4H.R*ffi*-l troH - Belghoria Janakalyan...

20

4H.R*ffi*-l cARE/KRO/RR/2OL'-L6/ Shri Bishwajit Das, Secreta ry Belghoria Janakalyan Samity AE-592, Sector - 1, Salt Lake City, Kolkata *700064 December 1-,201"5 Confidential Dear Sir, Grading of Micro Financine lnstitution (MFl) Please refer to our letter dated November 26,201"5 on the captioned subject. 2. As already advised, our Rating Committee has assigned a grading of 'MFl 3+'(MFlThree Plus) to your organisation. 3. The rationale fc.rr the grading is enclosed as an Annexure - I to this letter. 4. CARE's grading is an opinion o-f CARE on the relative capability of the organisation to undertake micro-financing activity and does not constitute a recommendation to buy, hold or sell any financial instrument issued by the organisation or to make loans/ donations/ grants to the said organisation. Thanking you, Yours faithfully, troH T|FNTTEIET Anolylicol lxcelhnce L325 ?,Vne f/'a-a'r"/'- (Pragati Khemka) Analyst tncl. - As above s* (Utkarsh Nopany) Manager CREDIT ANATYSIS & RESEARCH LTD. CORPORATE OFFICE: 4'h Floor, Godrei Coliseum, Somaiya Hospital Road, Off Eastern ExpressHighway, Sion (E), Mumbai 4OO 022. Tel.: +91-22-6754 3456; Fu: +91-22-67543457 Email: [email protected] I www.careratings.com 3rd Floor, Prasad Chambers, (Shagun Mall Bldg.) 10A, Shakespeare Sarani, Kolkata 700 071 Tel: +91 -33-401 I 1600 / 02 Fu: +91 -33-4018 1 603

Transcript of 4H.R*ffi*-l troH - Belghoria Janakalyan...

4H.R*ffi*-lcARE/KRO/RR/2OL'-L6/

Shri Bishwajit Das,

Secreta ry

Belghoria Janakalyan Samity

AE-592, Sector - 1,

Salt Lake City,

Kolkata *700064

December 1-,201"5

Confidential

Dear Sir,

Grading of Micro Financine lnstitution (MFl)

Please refer to our letter dated November 26,201"5 on the captioned subject.

2. As already advised, our Rating Committee has assigned a grading of 'MFl 3+'(MFlThree

Plus) to your organisation.

3. The rationale fc.rr the grading is enclosed as an Annexure - I to this letter.

4. CARE's grading is an opinion o-f CARE on the relative capability of the organisation to

undertake micro-financing activity and does not constitute a recommendation to buy,

hold or sell any financial instrument issued by the organisation or to make loans/

donations/ grants to the said organisation.

Thanking you,

Yours faithfully,

troHT|FNTTEIETAnolylicol lxcelhnce

L325

?,Vne f/'a-a'r"/'-

(Pragati Khemka)

Analyst

tncl. - As above

s*

(Utkarsh Nopany)

Manager

CREDIT ANATYSIS & RESEARCH LTD.

CORPORATE OFFICE: 4'h Floor, Godrei Coliseum, Somaiya Hospital Road,

Off Eastern ExpressHighway, Sion (E), Mumbai 4OO 022.Tel.: +91-22-6754 3456; Fu: +91-22-67543457Email: [email protected] I www.careratings.com

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.)

10A, Shakespeare Sarani, Kolkata 700 071

Tel: +91 -33-401 I 1600 / 02

Fu: +91 -33-4018 1 603

.

l_Igq qJ incorpora

Legal status

I Year of commencement of

| 41croliry1ce operations

Lending model

Srneturc:!_

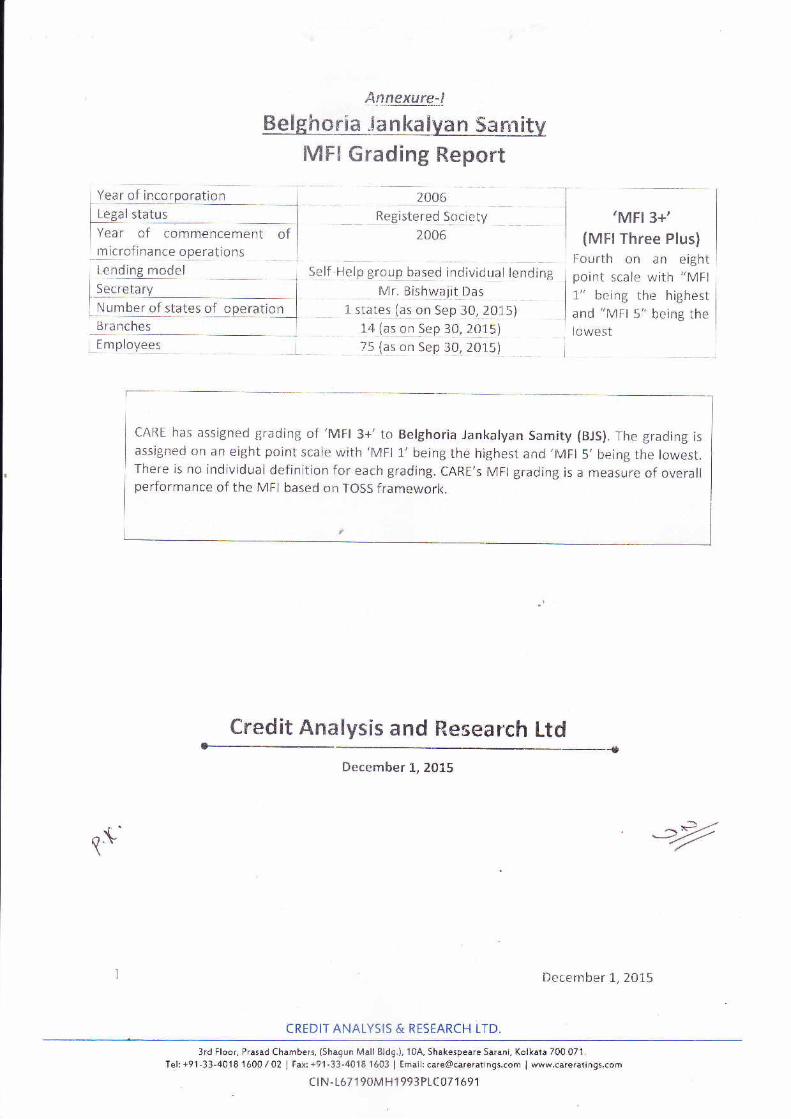

BelFhoria .lankalvan Samitv

MFI Gnading Report

20q6

ResEler_eq soqig!y

2006

Self'Help grogp bgsed individual lending

Mr, Bishwajit Das

1 slates- Iq: o.n Sep 30, 2015)

11 (r: o! 9ep 3q 201s)

75 {as on Sep 30, 2015)

CARE has assigned grading of 'MFl 3+'to Belghoria Jankalyan samityassigned on an eight point scale with'MFl 1,'being the highest and'tVlFlThere is no individual definition for each grading. cARE's MFI grading isperformance of the MFI based on TOSS framework.

,MFI 3+'

(MFl Three Plus)

Fourth on an eightpoint scale with "MFl

l" being the highest

and "MFl 5" being the

lowest

(BJS). The grading is

5' being the lowest.

a measure of overall

Credit Analysis and Research Ltd

q"\.'

December L,2075

CREDIT ANALYSIS & RESEARCH LTD.

December 1,201.5

__z

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071,

Tel:+9'l-33-40181600/02 | Fax:+91-33-40181603 | Email:[email protected] lwww.careratings.com

