of financial

information understand how firms in different countries may adopt international financial

reporting standards (IFRS). Researchers can also benefit as our study cautions them of

about the use of agency theory constructs where the institutional settings of the firms and

their environments are different from the settings depicted in the agency theory literature.

The remainder of the paper is organized into five sections. The second section lays downthe theoretical basis of the study. The third section develops the hypotheses. The fourth section

specifies the research design. The fifth section provides the results. The sixth section presents a

3 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 4/34

discussion and an analysis of the results. The final section includes the conclusions, limitations

and implications of this study.

2. Theoretical basis

Agency theory was developed by Berle and Means (1932) for a corporate setting with a

clear separation between ownership and control. Its central issue is how to resolve the

conflict between owners, managers, and debt holders over the control of corporate

resources through the use of contracts (Simerly & Li, 2000). An unambiguous separation of

ownership and control of firms is not common in many countries. Agency theory doesn't

take into consideration corporate environments that have no discernible separation between

ownership and control, nor does it consider that managers might have to make choices from

a perspective other than maximizing wealth for stockholders.

According to Simerly and Li (2000), organizations match the demands of their

environment with management and organizational systems in order to survive and succeed.

They argue that management and organizational systems most appropriate for any given

firm will be a product of the specific set of environmental contingencies being faced by the

firm. Similarly, the choice of capital structure is less a matter of predefined alternatives and

more a search for alternatives in a complex and uncertain environment in which the firm

exists. The choice of managerial and organizational systems and the capital structure, in turn,

affects accounting practices of firms within a particular corporate environment. Prior studies

have shown that various forms of organizational and capital structures exist outside the

Anglo-American countries (Fan & Wong, 2002; Nagano, 2003; Booth, Aivazian,Demirguc-Kunt, & Maksimovic, 2001; Antoniou, Guney, & Paudyal, 2008). This suggests

that there is a need for a more generic theoretical model to explain accounting behavior

across countries.

Institutional theory offers a generic framework to analyze corporate practices. It

provides insights into how an organization functions in its environment, and allows for an

explanation of the relationship between organizational practices and its environment. Its

premise is that organizations adopt or adapt to institutional norms and rules to gain stability

and enhance survival prospects. Through the processes of adoption and adaptation the

institutional norms and rules impact the positions, policies, programs, and procedures of

organizations (Scott, 2004).One common question addressed in institutional theory is — what makes organizations

so similar in a country? Meyer and Rowan (1977) and DiMaggio and Powell (1983)

observe that business practices arise mainly from three types of pressures in an institutional

environment, coercive, mimetic and normative. Coercive pressure comes from govern-

mental regulations; mimetic pressure happens when organizations embrace the system of

the existing institutions in their field; and normative pressure occurs when organizational

administrators intuitively follow the conventional practices. They conclude that rational

individuals make their organizational structures, functions, and operations increasingly

homogeneous not necessarily to increase efficiency but to meet social expectations or to be

socially acceptable.Institutional theorists point out that all social systems, hence all organizations, exist in an

institutional environment that defines social reality and that, just as with technical environments,

4 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 5/34

institutional environments are enormously diverse, and variable over time (Scott, 2001).

Institutional Theory proposes that organizations are affected by “common understandings of

what is appropriate and, fundamentally, meaningful behavior ” (Zucker, 1983, p.105).

Accordingly, Institutional Theory advocates that organizational structures and processes aremoderated by the institutional environment (Lincoln, Hanada, & McBride, 1986, p.340).

Institutional theory, therefore, is capable of explaining organizational behavior in any

setting, whereas, agency theory deals with the setting of separation between ownership and

control. In other words, institutional theory can explain why businesses have similar

organizational structures and cultural elements within a particular socio-cultural setting,

even though they are separate entities, and, in turn, can explain why the features of an

organization in a particular setting are different from those of another. Agency theory is a

theory of a particular institutional setting, the setting where ownership is separate from

control, whereas institutional theory is a generic theory intended to identify and explain the

features of organizations in any setting. From these features arise the actions of

organizational actors, which include accounting, control, and other review practices of

organizations (Scott, 2004). This is consistent with Zucker (1983) who points out that the

institutional setting exogenous to the firm and the endogenous setting within the firm

coexist. Likewise, one can argue that firm-specific practices, such as accounting practices,

are continuously responding to or are influencing the institutional setting of the firm.

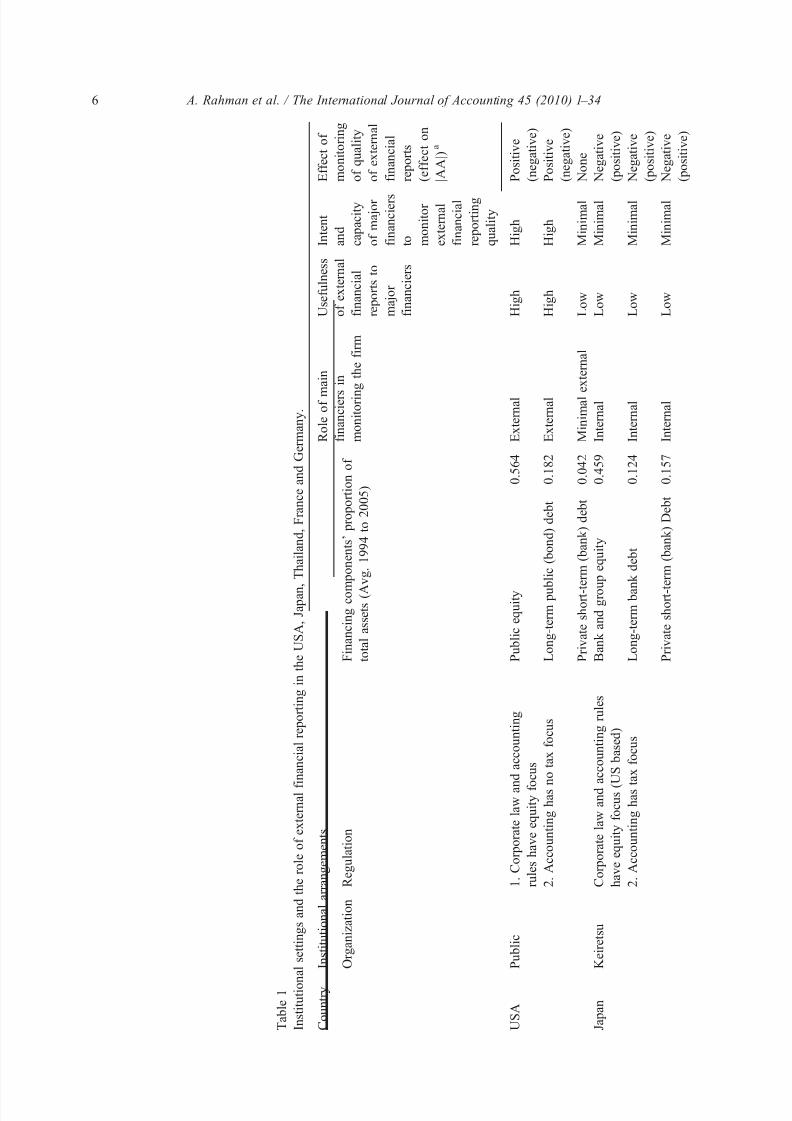

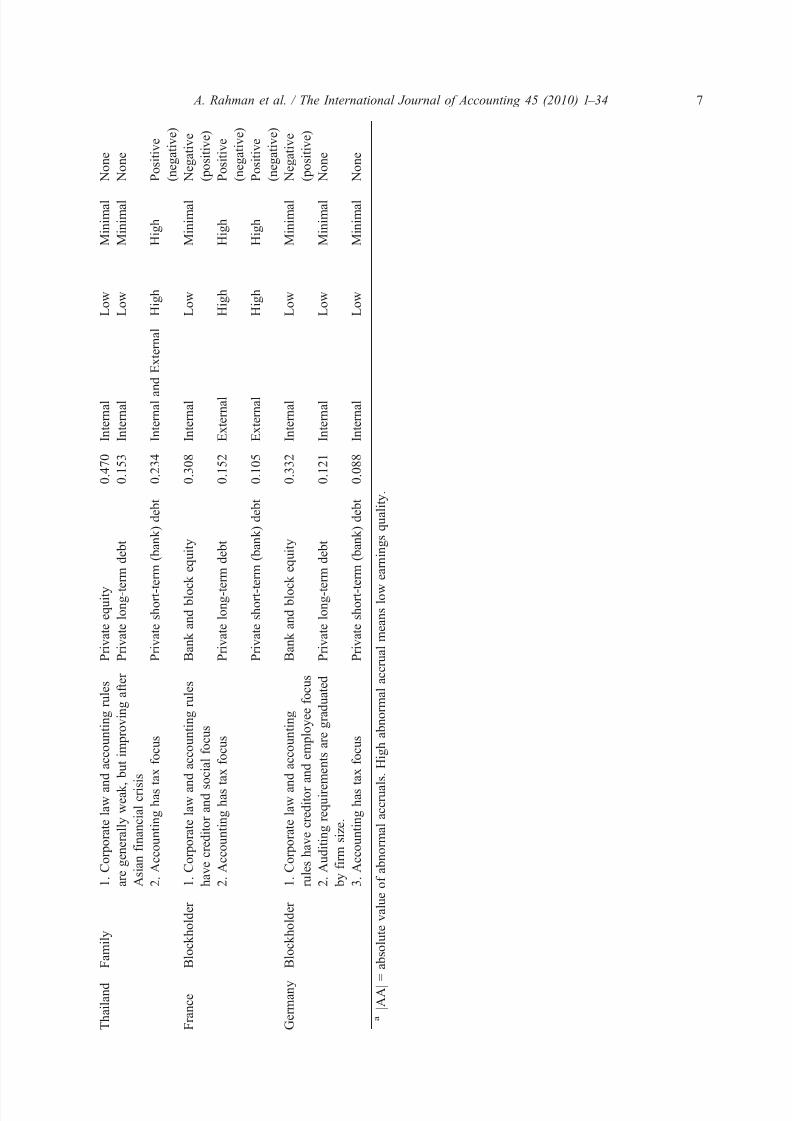

3. Hypotheses development

Prior literature in international financial accounting has linked the quality of accounting parameters to the nature of country level institutional arrangements. Ball et al. (2000), Ali

and Hwang (2000) and Ball et al. (2003) attribute the differences in institutional systems to

the legal origin of, and the nature of corporate finance in a country. Their evidence suggests

that in countries where companies depend more on debt finance than on equity finance, or

in countries which have code law (compared to common law), the quality of accounting in

companies is relatively inferior. Leuz, Nanda, and Wysocki (2003) also provide similar

conclusions in their study on earnings management across countries.

