Innovatie door waardecreatie met leveranciers - Facto.nl 2010 - presentatie D1 innovatie... ·...

30

Ruimte voor eventueel een bedrijfslogo 22 juni 2010 Stroom A ‘Verbeter uw (interne) samenwerking’ | Workshop 1A STROOM D | WORKSHOP D1 Innovatie door waardecreatie met leveranciers Hans Dijkhuis, Procurement Manager, ASML Wouter Crul, Managing Director, Purspective

Transcript of Innovatie door waardecreatie met leveranciers - Facto.nl 2010 - presentatie D1 innovatie... ·...

Ruimte voor eventueel

een bedrijfslogo

22 juni 2010 Stroom A ‘Verbeter uw (interne) samenwerking’ | Workshop 1A

STROOM D | WORKSHOP D1

Innovatie door

waardecreatie met

leveranciers

Hans Dijkhuis, Procurement Manager, ASML

Wouter Crul, Managing Director, Purspective

www.purspective.com

Porter 5 forces (1979)

www.purspective.com

Kraljic Matrix (1983)

Balance

Balance

Leverage

products

Strategic

products

Routine

products

Bottleneck

products

Competitive

BiddingPer-

formance based

partnership

e-Procurement

solutions

Secure supply +

search for

alternatives

Low

Low High

High

Impact on

financial

results

Supply-risk

Balance of power in in purchasing portfolio

www.purspective.com

MSU model (1991)

DevelopCommodity/Article Group

Strategies

II

Integrate Suppliersinto the new Product/ProcessDev. Process

V

Integrate Suppliersinto the Order

FulfillmentProcess

VI

Establish andLeverage a world-class Supply Base

III

Insourcing/Outsourcing

I

Develop andManage Supplier

Relationships

IV

SupplierDevelopment

and QualityMgt

VII

Manage Costsstrategically acrossthe Supply Chain

VIII

critical integratedsupply chain processes

INTEGRATED,ALIGNED AND

GLOBAL

Source: Robert.M. Monczka, Ph.D.

DeployGlobalization

III

Establish globallyintegrated and alignedpurchasing and supply

chain Strategies + Plans

I

Develop Organization and

Teaming strategies

II

Develop purchasing and supply chain Measurements

IV

Establish HumanResource develop-ment and training

VI

VDevelop and

implement enablingIS / IT systems

INTEGRATED,ALIGNED AND

GLOBAL

Source: Robert.M. Monczka, Ph.D.

www.purspective.com

The Purchasing Czar (1992-93)