ct N - 1671 90M H1 993PLC07 1 69 1

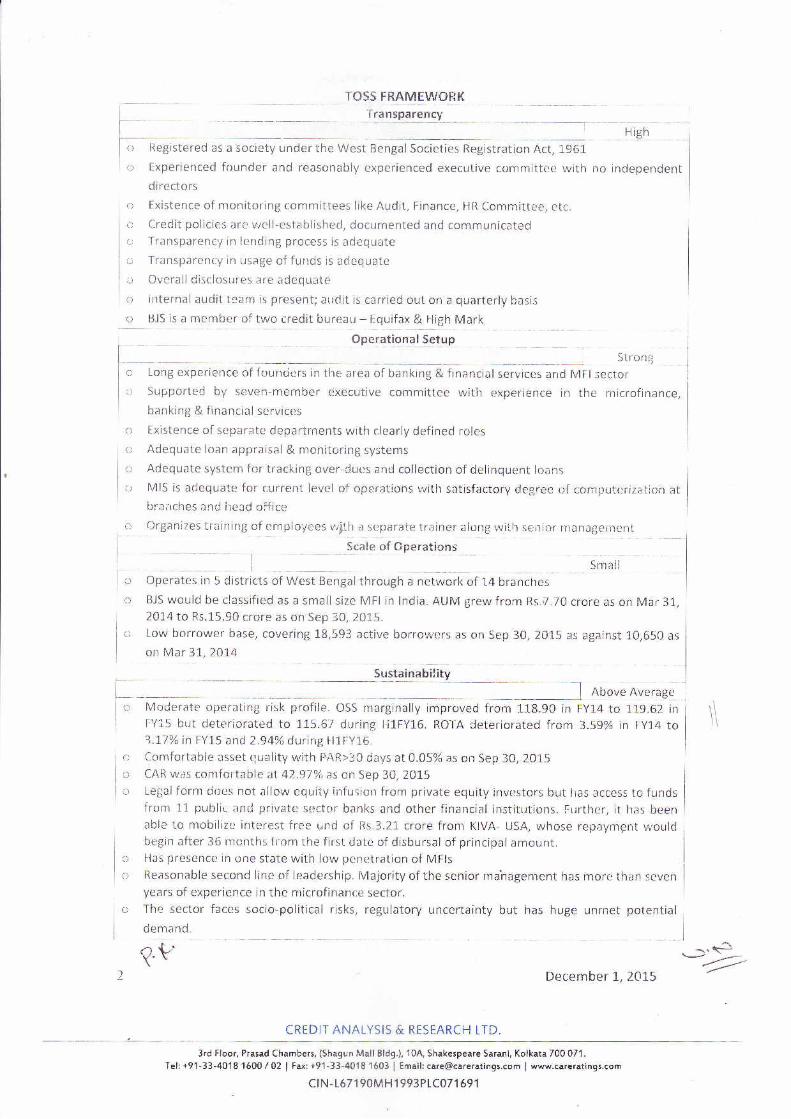

TOSS FRAMEWORK

r14!p"r"n.v

I o Registered as a society under the West Bengal Societies Registr-ation Act, 1961

H igh

o Experienced founder and reasonably experienced executive committee with no independent

d i recto rs

Fxistence of monitoring committees like Audit, Finance, I'lR Committee, etc

Credit policies are well-established, documented and communicatedT.ransparency in lerrding process is adequate

Transparency in usage of furrds is adequate

Overall disclosures are adequate

irrternal auditteam is present; audit is carried out on a quarterly basis

tsJS is a member of two credit bureau * Equifax & Fli51h Mark

Operational SetupI

long experiertce of f oundcrs in tlre or", of Urnting & frnanciafseruicc, arrd Ml,.".,l|'o"t

o

o

()

O

o

O

_rl

()

o Supported by seven-mernber executive committce with experience in the microfinance,

banking & fina rrcia I services

o Existence of separate departrnents with clearly defined roles

o Adequate loan appraisal & mcnitoring systems

o Adequate system for tracking over-dues and collection of delinquent loans

o Ml5 is adequate for current level of operations r,vith satisfactory degr^ee ol'computcrizalicn at

bra;rches and lreed office

o Organizes trairting of ernployees v;!th a scparate trainer along wiilr seirior nlanagement

Scale of OperaticnsI

Smaii

o Operates in 5 districts of West Bengal through a network of i"4 branches

o BJS would be classified as a small size MFI in lndia. AUM grewfrom Rs.7.70 crore as on Mar 31,

20L4to Rs.15.90 crore as on Sep 30, 201.5.

o Low borrower base, covering 18,593 active borrowers as on Sep 30, 20i5 as against L0,650 as

on Mar 31,2014

____Jgt_Frryqlity] niroue4r,,ergqa

o N{r.rderate operating risk profile. OSS marginally improved from l-18.90 in FY14 to 119.62 in['/i5 but deteriorated to 115.67 during l-i1FY16. ROTA Ceteriorated from 359% in FY].4 to3.17% in FYL5 and 2.94% during Hi,FY16.

o Comfortable asset cluality with PAR>:C days at 0.05% as on Sep 30, 2015

o CAR was comfortable at 42.97% as on Sep 30, 2015

o Legai form dr,.ies not allow equiiy infusiorr from private equity investors but has access to fundsfrom 11 publie and private sector banks and other financial institutions. Further, it has been

able to mobilizr: interest free und of Rs.3.2L crore from KIVA- USA, whose repayment wouldbegin after 36 months lrom the first dale of disbursal of principal amount.

c> Has presence in one state with low per-retration of MFls

o Reasonable second l.ine of leadership. Majority of the senior rnahagenrent has more than seven

years of experience in the microfinance sector.

o The sector faces socio-political risks, regulatory uncertainty but has huge unrnet potential

demand.

_. <3

December 1,2015 *tt=

CREDIT ANALYSIS & RESEARCH LTD.

\\

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91-33-4018 1600 / 02 | Fu: +91-33-4018 1603 | Email: [email protected] I www,careratings.com

ct N - 1671 90M H1 99 3P LC07 1 69 1

t? l{*Dl f,J G RAT! nlJrtLfBelghoria Janakalyan Sarnity (BJS) v;as eslablished in Jurre 2006 under the leadership of Mr.

Bishwajit Das to carry out various social and developmental activities. lt was registered as a

society under the West Bengal Societies Registration Act, 1961, and commenced

microfinance activity in Bashirhat region of 24 Parganas (North), West Bengal. lt started

lending under the'Self-Help Group'(SHG) based lending model, r,'yith modest contributions

l'rom tts founding members. Over the years, the society has received funding support from

various financial institutions enablirrg it to scale up its operations.

Thr: main objective of BJS is to provide loans to the rural poor who do not have access to

banking facilities for their economic upliftment. Major activities of BJS inciude the following:

c Formation and nurturing of SHGs

o inculcating savings habit among tfie poor

o lmparting skill to the SHG members by way of giving vocatiorral training on various

income generating activities

r Organising health camps, eye camps, medical check-up carnps

e Knowledge developrnent via finarrcial literacy arrd awareness canrpaigns

This apart, BJS also runs a non forrn"ul primary schoolfor kicls between the age of 3-10 years

in Baduria, West Bengal. Around 40 underprivileged students from the adjoining area are

admitted in the school. lt has also set-up BJS School of Financial Literacy, in collaboration

with iStVlW (lndian School of Microfinance for Women), for imparting financial literacy to

poor women. BJS also runs a handicraft training center and a computer training center for

imparting such skills to the poor free of cost. During FY15, BJS started a project'Targeting

Hardcore Poor'with financial and technical support of Bandhan. The project involves

selection of 100 poor women who have been selected under a pre-set selection criteria for

uplifting their economic condition. These women are provided training to earn their

livelihood and incorne generatir:g assets are distributed arnong tliem based on their clesire

and capability. Their activities are monitored closely and any further support which is

required by them is provided.

The day-to-day activities of BJS are icoi<ed after by Mr. Bishwajit Das who

employed with Bandhan Financial Services Pvt. Ltd for a period of six years.

o.t'1

was earlier

December 1,,201,5

CREDIT ANALYSIS & RESEARCH LTD.

.,\*)>-

3rd Floor, Prasad Chambers, (Shagun Mall Bldg,), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91-33-4018 160A / 02 | Fu: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

ct N- 1671 90M H1 993PLCO7't 69 1

As on Sep 30, 2015, BJS is operating in 5 districts of West Bengal. Operations of BJS are

managed through a networl< of 14 branches and have 18,593 active borrowers with total

outstanding portfolio of Rs.15.90 crore as on Sep 30,2015 (Rs.10.50 crore as on Mar 31,

2015). The operations of the society are managed by a workforce of 75 employees as on Sep

30,2015.

TRANSPARENCY

BJS is registered as a society under the West Bengal Societies Registration Act, 1961. The

leg;al form of organization does not allow the organization equity infusions. lt is c.iependent

upon the donations and contributicns from members.

The society is governed by a seven member executive committee uyith rich experience

across banking, financial services and MFI sector. lt is led by Mr. Satyabrata Chakraborty as

the President of the society. Executive committee meets on a bi-monthly basis to monitor

the progress, discuss financial and operational performance.

BJS has forrned sub-committees like audit committee, finance committee, HR committee,

etc.

Transpart'ncy in lending process

Lending policies (including interesr rate, processing fees arrd other charges) are clearly

communicated to the borrowers at group meetings throrrgh training programs &

orientations. Borrowers are made to sign a loan agreernent clearly stating the terms &

conditions and the covenants, thereof. Majority of borrowers are aware about the credit

policies.

Audit Quality

The auditor has given an unqualified report and satisfactory feedback.