The broadly framed analyses based on country level legal or financing variables have

limited explanatory power. There exists a variation in accounting quality within the broad

groups of countries. For example, Ball et al. (2003) find that the East Asian common-lawcountries do not have levels of accounting conservatism similar to those of the other

common-law countries. Leuz et al. (2003) find that common-law countries like Singapore

and Hong Kong have high, aggregate earnings-management scores similar to those of code-

law countries such as Germany and Japan. Additionally, Graham and King (2000) find that

methods of differentiating accounting practices of countries using accounting-regulation

differences also lead to inconclusive results. On the other hand, country-specific studies,

such as Fan and Wong (2002) provide interesting country-based explanations, but they

cannot typify differences of accounting practices between countries because they do not

attempt to draw comparisons.

An examination of variations in accounting practices between countries requires scrutinyof features specific to a country rather than the broad features, and an evaluation of how the

specific features cause accounting practices to be different across countries. It is important to

5 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 6/34

T a b l e 1

I n s t i t u t i o n

a l s e t t i n g s a n d t h e r o l e o f e x t e r n a l f i n a n c i a l r e p o r t i n g i n t h e U S A , J a p a n , T h a i l a n d , F r a n c e a n d G e r m a n y .

C o u n t r y

I n s t i t u t i o n a l a r r a n g e m e n t s

R o l e o f m

a i n

f i n a n c i e r s

i n

m o n i t o r i n g t h e f i r m

U s e f u l n e s s

o f e x t e r n a l

f i n a n c i a l

r e p o r t s t o

m a j o r

f i n a n c i e r s

I n t e n t

a n d c a p a c i t y

o f m a j o r

f i n a n c i e r s

t o m o n i t o r

e x t e r n a l

f i n a n c i a l

r e p o r t i n g

q u a l i t y

E f f e c t o f

m o n i t o r i n g

o f q u a l i t y

o f e x t e r n a l

f i n a n c i a l

r e p o r t s

( e f f e c t o n

| A A | ) a

O r g a n i z a t i o n

R e g u l a t i o n

F i n a n c i n g c o m

p o n e n t s ' p r o p o r t i o n o f

t o t a l a s s e t s ( A

v g . 1 9 9 4 t o 2 0 0 5 )

U S A

P u b l i c

1 . C o r p o r a t e l a w a n

d a c c o u n t i n g

r u l e s h a v e e q u i t y f o

c u s

P u b l i c e q u i t y

0 . 5 6 4

E x t e r n a l

H i g h

H i g h

P o s i t i v e

( n e g a t i v e )

2 . A c c o u n t i n g h a s n o t a x f o c u s

L o n g - t e r m p u b l i c ( b o n d ) d e b t

0 . 1 8 2

E x t e r n a l

H i g h

H i g h

P o s i t i v e

( n e g a t i v e )

P r i v a t e s h o r t - t e r m ( b a n k ) d e b t

0 . 0 4 2

M i n i m a l e

x t e r n a l

L o w

M i n i m a l

N o n e

J a p a n

K e i r e t s u

C o r p o r a t e l a w a n d a c c o u n t i n g r u l e s

h a v e e q u i t y f o c u s ( U S b a s e d )

B a n k a n d g r o u p e q u i t y

0 . 4 5 9

I n t e r n a l

L o w

M i n i m a l

N e g a t i v e

( p o s i t i v e )

2 . A c c o u n t i n g h a s t a x f o c u s

L o n g - t e r m b a n k d e b t

0 . 1 2 4

I n t e r n a l

L o w

M i n i m a l

N e g a t i v e

( p o s i t i v e )

P r i v a t e s h o r t - t e r m ( b a n k ) D e b t 0 . 1 5 7

I n t e r n a l

L o w

M i n i m a l

N e g a t i v e

( p o s i t i v e )

6 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 7/34

T h a i l a n d

F a m i l y

1 . C o r p o r a t e l a w a n

d a c c o u n t i n g r u l e s

a r e g e n e r a l l y w e a k , b u t i m p r o v i n g a f t e r

A s i a n f i n a n c i a l c r i s i s

P r i v a t e e q u i t y

0 . 4 7 0

I n t e r n a l

L o w

M i n i m a l

N o n e

P r i v a t e l o n g - t e r m d e b t

0 . 1 5 3

I n t e r n a l

L o w

M i n i m a l

N o n e

2 . A c c o u n t i n g h a s t a x f o c u s

P r i v a t e s h o r t - t e r m ( b a n k ) d e b t

0 . 2 3 4

I n t e r n a l a n d E x t e r n a l H i g h

H i g h

P o s i t i v e

( n e g a t i v e )

F r a n c e

B l o c k h o l d e r

1 . C o r p o r a t e l a w a n

d a c c o u n t i n g r u l e s

h a v e c r e d i t o r a n d s o c i a l f o c u s

B a n k a n d b l o c k e q u i t y

0 . 3 0 8

I n t e r n a l

L o w

M i n i m a l

N e g a t i v e

( p o s i t i v e )

2 . A c c o u n t i n g h a s t a x f o c u s

P r i v a t e l o n g - t e r m d e b t

0 . 1 5 2

E x t e r n a l

H i g h

H i g h

P o s i t i v e

( n e g a t i v e )

P r i v a t e s h o r t - t e r m ( b a n k ) d e b t

0 . 1 0 5

E x t e r n a l

H i g h

H i g h

P o s i t i v e

( n e g a t i v e )

G e r m a n y

B l o c k h o l d e r

1 . C o r p o r a t e l a w a n

d a c c o u n t i n g

r u l e s h a v e c r e d i t o r a n d e m p l o y e e f o c u s

B a n k a n d b l o c k e q u i t y

0 . 3 3 2

I n t e r n a l

L o w

M i n i m a l

N e g a t i v e

( p o s i t i v e )

2 . A u d i t i n g r e q u i r e m e n t s a r e g r a d u a t e d

b y f i r m s i z e .

P r i v a t e l o n g - t e r m d e b t

0 . 1 2 1

I n t e r n a l

L o w

M i n i m a l

N o n e

3 . A c c o u n t i n g h a s t a x f o c u s

P r i v a t e s h o r t - t

e r m ( b a n k ) d e b t

0 . 0 8 8

I n t e r n a l

L o w

M i n i m a l

N o n e

a

| A A | = a b s o l u t e v a l u e o f a b n o r m a l a c c r u a l s . H i g h a b n o r m a l a c c r u a l m e a n s l o w

e a r n i n g s q u a l i t y .

7 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 8/34

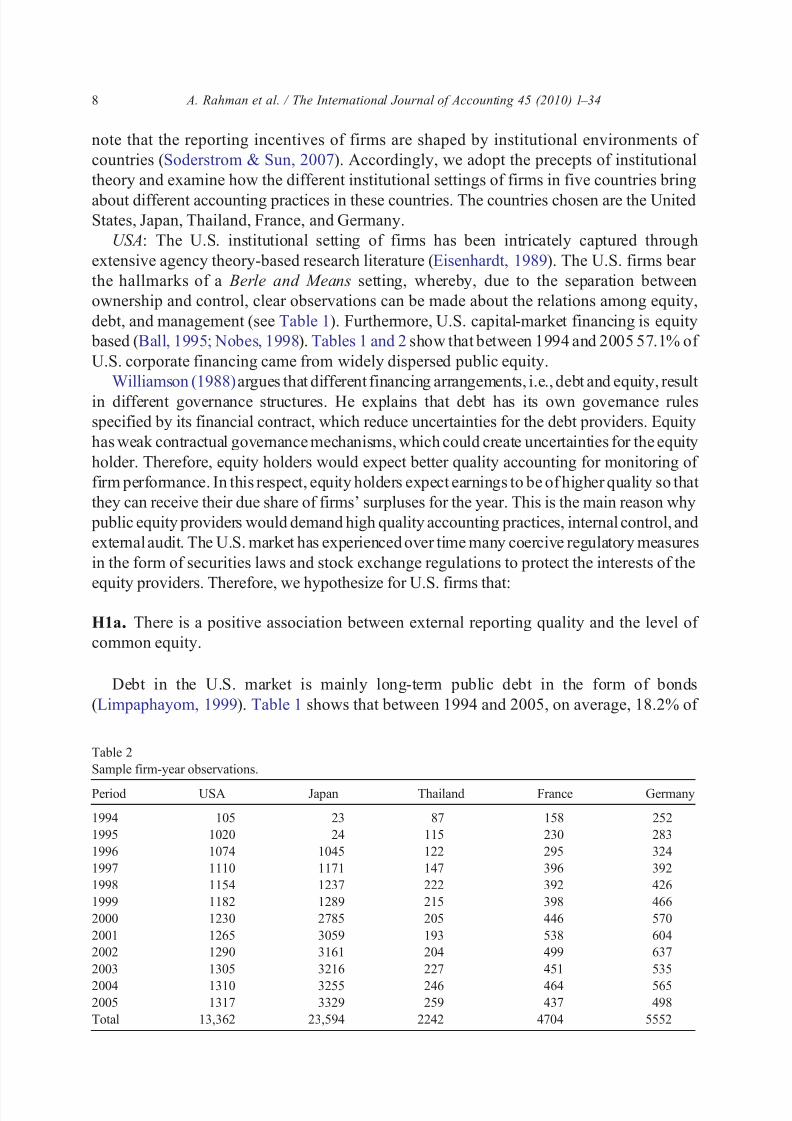

note that the reporting incentives of firms are shaped by institutional environments of

countries (Soderstrom & Sun, 2007). Accordingly, we adopt the precepts of institutional

theory and examine how the different institutional settings of firms in five countries bring

about different accounting practices in these countries. The countries chosen are the UnitedStates, Japan, Thailand, France, and Germany.

