MEA Unit V

10

DATTA MEGHE INSTITUTE OF ENGINEERING, TECHNOLOGY AND RESEARCH, SAWANGI (MEGHE), WARDHA Managerial Economics & Accountancy III rd Sem IT Yashwant Misale (B.E,MMS) [Faculty MBA Department]

-

Upload

yashwant-misale -

Category

Documents

-

view

218 -

download

0

Transcript of MEA Unit V

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 1/10

DATTA MEGHE INSTITUTE OF ENGINEERING,

TECHNOLOGY AND RESEARCH, SAWANGI(MEGHE), WARDHA

Managerial Economics&

Accountancy

IIIrd Sem IT

Yashwant Misale(B.E,MMS)

[Faculty MBA Department]

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 2/10

Unit : 5

Accounting Concepts and Introduction to GL

When a person starts a business his main aim is to earn profit. He receives money from certain sources likesale of goods, Interest from bank deposits etc. He has to spend money on certain items like purchase of

goods, salary, rent etc. These activities take place during the normal course of his business. Business

transactions are numerous, that it is not possible to remember all those transactions and recall as to how the

money had been earned and spent. If he had noted down his incomes and expenses he can get the required

information easily. Hence it becomes necessary to record activities, which have monetary effect, in a clear,

and a systematic manner to get answers for the following questions

1. What has happened to his investment?

2. What is the result of the business transactions?

3. What are the earnings and expenses?

4.

How much amount is receivable from customers to whom goods have been sold on credit?5. How much amount is payable to suppliers on account of credit purchases?

6. What are the nature and value of assets possessed by the business concern?

7. What are the nature and value of liabilities of the business concern?

These and several other questions are answered with the help of accounting.

Accounting

Accounting is nothing but recording a set of business transaction in the books of accounts. Any financial

transaction or non-financial transaction like (cash or non cash) even depreciation, goodwill etc has to berecorded.

The purpose of accounting is to provide the information that is needed for sound economic decision

making. The main purpose of financial accounting is to prepare financial reports that provide information

about a firm's performance during a period to external parties such as investors, creditors, and tax