Policies

BJS nas clearly defined and docurlented credit & HR policies. Credit policies are strictly

adhered to for fornration of groups, field verification arrd credit appraisal. The FIR policies

encompass recruitment and selection, induction anc training, performance management

and compensation management.

lnternal Control

lnternal audit or BjS is conducted by one nlember who has more than 1"0

experience with microfinance institutes, adequate accounting background and

1.L'4 December

years of working

knowledge about

-. \3\---/ -1-,201.s 4>-

CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91 - 3 3-4018 1600 / 02 | Fax: +91 -33-4018 1603 | E mail: [email protected] I www.careratings.com

crN-1671 90MH1 993P1C071 691

the organizational policies on accounting. Audit of branches are conducted on quarterly basis and

report is submitted directly to the executive committee. The objective of the department is to

monitor and evaluate financial as rvell as operational ciata and borrower level processes.

Transparency in usage offunds

BIS submits utilization report and book debt statenrent to the lenders on monthly or

quarterly basis as per the requirement of the lenders. Reporting to lenders on collection and

delinquency is also provided on regular basis.

Overall disclosures

BJS is regular in submitting operational and financial information to external associations

and agencies like Sadhan, Mix Market, ,rligh tt/lark and Equifax Credit Bureau. lt also provides

the operational and financlal information on its website, whiclr is updated on a regular

ba sis.

OPERATIONAL SETUP

Manageria I Factors

Ownership and Management

The organization is led by Mr. Satyabrata Chakraborty as the President. Mr. Bishwajit Das,

Secretary of BJS, whc was earlier employed with Bandhan Financial Services Pvt Ltd for six

years, looks after the day-to-day affairs of the organization.

Management Assessment

All the mernbers of the executive cornmittee have an overall experience of more than 7

yea rs.

The second line of leaderslrip irrcludes all the functional heads. Rll of them l'rave strong

leadership quality and rich experience in the field of microfinance.

Profile of senior management team

II, Narne I Qralification ; Oesignationr---.----l-

l/lr. Bishwajit Das I l'/t.Com I Cf i"t Executive Officer--

I vr. Tapan t<r.oas j rvt.cor I opcration tlead

I Vr. C. Ranjan Barai I M. Pharnr. I Busincss Developmerrt Hcad

li/lr. Balra|n Das ] B.Sc (Ag) ] A.dministration i.leacl

Mr. Dilip Kr. Maity ts.Sc (Ag) i Chief Finance Officer

Senior members have strong arrd diversified experience in fields of finan

agriculture & othcr social clevelopmental activities. Majority of the seni

I r"t"rv""iioi ]

I experience I- l---E-lI :r I1t

i23 I

I'o-l1 ,u

l

cial services,

or members

? t-'

5

-' t3

-.==-December 1",20L5

CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91-33-4018 160A / 02 | Fax: +91-33-4018 1603 I Email: [email protected] I www.careratings.com

ct N - 1671 90M H1993P LC07 1 69 1

understand the issues involved in day to day functioning and are involved in strategic

decision making of the organization.

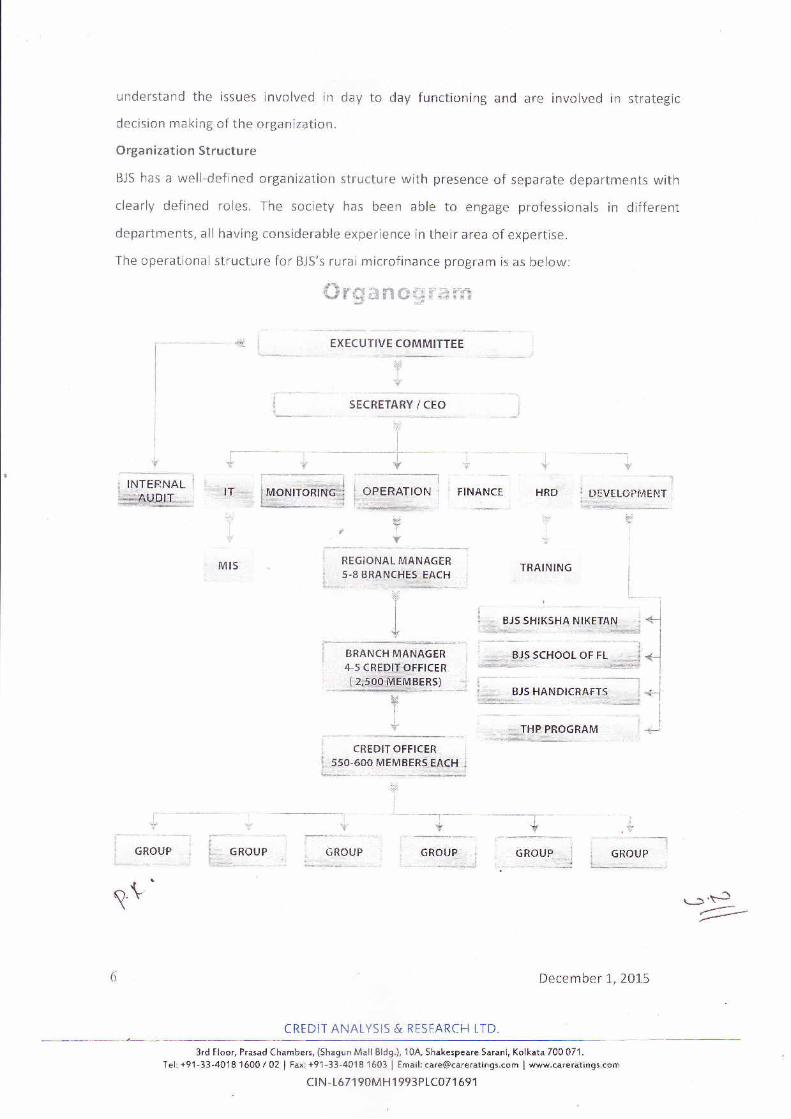

Organization Structure

BJS has a well-defined organization structure with presence of separate departments with

clearly defined roles. The society has been able to engage professionals in different

departments, all having considerable experience in their area of expertise.

The operational structure for BJS's rurai microfinance program is as below:

#rSffinsffir&ffi

EXECUTIVE COMMITTEE

&I

vSECRETARY / CEO

vI

*------?---"'" t I

v*::! INTERNAL i

ffi"S' mm

1*"----'*---*i: GROUP iil*-*"".-------;l

C).\\

IT

:Ii

Y

Mls

i**-9@:I OPERATTON l i

i"--",-=r=r-{f'il-"-1 I

VY

FINANCEi

1 -- -- .. *-----:rir DEVELOpMEI'IT.

I

!i'

HRD

V

i

*.:

I REGTONAL MANAGER j

{ s-eBRANcHEs EAcH lt,..",i

slY

I

III

v

TRAINING

December I,201.5

. -'$t=-'

i cREDtT OFFTCER j

i 550,600 MEMBFRS EACH ,|L:;;

". _:, _ -.=.,:i";.li; _., _"."__j

vl

, ' -l'-- - -i -'--- * r-- - -- - ---rY * v .v

CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Saranl, Kolkata 700 071.

Tel: +91 -3 3 -4018 160A / 02 | Fax: +91 -33 -401 I 1603 | Email: [email protected] I www.careratings.com

clN-1671 90MH1 993Pt C071 691

Level of decentralizotion of branches

At the branch level, a reporting structure has been created for effective monitoring of

operations. The credit officer identifies potential member and forwards the details to the

branch manager (Bl/l). BM then performs independent group verification assessment of the

members. Applications are then processed by him and are disbursed on his/her approval.

The operations are decentralized with branches handling field verification, ground level

credit appraisal and collection.

Recruitment & selection process

r Recruitment is done through employee referrals, advertisements in local dailies, soclety

website, etc.

r Selection process includes written test and a series of interviews with senior

management.

o The recruitment process is centralized at HO and mairily handled by the senior

management.

o Attritiorr rate is low at 5.8%

Training & Development

c Compulsory indrrction training fof all new recruits on joining for four days is provided by

an experienced trainer and senior management.

e Senior management participates in workshops and external training programs

corrducted by banks, financial institutions, etc.