www.purspective.com

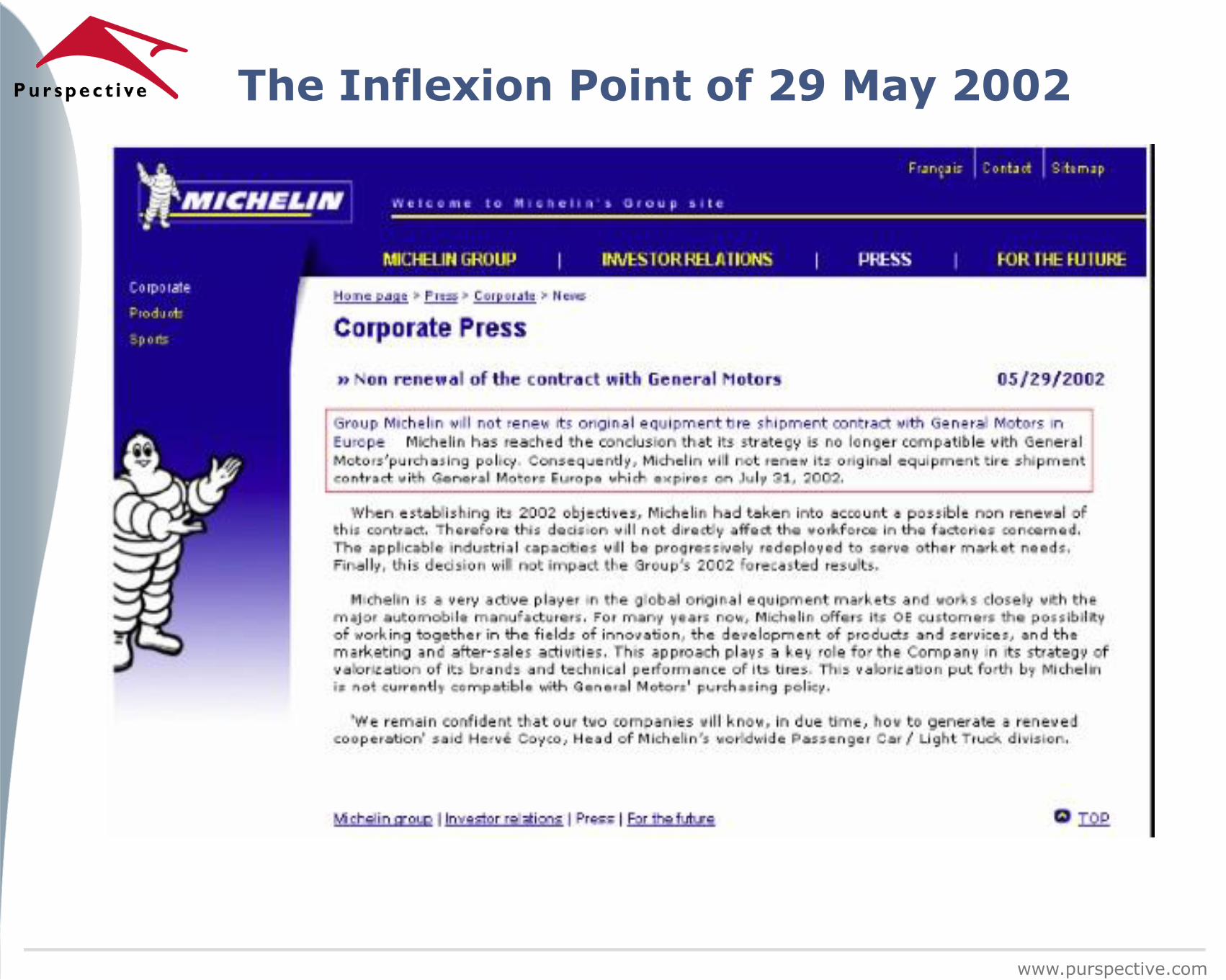

The Inflexion Point of 29 May 2002

www.purspective.com

2003 Attractivity & SRM

www.purspective.com

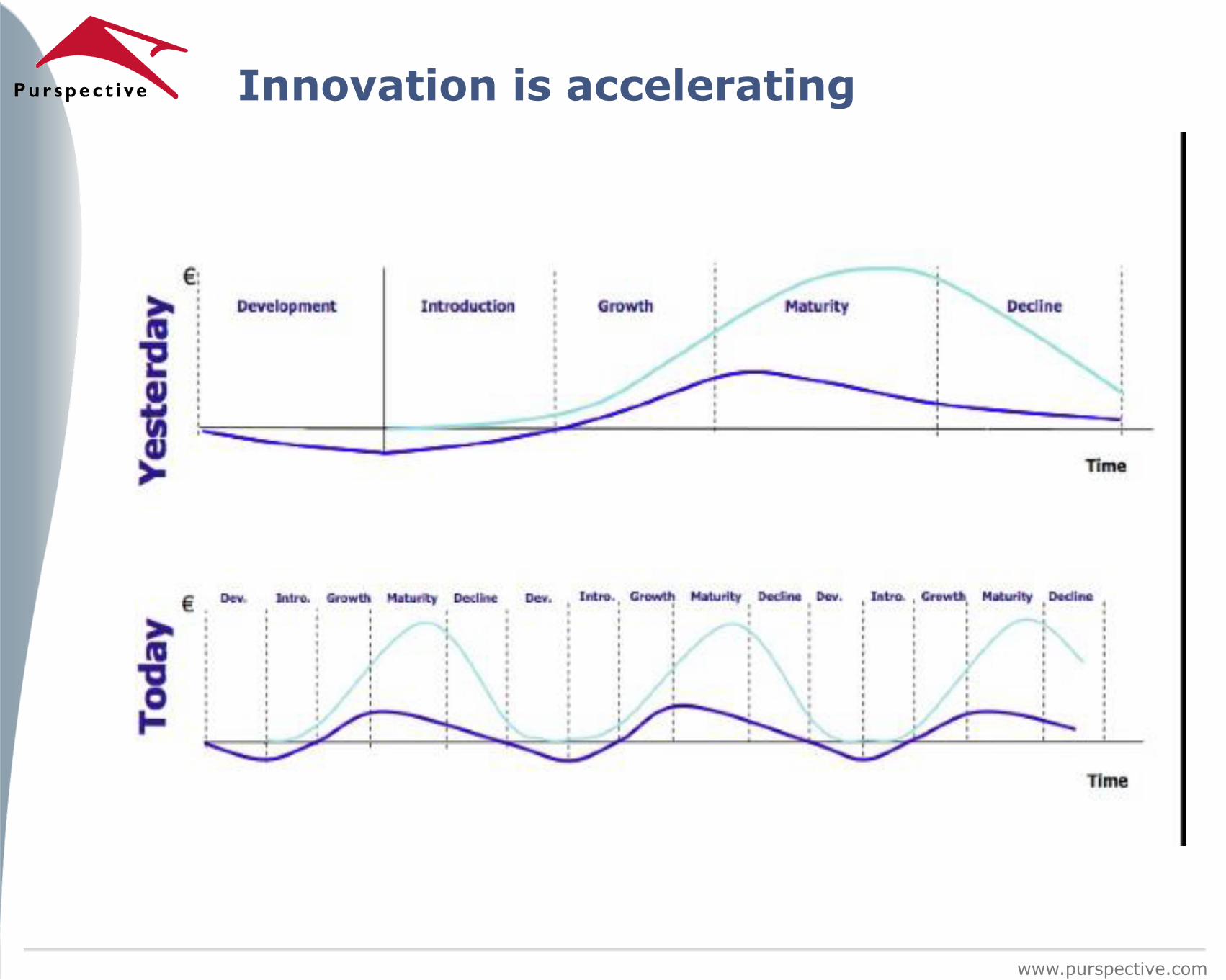

Innovation is accelerating

www.purspective.com

The Gillette example

www.purspective.com

Gillette Fusion Power Phantom Razor (2007)

/ Slide 11

Importance for a strategically aligned supply base

Hans Dijkhuis

Director SPRC Process Methodology

June 22nd, 2010

Nevi June 22nd, 2010/ Slide 12

Chips have many forms and functions

“I won’t even try to predict what things will be important 25 years from now,

but I bet we’ll have enabled some of them”

Martin van den Brink, Executive Vice President of Marketing and Technology

Freefloating sensors(Holst Centre)

MRAM (Magnetic RAM)

Micromirrors for beamers (TI) Accelerometer in

the iPhone (Apple)

Gyroscope ( UC Irvine)

40Watt Energy Harvester (IMEC)

Accelerometer ( IC Mechanics)

DNA analysis (Affymetrix)

Lab on a Chip (LOC) for counting red blood cells

Camera pill with camera, transmitter and computer

QuadCore Microprocessor(AMD)

64 Gbit memory(Samsung)

Harddisk read/write head (Western Digital)

