6) LBO

21

6) Going Private and L everaged Buyouts ( LB O)

Transcript of 6) LBO

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 1/21

6) Going Private and

Leveraged Buyouts (LBO)

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 2/21

Introduction

• Going private — transformation of a publiccorporation into a privately held rm

• Leverage buyout (LBO) — purchase of a

company by a small group of investorsusing a high percentage of debt nancing – Investors are outside nancial group or

managers or e!ecutives of company

–

"anagement buyout ("BO) — leveragedbuyout performed mainly by managers ore!ecutives of the company

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 3/21

– #esults in signicant increase of e$uity

share o%nership by managers – &urnaround in performance is usually

associated %ith formation of LBO

– &ypical LBO operation• 'inancial buyer purchases company using

high level of debt nancing

• 'inancial buyer replaces top management

• e% management maes operating

improvements

• 'inancial buyer maes public o*ering ofimproved company at higher price thanoriginally purchased

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 4/21

•

Buyout group may includeincumbent management and maybe associated %ith – Buyout specialists+ e,g,+ -ohlberg

-ravis #oberts . /o, (--#)

– Investment baners

– /ommercial baners

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 5/21

• "anagement buyouts ("BOs) – Investor group dominated by

incumbent management

– 0egment ac$uired from parent

company• LBO transaction may be reversed

%ith future public o*ering –

1im is to increase protability ofcompany and thereby increase maretvalue of rm

– Buyout group sees to harvest gain

%ithin three2 to ve2year period

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 6/21

• 3lements of a typical LBO operation – 'irst stage — raise cash re$uired for

buyout and devise managementincentive systems• 'inancing

– 1bout 45 of cash is put up by investor groupheaded by company7s top managers and8orbuyout specialist

– 1bout 95265 of re$uired cash through securedban loans

–

#est of cash by issuing senior and :uniorsubordinated debt

» Private placement %ith pension funds+insurance companies+ venture capital rms

» Public o*erings of ;high2yield; notes or bonds

(:un bonds)

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 7/21

• "anagement incentives – "anagers receive stoc price2based incentive

compensation in form of stoc options or%arrants

– Incentive compensation plans based onmeasures such as operating performance

–

0econd stage — organi<ing sponsorgroup taes company private• 0toc2purchase — buys all outstanding

shares of company

•

1sset2purchase — purchases all assets ofcompany and forms ne% privately heldcorporation

• e% o%ners sell o* parts of ac$uired rmto reduce debt

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 8/21

– &hird stage — management strives toincrease prots and cash =o%s• /ut operating costs

• /ut spending in research and development

• /ut ne% plants and e$uipment as long asprovisions for capital e!penditures areade$uate and satisfy lenders

• Increase revenues by changing mareting

strategies

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 9/21

– 'ourth stage — reverse LBOs• Investor group may tae improved

company public again through public e$uityo*ering (secondary initial public o*ering 20IPO)

• /reate li$uidity for e!isting stocholders• "uscarella and >etsuypens (4??5)

– @A reverse LBOs in 4?@624?@

– 6 of rms use o*ering proceeds to lo%er

company7s leverage – 3$uity participants reali<ed median annuali<ed

rate of return of A6,C on e$uity investment bytime of 0IPO

– "edian length of time bet%een LBO and 0IPO

%as A? months

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 10/21

• /onditions and circumstances of

going2private buyouts in the 4?5s – &ypical target industries

• Basic+ nonregulated industries – Predictable and8or lo% nancing re$uirements

– Predictable8stable earnings

• Digh2tech industry less appropriate – 0horter history of protability

– Greater business ris

– 'e%er leveragable assets – /ommand high P83 multiples %ell above boo

value

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 11/21

•

Lehn and Poulsen (4?) – Dalf of 45 LBOs during 4?524?C %ere in

ve industriesE

» #etailing

» &e!tiles

» 'ood processing» 1pparel

» 0oft drins

– /onsumer nondurable goods

» Lo% income elasticity of demand

» 0ales =uctuate less %ith GP

– "ature industry %ith limited gro%thopportunities

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 12/21

– Other target characteristics• &rac record of capable management

• 0trong maret position %ithin industry toenable it to %ithstand economic=uctuations and competition