Employee Strength:

t he manpow-i strengttr of BJS as on Septernbcr 30, 2015 is:

Senior Managemcrrt - 5

Credit Officer (CO)- a1

Branch Manager (BM)- 15

Regional Manager (RM) - 2

Divisional Manager (DM)- 1

Others {HO staff)- 11

I

r!l19

9

_00

23c

vv'December 1,201.5

CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91 - 3 3-4018 160A / 02 | Fu: +91 - 33-4018 1 603 | Email: [email protected] I www.careratings.com

c r N- 167 1 90M H1 993PLC07 1 69 1

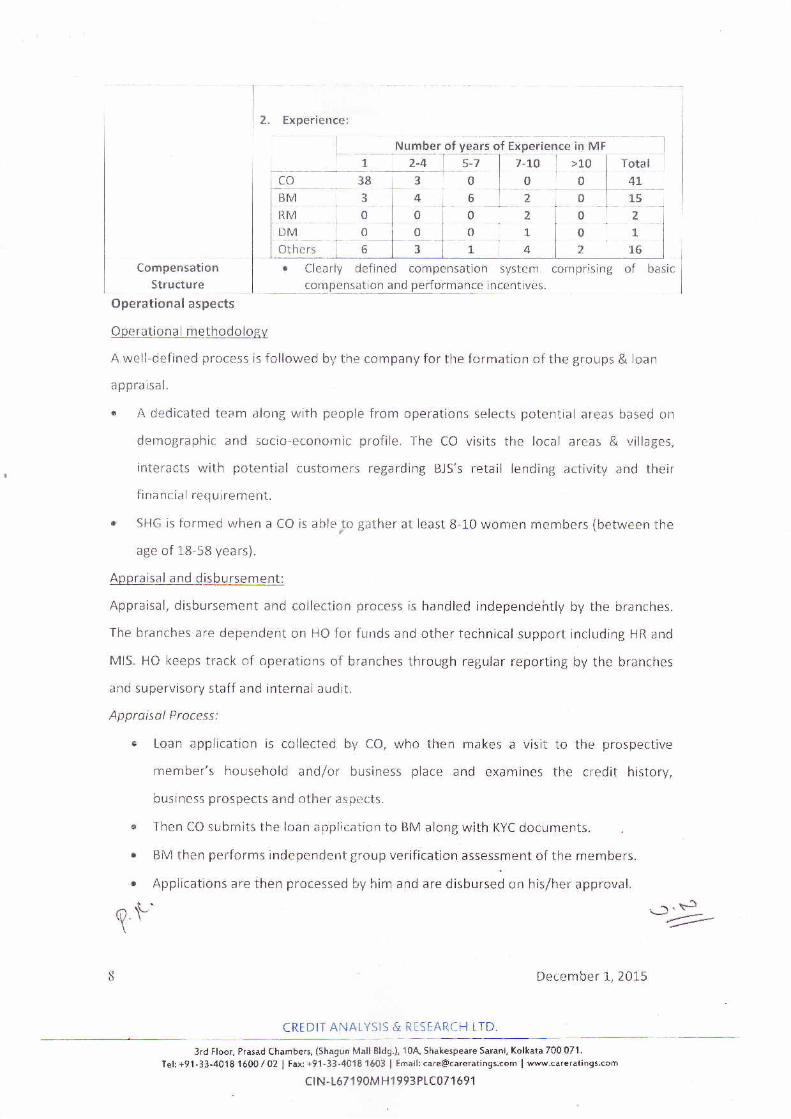

2. Experience:

Total

l

i

4L

Compensation

Structure

r Clearly defined compensation system comprising of basic

compensation and performance incentives

Operational aspects

O pe rq _tto n a I m eth qdpl_Sgy

A well-defined process is followed by the company for the formation of the groups & loan

a ppra isa l.

r I dedicated team along with people from operations selects potential areas based on

demographic and socio-econornic profile. The CO visits the local areas & villages,

interacts with potential customers regarding BJS's retail lending activity and their

financial requirement.

r SHG is formed when a CO is ablerto gather at least 8-10 wonren members (between the

age of 18-58 years).

Appraisal and disbursement:

Appraisal, disbursement and collection process is handled independehtly by the branches.

The branches are dependent on HO for funds and other technical support including HR and

MlS. HO keeps track of operations of branches through regular reporting by the branches

and supervisory staff and internai audit.

Appraisal Process:

e Loan application is collected by CO, who ihen makes a visit to the prospective

member's household andfor business place and examines the credit history,

business prospects and other aspects.

o Then CO sulrmits the loan applir:ation to BM along with KYC documents.

o BM then performs independent group verification assessment of the rnembers.

. Applications are then processed by him and are disbursei on his/her approval.

O \L' -.s5

' -t==-

December L,201"5

CREDIT ANALYSIS & RESEARCH LTD.

in Uaf

>10

0

0

oll

ol

2

L5

2

L

L6

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel:+91-33-4018160A/02 | Fu:+91-33-40181603 | Email:[email protected] lww.careratings.com

cr N- 1671 90M H1 993PLC07 1 69 1

Disbursement process:

o Cash disbursements are made to the borrowers in the presence of BM at the branch

off ice.

o Receipt voucher is collected from the borrower at the time of disbursement.

o Loan passbooks are provided to individual borrowers and loan register is maintained at

group level.

Loan collection process

o Loan collection tracking is done atthe branch levelthrough the loan register. Monitoring

is done at the HO.

r Collection is done on weekly basis in group meetings by the CO as per the demand

collection sheet.

. Entry is done at individual level (individual pass book) and also at group level (group loan

register). The cash collected is deposited into the bank account on the same day by the

CC.

o CO updates the cash book, daily deposits sheets and the software lVlll/l v,rhich is then

checked by BM.

Management lnformation Systems r

Backup Policy

The backup of the database of BJS is maintained in Cloud server using'Filezilla'software.

Apart from this, the data can also be retrieved through email as all the data is sent by the

branches to the HO over mail. Furthermore, the data backup is taken by the branches in a

pen drive on a daily basis and in a hard disk at the HO on a weekly basis.

Integrotion of HO with brqnches

BJS has an effective lT infrastructure in place to support its scale of operation. All the

branches have a computerized system of maintaining the data. They update the data in the

software'MlM'which has becn developed by the in-house lT team in collaboration with

Kanak Software and Solutions. After the data entry, reports are generated through MIM and

are sent to the HO over email. The HO then can access the data from its email.

The data sent from dlfferent branches gets reconciled at the HO.on a daily basis.

Alltypes of reports can be generated within short periocl of time (including overdue report).

The system is computerized with customized software'MllM'for loan tracking and

integrated with accounting software.

e.v'9

->'S:December 1,2A1-S

-CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel:+91-33-4018 160Al02 | Fax:+91-33-4018 1603 I Email:[email protected] I www.caretatings.com

ct N- 1671 90M H1 993PLC07 I 69 1

Underwriting/Appraisal and Sanctions

As discussed above, during appraisal the operations are decentralized. Appraisal process is

handled independently by the branches where the ultimate authority of sanctioning of loans

lies with the BM.

Criteria for sanctioning of loans (loan size, tenure, purpose etc.) are defined and

documented. The criteria for credit policies are adequate.

During appraisal, the documents that are coilected from the borrower are photo id proof,

and address proof. The docurnentation is adequate.

Mocie of disbursement

Disbursement amount for each MFI branch is transferred in the bank account of the branch.

2 COs or a CO along with BM withdraws cash from nearest bank branch. Then the

disbursements are made in cash to the borrowers in the presence of BM at the branch

off ice.

Reasonable level of documentation is done during disbursement.

Loan utilization checl<s are conducted hy the BM or CO one month after clisbursement.

Collectiorr is made byCO in cash and deposited in the banl<accourrtof FiO on the same day.

Loan repayment is tracked through ldan register and MiM software by the branches and HO.

Also demand collection book capturing information of demand, collection, overdues and

prepayments is maintained at the branch and field officer level.

Passbooks are provided to the borrowers.

Overdue monagement

BM is responsible for follow-up of all overdue loans of the CO reporting to him/her. Well-defined

process laid out for follow-up and collection of delinquent loans based on duration of overdue.

Loan delinquency is tracked in HO in regular manner through their software MlM. llo undue

influence and coercion is used to force the recovery. No late penalty charges are levied.

Re po rti n g fregu en cy after co I I ectio n

Reporting by the branches to Ho after collection is done on daily basis.

Borrawers per loan officer und gross loan portfolio per loan officer

Borrowers per loan officer and gross loan portfolio per loan. officer is moderate. No of

borrowers per ioan officer is 453 and gross loan portfolio per loan officer is approx. Rs.0.39

crore. * . -..x=? Y -47:--

December '1,2015

CREDIT ANALYSIS & RESEARCH LTD

l0

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 1 0A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91 -3 3 -401 8 1600 / 02 | Fa: +91 - 33 -4018 1603 I E mail: [email protected] I www.careratings.com

ctN-1671 90MH1 993PtC071 691

Risk Management Systems

Disaster recovery system

As discussed above, the backup of the database of BJS is maintained in Cloud server using

'Filezilla'software. Apart from this, the data can also be retrieved through email as all the

data is sent over maii. Furthermore, the data bacl<up is taken by the branches in a pen drive

on a daily basis and in a hard disl< at the FIO on a weekly basis.

lnsurance for Cosh in Transit/Limit on cash per laon officer, insuronce for borrowers

BJS does not take insurance for cash in transit and no limit is deflned on cash withdrawal

and deposit.

It provides insurance cover to its members from third party i.e. LIC on behalf of the

insurance company, BJS collects premium.

Presence of bank accounts ot branch level, mechanism for funds transfer andouthorizdtion for operating bsnk accountThere are separate bank accounts of every branch. Funds that need to be transferred from

HO to branches are done through RTGS.