USA: The U.S. institutional setting of firms has been intricately captured through

extensive agency theory-based research literature (Eisenhardt, 1989). The U.S. firms bear

the hallmarks of a Berle and Means setting, whereby, due to the separation between

ownership and control, clear observations can be made about the relations among equity,

debt, and management (see Table 1). Furthermore, U.S. capital-market financing is equity

based (Ball, 1995; Nobes, 1998). Tables 1 and 2 show that between 1994 and 2005 57.1% of

U.S. corporate financing came from widely dispersed public equity.

Williamson (1988) argues that different financing arrangements, i.e., debt and equity, result

in different governance structures. He explains that debt has its own governance rules

specified by its financial contract, which reduce uncertainties for the debt providers. Equity

has weak contractual governance mechanisms, which could create uncertainties for the equity

holder. Therefore, equity holders would expect better quality accounting for monitoring of

firm performance. In this respect, equity holders expect earnings to be of higher quality so that

they can receive their due share of firms' surpluses for the year. This is the main reason why

public equity providers would demand high quality accounting practices, internal control, and

external audit. The U.S. market has experienced over time many coercive regulatory measures

in the form of securities laws and stock exchange regulations to protect the interests of the

equity providers. Therefore, we hypothesize for U.S. firms that:

H1a. There is a positive association between external reporting quality and the level of

common equity.

Debt in the U.S. market is mainly long-term public debt in the form of bonds

(Limpaphayom, 1999). Table 1 shows that between 1994 and 2005, on average, 18.2% of

Table 2

Sample firm-year observations.

Period USA Japan Thailand France Germany

1994 105 23 87 158 252

1995 1020 24 115 230 283

1996 1074 1045 122 295 324

1997 1110 1171 147 396 392

1998 1154 1237 222 392 426

1999 1182 1289 215 398 466

2000 1230 2785 205 446 570

2001 1265 3059 193 538 604

2002 1290 3161 204 499 637

2003 1305 3216 227 451 535

2004 1310 3255 246 464 5652005 1317 3329 259 437 498

Total 13,362 23,594 2242 4704 5552

8 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 9/34

U.S. corporate financing came from long-term debt. Long-term debt in the U.S., e.g., bonds, is

issued publicly and managed by financial institutions in the interest of the debt providers. This

arrangement provides for robust monitoring of firms by external financiers, and accounting is

often the chosen device for monitoring. In an agency setting such as that of the U.S., wheremost financing is from public equity providers, managers (agents) tend to favor equity holders

(principals) through higher earnings and dividends. In this setting, the public long-term debt

providers tend to secure their debts with long-term assets. The long-term debt contracts also

have other means of controlling opportunistic behavior by managers. The long-term debts

issued publicly are monitored by trustees, who expect managers to focus on activities that are

necessary to ensure debt repayments (Simerly & Li, 2000). Trustees use debt covenant, often

based on accounting numbers in their trust deeds, to monitor firms. Companies failing to meet

debt covenant requirements are likely to be declared insolvent. Trustees monitor financial

reports of borrowing firms to ensure that earnings are not manipulated. The presence of the

monitoring pressures could be regarded as normative pressures. While legal provisions to

protect creditor rights are present, the U.S. has a system of financial institutions designed to

protect the interests of the debt providers, which obligates companies to provide good quality

accounting information. Accordingly, we also hypothesize for U.S. firms that:

H1b. There is a positive association between external reporting quality and the level of

long-term debt.

As for short-term debts in the U.S., these are often secured against unencumbered

physical assets of the business or guarantees from principals. The interest and repayment

arrangements are tied to the operating cash cycle of firms. Lenders normally charge a higher base rate of interest and favor businesses that have strong management, steady growth

potential, and reliable projected cash flow (McGuire & Dow, 2002). Given the short-term

nature of such debts and the more secure features, including private monitoring devices,

these debts require less public scrutiny through periodic reporting. Furthermore, U.S. public

corporations have low levels of short-term debts. Table 1 shows that between 1994 and

2005, only 4.2% of U.S. corporate financing came from short-term debt. Finally, we

hypothesize for US firms that:

H1c. There is no association between external reporting quality and the level of short-term debt.

Japan: Agency theory has had limited results in explaining the Japanese organizational

system (McGuire & Dow, 2009). Most Japanese firms are located in organizational groups

called keiretsu. The keiretsu firms are governed by a main bank and are generally financed

through both debt and equity. The companies of a keiretsu have cross-holdings in other firms

within the kereitsu. They also often have vertical and horizontal integration of business

activities with firms within the kereitsu (McGuire & Dow, 2002). Institutional theory can be

applied to explain the evolution of keiretsu organizations. Institutional theory views that

pressures for legitimacy drive firms to maintain structures, processes, and procedures although

they may depart from what would otherwise be dictated by economic rationality. Institutional

forces have traditionally supported keiretsus. Keiretsus are congruent with broader Japanesecultural values toward cooperation and collectivism (McGuire & Dow, 2009). We use the

institutional analysis of keiretsus to assess the nature of their accounting practices.

9 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 10/34

In a collectivistic society such as Japan's, keiretsu has been a very successful business

form.2 The interdependencies of keiretsus have led to efficient business practices such as

“ just in time” manufacturing. The keiretsu companies are known to weather the pressures

of business cycles collectively, and takeovers are not often the means of correctinginefficiencies (Gilson & Roe, 1993). In times of crisis, keiretsu main banks may intervene

in the operations of a company to ensure its continued existence (Gilson & Roe, 1993).

Keiretsu interrelated ownership also acts as a safeguard against hostile takeovers ( Shishido,

1999) and collapses (McGuire & Dow, 2009). Although these safety nets are known to be

important for the effective operation of keiretsu form, it has also been regarded as the

reasons for the Japanese banks' lack of action against nonperforming loans (Herr &

Miyazaki, 1999). The banks' involvement in both debt and equity make their agency

relationship with companies complex, particularly in times of corporate failures. In other

words, the members of keiretsus are not distinct entities, but are parts of a wider family of

firms (Gilson & Roe, 1993; McGuire & Dow, 2009). The banks themselves and other

keiretsu partners own substantial amounts (23%–42%) of shares in the keiretsu member

firms (McGuire & Dow, 2009). The monitoring by the debt providers of managers working

in the interest of equity providers, as in the Berle and Means agency setting, is likely to fail

in keiretsus. Also, keiretsu partners help weaker firms level-off their losses (McGuire &

Dow, 2009). To make matters more complex, keiretsu firms also have operational

relationships with firms of other keiretsus. Such relationships can further stifle the

relevance of accounting information as these firms are likely to have inside information.

Inside information by both the keiretsu partners and the outside affiliates lowers the

relevance of publicly disclosed earnings information.Japanese companies have been facing challenging circumstances since the early 1990s

(Gilson & Roe, 1993; McGuire & Dow, 2009). Since most investors and investees are

members of the same group of firms and their operations are linked, the investors' demands

for high quality accounting information can be relaxed when the investee firms face

difficult circumstances such as a recessionary conditions.

The main keiretsu banks and kereitsu partners have private knowledge of the activities

of the keiretsu firms (McGuire & Dow, 2009). A large source of corporate finance in Japan

is debt. Table 1 shows that on average 28.1% of the financing between 1994 and 2005 came

from debt, 12.4% of which was long-term debt and 15.7% was short-term debt. Most of

those debts are acquired from the keiretsu main banks (Gilson & Roe, 1993; Shishido,1999; Miyajima & Arikawa, 2002; Nagano, 2003). Additionally, equity in Japanese firms

often comes from keiretsu sources. Since both equity and debt sources are within the

kereitsu, debt and equity financiers have private access to information about firms within

the keiretsus on an ongoing basis (McGuire & Dow, 2002). Therefore, such financiers rely

less on public information of the firm's earnings and have little reason to monitor the

quality of accounting information in external reports.

In sum, the norm in Japan is that keiretsus are grounded in the idea of group value

maximization rather than maximization of individual interests. Keiretsus have an internal

2 Korea, another collectivistic society, has similar arrangements called chaebols. Chaebols were similarly

successful in the initial phases of development in Korea.

10 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 11/34

monitoring mechanism that reduces the need for outside monitoring. Also, in recent years

the main keiretsu banks, which are both equity and debt providers, have been demanding

higher rents for their participation and support in providing finance to firms (McGuire &

Dow, 2009). The absence of appropriate market-monitoring mechanisms may lead to theuse of methods of accounting that enhance key accounting numbers such as earnings.

Additionally, profit smoothing to allow firms to deal with the effects of economic

downturns has been an issue in keiretsus (McGuire & Dow, 2009). Leveling is done either

through real-earnings manipulation or through earnings management. Japan has

experienced slow or negative economic growth since the early 1990s. This has increased

the pressure on firms to provide higher earnings and, at the same time, deplete the firms'

capacity to manage real earnings. In these circumstances, firms with higher equity and debt

financing would tend to use higher abnormal accruals to prop up their earnings. This is

likely to motivate them to inflate their earnings using abnormal accruals, especially when

they are facing unfavorable economic conditions and the outside financiers do not have

strong monitoring capacity in a keiretsu-dominant setting. Therefore, we hypothesize for

Japanese firms that:

H2a. There is a negative association between external reporting quality and the level of

equity.

H2b. There is a negative association between external reporting quality and the level of

long-term debt.

