Enterprise Architectuur Management Magazine - The Voice of the Architect

PRESIDENTG. N. Venkataraman

email : [email protected] PRESIDENT

B. M. Sharmaemail : [email protected] COUNCIL MEMBERS

A. N. Raman, A. S. Durga Prasad,Ashwin G. Dalwadi, Balwinder Singh,Chandra Wadhwa, Hari Krishan Goel,Kunal Banerjee, M. Gopalakrishnan,

Dr. Sanjiban Bandyopadhyaya,S. R. Bhargave, Somnath Mukherjee,

Suresh Chandra Mohanty, V. C. Kothari,GOVERNMENT NOMINEES

Jaikant Singh, P. K. Sharma, R. K. Jain,S. C. Vasudeva, T. S. Rangan

CHIEF EXECUTIVE OFFICERSudhir [email protected]

Senior Director (Examinations)Chandana Bose

[email protected] Director

(Administration & Finance)R N Pal

[email protected] (Technical)

J. P. [email protected]

Director (Studies)Arnab Chakraborty

[email protected] (CAT)L. Gurumurthy

[email protected] Director (CEP)

Additional Director (Membership) cumJoint Secretary

Kaushik [email protected]

Additional Director (International Affairs)S. C. Gupta

Sudhir GalandeEditorial Office & Headquarters

12, Sudder Street, Kolkata-700 016Phone : (033) 2252-1031/34/35,

Fax : (033) 2252-1602/1492Website : www.icwai.org

Delhi OfficeICWAI Bhawan

3, Institutional Area, Lodi RoadNew Delhi-110003

Phone : (011) 24622156, 24618645,Fax: (011) 24622156, 24631532,

24618645

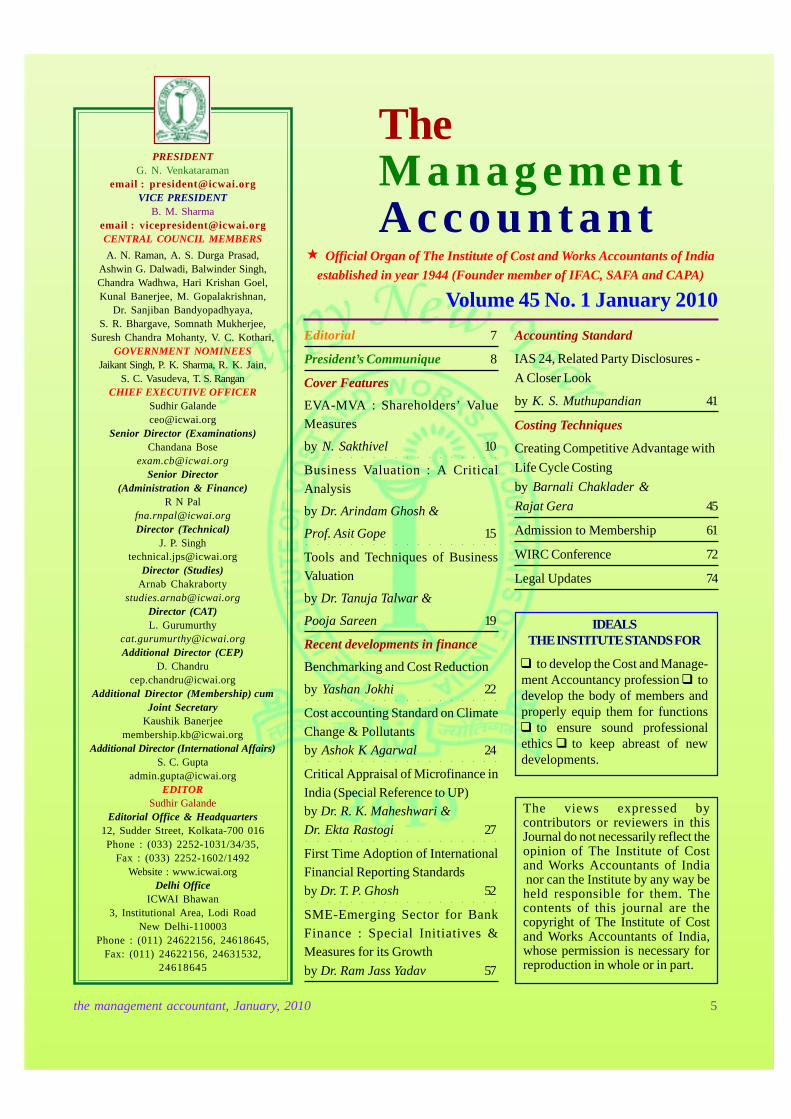

TheManagementAccountan t

« Official Organ of The Institute of Cost and Works Accountants of India

established in year 1944 (Founder member of IFAC, SAFA and CAPA)