• Dighly li$uid balance sheet – Little debt+ either short or long term

– Large unencumbered asset base — forcollateral

– Digh proportion of tangible assets %ith fairmaret value above net boo value

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 13/21

– Leverage factors•

Increase return on e$uity (#O3) and cash=o%s to retire debt

• 1ttractions for lenders – Interest rates only F29 points above prime rate

– /ompany and collateral characteristics

» Large amounts of cash8cash e$uivalents

» ndervalued assets (hidden e$uity)

» /ould li$uidate some subsidiaries to raisefunds

–

Digh prospective rates of return on e$uityespecially for lenders such as venture capitalistsand insurance companies %ith e$uityparticipation

– /ondence in management group spearheading

LBO

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 14/21

– "anagement factors•

#ecord of capability• Betting reputation and personal %ealth on

success of LBO

• Dighly motivated by potential large

personal gains from stoc o%nership – 0ources of "BO targets

• Hivestitures of divisions by publiccompanies

• Private companies %ith lo% gro%threcords

• Public corporations selling at lo% P83multiples representing large discounts

from boo values

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 15/21

• 0ources of gains in LBOs –

&a! benets — can enhance alreadyviable transaction• 0pecic ta! benets

– Interest ta! shelter from high leverage

– 1sset step2up provides higher asset value fordepreciation e!penses especially accelerateddepreciation on assets involving little recapture —more diJcult under &a! #eform 1ct of 4?6

– &a! advantages of using 30OP as LBO vehicle

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 16/21

– "anagement incentives and agencycost e*ects• Increased o%nership stae provides

increased incentives for improvedperformance

– Protable investments that re$uire

disproportionate e*ort of managers may only beundertaen if managers are givendisproportionate share of prots

– /oncentrated o%nership aligns managers andshareholders7 interest+ reducing agency costs

–

Hebt from LBO commits cash =o%s to debtpayment+ reducing agency costs of free cash=o%s

– Hebt puts pressure on managers to improverm performance to avoid banruptcy

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 17/21

– Kealth transfer e*ects• Payment of premiums in LBO transactions

may represent %ealth transfer toshareholders from other staeholders

• Kealth transfer from e!isting bondholdersand preferred stocholders

–

#eduction in value of rm7s outstanding bondsand preferred stoc due to

» Large increase in debt

» Bond covenants may not protect e!istingbondholders in event of control changes and

debt issue» In banruptcy proceedings+ ;absolute priority

rule; for senior security may not be strictlyfollo%ed

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 18/21

• Kealth transfer from current employees tone% investors

– "anagement turnover in buyout rms lo%erthan in average rm sometimes ne%management team is brought in after LBO

– umber of employees gro%s more slo%ly in LBOrm than others in same industry andsometimes even decreases — may result frompost buyout divestitures and more eJcient useof labor