H2c. There is a negative association between external reporting quality and the level of short-term debt.

Thailand : Thailand has an emerging capital market with an emerging regulatory system.

Its institutional setting prior to the Asian financial crisis (AFC) of 1997 was summed up by

the former prime minister of Thailand, Anand Panyarachun, in the following manner:

In our rush to catch up with the West, the lessons we learned from the West and

from our past — were incomplete. While the West had evolved checks and balances

to curb the excesses of capitalism, in our exuberance to reap the fruits of capitalism

the need for such mechanisms was unheeded. While transparency and accountabilityhad long been pillars of public governance in the West, in Asia the webs of power

and money remain largely hidden from public view…We created a hybrid form of

capitalism where patronage was put to the service of profit-maximization, indeed a

recipe for unbalanced and unsustainable development. (ADB, 1999 p. i)

Because of Thailand's weak judicial and regulatory system, Thai companies are

generally closely owned by families (Alba, Claessens, & Djankov, 1998; Jyoti,

Bunkanwanicha, Pramuan, & Yupana, 2006). Also, Thailand does not have an active

long-term debt market, and as a result, Thai companies have had a high propensity to rely

on short-term debt, even if it is for long-term assets. In the period prior to the AFC, largeamounts of short-term debt were acquired by companies from foreign sources making

themselves vulnerable to risks of currency value fluctuation (Dollar & Hallward-

11 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 12/34

Drlemeler, 2000). Explaining the risk created by such debt, Limpaphayom (1999) states

that:

In the prelude to the 1997 crisis, short-term private debt obligations grew to about 60% of total private sector debts. The majority of these debts were not properly

hedged. As a result, Thai corporations were collectively overexposed to exchange

rate risks. The fixed exchange rate policy, coupled with financial liberalization and

deregulation in the absence of an effective regulatory and supervisory system,

magnified the impact of these problems on the economy when the crisis hit. (p. 229).

Limpaphayom (1999) explains the borrowing situation in the following manner:

Companies generally issued short-term debt instruments like promissory notes or

bills of exchange. Investors had limited knowledge of debt instruments. A turning

point of the corporate debt market was the enactment of the SEA (Securities and

Exchange Act ) of 1992, which encouraged limited companies and public companies

to issue debt instruments. Four years after the passage of the SEA, the size of the

corporate debt market rose to Bhat 132.9 billion. (p. 225).

In post-AFC Thailand, regulatory measures were put in place to improve accounting

practices and attention was paid by both local and foreign regulators on the excessive use of

short-term foreign debt to finance long-term projects. According to Metzger (2004), the

SEC of Thailand reviewed the accounting principles and practices for listed companies to

bring them in line with international best practices. Tougher requirements were put in placefor improving financial reporting (including disclosure of external liabilities and off-

balance-sheet liabilities). Further, all listed companies were required to establish audit

committees comprised of independent directors.

While regulatory shortcomings and short-term debt have been highlighted in the

literature explaining the accounting practices in Thailand recently, a major feature that is

likely to drive accounting in that country is family control. Family control and long-term

debts from banks related to families is a dominant feature of Thai corporate finance and

governance arrangements (Jyoti et al., 2006). With the dominance of closely held family

firms, we expect neither the level of equity nor the level of long-term debt to have any

significant effect on the quality of externally related financial information. Ball et al. (2003) point out that more extensive family or other networks reduce the demand for accounting

transparency and timely public disclosure. The family-controlled firms, they believe, have a

preference for internal funds and bank loans over public equity and debt because the

families do not want to lose control over their businesses. This they argue reduces the

expected costs arising from stockholder and creditor litigation concerning alleged losses

arising from untimely disclosure.

Ball et al. (2003) further explain that the predominance of networked family business

groups is due to less developed capital, labor, and product markets. These groups, they argue,

are alternative contracting systems with low contracting costs for insiders. They also contend

that another factor that reduces the need for public disclosure in Southeast Asian countries isthe prominence of banks as suppliers of capital. To strengthen family control, the banks are

often controlled by the families that control the family groups (Bunkanwanicha, Gupta, &

12 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 13/34

Wiwattanakantan, 2007; Bertrand, Johnson, & Schoar, 2004). Therefore, we hypothesize for

Thai firms that:

H3a. There is no association between external reporting quality and the level of equity.

H3b. There is no association between external reporting quality andthe level of long-term debt.

Table 1 confirms that, relative to the U.S. firms, Thai firms have higher levels of short-

term bank debt (23.4% of total assets as compared to 4.2% for the U.S. for the years 1994 to

2005). Excessive use of short-term debt for long-term activities receives close attention

from commentators and financiers (Metzger, 2004). Long-term debt is scarce in Thailand

(Alba et al., 1998). For the period 1994 to 2005, 15.3% of the total assets have been

financed using long-term debt as compared to 23.4% for short-term debt ( Table 1). Since

short-term debt continues to be significant financing source and it has been receivingconsiderable scrutiny, we expect such a source to influence the quality of external reporting

of Thai firms. It is likely that Thai firms that have higher short-term debt produce better

quality external information. Therefore, we also hypothesize for Thai firms that:

H3c. There is a positive association between external reporting quality and the level of

short-term debt.

France: France's institutional setting is made up of firms that have high blockholder

concentration in company shares countered by regulations that have a creditor and social

focus. According to Van der Elst (2004), more than 70% of French companies have at least one blockholder holding over 25% of the company's shares and more than half of the

companies have a majority shareholder (holding above 50% of shares). Additionally, while

French firms are known to have high levels of debt relative to equity (more than a 2 to 3

ratio of debt to equity as opposed to about one-third for the U.S., Table 1), they have

significant amounts of reserves and provisions that are under the control of the blockholders

of shares. While the requirements to provide for provisions and reserves can counteract

against opportunistic behavior of the blockholders, the ability to be opportunistic can

increase with the level of equity financing. The level of equity gives control to the insiders

to manage earnings opportunistically to attract minority shareholders and expropriate their

wealth, and also allows the insiders to monitor their interests in the firm.France has a conservative approach to regulating business activities, including

accounting. It follows a codified regulatory system whereby its accounting system is part

of a wider national code. At the business level, this code tends to safeguard the interests of

the creditors and the society at large. The accounting rules, within the codified business

rules, demands conservative practices. Moreover, corporate accounting in France is closely

associated with French taxation procedures. This provides fewer opportunities for

manipulating accounting numbers. In spite of the conservative measures, because of the

presence of blockholders, control can be established by insiders to manage earnings

opportunistically. Since blockholding is quite common in companies of all sizes, the

tendency to manage earnings will be higher in firms with higher levels of equity (larger equity firms are likely to have more minority shareholders). In this respect Goyer (2003)

notes that French companies maintain various practices such as earnings management that

13 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 14/34

effectively disenfranchise minority shareholders, allowing them to raise capital without

losing control of the firm. Therefore, we hypothesize for French firms that:

H4a. There is a negative association between external reporting quality and the level of equity.

Debt financing is a major source of company financing. As shown in Table 1 about 25%

of financing of French firms is directly from debt. Banks are allowed to hold company

shares and be represented on a company's board. Although such arrangements should result

in internal monitoring of company activities and finances, which should not require better

quality external reporting, the French regulatory system requires better accounting

disclosures to protect the interests of the creditors and debt providers. Furthermore, the

larger the firm the greater is the stringency of the auditing requirements. In France, the debt

providers are regarded as an external source of funds, whereas the equity providers areregarded as “own funds” (Friderichs, Paranque, & Sauve, 1999). To protect the interests of

the debt providers, the French laws also require significant amounts of provisions and

reserves, and requires a better accounting practices when the debt levels are high (Friderichs

et al., 1999). There seems to be no distinction made between long-term and short-term debt.

Likewise, we also hypothesize for French firms that:

H4b. There is a positive association between external reporting quality and the level of

long-term debt.

H4c. There is a positive association between external reporting quality and the level of

short-term debt.

Germany: In Germany, at the outset the accounting institutional setting looks similar to

that of France. However, it has its own peculiarities as well. Blockholding of shares is very

high and prevalent across firms of all sizes. Among the Western European countries, its

blockholder control is second only to France. The most important blockholders are other

business enterprises followed by families and then the large banks (Schmidt, 2003).

German companies have blockholder concentration in excess of 50%, giving the

blockholders veto rights (Schmidt, 2003; Van der Elst, 2004). Such a capacity allows

controlling shareholders to manage earnings opportunistically if the level of equity is higher

relative to other forms of financing. This is perhaps why German firms with higher

blockholder concentration report higher earnings (Schmidt, 2003). It can be argued that

when insiders control the firm they are in a position to manage earnings to portray a better

performance profile of the firm. Accordingly, we hypothesize for German firms that:

H5a. There is a negative associationbetween external reporting quality and the level of equity.

Unlike in France, the amount of debt relative to equity is low and debt providers maintain

ownership and board representation in Germany (Friderichs et al., 1999). Germany has a two

tier system of governance with two governing boards. The overall governing board is thesupervisory board which has representation from shareholders, employees and debt holders

(also known as co-determination: Schmidt, 2003). The second board, the management board,

14 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 15/34

conducts the day-to-day activities of the firm (Schmidt, 2003; Altana, 2008). The presence of

debt providers in the supervision of the firm and their ability to be a significant part of

ownership enables them to have private access to company information. German bankruptcy

legislation guarantees creditor protection interests (Friderichs et al., 1999). Protection of thedebt provider is also an important goal of the German legal arrangements.

Furthermore, historically German law has provided for stricter audit requirements (Shiobara

& Inoue, 2001). Within Germany, the supervisory board, not the management board, is

responsible for auditing (Leuz & Wüstemann, 2003). As supervisory boards often have

members who are debt providers, such external audits are expected to highlight the interests of

the debt providers. Given their capacity to monitor internally, the presence of regulations, and

thelow level of debt relative to equity, German debt providers have little need for to use external

financial reports to monitor firms. Likewise, we also hypothesize for German firms that:

H5b. There is a no association between external reporting quality and the level of long-

term debt.