Volume 45 No. 1 January 2010

the management accountant, January, 2010 5

Editorial 7

President’s Communique 8

Cover Features

EVA-MVA : Shareholders’ Value

Measures

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by N. Sakthivel 10

Business Valuation : A Critical

Analysis

by Dr. Arindam Ghosh &

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Prof. Asit Gope 15

Tools and Techniques of Business

Valuation

by Dr. Tanuja Talwar &

Pooja Sareen 19

Recent developments in finance

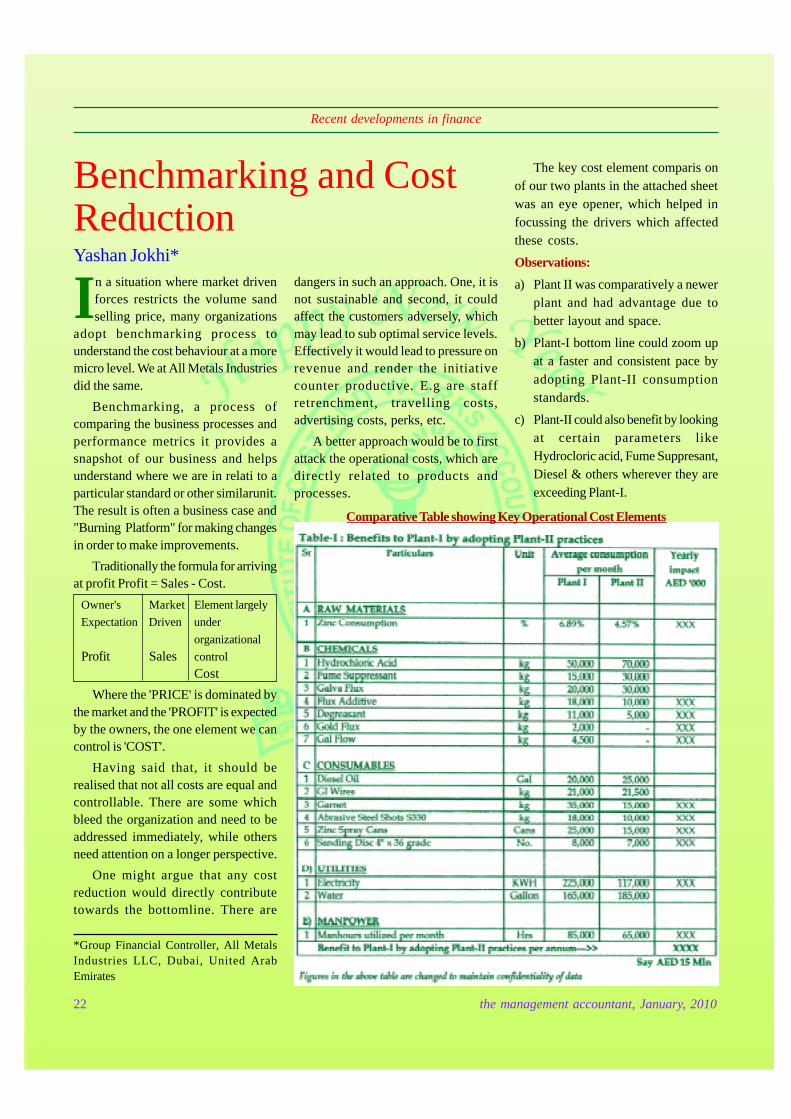

Benchmarking and Cost Reduction

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by Yashan Jokhi 22

Cost accounting Standard on Climate

Change & Pollutants

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by Ashok K Agarwal 24

Critical Appraisal of Microfinance in

India (Special Reference to UP)by Dr. R. K. Maheshwari &

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Dr. Ekta Rastogi 27

First Time Adoption of InternationalFinancial Reporting Standards

○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

by Dr. T. P. Ghosh 52

SME-Emerging Sector for Bank

Finance : Special Initiatives &Measures for its Growth

by Dr. Ram Jass Yadav 57

IDEALSTHE INSTITUTE STANDS FOR

q to develop the Cost and Manage-ment Accountancy profession q todevelop the body of members andproperly equip them for functionsq to ensure sound professionalethics q to keep abreast of newdevelopments.

The views expressed bycontributors or reviewers in thisJournal do not necessarily reflect theopinion of The Institute of Costand Works Accountants of India nor can the Institute by any way beheld responsible for them. Thecontents of this journal are thecopyright of The Institute of Costand Works Accountants of India,whose permission is necessary forreproduction in whole or in part.

Accounting Standard

IAS 24, Related Party Disclosures -

A Closer Look

by K. S. Muthupandian 41

Costing Techniques

Creating Competitive Advantage with

Life Cycle Costing

by Barnali Chaklader &

Rajat Gera 45

Admission to Membership 61

WIRC Conference 72

Legal Updates 74

The Management AccountantTechnical Data

Periodicity MonthlyLanguage English

Overall size - 26.5 cm. x 19.5 cm.Printed Area - 24 cm. x 17 cm.

Screens - up to 130

Subscription

Rs. 300/- (Inland) p.a.Single Copy : Rs. 30/-

Overseas

US $ 150 for AirmailUS $ 100 for Surface Mail

Concessional Subscription Rates for RegisteredStudents & Grad CWAs of the Institute

Rs. 150/- p.a.Single Copy : Rs. 15/- (for ICWAI

Students & Grad CWAs)

Subscription rate and price ofThe Management Accountant

(Student Edition)Annual Subscription rate : Rs. 50Price of Single copy : Rs. 5

Advertisement Rates forThe Management Accountant

Rs. (US $)Back Cover (colour only) 30,000 2,000

Inside Cover (colour only) 25,000 1,500

Ordy. Full page (B/W only) 12,000 1,200

Ordy. Half page (B/W only) 9,000 1,000

Ordy. Qrtr. page (B/W only) 5,000 500

Advertisement Rates for

Student Edition

Full Page Rs. 10,000

Back Page Rs. 8,000

(Always Half Page only)

Inside Half Page Rs. 5,000

Inside Quarter Page Rs. 3,000

The Institute reserves the right to refuse anymatter of advertisement detrimental to theinterest of the Institute. The decision of theEditor in this regard will be final.

6 the management accountant, January, 2010

MISSION STMISSION STMISSION STMISSION STMISSION STAAAAATEMENTTEMENTTEMENTTEMENTTEMENT

�ICWAI Professionals would ethically driveenterprises globally by creating value tostakeholders in the socio-economic contextthrough competencies drawn from theintegration of strategy, management andaccounting.�

VISION STVISION STVISION STVISION STVISION ST AAAAATEMENTTEMENTTEMENTTEMENTTEMENT

�ICWAI would be the preferred source ofresources and professionals for the financialleadership of enterprises globally.�

DISCLAIMER

The views expressed by the authorsare personal and do not necessarilyrepresent the views and should notbe attributed to ICWAI.