Nevi June 22nd, 2010/ Slide 13

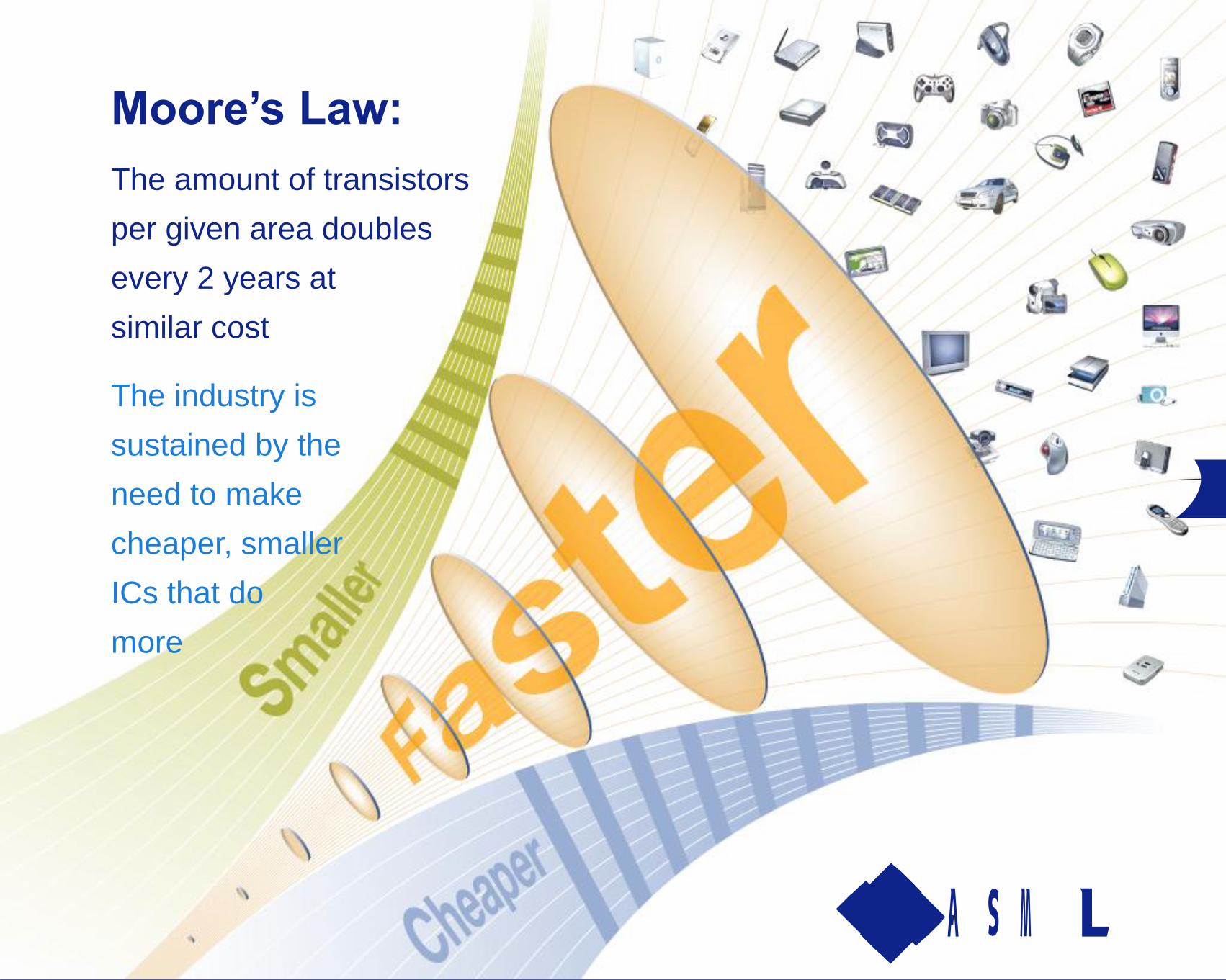

Moore’s Law:

The amount of transistors

per given area doubles

every 2 years at

similar cost

The industry is

sustained by the

need to make

cheaper, smaller

ICs that do

more

Nevi June 22nd, 2010/ Slide 14

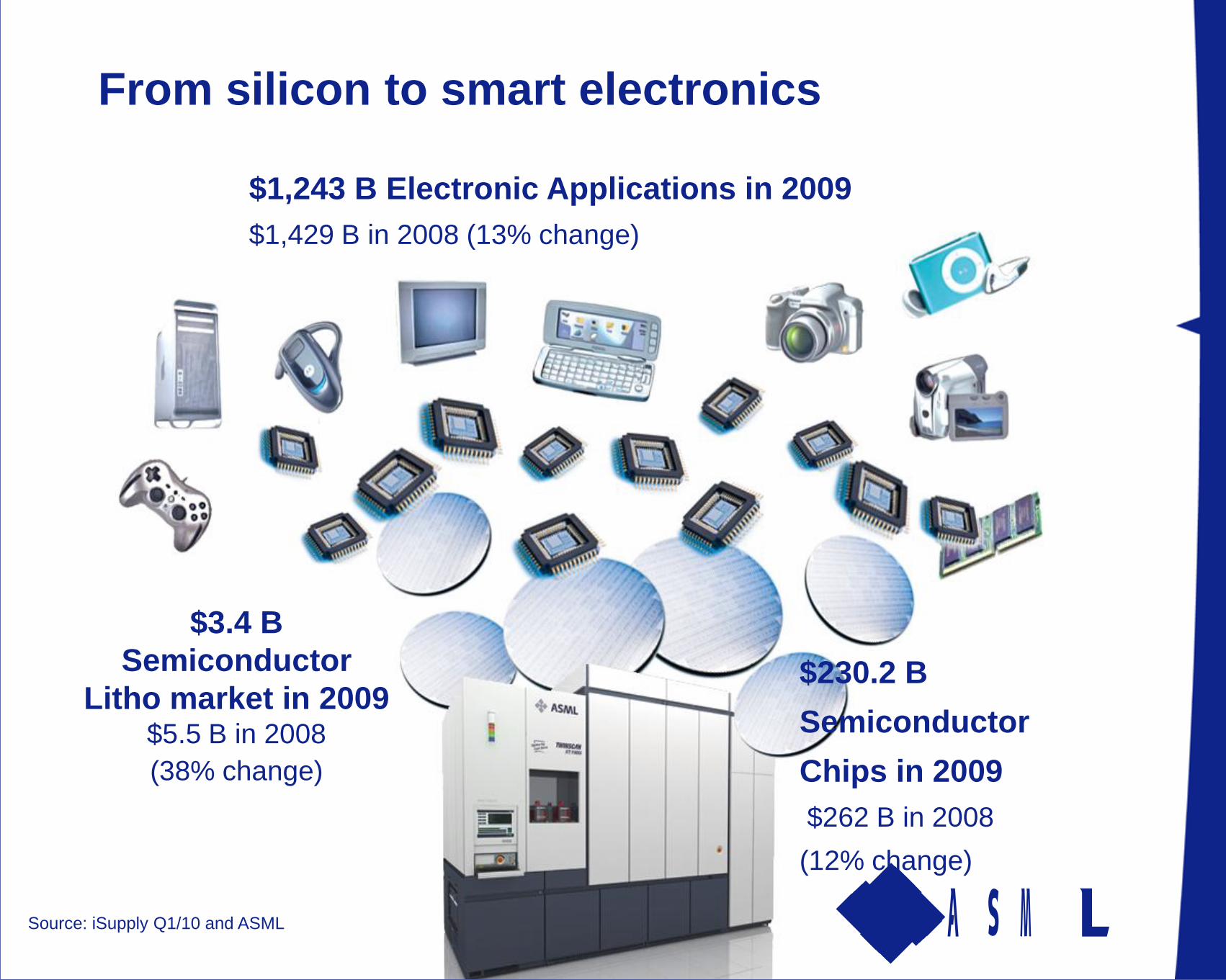

$230.2 B

Semiconductor

Chips in 2009

$262 B in 2008

(12% change)

$1,243 B Electronic Applications in 2009

$1,429 B in 2008 (13% change)

$3.4 B

Semiconductor

Litho market in 2009$5.5 B in 2008

(38% change)