authorities and the financial position of the firm as on a particular date

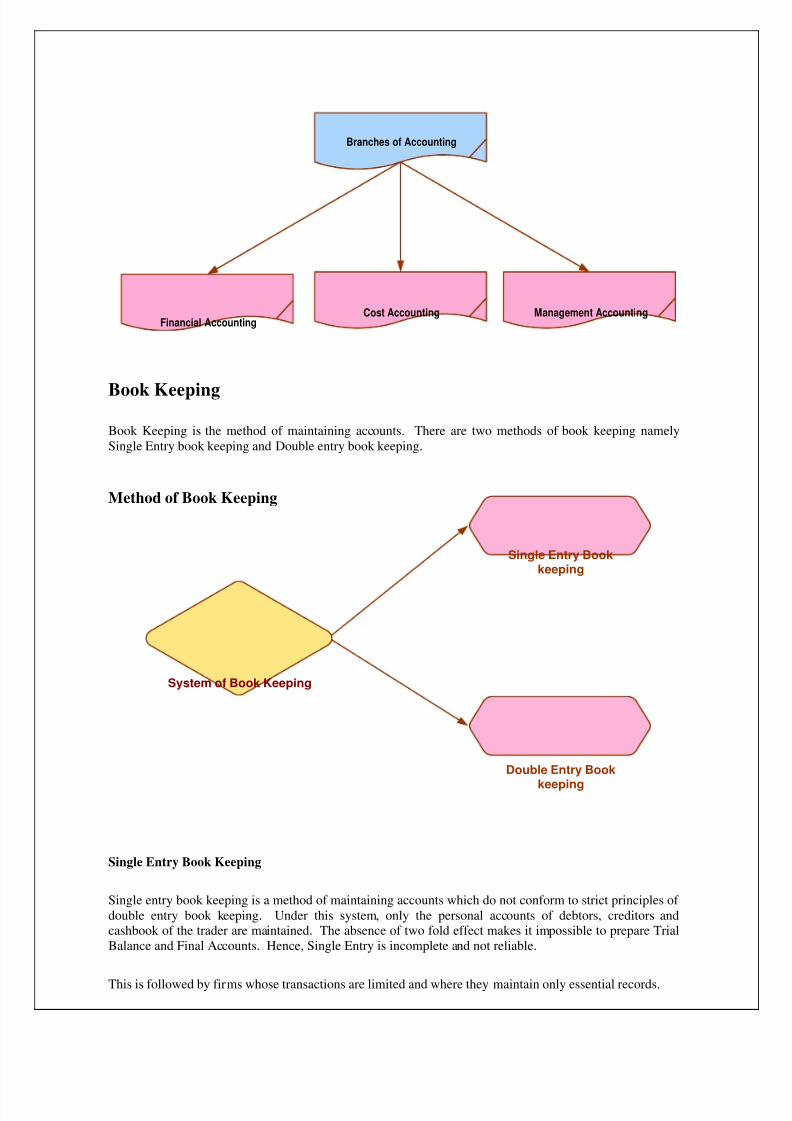

Branches of Accounting

Financial Accounting is concerned with recording of business transactions in the books of accounts insuch a way that operating result of a particular period and financial position on a particular date can be

known. It deals with preparation of financial statement like profit & loss account, balance sheet etc. which

is used by all types of companies.

Cost Accounting relates to collection, classification and ascertainment of the cost of production or jobundertaken by a firm. It is used by only manufacturing companies. This deals with preparation of various

cost based statements to fix the selling price for a product, break-even analysis, etc.

Management Accounting relates to the use of accounting data collected with the help of financial

accounting and cost accounting for the purpose of policy formulation, planning, control and decision

making by the management. Any type of company can use management Accounting. This deals with

preparation of various reports for the management based on which they take decisions.