CONDOLENCE

We inform with deep sorrow thedemise of our beloved past Secretaryof ICWAI, Shri S.N.Ghose onDecember 24th, 2009 at Kolkata. Wepray for peace of the departed souland hope that his family has strengthto bear the irreparable loss.

Editorial

the management accountant, January, 2010 7

Valuable Valuation

Readers will recall that the last issue of TheManagement Accountant focused on corporatestrategy. One of the foremost requirements offormulating a corporate strategy is to estimate thevalue of one's organization. Business valuation is aprocess and a set of procedures used to estimatethe economic value of an owner's interest in abusiness. Valuation is used by financial marketparticipants to determine the price they are willingto pay or receive to consummate a sale of a business.In addition to estimating the selling price of a business,the same valuation tools are often used by businessappraisers to resolve disputes related to estate andgift taxation, allocate business purchase price amongbusiness assets, establish a formula for estimatingthe value of partners' ownership interest for buy-sellagreements, and many other business and legalpurposes.

The most common benefits of an annual businessvaluation policy include: Accountability andPerformance (an annual business valuation enablesthe shareholders to see the value that is beingconsistently created or destroyed by the managementof the firm), Estate Planning Purposes (manyshareholders have on-going estate planning strategiesaimed at protecting wealth for heirs), Buy-sellsituations (for those firms that do not have buy-sellagreements in place, annual business valuations area good way of avoiding disputes that may arise whena shareholder seeks to sell his shares to the othershareholders), Facilitate Banking (the ability of a firmto borrow based on the value of the goodwill or thevalue of the company's shares may expand theuniverse of value-creating investment optionsavailable) and Expands the Investment Options (for

closely held firms which suffer from a lack ofliquidity).

The most common approaches to valuate a businessare: asset approach (establishment of fair marketvalue, replacement value or liquidation value of theassets and liabilities), market approach (futuremaintainable earnings valuation- capitalisation rate,discount rate and discounted cash flow methods)and market appoach (relative valuation comparedto company & comparable transactions).

Understanding how to value a business and give anaccurate business appraisal is a difficult and timeconsuming process. Setting a price for a businessthat is too high can result in the business not beingsold for a long period of time; sometimes not at all.If the business owner eventually adjusts the price tohow the market is responding, the deal will often betainted with the view that something is wrong withthe business or that the owner is desperate. Settinga price for a business that is too low can often resultin the business owner not realizing the full benefit oftheir investment, ultimately losing out on the truebusiness value. Determining the cost of valuing abusiness is dependent on the size and complexity ofthe business being evaluated, as well as anyfundamental factors that may affect the businessvalue: Business Cash Flow, Industry Sector,Competition, Buyer Market, Employee Skill Level,Customer Base, Owner Involvement, Revenue, Ageof Business, Availability of Vendor Financing andProfitability Trend.

The articles covered in the current issue are aimedto equip readers with facts and issues on businessvaluation.

8 the management accountant, January, 2010

lPresident�s Communique l

Dear Professional friends,At the outset, let me wish you a VERY VERY HAPPY AND PROSPEROUS YEAR 2010.1. INDIA CORPORATE WEEK:The month of December was filled with hectic events of ICWAI and I congratulateall my professional friends, especially from the Chapters and Regions, along withmy Council colleagues, for having contributed for much more visibility of ICWAI. Imay have to mention that the recently concluded INDIA CORPORATE WEEK2009 held from 14th to 21st December 2009 along with MCA was a tremendoussuccess and brought more laurels to the members of our profession. The reportingof the celebrations was noticed especially by our Minister, Mr. Salman Khurshidand he congratulated our Institute for arranging such programmes. One of thenewspapers reported that ICAI and ICSI were following the path of ICWAI. Thecredit goes to all of you. Apart from the Minister, our Secretary, Shri Bandyopadhayaji and MCA AdditionalSecretary, Mr. Sudhakar and MCA Joint Secretaries, Mrs. Renuka Kumar and Mr. Srivastava appreciatedICWAI's contribution for the grand success of INDIA CORPORATE WEEK 2009. The programmesincluded Corporate Awareness Run, Blood Donation, Essay Competition and address by eminent speakerson Corporate Governance and Corporate Social Responsibility. The ICWAI has brought out 6 publicationsduring the occasion to herald ICWAI's participation in the inclusive growth of economy of the country. Thepublications were released by ROC-Chennai. Compendium of 1 to 10 Standards was also released as wehave made it mandatory for all our members to adhere to CAS 1 to 10 from 1st April 2010.The finale of the INDIA CORPORATE WEEK 2009 was held at New Delhi on 21st December 2009 withaddress by Her Excellency, Mrs. Prathibha Patil, President of India, along with Hon'ble Minister for CorporateAffairs, Mr. Salman Khurshid and Secretary-MCA, Shri Bandyopadhyaya. It was sponsored by IICA andNFCG, representatives of all industry associations and three Professional Institutions, including ICWAI.2. AWARD OF EXCELLENCE FOR ICWAI:During this occasion, we were happy to be awarded with Corporate Excellence Award by the President ofIndia, which was received by me along with my colleagues. This is a great honour given to our professionover the past several years and I cherish the same along with all of you and thank you for enabling us toreach this height. The MCA has also brought out 2 publications during this occasion, titled 'VoluntaryGuidelines of Corporate Social Responsibility 2009' and 'Corporate Governance 2009'. I congratulateMCA, IICA and NFCG for giving a thrust for these events to happen for the first time in Corporate India.This will be the annual feature from now onwards.3. ICWAI'S PARTICIPATION IN THE INDO-UK TASK FORCE:I am extremely happy to have represented the Indo-UK Task Force of Govt. of India, headed by ShriBandyopadhyaya, IAS, Secretary-MCA and Shri Jitesh Khosla, IAS, OSD-IICA. The Task Force hadfruitful meetings with the Right Hon'ble Mayor of London and his officials. Several meetings with theMinistry Officials of UK and other professional bodies were the hallmark for continuation of our tie-up withprofessional bodies like CIMA, UK. Shri Kunal Banerjee, CCM-IPP, accompanied me.4. OUR MINISTER'S CALL FOR INNOVATION BY ICWAI:The SAFA's International Seminar was inaugurated by our Hon'ble Minister Mr. Salman Khurshid on 26th