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 19/21

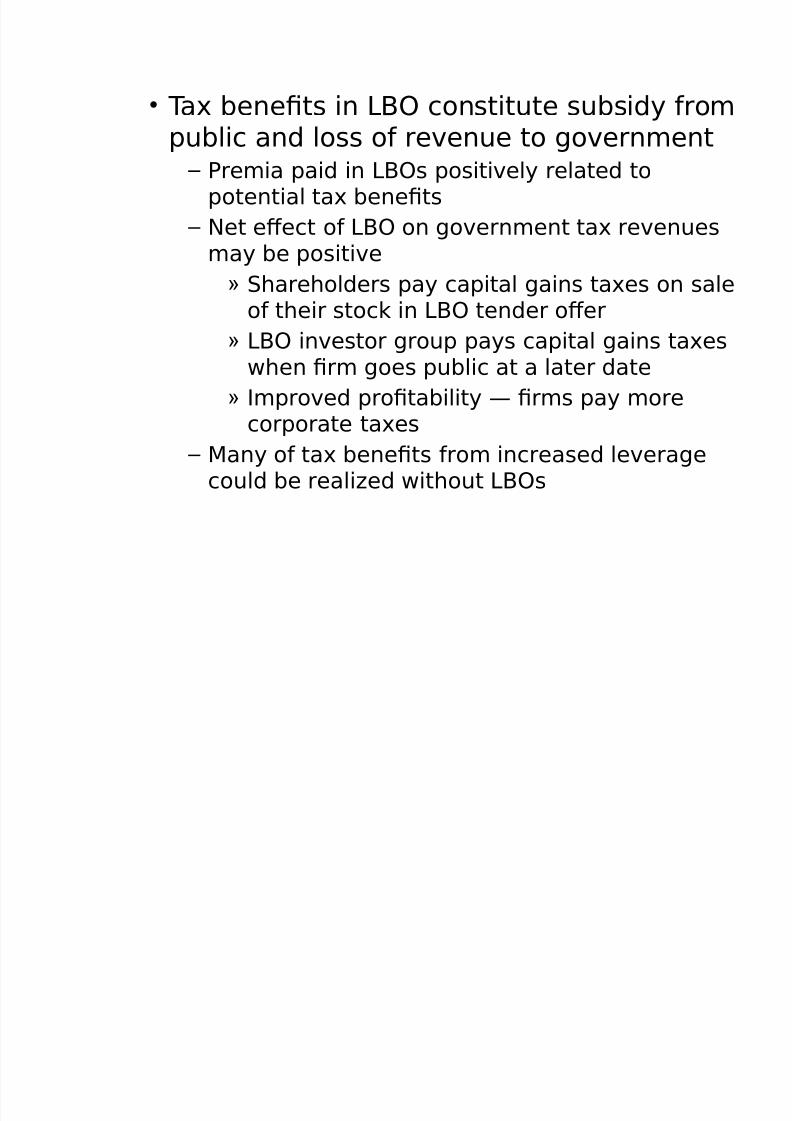

• &a! benets in LBO constitute subsidy from

public and loss of revenue to government – Premia paid in LBOs positively related to