Frequency for depositing cash in the bank (ofter repayment collectian), security af cush

Co deposits cash in the bank account of HO on the same day of collection. BJS encourages

nil cash in hand policy but sometimJs because of adverse situations some cash may remain

in hand, but the same gets deposited the immediate next working day. Cash vaults are

present at every branch for safe keeping of cash. No insurance has been taken for the same.

Credit discipline of borrowers

Attendance of borrorvers is above 90%. The meetings are conclucted orr a regular basis with

no penalties imposed.

Borrowers maintain the relevant documents provided by the MFl, i.e. passbook.

Process as per the operational manual is followed.

SCALE CIF OPERATIOT{S

BJS has built its microfinance portfolio since 2006 and has adequate track recorrj in the

microfinance sector.

The key operational p3rameters of the society, over the last two years, were as under:

Decernber 1,201,5

CREDIT ANALYSIS & RESEARCH LTD.

l1

. -'t--a2-

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tef: +91-33-4018 1600 / 02 | Fax: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

ct N - 1671 90M H1993P LCOT 1 69 1

For the period ended / As on, Y{ry Mar'15 Sep'15

Di stri cts

Bra nches

Number of active SHG members

Number of active SHG borrowgr:

Amount of loan disbursed during the year (Rs. crore)

3

_19

11,156

10r650

15.42

4

i)1,5,272

14,380

2L.30

5

1,4

20,139

18,593

1.s.ii

Employee Profile

Field officers

Total employees

2t

45

31

63

41

75

Employee productivity

ttl11!1of b91py,,ers per field officer

Anlount of Lc-ran per field officer (Rs. crore,)

507 464 453

4.37 0.34 0.39

Branch productivity

Nuller of lgmbers per branch

Amount of loan outstanJi;g per bianch (ns. crore)

r:1'16

0.77

1,273

0.87

L,481"

1.1,4

SUSTAINABILITY

Financial Sustainability

I ii!4".iI

Ir4_a11clql ledglCI4nqC

Depleqa!io1

Net surplus

Loan outstandiratios

EqlgrI oLr_lqlala9SeE

Operatl_oq q! Se lf- Suffi qr,qncy

FinanciaI Sqlf Sufficjency

In!gfel! inconne/lnterest earning assets

b!9rest / Ayg. bqrrowed fundslnterest spread

Ope rat i n g Expen q es_/ Tola l _ca p ita l_e ;n p

! CyedCapitaI adequacy ratio

?AB > 3Q dcy!P{R > 90 lays

4p91.86

0,Eq

Q160,q3

0.29

7.70

118 90

LLt,1?

24 70

16.99

1.71

_ !1,4941 83

0.03

lrlrI

I

1,54

3.s9

2.06

3.r71.1.9.67

M.7225 39

1I.4313 e6

_!?.]948.03

_ _ Q,qs0.030.03

Profita bilitv

The operating performance of the society has improved in FY15 as NIM improved from

1'3.37% in FY14 Io 15.7I% in FY15 on the back of funding received fronr KIVA and Kashi

Vishwanatha Vidya Samasthe at 0% interest rate during FY15. Operating expense (excluding

provision & write-off)/Avg. capital employed deteriorated from 10.77% in FY14 to 11.39% inot'\' Y

->'\-312 December I,2A1,S t=>-

CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91-33-4018 160A / OZ I Fu: +91-33-4018 1603 | Email: [email protected] I www,careratings.com

cr N- 1671 90M H1 993P1C07 1 69',!

FYI-5 on account of opening of new branches and higher expenditure made on social

activities. Provisioning expense (including write-offs) continued to remain atOJ,5% in FY15.

ROTA deteriorated from 3.59% as on March 31., 201.4 lo 3.1,7% as on March 31", 201,5;

however, PAT level has increased on an absolute basis.

ln H1FY16, BjS generated a profit of Rs.0.27 crore on a total income of Rs.1.65 crore.

Asset Qualitv

Although BJS has been lending to a high risk segment, it has been able to maintain a

reasonable track record. Asset quality is healthy with portfolict at risk greater than 30 days

(PAR>30 days) at O.O5% as on 5ep 30, 2015 and Mar 3I,2OI5 as against A.A3% as on Mar 31,

201.4.

Level of ca pita lization

CAR stood a|42.97% as on Sep 30,2OI5 as against CAR of 48.O3% as on Mar 3l-,201"5 and

41.83% as on Mar 3I,2014.

Access to funds and abilitv to raise funds

BJS has been successful in accessing funds from various public and private sector bairks,

financial institutions and NBFCs for onward lending to the individual borrowers under the

groups. t

Durirrg FY15, BJS raised funds of Rs.2.0 crore each from IOB and UBl, Rs.1.0 crore eaclr from

Dena Bank and UCO Bank, Rs.2.48 crore from KIVA (out of which Rs.1.O3 crore was

disbursed in H1FY16) and Rs.3.02 from Kashi Vishwanatha Vidya Samasthe (out of which

Rs.1.55 crore was disbursed in H1.FY16). Further, during H1FY16, the society has raised

Rs.2.25 crore from UBl, Rs.l-.0 crore each from SIDBI and Ananya Finance for lnclusive

Growth Pvt. Ltd.

Operational Sustainability

Second line of leadershiq

Majority of the senior nrembers understand the issues involved in day to day functioning

and are involved in strategic decisions as they have developed a good understanding of the

microfinance sector. BJS's senior management have strong and diversified experience in

fields like banking, financial services, MFl, etc.

O.\Lt

December 1,,7-OJ-5

CREDIT ANALYSIS & RESEARCH LTD.

-.13:

ti

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.),'10A, Shakespeare Sarani, Kolkata 700071.

Tel: +91-33-4018 160A / 02 | Fax: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

cr N - 1671 90M H1 993PLC07 1 69 1

Reg u I ato rV e nv i ro n me nt & sectoj-qg4--ogk

Post the AP crisis and regulatory intervention by RBl, the microfinance sector has seen

growth in loan portfolio. Overallthe credit profile of the MFls has shown improvement with

increasing loan portfolio on account of improving funding profile, control in operating

expenses, improving margins and moderate leverage levels.

Current focus of the microfinance sector is mainly on micro-credit with other products still

evolving including thrift, insurance and remittance etc. Going forward, MFls are likely to

expand their client base and reach out to more underserved areas of the country.

We believe that the microfinance sector has adapted to the new business environment

more than three years post the AP crisis. This phase is expected to be characterized by a

morc stable regulatory environment, steady availability of funds, improving profitability

with comfortable asset quality & capital adequacy and relatively lesser impact of

concentration risk. While we see improvement in credit profiles on account of the above

factors, credit view urill continue to factor in risks associated with unsecured lending, socio-

political intervention, geographic cclnceirtration and operational risks rciated tc cash based

transaction. Entity specific parameters relating to scale of operations, other operational

parameters and financial profile aldng with above factors will deterrnine individual MFI

credit views.

Loan Products

Product Name Ananya

Loan Tenure

Loan Size (Rs.)

r91l_

* interest rate is calculated on reducinq

?v'

Weekly/Fortnightly/ Month ly

_977 _ _

cing bolance method

Higher

Education

General

Education

lndividual women

18-58

Upto

s,000 -11,000

December 1,,2015

pto 2 years

10,000

30,000

processing Fees --_l

1% ' 1i/o I v" I r% 1% I, ty"Processing Fees ] 1o/o 1% I I% I I% 1% ', !%tnsurance ---l os% I o.sy" I o.sy" I o.sy, I o.sn. | 0s%

o/samiu'*s"d1s(R;ct- 0.30 l-r4oo I ] 006 | o.tr I _W,

o'rit" I ;:r,I ooo

I

l.:-3

-c1=-

CREDIT ANALYSIS & RESEARCH LTD.

*ot"n18-58

Upto 2

yeq !!16,000-

40,000

Limit (vrs)

I nsurance

11

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91.33-4018 1600 / 02 | Fax: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

crN-1671 90M H 1 993Pt_C07'l 691

Mr.

Satya brata

Cha kraborty

Ms. Kakali

Das Halder

Mr. Ranjit

Kumar Dutta

Ms. Mary

Banerjee

Ms. Mira

Debnath

President

Vice

President

M.Com

B,A.

M.A.