November 2009 and he gave a call to ICWAI to work with innovative ideas including Corporate SocialResponsibility and suggested CSR Credit Rating on the lines of Carbon Credit Rating. He expressed thathe would be very happy to see that ICWAI takes the lead along with SAFA so that the other parts of theworld follows it. In this direction, I am happy to say that ICWAI has initiated certain programmes, which Iwill be sharing with you when it materializes and this will be a good contribution of ICWAI to the wholeworld, if not just for the Corporate Sector.

the management accountant, January, 2010 9

5. REGIONAL COST CONVENTIONS:5.1 Regional Cost Convention of SIRC:The SIRC organized Regional Cost Convention 2009 at Hyderabad on 4th and 5th December 2009. Thetheme of this Convention was "Business Strategies for Economic Revival - Role of ManagementAccountants." The Chief Guest of this Convention and also Chairman of the Insurance Regulatory Authority,called for ICWAI to help with quality manpower to service the Insurance Sector. I also mentioned aboutthe necessity for revival of ICWAI to meet the current-day challenges. On this occasion, I congratulatedthe Hyderabad Chapter of Cost Accountants for effectively conducting the Regional Cost Convention2009.

5.2 Residential Regional Convention of NIRC:NIRC organized a Residential Regional Conference at Agra on 18th and 19th of December 2009. Thetheme of this Convention was "Transformational Journey - An Update on Changes." I was happy toparticipate in this Convention and the Member-CERC, Mr. Krishna Murthy, was the Chief Guest. Hisadvice to the Cost and Management Accountants to take up many challenges in the emerging sectorsincluding Electricity was well received by the audience. Our members were happy to note the challengesgiven by Shri Krishna Murthy that the Cost Accountants/Cost Auditors are also included for certifyingthe cost report on the tariff of Private Power Sectors apart from Chartered Accountants. I appreciated theinnovative idea of NIRC for making the Regional Convention as a Residential Regional Convention in avery meaningful atmosphere at Agra and it was a good deliberation of two days and members participatedin a big number.

5.3 Regional Cost Convention of EIRC:I congratulated the Rourkela Chapter of Cost Accountants for having taken the responsibility of holding thisConvention at Rourkela. The theme of this Convention also was apt for the current economic scenario.

I was also happy to address a grand 2-day Convention organized by Cochin and Thrissur Chapters on 20thand 21st November 2009 consisting of all the Chapters in Kerala. A good coverage of all the above eventshas appeared throughout Kerala. The theme of this Convention being "Cost Management - Key to EnterpriseExcellence."

While talking to the representatives of Gulf countries at Ooman, there was a lot of enthusiasm from themembers who are settled in Muscat and Bahrain to start Overseas Centres as is done in Dubai and otherplaces. I have advised the members in these countries to send the proposals, which will be good for us toserve the cause of Cost and Management Accountants in the Gulf region.

I am extremely happy to note that out of our visibility of ICWAI throughout the country, there is a goodnumber of increase in admission in all the Chapters and Regions. I congratulate all the members and theChapters for taking up this challenge. I am also happy to note that for over several years, for the first time,the number of people who are taking ICWAI examination has also crossed 43,000 and this adds to ourcapacity building programme of Cost and Management Accountancy.

With regards and wishing once again A HAPPY NEW YEAR.Yours sincerely

(GN Venkataraman)PresidentDate : 1st January, 2010

lPresident�s Communique l

10 the management accountant, January, 2010

EVA - MVA: Shareholders'Value MeasuresMaximizing shareholders value is becoming the new corporate standard in India.The corporates, which gave the lowest preference to the shareholders’inquisitiveness, are now bestowing the utmost inclination to it. Shareholders’value is measured in terms of the returns they receive on their investment. Thereturns can either be in the form of dividends or in the form of capital appreciationor both. Capital appreciation in turn depends on the subsequent changes in themarket value of shares. This market value of shares is influenced by a number offactors, which can be company specific, industry specific and macro-economicin nature.

To help corporates to generate value for shareholders, value basedmanagement systems have been developed. For measuring the corporate financialperformance, there are accounting profitability measures and shareholders’value based measures. Accounting profitability measures include ROI, ROE,EPS, ROCE and DPS etc., Shareholders valued based measures include EVAand MVA. Against this background, this article is an attempt to discuss theconcepts of EVA and MVA, evolution and growth of EVA, computation of EVAand MVA, EVA and financial performance, EVA in Indian environment andrelationship between EVA (Economic Value Added) and MVA (Market ValueAdded).

N. Sakthivel*

*Lecturer, PG & Research Dept. ofCommerce, Gobi Arts & Science College,Gobichettipalayam, Erode, Tamilnade-638453. E-Mail ID: sakthivel_ gasc @rediffmail.com

INTRODUCTION

M any companies in India andabroad have adopted theconcept of shareholders' value

added (SVA) in their annual statement.Value management is a technique ofintegrating the thinking aboutshareholder value throughout acompany. Two most important phasesof value management are: 1) EconomicValue Added (EVA) 2) Market ValueAdded (MVA). The company form oforganization's real owners are equityshareholders. They all invest theirmoney in equity shares of a companywith the primary motive of achievinggood capital appreciation and regular& stable return (i.e., dividends). Theinvestors' objectives are purely basedon the profitability and financial

performance of the company. So, beforetaking their investment decisions, theinvestors consider several factorswhich influence the corporateperformance. For measuring thecorporate financial performance, thereare accounting profitability measuresand shareholders' value basedmeasures. Accounting profitabilitymeasures include ROI, ROE, EPS, ROCEand DPS etc., Shareholders valuedbased measures include EVA, MVA.