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 3/10

Branches of Accounting

Cost Accounting Management AccountingFinancial Accounting

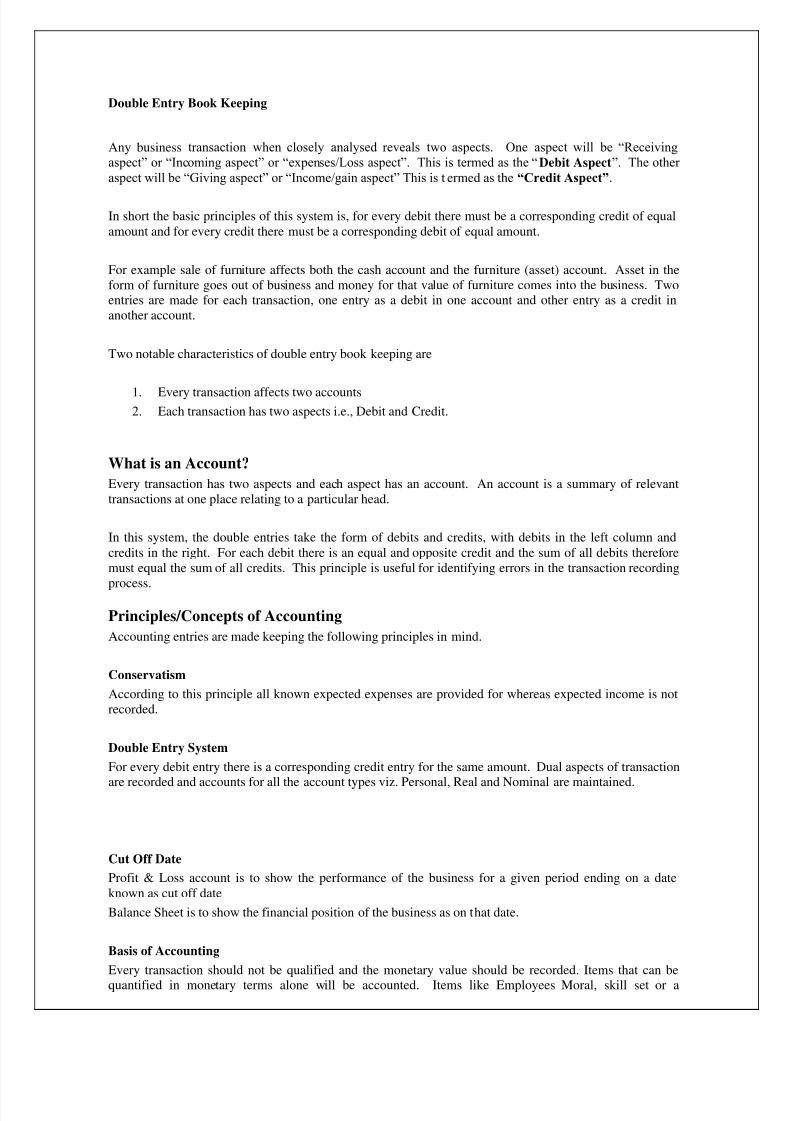

Book Keeping

Book Keeping is the method of maintaining accounts. There are two methods of book keeping namely

Single Entry book keeping and Double entry book keeping.

Method of Book Keeping

System of Book Keeping

Double Entry Book

keeping

Single Entry Bookkeeping

Single Entry Book Keeping

Single entry book keeping is a method of maintaining accounts which do not conform to strict principles of

double entry book keeping. Under this system, only the personal accounts of debtors, creditors andcashbook of the trader are maintained. The absence of two fold effect makes it impossible to prepare Trial

Balance and Final Accounts. Hence, Single Entry is incomplete and not reliable.

This is followed by firms whose transactions are limited and where they maintain only essential records.

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 4/10

Double Entry Book Keeping

Any business transaction when closely analysed reveals two aspects. One aspect will be “Receiving

aspect” or “Incoming aspect” or “expenses/Loss aspect”. This is termed as the “Debit Aspect”. The other

aspect will be “Giving aspect” or “Income/gain aspect” This is termed as the “Credit Aspect”.

In short the basic principles of this system is, for every debit there must be a corresponding credit of equal

amount and for every credit there must be a corresponding debit of equal amount.

For example sale of furniture affects both the cash account and the furniture (asset) account. Asset in the

form of furniture goes out of business and money for that value of furniture comes into the business. Twoentries are made for each transaction, one entry as a debit in one account and other entry as a credit in

another account.

Two notable characteristics of double entry book keeping are

1. Every transaction affects two accounts2. Each transaction has two aspects i.e., Debit and Credit.

What is an Account?

Every transaction has two aspects and each aspect has an account. An account is a summary of relevant

transactions at one place relating to a particular head.

In this system, the double entries take the form of debits and credits, with debits in the left column and

credits in the right. For each debit there is an equal and opposite credit and the sum of all debits therefore

must equal the sum of all credits. This principle is useful for identifying errors in the transaction recording

process.

Principles/Concepts of Accounting

Accounting entries are made keeping the following principles in mind.

Conservatism

According to this principle all known expected expenses are provided for whereas expected income is not

recorded.

Double Entry System

For every debit entry there is a corresponding credit entry for the same amount. Dual aspects of transaction

are recorded and accounts for all the account types viz. Personal, Real and Nominal are maintained.

Cut Off Date

Profit & Loss account is to show the performance of the business for a given period ending on a date

known as cut off date

Balance Sheet is to show the financial position of the business as on that date.

Basis of Accounting

Every transaction should not be qualified and the monetary value should be recorded. Items that can be

quantified in monetary terms alone will be accounted. Items like Employees Moral, skill set or a

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 5/10

company’s brand image, quality of management are not accounted (unless someone is prepared to paysomething for them)

Revenue Recognition

Revenue is both revenue income and revenue expenditure.

Eg. Claim provision is made on intimation date itself. Similarly for revenue income, premium has to berecognised on the date on which the coverage commences. Only at that time the revenue should be

recognized in the books of accounts. If policy issue date is 15, March 2005 and premium is collected on 15,

March 2003 and if the policy effective date is April 1, 2005 then this is the date on which the revenue has

to be recognised in the books of account.