Source: iSupply Q1/10 and ASML

From silicon to smart electronics

Nevi June 22nd, 2010/ Slide 15

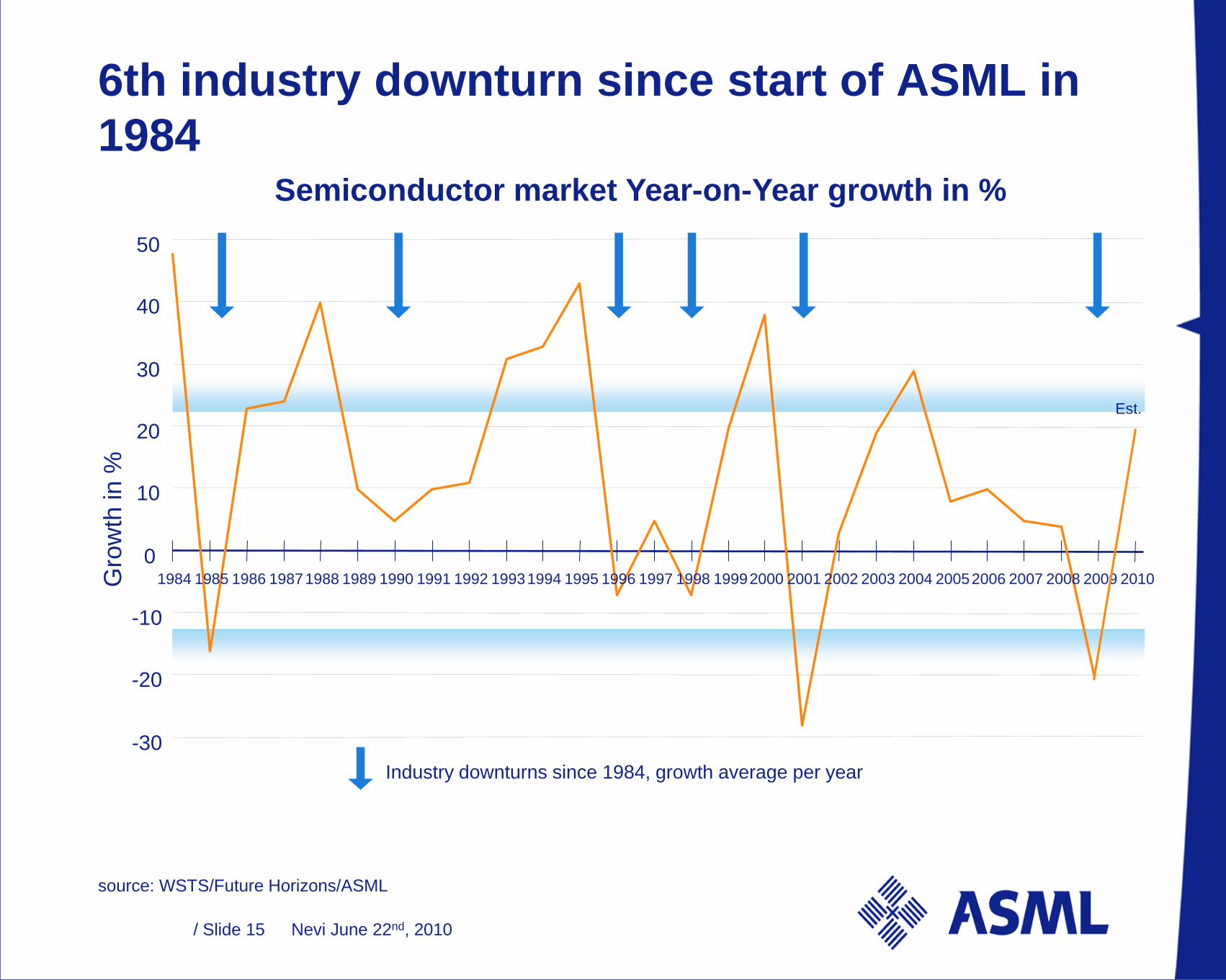

6th industry downturn since start of ASML in

1984

source: WSTS/Future Horizons/ASML

Semiconductor market Year-on-Year growth in %

-30

-20

-10

0

10

20

30

40

50

1984 1985 1986 19871988 1989 1990 1991 1992 19931994 1995 1996 1997 1998 19992000 2001 2002 2003 2004 20052006 2007 2008 2009Gro

wth

in %

Industry downturns since 1984, growth average per year

2010

Est.