Maximizing the shareholder valueisconsidered as one of the fundamentalgoals of all businesses. In United States,top management is expected to maximizeshareholder value. There are a numberof value based management (VBM)frameworks i.e. shareholder valueanalysis (SVA) Rapport (1986) andEconomic Value Analysis (EVA)developed by Stern Stewart (1990) arethe two well-known ones.

Maximizing shareholders value isbecoming the new corporate standard

in India. The Corporates, which gavethe lowest preference to theshareholders' inquisitiveness, are nowbestowing the utmost inclination to it.Shareholders' wealth is measured interms of the returns they receive on theirinvestment. The returns can either bein the form of dividends or in the formof capital appreciation or both. Capitalappreciation in turn depends on thesubsequent changes in the market valueof shares. This market value of sharesis influenced by a number of factors,which can be company specific,industry specific and macro-economicin nature. To help Corporates togenerate value for shareholders, valuebased management systems have beendeveloped. Indeed, value basedmanagement, which seeks to integratefinance hypothesis with strategiceconomic philosophy, is considered asone of the most significant contributionto corporate financial planning in thelast two decades or so. Against thisbackground, this article is an attempt todiscuss the concepts of EVA and MVA,evolution and growth of EVA,computation of EVA and MVA, EVA andfinancial performance, EVA in Indianenvironment and relationship betweenEVA and MVA (Market Value Added).

Market Value Added (MVA)With a view to measure share-

holders' value, Stewart invented theterm Market Value Added (MVA).Market Value Added (MVA) is definedas "the difference between market valueof invested capital and book value ofinvested capital of a company at a givenperiod of time". Market value ofinvested capital refers the market valueof equity capital and debt capital, butthe market value of debt is not easilyavailable as debts are not generallytraded. Thus, the definition of MVA canbe stated as market capitalization lessnet worth. Market capitalization is theproduct of closing share price andnumber of out standing shares as onthat date (i.e., date of balance sheet).Whereas, net worth is the sum of equitycapital, reserves and surplus net of

Cover Feature

the management accountant, January, 2010 11

revaluation reserve less accumulatedlosses and miscellaneous expenditure.

MVA = Market Capitalisation - NetWorthMarket Capitalisation = Closing SharePrice x Number of Outstanding Shares.Net Worth:

1. Equity Share Capital -2. Reserve and Surplus

(net of revaluation reserve) -Total -

Less:

1. Accumulated Losses -2. Miscellaneous Expenditure -

Net Worth -It is clear from the above definition

that MVA simply reflects the price tobook value relationship that is depictedby P/B ratio (Market price to book valueratio). The only difference betweenMVA and P/B ratio is that MVA is anabsolute measure whereas P/B ratio is arelative measure. A positive MVAimplies that P/B ratio is greater than one(P/B ratio > 1). If MVA is negative itimplies that P/B ratio is less than one(P/B ratio < 1). Therefore, it may beconcluded that MVA is the change inmarket value of a company between twodifferent points of time with referenceto a fixed quantity of outstandingshares. It may be noted that if thenumber of shares change between twogiven points of time, MVA should becalculated with reference to sharesoutstanding on the latest point of time.This would mean that the marketcapitalization at the end of current yearreflects the market value of outstandingshares at the end of current year. For ameaningful and objective comparison,market capitalization at the previous yearshould be modified to reflect thenumber of outstanding shares at theend of the current year.

MVA represents the value added toa particular share over its book value.MVA informs how much value ashareholder has added to this wealth,which he has invested in the share.Accordingly, a company with an

objective of enhancing the share-holders' wealth should attempt tocapitalize on its MVA. MVA can beestimated by subtracting the book valueof shares from the market value ofshares. It is silent that EVA helps inpushing up the MVA of an organization.As a result, EVA can be considered asan internal measure and MVA as theexternal measure of a company'sperformance.

MVA is considered as a measure ofshareholders' wealth. MVA denotes theextent to which the market has addedvalue to the net worth of a company.An increase in MVA infers maximizationof shareholders' wealth. This is becauseshareholders want to see appreciationin stock price. MVA can improve ifmarket capitalization increases for thesame level of net worth or if net worthof a company decreases. MVA providesthe stock market's assessment of howefficient a company is in using capital.A positive MVA indicates that acompany is building value for itsshareholders and a negative MVAindicates that a company is destroyingshareholders' value.

Economic Value Added (EVA)The concept of Economic Value

Added was introduced by a New Yorkbased consulting firm M/s Stern Stewart& Co in early eighties. The corporatesector in India is gradually recognizingthe importance of EVA as a result ofwhich some Indian companies viz.,Ranbaxy Laboratories, Samuel IndiaLtd.etc., have started calculating EVA.Infosys Technologies Ltd is the firstIndian company to report its EVA in theannual report. EVA attempts to measuretrue economic profit as it comparesactual rate of return as against therequired rate of return. EVA explainswhether a business unit best utilizes itsassets to generate return and maximizeshareholders' value. EVA is just a wayof measuring an operation's realprofitability. EVA effectively measuresthe productivity of all the factors ofproduction. viz., land, labour, capital,entrepreneur and management.