Historical Data

Transaction should be recorded after it has happened.

Going Concern Concept

Assumed that the business will go on forever.

Ownership & Control Segregation

Owner and business are separate. Types of ownership are sole proprietor, partnership, private limited

company, public limited company, and co-operative society.

Any household or personal expenses paid from the business should not be debited as business expense, butit should be debited to the personal account

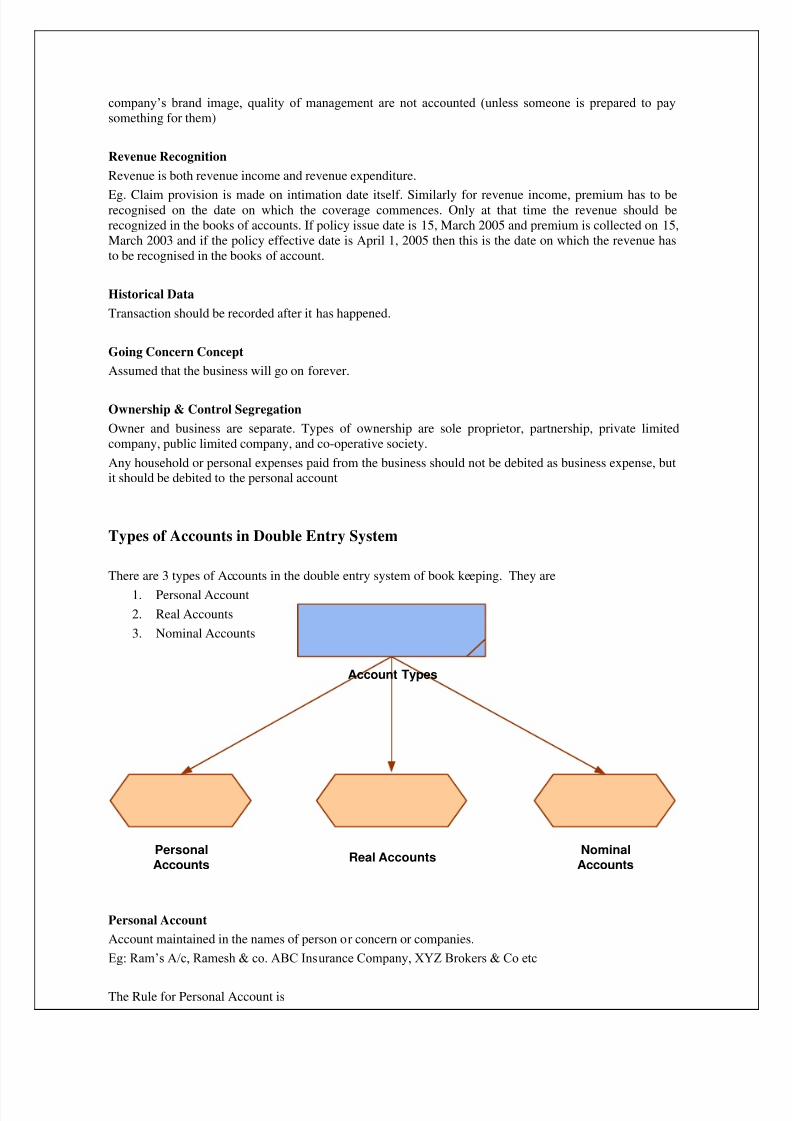

Types of Accounts in Double Entry System

There are 3 types of Accounts in the double entry system of book keeping. They are

1. Personal Account

2. Real Accounts

3. Nominal Accounts

Account Types

Personal

Accounts

Nominal

AccountsReal Accounts

Personal Account

Account maintained in the names of person or concern or companies.

Eg: Ram’s A/c, Ramesh & co. ABC Insurance Company, XYZ Brokers & Co etc

The Rule for Personal Account is

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 6/10

Debit the Receiver

Credit the Giver

Real Account

Asset Account (other than Personal Accounts) is classified as Real accounts.