Nevi June 22nd, 2010/ Slide 16

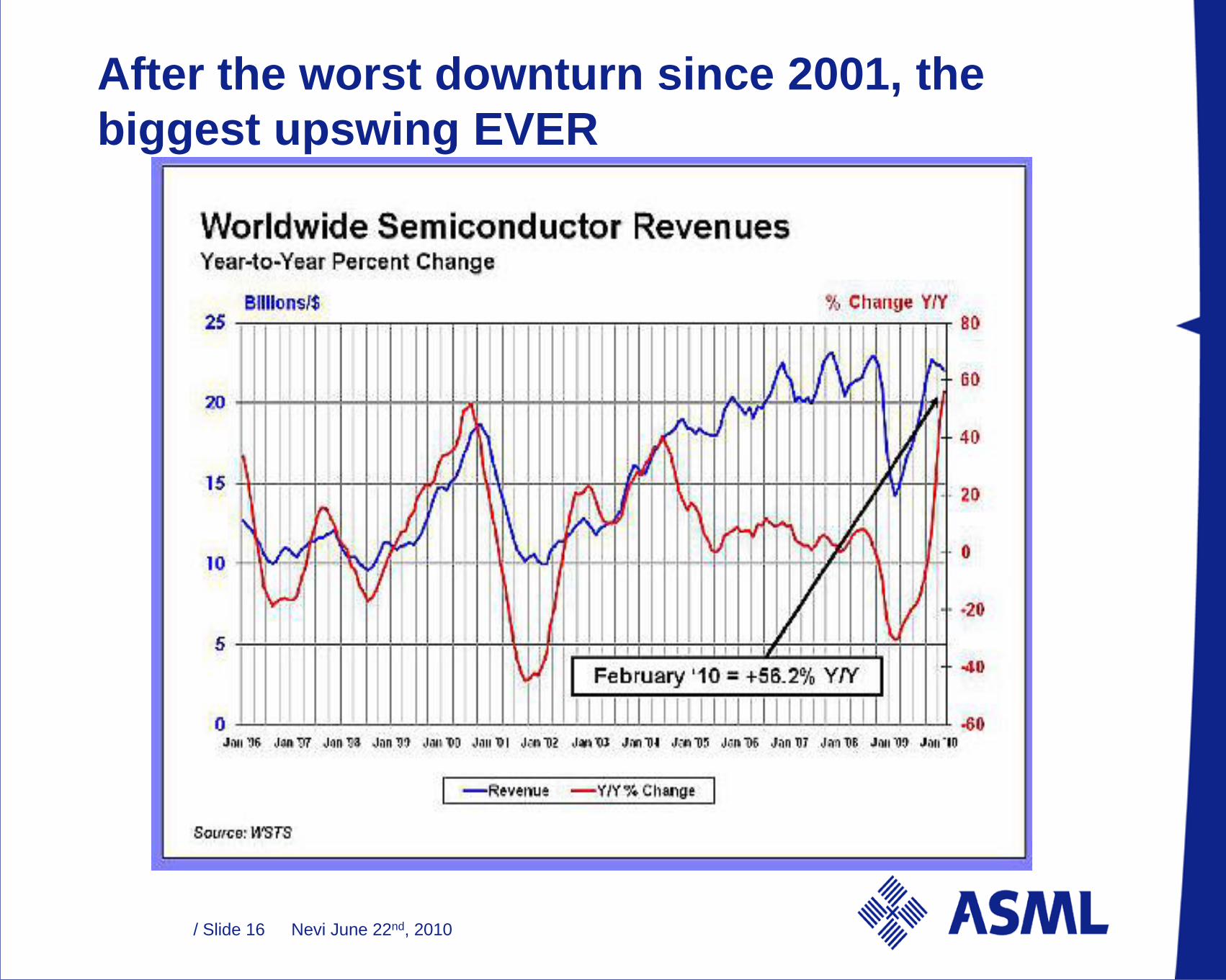

After the worst downturn since 2001, the

biggest upswing EVER

Nevi June 22nd, 2010/ Slide 17

Total net sales M€

Numbers have been rounded for readers’ convenience.

1,543

2,465 2,529

3,5823,768

2,954

1,596

318 453685 629

949 919

184

329

616

763 942

930844

277

370

611

533

958

934

697

555

526

785548

1053

955

494

581

742

950

est.

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2003 2004 2005 2006 2007 2008 2009 2010

guidance

Net sale

s

Q4

Q3

Q2

Q1

Nevi June 22nd, 2010/ Slide 18

January 2009

and for scenario’s for the coming years:

Nevi June 22nd, 2010/ Slide 19

Source: ASML Marketing (Q1/09)

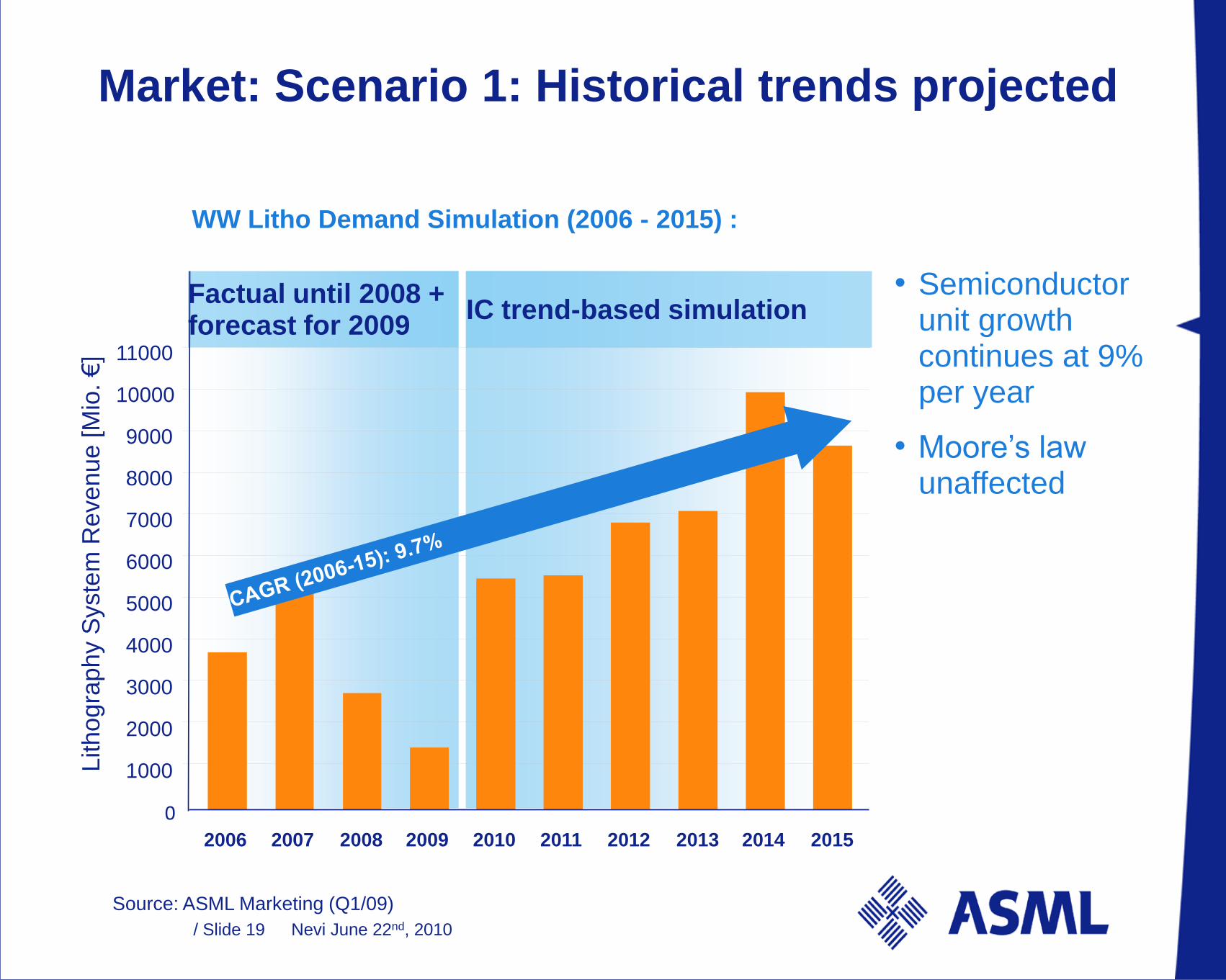

Market: Scenario 1: Historical trends projected

Factual until 2008 + forecast for 2009

IC trend-based simulation

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WW Litho Demand Simulation (2006 - 2015) :

Lith

og

rap

hy S

yste

m R

eve

nu

e [M

io.