Economic Value Added (EVA) is aresidual income that subtracts the costof capital from the operating profitsgenerated by a business. EVA is anexcess profit of a firm after chargingcost of capital. EVA essentially seeksto Measure Company's actual rate ofreturn as against the required rate ofreturn. To put it simply, EVA is thedifference between Net Operating ProfitAfter Tax (NOPAT) and the capitalcharge for both debt and equity (WACC-Weighted Average Cost of Capital). IfNOPAT exceeds the capital charge(WACC), EVA is positive and if NOPATis less than capital charge, EVA isnegative. EVA is a corporate surplus,which is shared by the employees,management and the shareholders.Efficiency bonus, profit sharingschemes, managerial remuneration overand above minimum sustenance salary,issue of bonus shares and incentivedividend to equity and preferenceshareholders respectively can be linkedto EVA.

Evolution and Growth of EVAEVA is not a newer innovation. An

accounting performance measure calledresidual income that is defined asoperating profit subtracted with capitalcharge. EVA is thus, one variation ofresidual income with adjustments tohow one works out income and capital.According to Wallace, one of theearliest to point out the residual incomeconcept was Alfred Marshall in 1890.Marshall described economic profit astotal net gains less the interest oninvested capital at the current rate.According to Odd and Chen, the ideaof residual income appeared first inaccounting theory literature early in thiscentury. It was initiated by Church in1917 and further defined by Scovell in1924. Later, this concept appeared inmanagement accounting literature in the1960s.

Knowing this backdrop, severalresearchers have been wondering aboutthe big media hype and praise that hasencircled EVA in the recent days. TheEVA concept is recurrently called as

Cover Feature

12 the management accountant, January, 2010

Economic Profit (EP) in order to stayaway from problems caused by the trademarking. On the other hand, the nameEVA is so popular and well known thatoften all residual income concepts arecalled EVA although they do not takeaccount of even the main elementsdefined by Stern Stewart & companyfor the purpose. For instance, hardlyany of those Finish Companies thathave adopted EVA calculate rate ofreturn based on the beginning capitalas Stewart has defined it, becauseaverage capital is in practice a betterestimate of the capital employed. So,they do not actually use EVA but otherresidual income measures. Thisimmaterial detail is overlooked later onin order to avoid more severemisapprehensions and is foundjustified to say that the EVA concept,the Finish companies are usingcorresponds approximately the EVAdefined by Stern Stewart & Company.During 1970s, the residual incomeconcept did not get ample publicity andit did not finish up to be the primeperformance measure of companies.However EVA, practically, the sameconcept with a different name, has cometo fore in the recent years. Moreover,the propagation of EVA and otherresidual income measures does notseem to be on an abating trend. On thecontrary, the number of companiesadopting EVA is increasing rapidly. Onecan only guess why residual income didnever gain recognition of this level. Oneof the possible reasons is that EconomicValue Added was marketed with aconcept of Market Value Added (MVA)and it did not offer a hypotheticallysignificant connection to marketvaluations. In the times when investorsinsist on shareholders' value, this washigh time to sink your teeth into theconcept. The clarity that EVA hasbrought to the pursuit of shareholdervalue has led more than 400 companiesto adopt the discipline since SternStewart introduced the new system backin 1982. EVA has long had a base inSouth Africa, owing primarily to thelectures that Joel Stern gave before

academic and business groups. In thelast couple of years, EVA has fascinatedan increasing number of Corporatestogether in Europe, Asia, Australia andLatin America.

In mid-1996, Joel Stern was invitedto give a full- dress presentation on EVAto top management and later that year,the company signed up and formed anEVA Steering Group to implement EVA.As part of the initial phase of the EVAproject, Tate & Lyle decided to pilot EVAin two businesses-UM, UK-basedmolasses trading company andRedpath, a Canadian sugar refiner. Theobjective was to determine whether thetheory of EVA would be appropriate inpractice and to test the EVA groundrules formulated by Steering Group.

First, a retrospective study wasconducted to provide a record of pastEVA, against which future performancewas to be measured. The key valuedrivers were identified, especially in thecapital area, in addition to opportunitiesfor increasing NOPAT throughcontinuation of the existing costmanagement initiatives.

The pilot schemes were successfuland demonstrated the merits of EVA, notjust as a measure but also as a valuablemanagement tool. It was then decidedto roll out EVA throughout Tate & Lylebeginning with the training of all thefinance managers of the varioussubsidiaries followed by the operatingpeople. For the fiscal year that began inOctober 1997, some 60 of the topmanagers had their cash bonus linkedto EVA performance. EVA may berealistically in young age in the west,has been going through its babyhoodin country like ours. It may be quiteemerging concept in the mind of Indiancorporate policy makers and managers.

EVA and Financial Performance

According to accounting concept,business profit is measured bydeducting expenses from income earnedduring the period. On the other hand,according to economic concept,business profit is considered to be the

maximum amount that the business iscapable of distributing to itsshareholders while still remaining in thesame position at the end of the periodas it was at the beginning. Notably, theaccounting concept does not take intoaccount opportunity cost and riskadjusted return on capital employed inthe business in order to overcomelimitations of accounting basedmeasures of financial performance.

EVA as a tool of financialperformance measurement enlightenswhether the operating profit is enoughto cover the cost of capital.Shareholders must earn sufficientreturns for the risk they have taken ininvesting their funds in company'scapital. The return generated by thecompany for shareholders has to bemore than the overall cost of capital tojustify risk taken by shareholders. TheEVA framework is becoming more andmore admired tool for measuring thefinancial performance of Corporates.EVA offers a consistent approach to setgoals and measure performance,communicate with investors, evaluatestrategies, allocate capital valuingacquisitions and determine incentivebonuses. However, the EVAimplementation and improvementprocess is one of the several ongoinginitiatives for a new corporate. A firmcan improve its EVA in three ways:

l Earn more profit without using morecapital.

l Downsize unprofitable units ordivisions.

l Make investment where the returnis more than the marginal cost ofcapital.