H5c. There is a no association between external reporting quality and the level of short-

term debt.

Akin to the explanations of institutional theory, we note varying pressures in the financial

reporting processes across different countries, not all of which resemble the classic agency

relationships discussed in the agency theory literature. Agency theory assumes a separation

between managerial control, ownership/equity, and debt; and because equity and long-term

debt are generally publicly held in agency settings, e.g., the U.S. S&P1500 firms, we expect

better quality reporting for higher levels of equity and long-term debt. For non-U.S. settings, we

argue that specific organizational, ownership, and regulatory arrangements create different

pressures from those of the U.S. These pressures alter the role of financing sources as monitors

of earnings quality, giving rise to a different set of associations between earnings quality and

forms of financing.

4. Research design

4.1. Research model

An effective way for management to influence reported earnings subtly is to manipulate

accounting policies relating to abnormal accruals. Users of financial reporting data can be

misled into interpreting reported accounting earnings as equivalent to economic profitability

(Fields, Lys, & Vincent, 2001, p. 279). However, accruals can also inform the investors

about future cash flows as they require assumptions and estimates of future cash inflows and

outflows. Estimating accruals requires managerial judgment and prudent accounting

allocations. Callen and Segal (2004) find that accruals are a driver of current stock returns.

Studies such as Francis, LaFond, Olsson, and Schipper (2004) and Boonlert-U-Thai, Meek,

and Nabar (2006), among others, use accruals quality to study earnings quality and viewearnings to be of higher quality if accruals quality is high. Several models of accruals quality

have been developed since Jones (1991). We choose the relatively simple modified Jones

15 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 16/34

model as stated in Kothari, Leone, and Wasley (2005) without the performance control. We

make this choice for two reasons. First, we have data constraints for Japan, Thailand, France,

and Germany, so a simple model would lead to a better sample size as it would have fewer

variables leading to fewer missing observations. Second, the abnormal accruals of the modifiedJones model provides a reasonable indication of the nature of accounting practice and policy

choice of a firm, and is broad enough to capture the effects of institutional influences on

accounting practice. Haw, Hu, Hwang, and Wu (2004) argue that absolute abnormal accruals

using the Jones (1991) model captures the insiders' tendency to both overstate reported income

to conceal resource diversion and to understate income in good performance years to create

reserves for poor-performance periods in the future. According to them, this measure also

avoids conceptual ambiguity associated with benchmark measures. Benchmark measures, they

believe, do not consider whether the observed results are achieved through income

management, expectations management, or improvement in operations. They further argue

that the unsigned abnormal accrual is the most appropriate measure of earnings management

because it captures the net effect of both income-increasing and income-decreasing abnormal

accrual estimations. Income-increasing abnormal accruals represent management of current-

period income, while income-decreasing abnormal accruals indicate intentions of future

earnings management or a reversal of previous period earnings management. Since we are

interested only in accounting-based earnings management, we use absolute abnormal accruals

as a broad proxy to capture the quality of financial reporting practices.

To compute abnormal accruals, we first determine a firm's total accruals for the year as

the difference between operating cash flows and net income. Then we separate the

abnormal component of total accruals in the following manner:

TAat = Aat −1 = αa + β11 = Aat −1 + β2Δ REV at = Aat −1 + β3 PPE at = Aat −1 + εat

ðModel 1Þ

where:

TAat total accruals for firm a in year x (income before tax less cash flow from

operations)

ΔREVat revenues for firm a in year x less revenues for year ( x−1)

PPEat gross property, plant and equipment for firm a in year xAat −1 total assets for firm a in year t −1

εat a residual term that captures abnormal accruals.

The inclusion of ΔREVat and PPEat is to account for normal accruals of current assets

and liabilities and the normal aspect of amortization and depreciation expenses that is

dependent on the firm's investment in capital assets, respectively. The residual, i.e., εat , is

an estimate of the abnormal accrual of year x for firm a.

Following Kothari et al. (2005), we compute abnormal accruals by year and industry. For

industry, we use single digit Global Industry Classification Standard (GICS) codes instead of

two digit GICS codes used by Kothari et al. (2005) because Thailand, France, and Germanyhad too few companies within several two digit codes in some years. Dropping these

companies would reduce the already small sample sizes for each year for these countries, and

16 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 17/34

would make the samples of these countries different in industry composition from those of the

U.S. and Japan. We identify the following industries: Consumer Discretionary, Consumer

Staples, Energy, Financials, Health Care, Industrials, Information Technology, Materials,

Telecommunication, and Utilities. Computation by year is needed to control for macroeconomic fluctuations that affect firm growth and performance, and computation by

industry is needed because product and cash flow cycles are different in different industries.

Firms having longer product and cash flow cycles are likely to have higher accruals allowing

managers more leeway for manipulating the accruals.

To test the hypotheses, we model the relation between absolute abnormal accruals (|AAt |)

or financial reporting quality and the independent variables in the following manner:

lg j AAt j = α + β1lgEQUITY t + β2lgLT DEBT t + β3lgST DEBT t + β4lgRET t

+ β5 RET SIGN t + β6 lgSIZE t + β7lgGRWTH t ðModel 2Þ

where:

lg|AA| log of absolute abnormal accruals (|εax| of Model 1). A higher value means lower

earnings quality. A positive (negative) association with |AA| means a negative

(positive) association with earnings quality.

lgEQUITY log of the ratio common shareholder equity by total assets

lgLT_DEBT log of the ratio long-term debt by total assets

lgST_DEBT log of the ratio short-term debt by total assets

lgRET log of the ratio absolute value of prior-year market returnRET_SIGN sign of prior-year market return

lgSIZE log of end-of-year market value

lgGRWTH log of the ratio market value of equity to book value of equity.

All measures for the above variables are from Global Vantage. lg|AA| is the dependent

variable for all of our hypotheses. lgEQUITY, lgLTDA2A, and lgST_DEBT are the

independent variables. All other variables are control variables. lgRET and RET_SIGN are

employed to control for market-based influences that provide incentives for firms to manage

their earnings. Market euphoria has often been cited as a reason for firms to provide

overestimated earnings numbers to make firm performance impressive relative to other firmsin the market. The return that is used for lgRET is the prior-year return of a firm. In a euphoric

market, firms are likely to attempt to meet the earnings expectation of the market set in the

prior-year returns. Alternatively, they could attempt to improve the current year returns by

enhancing current-year earnings when the previous year returns are low. The magnitude and

sign of annual returns are separated because the absolute value of returns has to be used due

to the use of the absolute value of abnormal accruals as the dependent variable.

lgSIZE captures the effects of missing variables that are related to firm size, e.g.,

corporate governance arrangement arising from the use of better auditors in larger firms.

lgGRWTH is used to control for the influence of growth on abnormal accruals.3 Firms that

3 Growth in the form of ΔREV has been considered while computing |AA| in Model 1. However, ΔREV

captures only short-term growth and not long-term future growth generated by current operations.

17 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 18/34

have high market value relative to book value are considered as growth firms. They are

likely to have high positive abnormal accruals due to high revenues or high negative

abnormal accruals due to large accrued expenses for probable positive NPV projects.

4.2. Sample and data collection

Our data consist of firm-year observations from 1994 to 2005. We have five samples,

one for the US S&P1500 firms and one each for Japanese, Thai, French, and German firms.

Data were collected from Compustat for the US firms and from Global Vantage for firms in

the other four countries. We collected all firm-year data available from these two databases

for computing our variable measures for the eleven years. In all, we have 13,362 firm-year

observations for US firms, 23,594 for Japanese firms, 2242 for Thai firms, 4704 for French

firms and 5552 for German firms (Table 2). We use S&P1500 firms for the U.S. because

they represent small-cap, mid-cap and large-cap firms, thereby providing a broad sample of

firms with agency settings as depicted in the agency theory literature.

A summary of the sample by countries and years is provided in Table 2. We took all

firm-year observations since 1994. Samples were small for 1994 due to a lack of data. In

particular, cash flow information was absent for many Japanese firms for both 1994 and

1995. According to S&P, the publishers of COMPUSTAT, and GLOBAL VANTAGE,

many Japanese companies did not report depreciation and amortization numbers until 1995.

Cash flow from operations cannot be computed without depreciation and amortization

numbers. Because of the small number of firms for Thailand, France, and Germany, we

reduced the required number of firms for each GICS-year group for computing |AA| to onlyfive. The required number in most U.S. studies is 15.