Eg. Cash A/c, Bank A/c, Furniture A/c, Building & Machinery A/c

The Rule for Real Account

Debit what comes in

Credit what goes out

Nominal Account

Accounts maintained for Incomes, Expenses, Profits and Losses are classified as Nominal Accounts.

Eg. Salary A/c, Premium A/c, Dividend Account, Rent Account etc.

The Rule for Nominal Account

Debit all expenses and losses

Credit all incomes and gains

Some Important Accounting Documents

Journal

A Journal is a chronological listing of the firm’s transaction including the amounts, accounts that are

affected and whether the affected account is to be debited or credited. Journal is the primary book of

accounts from which the different accounts are debited or credited.

Ledger

Ledger is a principal or main book which contains all the accounts to which the transactions recorded in the

Journal are transferred / posted.

In Journal each transaction is recorded separately and it is not possible to know the net result of many

transactions pertaining to a particular account at a glance. A ledger is a book which contains all the

accounts whether personal, real or nominal. It is an account wise collection of transaction. So that tracking

of individual account balances becomes easier. After recording a transaction in the Journal it is then

transferred to the ledger. The process of transferring the debits and credits to the Ledger is called Posting.

Each Ledger Account will have Debit and Credit columns. Based on each transaction in journal, the ledger

account can have debit or credit or both entries. Both debit and credit columns will be totalled to find out

the net balance of the account.

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 7/10

Posting

The process of transferring the entries recorded in the journal or subsidiary books to the respective accounts

opened in the ledger is called posting. In other words, posting refers to grouping of all the transactions

relating to a particular account at one place.

It is necessary to post all the transactions into various accounts in the ledger because posting helps us to

know the net effect of various transactions during a given period on a particular account.

Cash Book

This is a ledger for cash transactions where the cash receipt are recorded on the debit side and cash

payments are recorded on the credit side.

Bank Book

This is a ledger where bank related transactions are posted. All the bank receipts are posted on the debit the

side and bank payments are posted on the credit side. Bank receipt refers to income by way of cheque and

Bank payment refers to any payment by way of cheque.

Trial Balance

The Trial balance is a listing of all Leger Account Balances, which can be a Debit or Credit Balance. The

total of all debit Balances should tally with the total of Credit balances. If it does not tally then there ismistake in posting/totalling/balancing the accounts

Such errors will come to light by preparing this trial balance.

Final Accounts

The businessman is interested in knowing whether the business has resulted in profit or loss and what is the

financial position of the business at a given date. In short he wants to know the profitability and thefinancial soundness of the business. This could be ascertained by preparing the final accounts.

Final accounts are prepared at the end of the year from the trial balance. The parts of final accounts are

1. Trading account

2. Manufacturing account

3. Revenue account in case of Insurance Companies

4. Profit and Loss account

5. Balance sheet

Trading AccountTrading means buying and selling. This account shows the results of buying and selling of goods. Gross

profit or Gross loss is ascertained by preparing Trading account. This is prepared by trading companies to

find out the trading profit/loss. Expenses include purchase, wages, etc. Income includes sales, closing stock

etc.

Manufacturing Account (For Manufacturing Concerns)

This is a statement prepared by manufacturing firms to find out at the end of the financial year whether they

have made a profit or loss. This is prepared taking into account only the income and expenses, which are

directly related to the manufacturing operations. It does not include income like interest from investment

and expenses like salary to permanent staff. It is prepared taking expenses like wages, materials,

manufacturing expenses like power, water etc and income include closing stock.