Computation of EVA

EVA is the excess of Net OperatingProfit After Tax (NOPAT) over theWeighted Average Cost of Capital(WACC). In other words, EVA is acompany's net operating profit after taxafter deducting the cost of capitalemployed on total investment in thebusiness. EVA takes into account thetotal cost of capital employed which

Cover Feature

the management accountant, January, 2010 13

makes EVA so revealing. The traditionalpractice normally considers only asingle component of the total cost ofcapital (i.e., the explicit cost of borrowedcapital) to arrive at net profits. EVArecognizes explicit cost of borrowedcapital as well as implicit cost of owncapital as part of cost to be deductedfrom the figure of net operating profits.

While computing EVA, capitalemployed represents capital invested atthe beginning of the year. The logicbehind taking beginning capital forcomputing EVA is that a companywould take at least one year time to earna return on investment. It may bementioned here that calculation of EVAinvolves some tricky issues. Eachelement of EVA, therefore, has beendiscussed individually. EVA requiresthree different inputs for itscomputation. They are given below: (A)NOPAT (Net Operating Profit After Tax)B) Invested Capital (C) WeightedAverage Cost Of Capital (WACC).

EVA = NOPAT - (WACC x InvestedCapital)

(A) Net Operating Profit After Tax(NOPAT)

Stewart (1991) defined NOPAT asthe "Profits derived from company'soperations after taxes but beforefinancing costs and non-cash bookkeeping entries. Such non-cash bookkeeping entries do not includedepreciation since depreciation isconsidered as a true economic expense.In other words, NOPAT is equal to theincome available to shareholders plusinterest expenses (after tax). However,Stewart considered regular non-operating incomes as part of NOPAT.Stewart (1991) provided the followingcalculation for computing NOPAT:

1. Profit after tax -

2. Non-recurring expenses -

3. R&D expenditures -

4. Interest Expenses -

5. Provision for taxes -

TOTAL -

LESS:

1. Non-recurring incomes -

2. R&D amortization -

3. Cash operating taxes* -

NOPAT -

*Where, Cash Operating Taxes =(Provision for taxes + tax benefit ofnon-recurring expenses + Tax benefitof interest expenses) - (Tax on non-recurring incomes)

B) Invested Capital / Capital Employed

Invested capital or capital employedrefers to total assets net of non-interestbearing liabilities. From an operatingperspective, invested capital can bedefined as Net Fixed Assets plusInvestments plus Net current assets.Net current assets denote currentassets net of non-interest bearingcurrent liabilities. From a financingperspective, the same can be definedas Net Worth plus total borrowings.Total borrowings denote all interestbearing debts

(C) Weighted Average Cost of Capital(WACC)

WACC represents overall cost ofcapital employed in the business (i.e.,cost of debt capital and cost of equitycapital). For calculating WACC, cost ofeach source of capital is calculatedseparately then weights are assignedto each source on the basis ofproportion of a particular source in thetotal capital employed. Weights can beassigned on market value basis or bookvalue basis. Stewart suggested marketvalue basis. WACC can be calculatedas below:

WACC = E/CE ́ Ke + LTB/CE x Kd

Where,

E = Equity Capital

CE = Capital Employed

LTB = Long Term Borrowings

Ke = Cost of Equity Capital

Kd = Cost of Debt Capital

WACC includes two specific costs viz.,(i) cost of equity (Ke), (ii)cost of debt

(Kd).

I) Calculation of Cost of Debt (Kd)

Cost of debt is calculated bymultiplying the pre-tax debt cost by (1-t), Where't' refers the effective tax rate.This will furnish the post tax cost ofdebt. The post tax cost of debt iscalculated because debt cost enjoys taxshield. In other words, tax reduces theeffective cost of debt. Cost of debt canbe calculated by applying the followingformula:

Cost of Debt = (Total Interest Expense /Beginning Total Borrowings)

(1-t)´100

Kd = (TIE / BTB) x (1-t) x 100

II) Calculation of Cost of Equity (Ke)

Cost of equity (Ke) is theopportunity cost that is equal to the totalreturn that investor could expect to earnfrom alternative investments ofcomparable risk. It is not an explicit costas the cost of debt. The dividend basedor earning based approach for findingcost of equity is not considered a properway of computing the return expectedby equity shareholders. Theseapproaches measure the explicit cost ofservicing equity whereas the truemeasure of cost of equity is not what acompany offers but what investorsreasonably expect. Conceptually, thecost of equity may be stated as "theminimum rate of return that a companymust earn on the equity-financialposition of an investment project inorder to leave unchanged the marketprice of the shares". The cost of equitycan be calculated by the Capital AssetPricing Model (CAPM). The CAPM isnormally used to determine minimumrequired rates of return from investmentin risky assets. Stewart also usedCAPM consistently as a measure forcost of equity in his methodology forcomputing EVA. The expected return onequity can be calculated under CAPMby applying the formula given below:

Rj = Rf + b (Rm - Rf)

Where,

Cover Feature

14 the management accountant, January, 2010

Rj = Expected Return on Scrip j

Rf = Risk free rate of return

b = Beta representing the volatilityof scrip j against marketvolatility.

Rm = Expected stock market return.

From the above formula, it can beconcluded that the required rate ofreturn on equity is equal to the sum ofthe risk-free rate of return and anincrement that compensates theinvestors for accepting the assets risk.

EVA in Indian Environment

Bennett Stewart, along with JoelStern founded the New York-basedglobal financial consultancy firm underthe name "Stern Stewart & Company"in 1990. An EVA company has believedthat EVA is such financial performancetool that comes closer than any othertools to capture the true economic profitof an organization. The EVA analysishas attracted much attention in theWestern countries both as amanagement innovation as well as stockmarket analysis. The acceptance ofsuch a technique in Indian context,however, shows somewhat diversetrends. Some corporate houses likeInfosys, BPL, Hindustan Lever Limited,Balarpur Chinni Mills, NIIT, TataConsultancy Services, Godrej Soapshave started publishing EVA in theirfinancial statements. Majority ofcompanies are still not willing to installthe EVA technique for evaluating theirfinancial performance because ofcertain inherent difficulties associatedwith the computation. Again, it isobserved by some scholars that inIndian context, it may be very difficulttask to establish the existence of anyrelationship between stock price andeconomic value added (EVA).