€]

• Semiconductor unit growth continues at 9% per year

• Moore’s law unaffected

Nevi June 22nd, 2010/ Slide 20

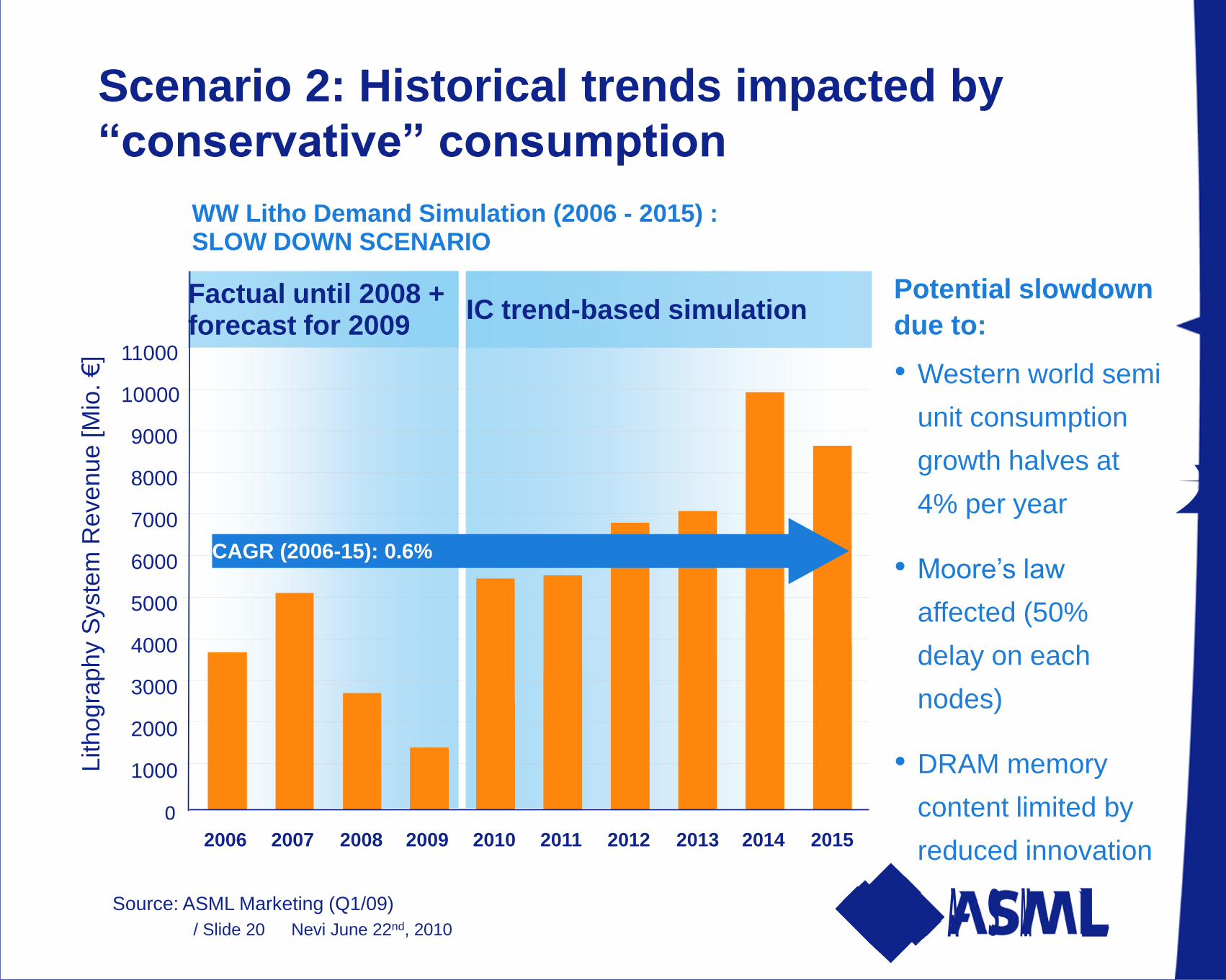

Scenario 2: Historical trends impacted by

“conservative” consumption

Factual until 2008 + forecast for 2009

IC trend-based simulation

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WW Litho Demand Simulation (2006 - 2015) : SLOW DOWN SCENARIO

Lith

og

rap

hy S

yste

m R

eve

nu

e [M

io.

€]

CAGR (2006-15): 0.6%

Potential slowdown

due to:

• Western world semi

unit consumption

growth halves at

4% per year

• Moore’s law

affected (50%

delay on each

nodes)

• DRAM memory

content limited by

reduced innovation

Source: ASML Marketing (Q1/09)

Nevi June 22nd, 2010/ Slide 21

Bottom-up scenario: Four engines of growthEven when assuming slow chip unit growth of 4%

More DRAM

in expanding

consumer

electronics.

Additional

€1.2B Litho

revenue over

6 years.

Emerging new Storage Class

Memory makes computer

servers perform 25% better,

leading to 30% penetration by

2015, adding €1.8B Litho

revenue in 2012-2015 period.

Middle class population growth

expected, driven by Brazil,

Russia, India and China (BRIC).

Electronics spending in BRIC to

more than double to $46/year,

adding €6.4B in Litho revenue

over 6 years.

NAND/ReRAM

penetration rises to

10% of hard disk

drives storage

capacity, versus 7%

in slow-down

scenario, adding

€6.8B in Litho

revenue over 6

years.