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 8/10

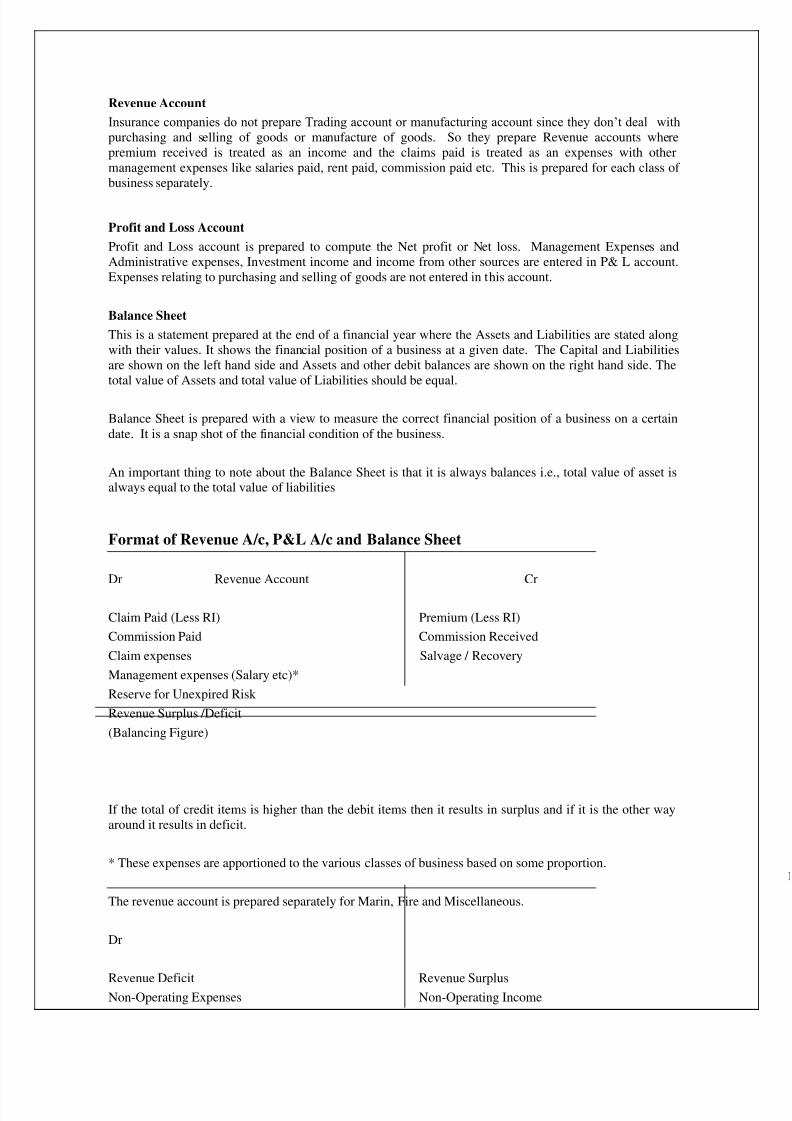

Revenue Account

Insurance companies do not prepare Trading account or manufacturing account since they don’t deal with

purchasing and selling of goods or manufacture of goods. So they prepare Revenue accounts where

premium received is treated as an income and the claims paid is treated as an expenses with other

management expenses like salaries paid, rent paid, commission paid etc. This is prepared for each class of

business separately.

Profit and Loss Account

Profit and Loss account is prepared to compute the Net profit or Net loss. Management Expenses and

Administrative expenses, Investment income and income from other sources are entered in P& L account.

Expenses relating to purchasing and selling of goods are not entered in this account.

Balance Sheet

This is a statement prepared at the end of a financial year where the Assets and Liabilities are stated along

with their values. It shows the financial position of a business at a given date. The Capital and Liabilities

are shown on the left hand side and Assets and other debit balances are shown on the right hand side. The

total value of Assets and total value of Liabilities should be equal.

Balance Sheet is prepared with a view to measure the correct financial position of a business on a certain

date. It is a snap shot of the financial condition of the business.

An important thing to note about the Balance Sheet is that it is always balances i.e., total value of asset isalways equal to the total value of liabilities

Format of Revenue A/c, P&L A/c and Balance Sheet

Dr Revenue Account Cr

Claim Paid (Less RI) Premium (Less RI)

Commission Paid Commission Received

Claim expenses Salvage / Recovery

Management expenses (Salary etc)*

Reserve for Unexpired Risk

Revenue Surplus /Deficit

(Balancing Figure)

If the total of credit items is higher than the debit items then it results in surplus and if it is the other way

around it results in deficit.

* These expenses are apportioned to the various classes of business based on some proportion.