B.Com

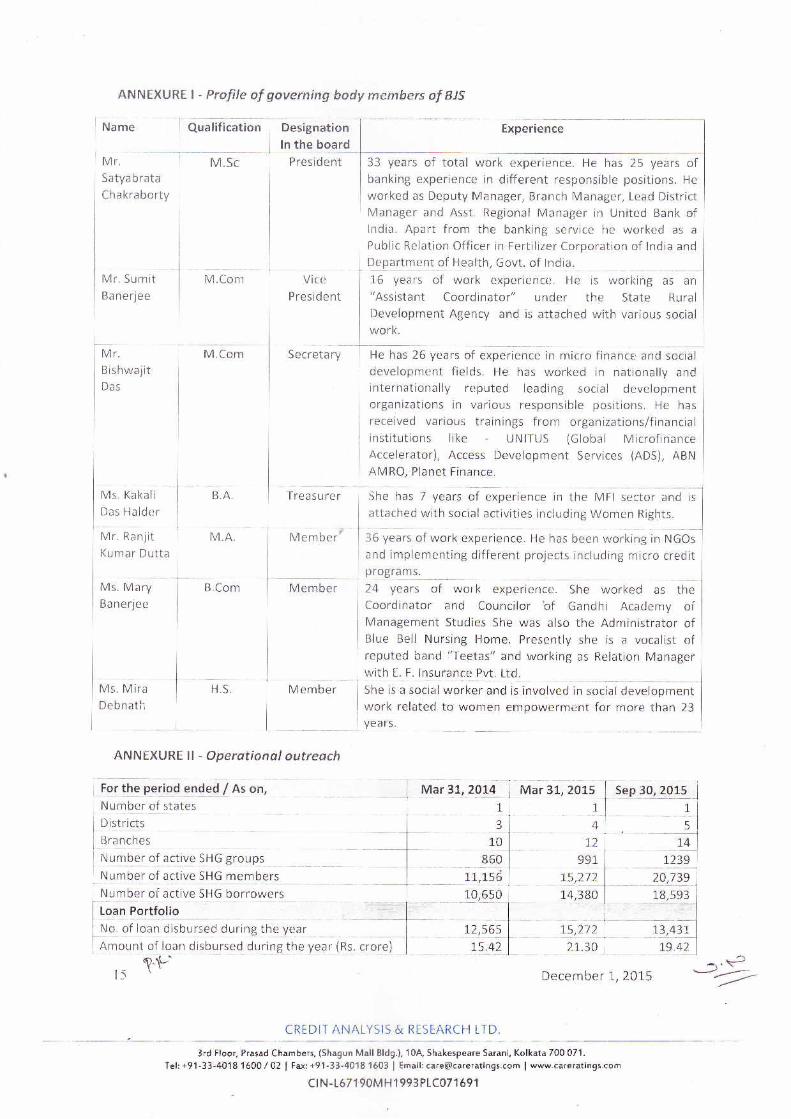

ANNEXURE I - Prafile of governing body members of BIS

Designation

ln the board

Experience

33 years of total work experience. He has 25 years of

banking experience in different responsible positions. He

worked as Deputy Manager, Branch Manager, Lead District

Manager and Asst. Regional Manager in United Bank oflndia. Apart from the banking service he worked as a

Public Relation Officer in Fertilizer Corporation of lndia and

Department of Health, Govt. of lndia.

16 years of work experience. He is working as an

"Assistant Coordinator" under the State Rural

Development Agency and is attached with various social

work.

He has 26 years of experience in micro finance and social

development fields. He has worked in nationally and

internationally reputed leading social developmentorganizations in various responsible positions. He has

received various trainings from organizations/financial

institutions Iike - UNITUS (Global Microfinance

Accelerator), Access Development Services (ADS), ABN

AMRO, Planet Finance.

She has 7 years oi u"p"ii"n." ln tf," vtrJ iector rnC iiattached with social activities including Women Rights

36 years of work experience. He has been working, in NGOs

Blue Bell Nursing Home. Presently she is a vt_rcalist ofreputed band 1'Teetas" and working as Relation Manager

wit| E, F, !lsurance Pvt. Ltd.

She is a social worker and is involved in .o.iaidevelopmentwork related to women empowerment for more than 23

yea rs.

l

Secreta ry

Treas u re r

Member/

H.S.

Member

Member

ANNEXURE 1l - Operotional outreach

ior tft" period ended / As on,

Number of states

D istri cts

Branches

Number of active 5HG glgups

Num!e1 9! ag_tive SHG r"rO"rtNumb91 9i activg !HG borrowers

Loan Portfolio

No. of loan disbursed during the year

Amount of loan disbursed during tne Vearl (ns

g \L'15 \

rvrr!ii, zoil1

q

19

860

11]!gr-_0/ql0

12,565

is.q)

CREDIT ANALYSIS & RESEARCH LTD.

t,4

1_2

e.e1

'rs/ry_

1a,990

L5,272

)r.zo

-'t3December I,201,5 *ti=

Mar 31, 201.5 Sep 30,2015 |-ltI

sl

'.1123e I

?o,1]d18,593

|"l13,431

]

is i-l

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91-33-4018 160A / OZ I Fax: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

c I N- 167 1 90M H1 993PLCO7 1 69 1

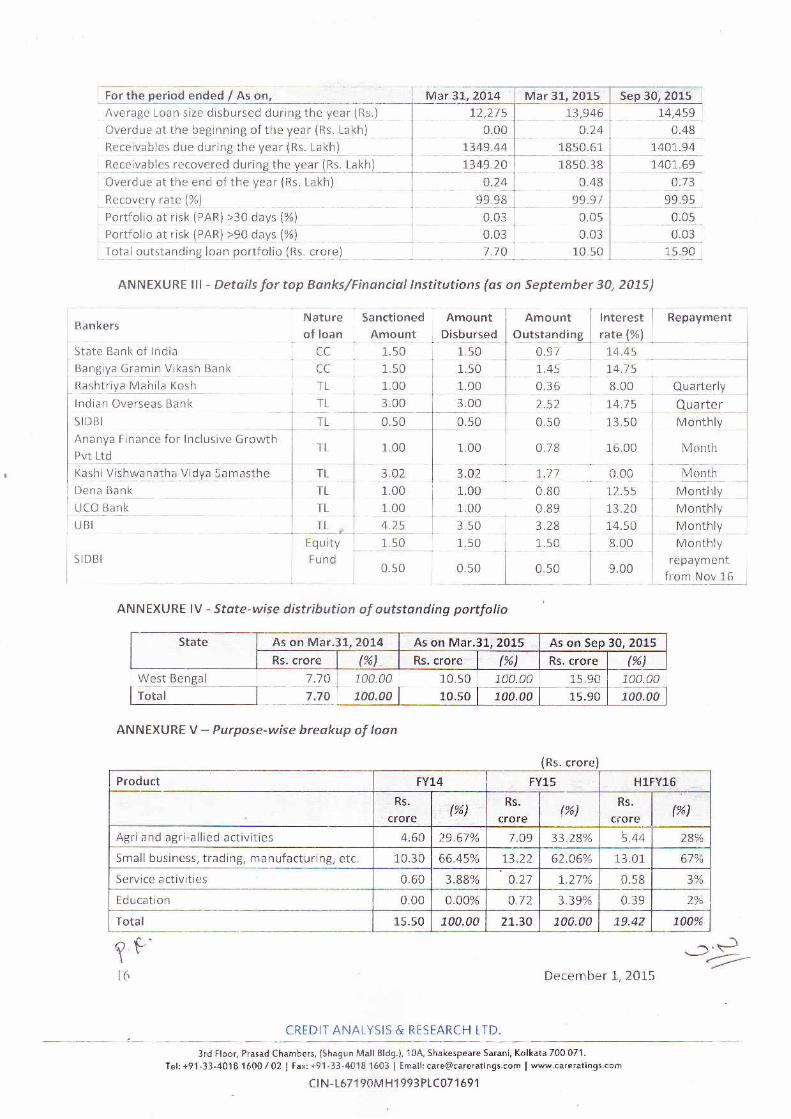

[*;;" a";. ri; oisorrseo ouring the ycar (Rs.)I

Overciue at the beginning of the year (Rs. Lakh)

I Receivablcs due during the year (Rs. Lakh)' ^ , , -;^ ,, ,

i Receivables recovered Aut!lg !,f'g yelr ing !a!1h)__Overdue at the end of the year (Rs. Lakh)

Mar 31, 2014 Mar 31,2015 Sep 30, 2015

12!472

o,9o

1349.44

L3-49 20

024es 9p

0.03

0.03

1.70

1.3,946

0.24

1_qsq 61

1850.38

0.48

99.91

0.05

0.03

10.50

L4,459

0r4,8_

1!9Le!1.401..69

Recovery rale (%)

Portfolio at risk (PAR) >30 days (%)

Portfolio at risk (PAR)>90 days (%)

Total outstanding loan portfolio (Rs. crore')

I nterest

rate (%l

14.45

1.4.7 5

8.00

1"4.7 5

16.00

0.00

1,2.55

L3.20

14.50

8.00

9.00

o.t3

99195

0 _0_l

0.03

15.90

Repayment

9vg!"rLv

9q!l!srMonthly

Month

ANNEXURE lll - Details for top Banks/Financial lnstitutions (as on September 30, 20L5)