5. Results

5.1. Descriptive statistics

The trends of median |AA| of all firms, positive |AA| firms, and negative |AA| firms and

the proportion of firms in these three categories of all five countries for the years 1994 to

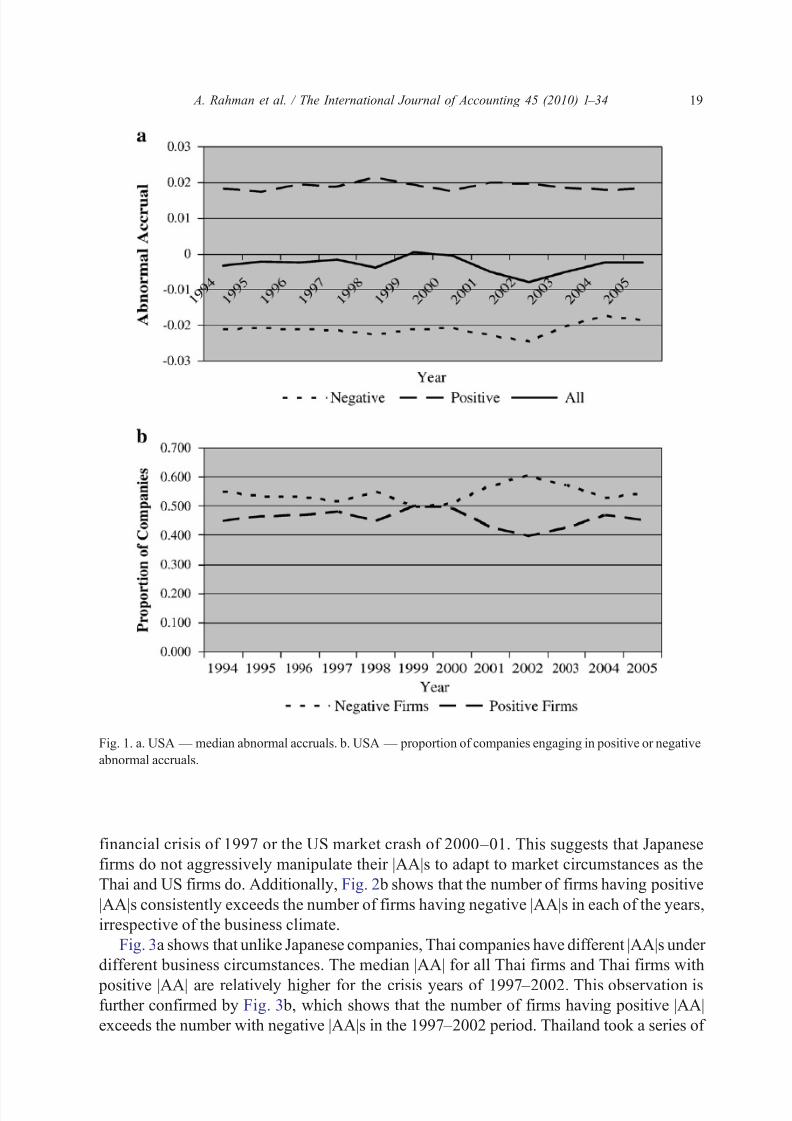

2005 are charted in Figs. 1–5. For the U.S., Fig. 1a shows that the median |AA|s for all firms

are higher in years 1999 to 2000 than 2002 to 2004. The years 2000 and 2001 are regardedas the dot.com crash years and Sarbanes–Oxley Act was enacted in 2002 and came into

effect in 2004. However, by 2005 the median |AA| started to rise again, which perhaps is a

precursor to the 2008 crash. The median |AA| of the U.S. positive |AA| firms is at a similar

level for all years, while for negative |AA| firms the |AA| dropped slightly after the dot.com

crisis, but then went to similar levels as in 2004 and 2005.

Fig. 1 b shows that the number of firms having negative |AA|s exceeds those having

positive |AA|s in the period prior to 2000. This situation is reversed for a brief period in

1999 and 2000. After 2000 the number of negative |AA| firms far exceeds the number of

positive |AA| firms.

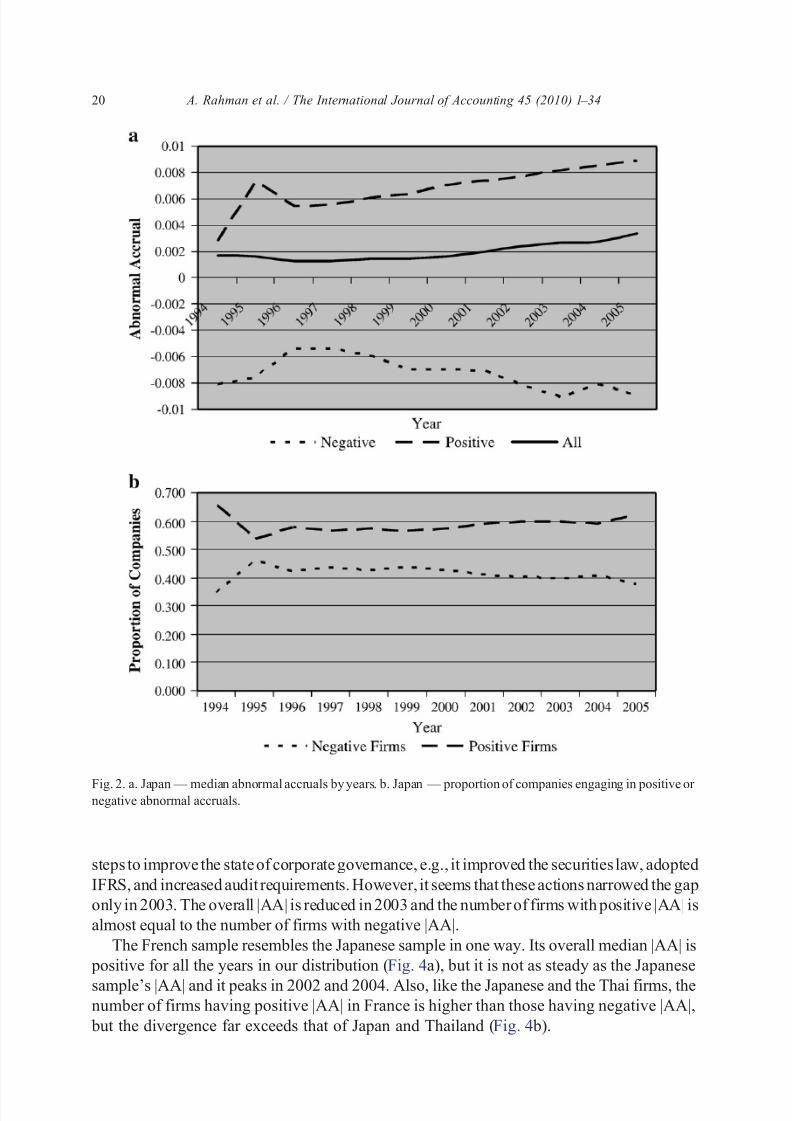

Overall, although Fig. 2a and b show that the median |AA|s for all Japanese firms and the proportion of Japanese firms with positive |AA| were rising gradually, the negative |AA|

medians were declining. The trend was smooth and remained unaffected by the Asian

18 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 19/34

financial crisis of 1997 or the US market crash of 2000–01. This suggests that Japanese

firms do not aggressively manipulate their |AA|s to adapt to market circumstances as the

Thai and US firms do. Additionally, Fig. 2 b shows that the number of firms having positive

|AA|s consistently exceeds the number of firms having negative |AA|s in each of the years,

irrespective of the business climate.

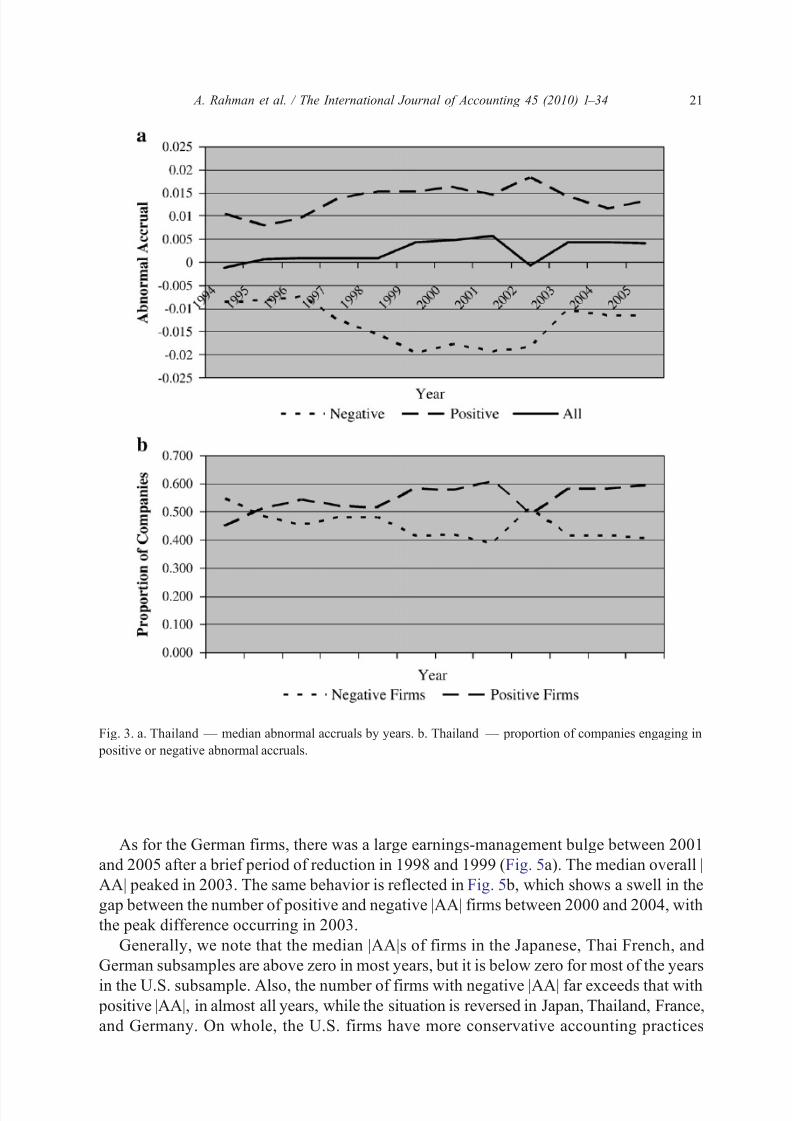

Fig. 3a shows that unlike Japanese companies, Thai companies have different |AA|s under

different business circumstances. The median |AA| for all Thai firms and Thai firms with

positive |AA| are relatively higher for the crisis years of 1997–2002. This observation isfurther confirmed by Fig. 3 b, which shows that the number of firms having positive |AA|

exceeds the number with negative |AA|s in the 1997–2002 period. Thailand took a series of

Fig. 1. a. USA — median abnormal accruals. b. USA — proportion of companies engaging in positive or negative

abnormal accruals.

19 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 20/34

steps to improve the state of corporate governance, e.g., it improved the securities law, adopted

IFRS, and increased audit requirements. However, it seems that these actions narrowed the gap

only in 2003. The overall |AA| is reduced in 2003 and the number of firms with positive |AA| is

almost equal to the number of firms with negative |AA|.