The revenue account is prepared separately for Marin, Fire and Miscellaneous.

Dr

Revenue Deficit Revenue SurplusNon-Operating Expenses Non-Operating Income

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 9/10

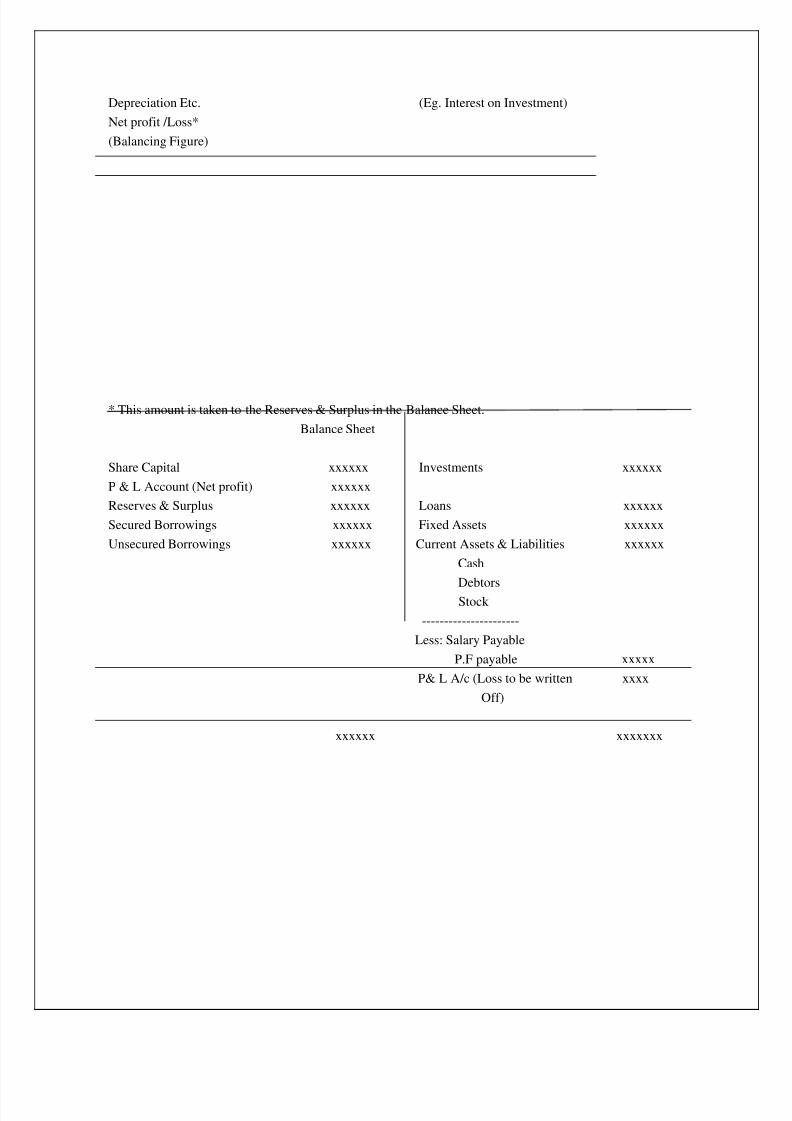

Depreciation Etc. (Eg. Interest on Investment)

Net profit /Loss*

(Balancing Figure)

* This amount is taken to the Reserves & Surplus in the Balance Sheet.

Balance Sheet

Share Capital xxxxxx Investments xxxxxx

P & L Account (Net profit) xxxxxx

Reserves & Surplus xxxxxx Loans xxxxxx

Secured Borrowings xxxxxx Fixed Assets xxxxxx

Unsecured Borrowings xxxxxx Current Assets & Liabilities xxxxxx

Cash

Debtors

Stock

----------------------

Less: Salary Payable

P.F payable xxxxx

P& L A/c (Loss to be written xxxx

Off)