Nevi June 22nd, 2010/ Slide 22

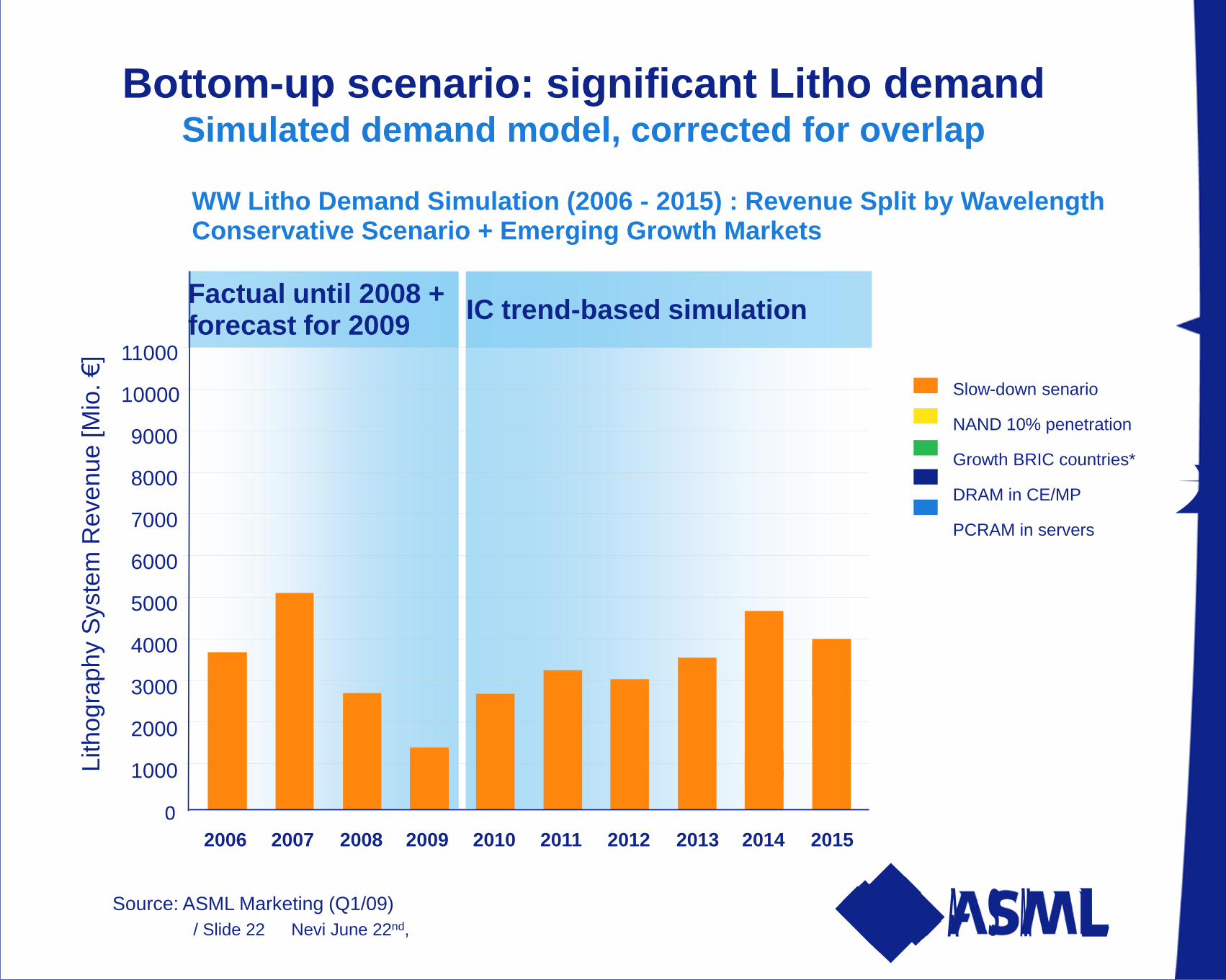

Bottom-up scenario: significant Litho demandSimulated demand model, corrected for overlap

Factual until 2008 + forecast for 2009

IC trend-based simulation

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WW Litho Demand Simulation (2006 - 2015) : Revenue Split by WavelengthConservative Scenario + Emerging Growth Markets

Lith

og

rap

hy S

yste

m R

eve

nu

e [M

io.

€]

Slow-down senario

NAND 10% penetration

Growth BRIC countries*

DRAM in CE/MP

PCRAM in servers

Source: ASML Marketing (Q1/09)

Nevi June 22nd, 2010/ Slide 23

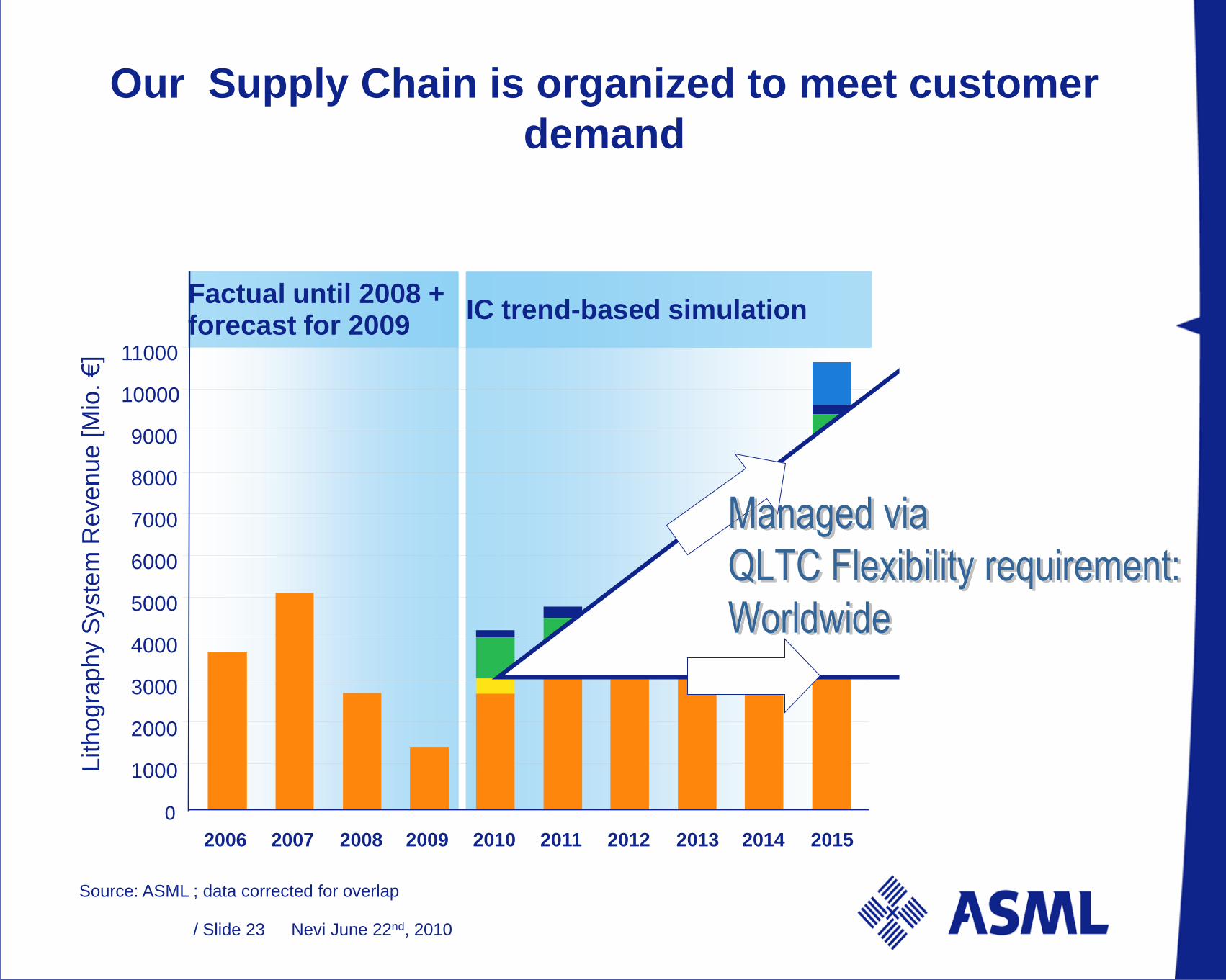

Source: ASML ; data corrected for overlap

Factual until 2008 + forecast for 2009

IC trend-based simulation

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Lith

og

rap

hy S

yste

m R

eve

nu

e [M

io.