Bankers

State Bank of lndia

Bangiya Gramin Vikash Bank

Rashtriya_Mahila Kosh

lndian Overseas Bank

SI DBI

Ananya Finance for lnclusive Growth

Pvt Ltd

Kashi Vishwanatha VlQya 5amasthe

Dena Bank

iJCO tsank

UBI

SIDBI

Amount

Outstanding

o.97

L.45

0.36

2.52

0.50

0.78

t./70.80

0.892 )a

1 .50

0.s0

ANNEXURE lV - State-wise distribution of outstanding portfolio

ANNEXURE V - Purpose-wise breakup of loan

YPl6

CREDIT ANALYSIS & RESEARCH LTD-

-.J-Ca---December 1", ?-01,5

sanitioned T Rrnount

Amount Disbursed

1.50 , 1.50

1.50 1.50

1.00 1.00

3.00 i :.ooI0.50 0.s0

I1.00 1 .00I

3.O2 3,O2

1.00 I 1.00/

1.00 : 1.00

4.2s I : sol1.50 1.50

I0.50 0 s0l

Nature

of loan

TL

TL

TL

TL

TI

TL

Tt

TL

Equ ity

F und

State As on Mar.3L,2014 As on Mar.3\ZAts As on Sep 30, 2015

Rs. crore I (%) Rs. crore (%) Rs. crore (%)

welt 89lgal

Total

tlo7.74

100.00

100.00

10.50 100.00 15.90 100.00

10.50 700.00 15.90 L00.00

(Rs. crore)

Product FYT4 FY15 H1FY16

Rs.

crore(%)

Rs.

crore {%)Rs.

crore(%)

Agri and agri-allied activities 4.60 29.67% 7.O9 33.28% 5.44 28%

Small business, trading, manufacturing, etc. 10.30 66.45% L3.22 62.A6% 1-3.01 67%

Service activities 0.60 3.88% o.2l a 114/ 0.58 3%

Education 0.00 0.00% 0.72 3.39% 0.39 10;

Total 15.s0 100.00 2L.30 70a.o0 79.42 740%

3rd Floor, Prasad Chambers, (Shagun Mall Bld9.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91-33-4018 160A / 02 | Fu: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

ct N- 167 1 90M H1 99 3PLC07 1 69 1

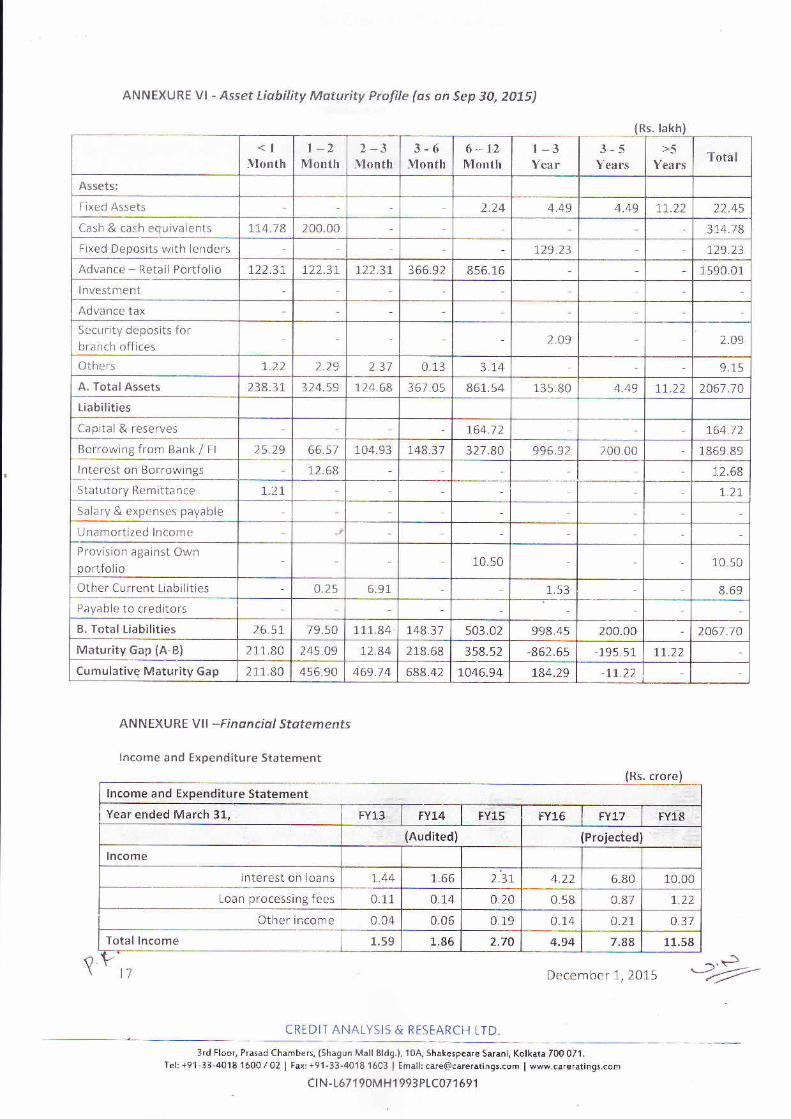

ANNEXURE Vl - Asset Liability Moturity Profile (as on Sep 30, 2015)

ANNEXURE Vll *Financial Statements

lncome and Expenditure Statement

q

(Rs. crore)

December I,20L5.-}

-2=-CREDIT ANALYSIS & RESEARCH LID

lakh

| -2Month

6-12Month

Fixed Assets

Cash & cash equivalents

Fixed Deposits v;ith lenders

1-14.78 3!4.78

L29.23

Advance - Retail Portfolio

lnvestment

I22.31 L22.31 L22.31 159C.01

Advance tax

Security deposits for

branch offices

A. Total Assets 861.54

Capital & reserves

Borrowing from Bank / Fl

lnterest on Borrowings

Statutory Remittance

164.12

L48.37

Salary & expenses payable

Unamortized lncome

Provision against Own

portf olio

Other Current Liabilities

Payable to creditors

B. Total Liabilities

Maturity Gap (A-B)

Cumulative Maturity Gap

L48.3l

358.52 -195.5 1

-11.22

lncome and Expenditure Statement

Year ended March 31, FY13 FY14 FY15 FY16 FY17 FY18

(Audited) (Projected)

lncome

lnterest on loans L.44 1.66 2.31 4.22 6.80 10.00

Loan processing fees 0.11 0.1"4 0.20 0.58 0.87 1,.22

Other income 0.04 0.06 0.19 0.1.4 0.21 0.37

Total lncome 1.59 1.86 2.70 4.94 7.88 11.58

t1

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91 -33-4018 '1600 / 02 | Fu: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

ctN- 167190M H1993PLC07'.t 691

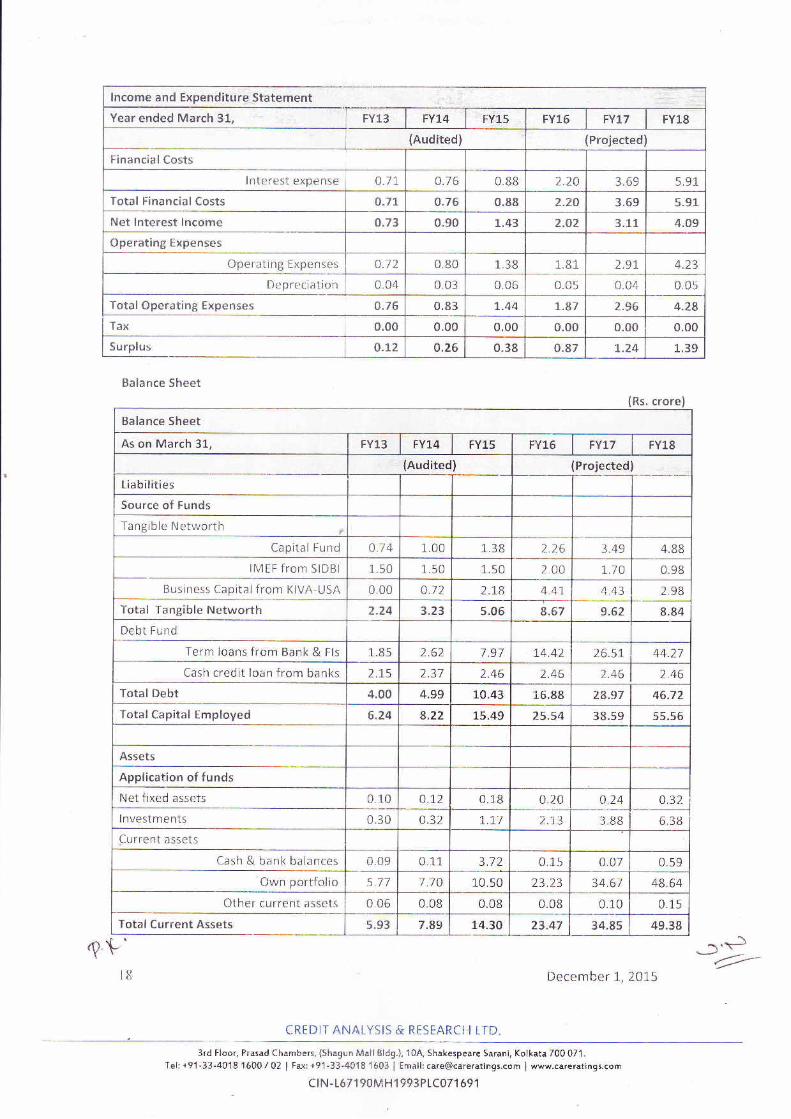

lncome and Expenditure Statement

Year ended March 31, FY13 FY14 FY15 FY16 FYLT FY18

(Audited) IProjected)