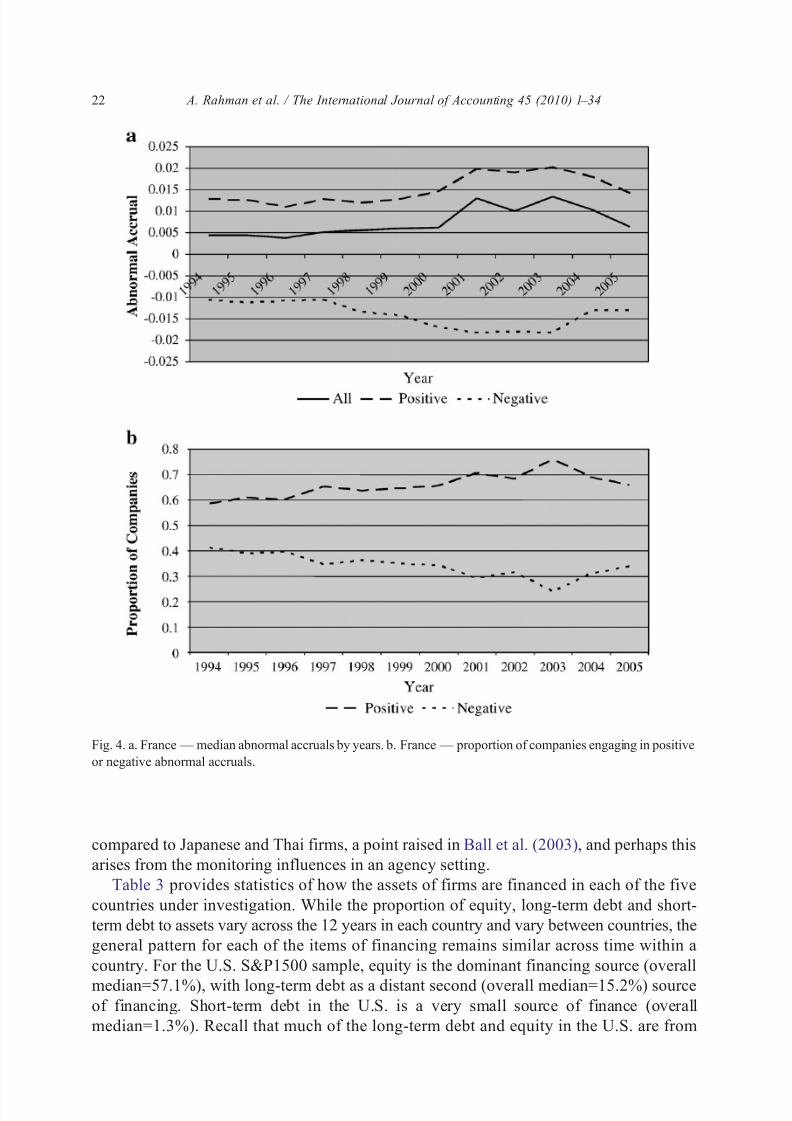

The French sample resembles the Japanese sample in one way. Its overall median |AA| is

positive for all the years in our distribution (Fig. 4a), but it is not as steady as the Japanese

sample's |AA| and it peaks in 2002 and 2004. Also, like the Japanese and the Thai firms, thenumber of firms having positive |AA| in France is higher than those having negative |AA|,

but the divergence far exceeds that of Japan and Thailand (Fig. 4 b).

Fig. 2. a. Japan—median abnormal accruals by years. b. Japan — proportion of companies engaging in positive or negative abnormal accruals.

20 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 21/34

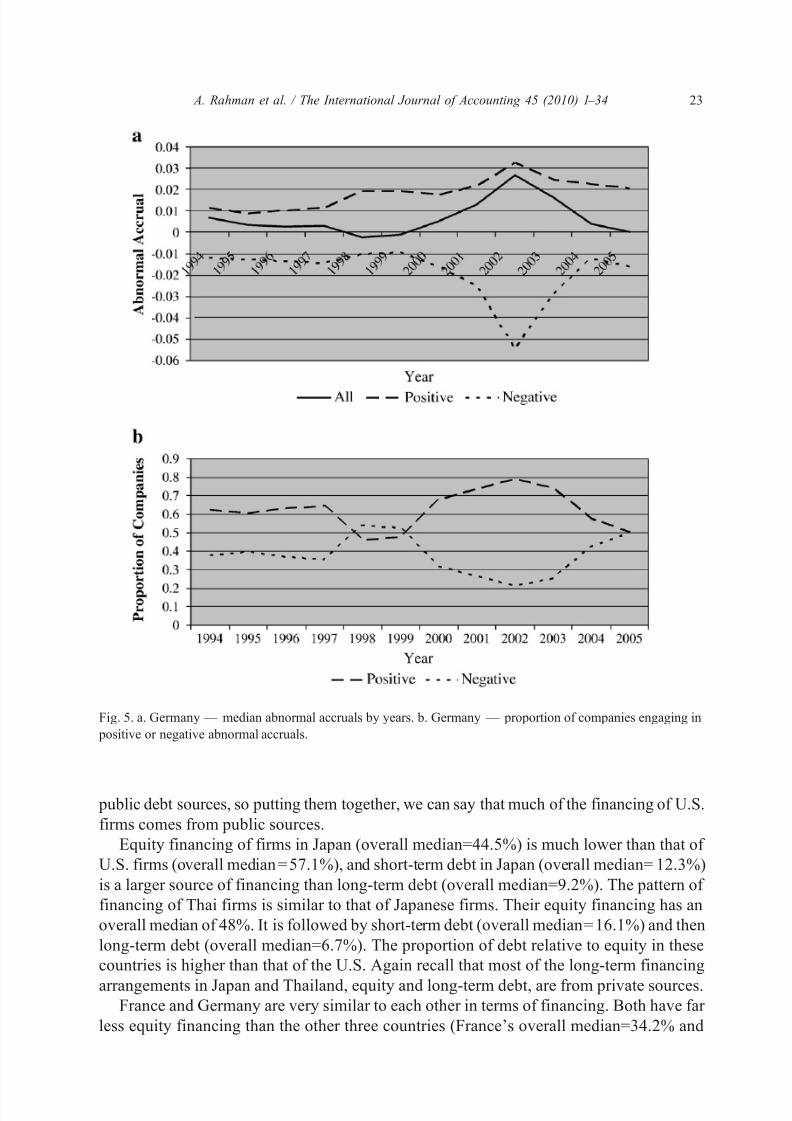

As for the German firms, there was a large earnings-management bulge between 2001

and 2005 after a brief period of reduction in 1998 and 1999 ( Fig. 5a). The median overall |

AA| peaked in 2003. The same behavior is reflected in Fig. 5 b, which shows a swell in the

gap between the number of positive and negative |AA| firms between 2000 and 2004, with

the peak difference occurring in 2003.

Generally, we note that the median |AA|s of firms in the Japanese, Thai French, and

German subsamples are above zero in most years, but it is below zero for most of the years

in the U.S. subsample. Also, the number of firms with negative |AA| far exceeds that with positive |AA|, in almost all years, while the situation is reversed in Japan, Thailand, France,

and Germany. On whole, the U.S. firms have more conservative accounting practices

Fig. 3. a. Thailand — median abnormal accruals by years. b. Thailand — proportion of companies engaging in

positive or negative abnormal accruals.

21 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 22/34

compared to Japanese and Thai firms, a point raised in Ball et al. (2003), and perhaps this

arises from the monitoring influences in an agency setting.

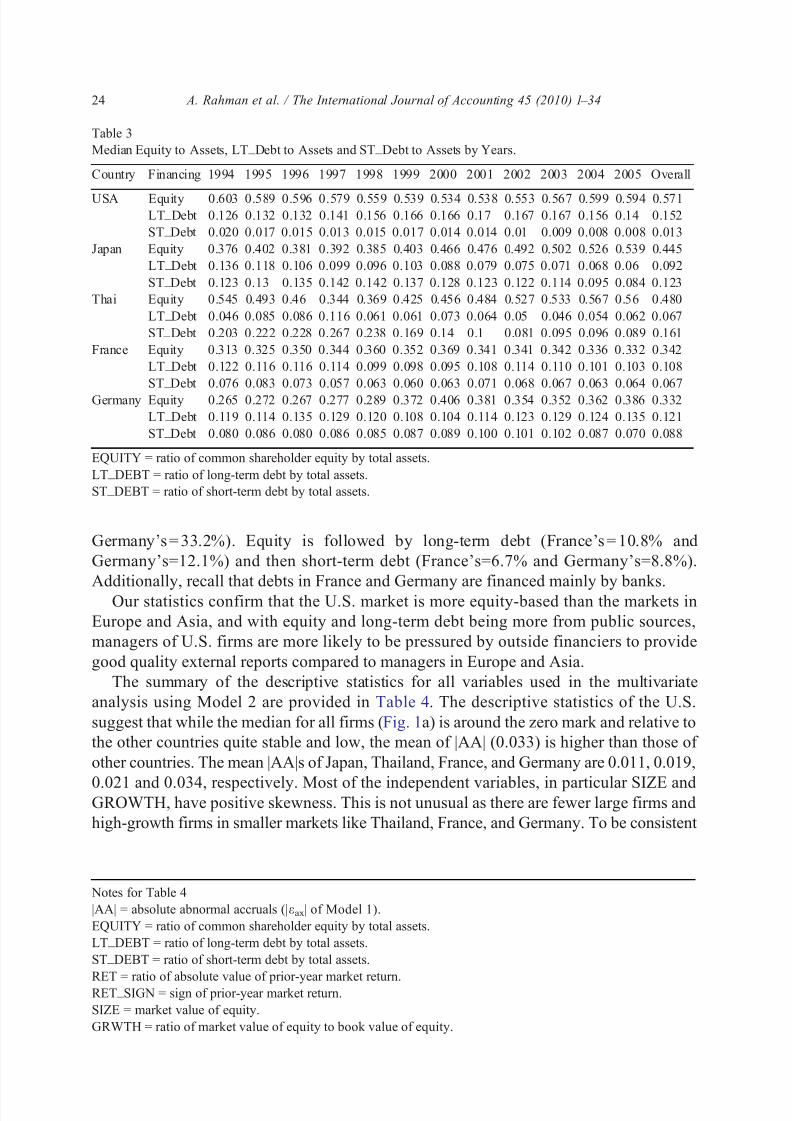

Table 3 provides statistics of how the assets of firms are financed in each of the five

countries under investigation. While the proportion of equity, long-term debt and short-

term debt to assets vary across the 12 years in each country and vary between countries, the

general pattern for each of the items of financing remains similar across time within a

country. For the U.S. S&P1500 sample, equity is the dominant financing source (overall

median=57.1%), with long-term debt as a distant second (overall median=15.2%) sourceof financing. Short-term debt in the U.S. is a very small source of finance (overall

median=1.3%). Recall that much of the long-term debt and equity in the U.S. are from

Fig. 4. a. France —median abnormal accruals by years. b. France— proportion of companies engaging in positive

or negative abnormal accruals.