€]

Our Supply Chain is organized to meet customer

demand

/ Slide 24

Value Sourcing

Nevi June 22nd, 2010/ Slide 25

ASML Sourcing Model: Value SourcingAdding Value to the Customer, the Supply Base &

ASML

l ASML Customer acceptance by the Supply Chain

l Long Term supplier relationships

l QLTC Performance in all phases of the life cycle:

l managed intergral and cross functional

l measured

l Continuously improved

l Securing World Wide competitiveness

l Continuously adapting to changing customer requirements

Nevi June 22nd, 2010/ Slide 26

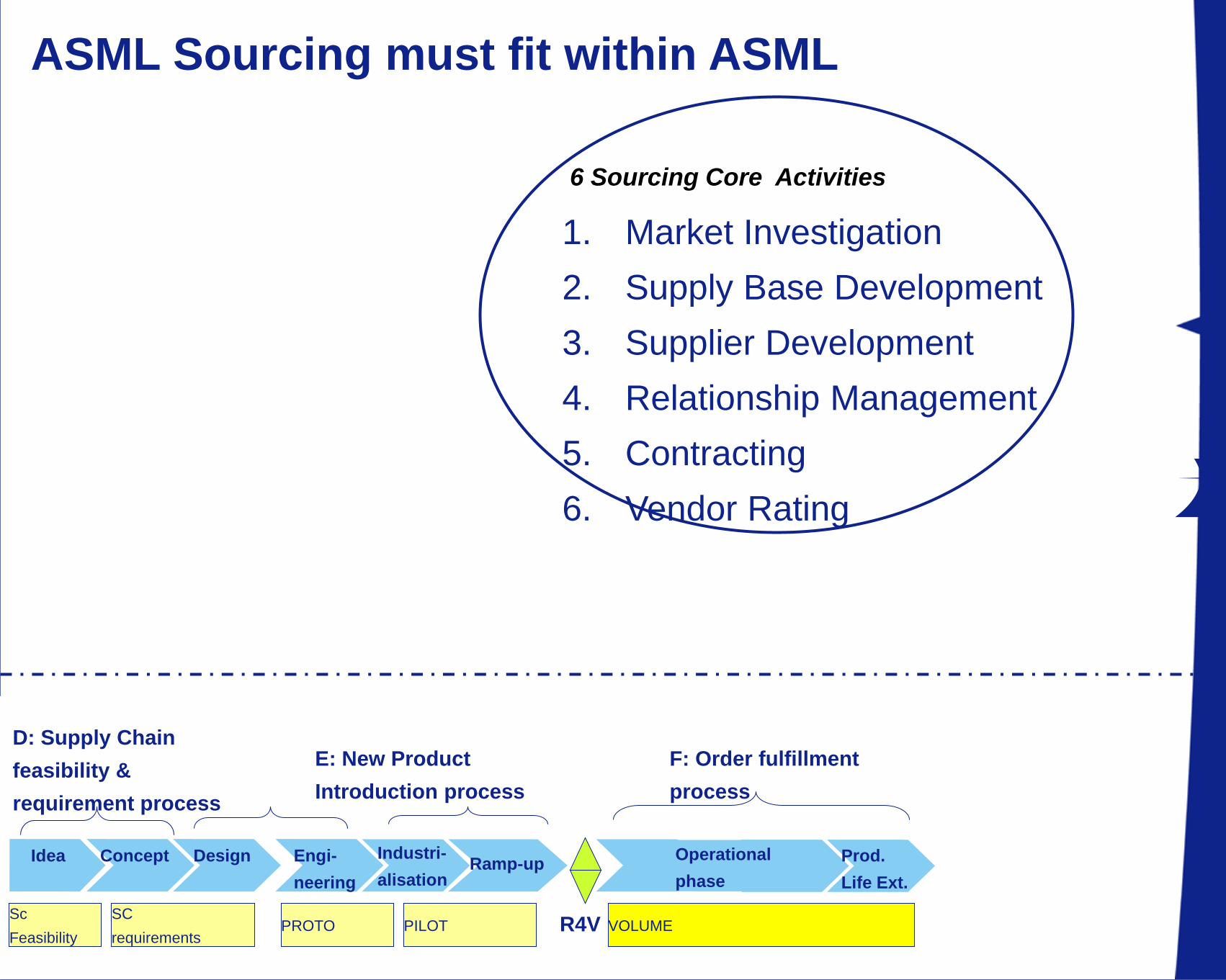

ASML Sourcing must fit within ASML

1. Market Investigation

2. Supply Base Development

3. Supplier Development

4. Relationship Management

5. Contracting

6. Vendor Rating

6 Sourcing Core Activities

D: Supply Chain

feasibility &

requirement process

F: Order fulfillment

process

E: New Product

Introduction process

PROTO PILOT VOLUMESC

requirements

Sc

Feasibility

Idea Concept Operational

phaseRamp-up

Industri-

alisation

Engi-

neering

Design Prod.

Life Ext.

R4V

Nevi June 22nd, 2010/ Slide 27

Supplier

Supplier

Supplier

Supplier

OPERATIONAL

TACTICAL

STRATEGIC

A: Preferred supplier

management process

Value Sourcing model: Supply Chain Processes are aligned with ASML

D: Supply Chain

feasibility &

requirement process

ASML Technology Roadmap

F: Order fulfillment

process

E: New Product

Introduction process

•ASMLCustomer

Market characteristics

Product Market

characteristics

SATC: Supplier performance

control process

B: Supplier strategic

alignment process

SPFT

PROTO PILOT VOLUMESC

requirements

Sc

Feasibility

Idea Concept Operational

phaseRamp-up

Industri-

alisation

Engi-

neering

Design Prod.

Life Ext.

R4V

•ASMLBusiness

strategy

Nevi June 22nd, 2010/ Slide 28

Supplier

Supplier

Supplier

Supplier

OPERATIONAL

TACTICAL

STRATEGIC

Value Sourcing model: 6 Core activities of procurement

D: Supply Chain

feasibility &

requirement process

ASML Technology Roadmap

F: Order fulfillment

process

E: New Product

Introduction process

SAT

SPFT

PROTO PILOT VOLUMESC

requirements

Sc

Feasibility

Idea Concept Operational

phaseRamp-up

Industri-

alisation

Engi-

neering

Design Prod.

Life Ext.

R4V

Nevi June 22nd, 2010/ Slide 29

Commitment to QLTC

Ruimte voor eventueel

een bedrijfslogo

22 juni 2010 Stroom A ‘Verbeter uw (interne) samenwerking’ | Workshop 1A

Bedankt voor uw

aandacht!