potential ta! benets

– et e*ect of LBO on government ta! revenuesmay be positive

» 0hareholders pay capital gains ta!es on saleof their stoc in LBO tender o*er

» LBO investor group pays capital gains ta!es%hen rm goes public at a later date

» Improved protability — rms pay more

corporate ta!es

– "any of ta! benets from increased leveragecould be reali<ed %ithout LBOs

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 20/21

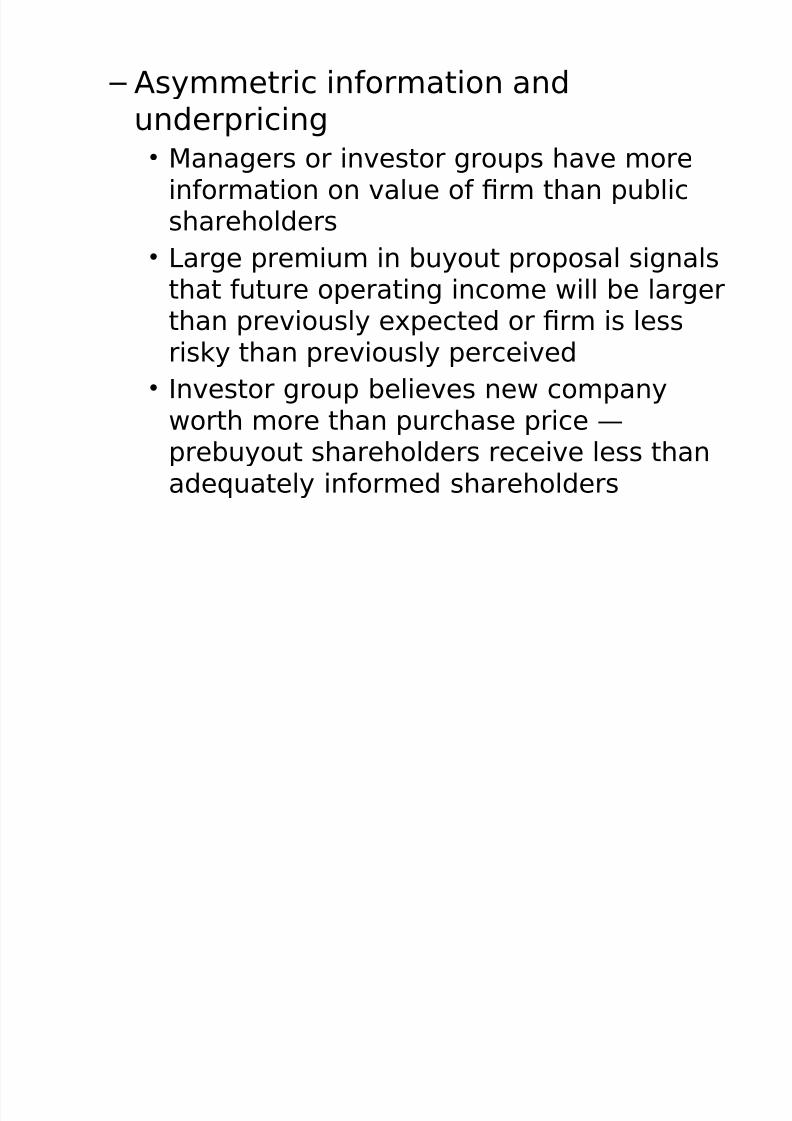

– 1symmetric information andunderpricing• "anagers or investor groups have more

information on value of rm than publicshareholders

• Large premium in buyout proposal signalsthat future operating income %ill be largerthan previously e!pected or rm is lessrisy than previously perceived

• Investor group believes ne% company

%orth more than purchase price —prebuyout shareholders receive less thanade$uately informed shareholders

8/20/2019 6) LBO

http://slidepdf.com/reader/full/6-lbo 21/21

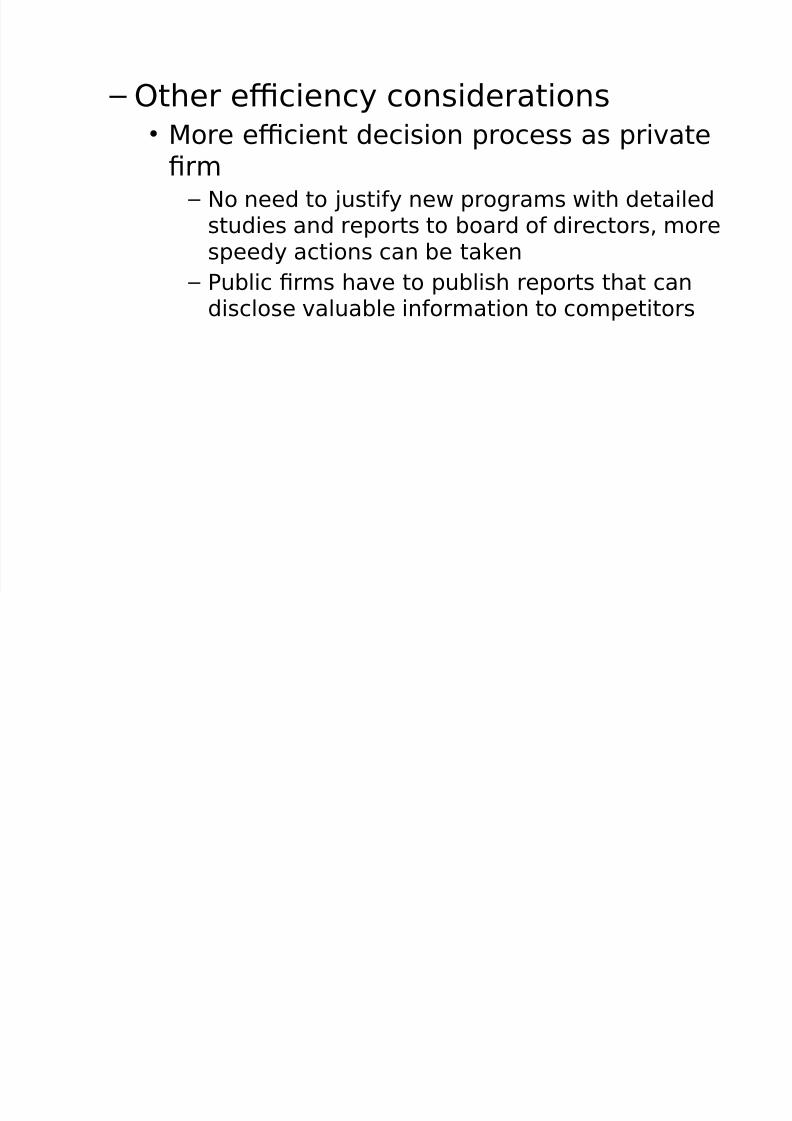

– Other eJciency considerations

• "ore eJcient decision process as privaterm

– o need to :ustify ne% programs %ith detailedstudies and reports to board of directors+ morespeedy actions can be taen

– Public rms have to publish reports that candisclose valuable information to competitors