FinancialCosts

lnterest expense 0.71 o.76 0.88 2.24 3.69 5.91

Total Financial Costs o.7t o.76 0.88 2.ZO 3.69 5.9L

Net lnterest lncome o.73 0.90 L.43 2.02 3.LL 4.09

Operating Expenses

Operating Expenses o.72 0.80 1.38 1-.8 1 2.91 4.23

De preciation 0.04 0.03 0.06 0.05 0.04 0.05

Total Operating Expenses 0.76 0.83 L.44 L.87 2.96 4.28

TaN 0.00 0.00 0.00 0.00 0.00 0.00

Surplus o.L2 o.26 0.38 0.87 L.24 1.39

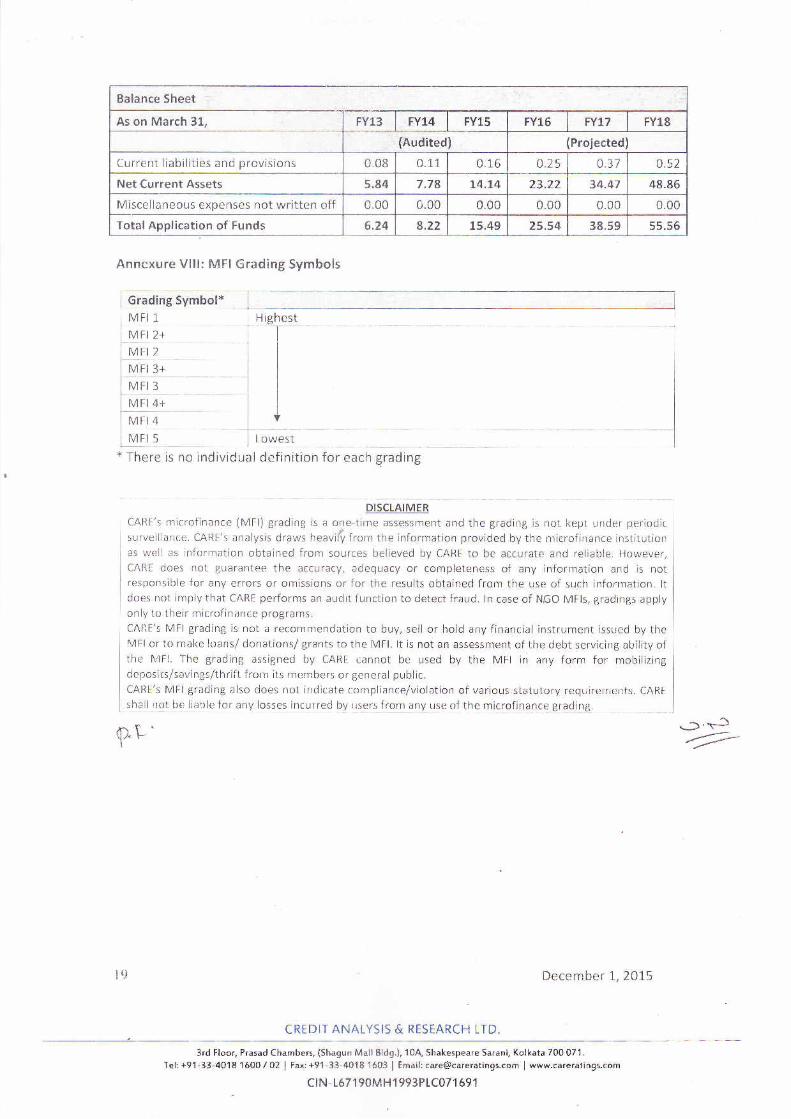

Balance Sheet

(Rs. crore)

Balance Sheet

As on March 31, FY13 FY14 FY15 FY16 TYLT FY18

(Audited (Projected

Liabilities

Source of Funds

Tangible Networth d

Capital Fund 0.7 4 1.00 1.38 2.26 3.49 4.88

IMEF from SIDBI 1.50 1.50 1.50 2.00 L.70 0.98

Business Capital from KIVA-USA 0.00 0.12 L. T6 4.4L 4.43 2.98

Total Tangible Networth 2.24 3.23 s.06 8.67 9.62 8.84

Debt Fund

Term loans from Bank & Fls 1.85 2.62 1.97 14.42 26.51 44.27

Cash credit loan from banks 2.15 2.37 2.46 2.46 2.46 2.46

Total Debt 4.00 4.99 10.43 15.88 28.97 46.72

Total Capital Employed 6.24 8.22 15.49 25.54 38.s9 55.56

Assets

Application of funds

Net f ixed assets 0.10 0.1.2 0.1 8 0.20 o.24 0.32

I nvestm ents 0.30 0.32 1".I7 2.r3 3.88 6.38

Current assets

Cash & bank balances 0.09 0.11 3.72 0.1.5 0.07 0.59

Own portfolio 5.71 1.70 10.50 z3 1) 34 67 48.64

Other current assets 0.06 0.08 0.08 0.08 0.10 0.15

Total Current Assets s.93 7.89 14.30 23.47 34.85 49.38

,? \-'t8

-.xJ-Ca--

December 1", 2015

CREDIT ANALYSIS & RESEARCH LTD.

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 0/1.Tel: +9'l -33-4018 160A / 02 | Fu: +91-33-4018 1603 | Email: [email protected] I www.careratings.com

ct N- 1671 90M H1 993PLCO7 1 69 1

Balance Sheet

As on March 31, FY13 FY14 FY15 FY16 FYLT FY18

(Audited) (Projected)

Current liabilities and provisions 0.08 0.11 0.16 o.2s 0.37 o.52

Net Current Assets 5.84 7.78 L4,L4 23.22 34.47 48.86

Miscellaneous expenses not written off 0.00 0.00 0.00 0.00 0.00 0.00

Total Application of Funds 6.24 8.22 15.49 25.54 38.59 55.56

Anncxure Vlll: MFI Grading Symbols

Grading Symbol*

MFI 1

MFI 2't

MFI 2

MFI 3

MFI 4+

MFI4

MFI5* There is no individual definition for each grading

DISEIAIMEB

CARE's microfinance (MFl) grading is a one-time assessment and the grading is not kept under periodic

surveiilance. CARF's analysis draws heavi$ from the information provided by the nricrofinance institutionas well as information obtained frorn sources believed by CARE to be accurate and reliable. However,

CARE does not guarantee the accuracy, adequacy or completeness of any information and is not

responsible for any errors or omissions or for the results obtained from the use of such inforrnation. ltdoes not imply that CARE performs an audit function to detect fraud. ln case of N,GO MFls, gradings apply

only to their microfinance programs.

CAIIF's MFI grading is not a recommendation to buy, sell or hold any financial instrument issued by thel/lFl or to make loans/ donations/ grants to the MFl. lt is not an assessment of the debt servicing ability ofthe N4FI. The grading assigned by CARE cannot be used by the MFI in any form for rnobilizing

deposits/savings/thrift from its members or general public.

CARE's MFI grading also does not indlcate compliance/violation of various statutory requirerrents. CARE

shall not be liable for ariy losses incurred by users from any use of the microfinance grading.

P.t

December I,2O1-':

CREDIT ANALYSIS & RESEARCH LTD.

.;1 '5:

at'-

t9

ct N- 167 1 90M H1 993PLCO7',t 69 1

3rd Floor, Prasad Chambers, (Shagun Mall Bldg.), 10A, Shakespeare Sarani, Kolkata 700 071.

Tel: +91 - 3 3-4018 160A / 02 | Fu: +91 -33-4018 1603 | Email: [email protected] I www.careratings.com

![H3C - IIT-ians PACE...lffiEffil s. dri-q ffi rclliq olq rzo" t 3 6. 0) PH3€) cFsG) NCt3/p" Bcl3tre { t dn co }ffi ff+t?0) tq].d]frr14 la { erFa qe {q0) ctrsrR6) crEcf{q d t fc'q](https://static.fdocuments.nl/doc/165x107/5e6dff08fd502246e8213bda/h3c-iit-ians-pace-lffieffil-s-dri-q-ffi-rclliq-olq-rzo-t-3-6-0-ph3a.jpg)