xxxxxx xxxxxxx

8/3/2019 MEA Unit V

http://slidepdf.com/reader/full/mea-unit-v 10/10

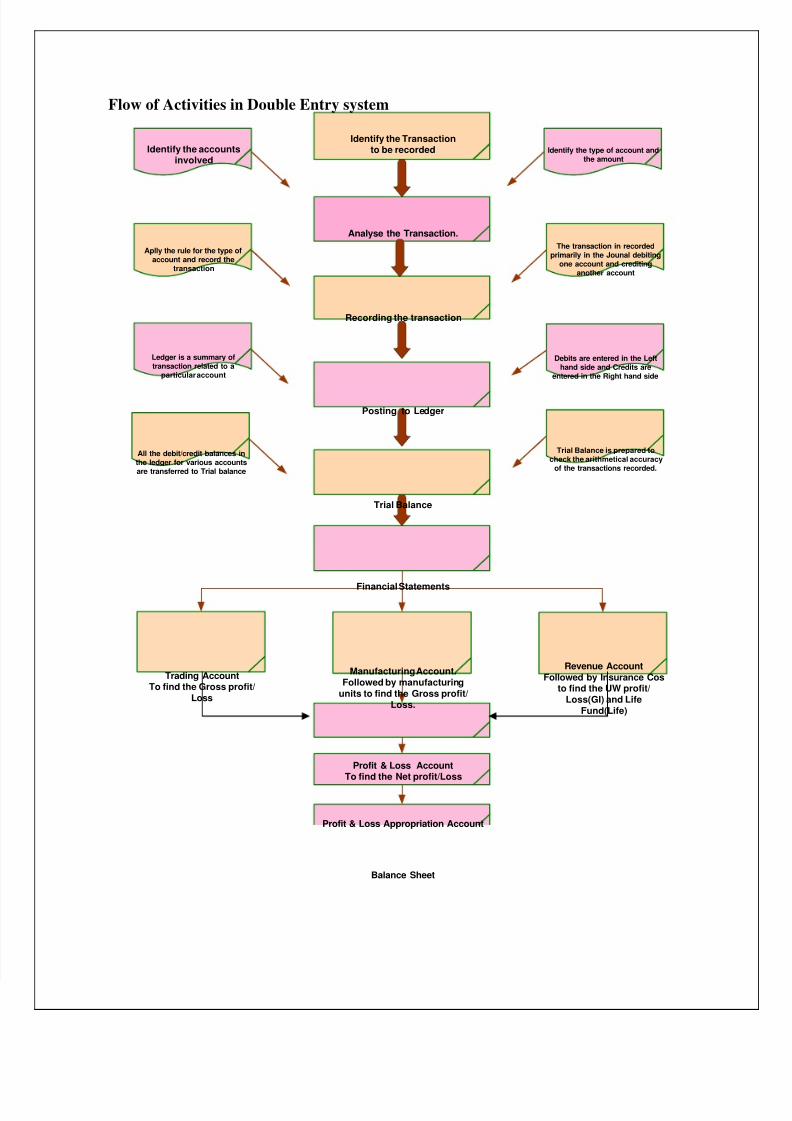

Flow of Activities in Double Entry system

Identify the Transactionto be recorded

Analyse the Transaction.

Identify the accountsinvolved

Identify the type of account andthe amount

Recording the transaction

Aplly the rule for the type ofaccount and record the

transaction

The transaction in recordedprimarily in the Jounal debiting

one account and creditinganother account

Posting to Ledger

Ledger is a summary oftransaction related to a

particular account

Debits are entered in the Lefthand side and Credits are

entered in the Right hand side

Trial Balance

All the debit/credit balances inthe ledger for various accountsare transferred to Trial balance

Trial Balance is prepared tocheck the arithmetical accuracy

of the transactions recorded.

Financial Statements

Trading AccountTo find the Gross profit/

Loss

Manufacturing Account.

Followed by manufacturing

units to find the Gross profit/

Loss.

Revenue Account

Followed by Insurance Costo find the UW profit/

Loss(GI) and Life

Fund(Life)

Profit & Loss AccountTo find the Net profit/Loss

Profit & Loss Appropriation Account

Balance Sheet