22 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 23/34

public debt sources, so putting them together, we can say that much of the financing of U.S.

firms comes from public sources.

Equity financing of firms in Japan (overall median=44.5%) is much lower than that of

U.S. firms (overall median = 57.1%), and short-term debt in Japan (overall median= 12.3%)

is a larger source of financing than long-term debt (overall median=9.2%). The pattern of

financing of Thai firms is similar to that of Japanese firms. Their equity financing has an

overall median of 48%. It is followed by short-term debt (overall median= 16.1%) and then

long-term debt (overall median=6.7%). The proportion of debt relative to equity in these

countries is higher than that of the U.S. Again recall that most of the long-term financing

arrangements in Japan and Thailand, equity and long-term debt, are from private sources.France and Germany are very similar to each other in terms of financing. Both have far

less equity financing than the other three countries (France's overall median=34.2% and

Fig. 5. a. Germany — median abnormal accruals by years. b. Germany — proportion of companies engaging in

positive or negative abnormal accruals.

23 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 24/34

Germany's = 33.2%). Equity is followed by long-term debt (France's = 10.8% and

Germany's=12.1%) and then short-term debt (France's=6.7% and Germany's=8.8%).

Additionally, recall that debts in France and Germany are financed mainly by banks.

Our statistics confirm that the U.S. market is more equity-based than the markets in

Europe and Asia, and with equity and long-term debt being more from public sources,

managers of U.S. firms are more likely to be pressured by outside financiers to provide

good quality external reports compared to managers in Europe and Asia.

The summary of the descriptive statistics for all variables used in the multivariate

analysis using Model 2 are provided in Table 4. The descriptive statistics of the U.S.

suggest that while the median for all firms (Fig. 1a) is around the zero mark and relative to

the other countries quite stable and low, the mean of |AA| (0.033) is higher than those of

other countries. The mean |AA|s of Japan, Thailand, France, and Germany are 0.011, 0.019,

0.021 and 0.034, respectively. Most of the independent variables, in particular SIZE andGROWTH, have positive skewness. This is not unusual as there are fewer large firms and

high-growth firms in smaller markets like Thailand, France, and Germany. To be consistent

Table 3

Median Equity to Assets, LT_Debt to Assets and ST_Debt to Assets by Years.

Country Financing 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Overall

USA Equity 0.603 0.589 0.596 0.579 0.559 0.539 0.534 0.538 0.553 0.567 0.599 0.594 0.571LT_Debt 0.126 0.132 0.132 0.141 0.156 0.166 0.166 0.17 0.167 0.167 0.156 0.14 0.152

ST_Debt 0.020 0.017 0.015 0.013 0.015 0.017 0.014 0.014 0.01 0.009 0.008 0.008 0.013

Japan Equity 0.376 0.402 0.381 0.392 0.385 0.403 0.466 0.476 0.492 0.502 0.526 0.539 0.445

LT_Debt 0.136 0.118 0.106 0.099 0.096 0.103 0.088 0.079 0.075 0.071 0.068 0.06 0.092

ST_Debt 0.123 0.13 0.135 0.142 0.142 0.137 0.128 0.123 0.122 0.114 0.095 0.084 0.123

Thai Equity 0.545 0.493 0.46 0.344 0.369 0.425 0.456 0.484 0.527 0.533 0.567 0.56 0.480

LT_Debt 0.046 0.085 0.086 0.116 0.061 0.061 0.073 0.064 0.05 0.046 0.054 0.062 0.067

ST_Debt 0.203 0.222 0.228 0.267 0.238 0.169 0.14 0.1 0.081 0.095 0.096 0.089 0.161

France Equity 0.313 0.325 0.350 0.344 0.360 0.352 0.369 0.341 0.341 0.342 0.336 0.332 0.342

LT_Debt 0.122 0.116 0.116 0.114 0.099 0.098 0.095 0.108 0.114 0.110 0.101 0.103 0.108

ST_Debt 0.076 0.083 0.073 0.057 0.063 0.060 0.063 0.071 0.068 0.067 0.063 0.064 0.067

Germany Equity 0.265 0.272 0.267 0.277 0.289 0.372 0.406 0.381 0.354 0.352 0.362 0.386 0.332

LT_Debt 0.119 0.114 0.135 0.129 0.120 0.108 0.104 0.114 0.123 0.129 0.124 0.135 0.121

ST_Debt 0.080 0.086 0.080 0.086 0.085 0.087 0.089 0.100 0.101 0.102 0.087 0.070 0.088

EQUITY = ratio of common shareholder equity by total assets.

LT_DEBT = ratio of long-term debt by total assets.

ST_DEBT = ratio of short-term debt by total assets.

Notes for Table 4

|AA| = absolute abnormal accruals (|εax| of Model 1).

EQUITY = ratio of common shareholder equity by total assets.

LT_DEBT = ratio of long-term debt by total assets.

ST_DEBT = ratio of short-term debt by total assets.

RET = ratio of absolute value of prior-year market return.RET_SIGN = sign of prior-year market return.

SIZE = market value of equity.

GRWTH = ratio of market value of equity to book value of equity.

24 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 25/34

Table 4

Descriptive statistics.

Percentile

Mean Std. Dev. 5 25 75 95 99

USA

|AA| 0.033 0.070 0.000 0.010 0.040 0.100 0.220

EQUITY 0.783 0.176 0.480 0.660 0.950 1.000 1.000

LT_DEBT 0.180 0.158 0.000 0.030 0.290 0.460 0.620

ST_DEBT 0.037 0.070 0.000 0.000 0.040 0.150 0.340

RET% 36.513 273.024 1.000 1.000 41.450 121.150 294.060

SIZE ($ m) 6895.361 23,471.070 130.499 502.425 4152.454 27,028.012 108,719.476

GRWTH 2.798 65.342 0.420 0.910 2.560 6.160 11.870

Japan

|AA| 0.011 0.015 0.000 0.000 0.010 0.030 0.060EQUITY 0.378 0.193 0.080 0.230 0.510 0.720 0.820

LT_DEBT 0.099 0.099 0.000 0.020 0.140 0.290 0.440

ST_DEBT 0.171 0.132 0.010 0.070 0.250 0.420 0.570

RET% 38.867 59.433 1.900 10.500 47.350 116.560 260.680

SIZE (¥ m) 92,462.555 452,873.438 1310.878 4388.979 43,891.385 391,127.154 1,315,870.334

GRWTH 1.614 5.726 .292 .570 1.641 4.226 11.032

Thailand

|AA| 0.019 0.025 0.000 0.010 0.020 0.050 0.130

EQUITY 0.531 0.213 0.200 0.370 0.690 0.900 0.950

LT_DEBT 0.119 0.149 0.000 0.000 0.200 0.430 0.600

ST_DEBT 0.172 0.158 0.000 0.040 0.270 0.500 0.610

RET% 51.602 107.659 2.170 11.320 51.480 160.000 528.320

SIZE (B m) 10,559.440 43,716.341 183.000 543.000 3909.000 38,958.000 249,774.000

GRWTH 2.396 13.795 0.390 0.760 1.910 4.820 15.330

France

|AA| 0.021 0.039 0.000 0.010 0.020 0.050 0.140

EQUITY 0.373 0.179 0.110 0.240 0.480 0.690 0.850

LT_DEBT 0.132 0.117 0.000 0.040 0.190 0.360 0.490

ST_DEBT 0.092 0.083 0.000 0.030 0.130 0.250 0.370

RET% 38.244 71.787 2.100 11.120 46.960 97.560 219.360

SIZE (€

m) 2427.574 9019.960 6.596 36.622 874.870 11,476.733 45,059.986GRWTH 3.145 24.944 0.510 1.030 2.820 7.130 19.390

Germany

|AA| 0.034 0.073 0.000 0.010 0.040 0.090 0.320

EQUITY 0.371 0.217 0.070 0.210 0.510 0.790 0.920

LT_DEBT 0.105 0.125 0.000 0.000 0.160 0.350 0.540

ST_DEBT 0.090 0.109 0.000 0.010 0.130 0.320 0.470

RET% 38.079 55.520 1.820 9.850 49.350 102.690 244.140

SIZE (€ m) 1977.999 7470.745 6.660 33.200 567.972 10,641.864 35,712.168

GRWTH 4.825 51.735 0.400 1.020 2.880 7.890 28.820

25 A. Rahman et al. / The International Journal of Accounting 45 (2010) 1 – 34

8/10/2019 Rahman et al 2010.pdf

http://slidepdf.com/reader/full/rahman-et-al-2010pdf 26/34

in manner, we normalize the distributions between years and between countries we use log

transformation to reduce skewness.

The distribution of the means of EQUITY, LT_DEBT and ST_DEBT in Table 4 are

generally in line with the distribution of medians of these variables in Table 3. Thisconfirms that equity is the main financing variable in all five countries, but it is used far