In developing economy like India,depending on EVA could be an obstaclein making new investment decisions.Moreover, when talking aboutshareholders' value, the profile of theshareholders also needs to be taken

care. In India, for a particular businessor company there is no one particularset of shareholders. In fact, there isalways more than one set. Thensituations may arise when the companyends up satisfying one set ofshareholders at the cost of another set.In India, we have large businesshouses, which started off with onebusiness but diversified during thecourse of time. In the entire process,they ended up creating many sets ofshareholders thus making the spread ofvalue creation all the more complicated.Considering all these situations whatbecomes important is reporting andtransparency & consistency inreporting which can assure the successof EVA to some extent.

EVA, MVA and Share Prices

The EVA theory defines marketvalue of a company as its book valueplus the current value of future EVA.Through this relationship, EVAinfluences market value of shares butthis relationship is again debated anddifferent studies have revealed differentresults. Stewart studied the relationshipbetween EVA and MVA by takingmarket data of 618 US firms and Stewartfound that the relationship between EVAand MVA is quite high in US firms. Butin situation, where both EVA and MVAare negative and the relationship doesnot hold good. The reason behind thisbehaviour is that the market valuereflects the asset base of companiesand the companies, which have highasset base will also, have high marketvalues irrespective of their returns. Incase of low or negative EVA, the marketstart valuing the companies on thepotential of liquidation, recovery,recapitalization or takeover, but if theEVA is positive, then the valuation ison the basis of expected return andgrowth potential and not on the basisof liquidation or recovery value.

While establishing a correlationbetween EVA and MVA, it is best toconsider the change rather than the

absolute figures. Considering changesin the value is safer because they arenot affected much by accountingdistortions and inflation than theabsolute values. There is onefundamental question in correlatingEVA with share prices i.e. the main basefor market value is the expectation offuture cash flows. The change in thecurrent share price is a reflection of thechange in the future cash flows andfuture EVA expectations. Hence, thecurrent EVA cannot explain the currentshare price. When the current EVAchanges, it infers that the future EVA isalso likely to change. Therefore, likeother measures, EVA also has the powerto explain, may be a little more strongly.EVA is more appropriate in case ofcorporate control and the use of EVAas discounted cash flow to estimatecurrent valuations with future EVAestimate is really informative. More thanthe share price, EVA has morecorrelation with MVA. Share prices canalso rise when more money is pumpedup into the business, but EVA and MVArise only when the returns generatedwith the additional money is more thanthe incremental cost of capital. One ofthe reasons of poor correlation betweenEVA and share price is distorted. EVA isno better than any other accountingmeasure like ROI or EPS. Also, thesedistortions could be responsible for thefact that more than absolute valuechanges in EVA correlates with shareprices.

EVA reflects the true economic profitof an organization. It is an internalmeasure of performance oforganisations. In order to make EVAmore popular in Indian environment, itis essential to remove many practicaldifficulties in implementing EVA inbusiness houses. It can be concludedthat maximizing shareholders' value isthe primary objective of any businessorganization and it should be kept inmind that change is the only way, which

Cover Feature

Contd. on Page 18

the management accountant, January, 2010 15

Business Valuation:A Critical AnalysisDr. Arindam Ghosh*Sri Asit Gope**Introduction:

B usiness valuation is ameasurement process. In orderfor any measurement process to

be useful, the results must be consistent,precise, and accurate. Unlike ordinaryphysical measurements, the businessvaluation process involves multiplequalitative judgements, as well asquantitative procedures. To achievegreater precision and consistency,valuation professionals have attemptedto make the valuation process moredependent on quantitative proceduresand less dependent on qualitativejudgements. Qualitative judgementsoften are thought to be inherently moresubjective and prone to bias thanquantitative procedures. Despite thefact that qualitative judgements are notnecessarily biased in principle, inpractice such judgements are often thesource of biased and inconsistentappraisal results. Many users ofbusiness valuations have noted thisproblem. Business valuation is a processor a set of procedures that is used toestimate the economic value of theowner's interest in a business. Valuationis used by financial market participantsto determine the price they are willingto pay or receive to consummate a saleof a business. Business valuationresults can vary considerablydepending upon the choice of both thestandard and premise of value. In an

actual business sale, it would beexpected that the buyer and seller, eachwith an incentive to achieve an optimaloutcome, would determine the fairmarket value of a business asset thatwould compete in the market for suchan acquisition. Valuing a company ishardly a precise science and can varydepending on the type of business andthe reason for coming up with avaluation. There are a wide range offactors that go into the process -- fromthe book value to a host of tangible andintangible elements. In general, thevalue of the business will rely on ananalysis of the company's cash flow. Inother words, its ability to generateconsistent profits will ultimatelydetermine its worth in the marketplace.Business valuation should beconsidered a starting point for buyersand sellers. It is rare that buyers andsellers come up with a similar figure, if,for no other reason, than the seller islooking for a higher price. The goal ofthe valuation should be to determine aapproximate figure from which thebuyer and the seller can negotiate aprice that they can both live with.

The Need for Valuation:

The need for valuing a business ora firm can well be identified byanswering the question-"Whatpurpose does a valuation serve?". Toanswer that question we have toconsider the benefits that are gained bydifferent parties, directly or indirectlyengaged their interests in the businessconcerned. To judge that we need tocalculate the view points of all theparties who are directly or indirectlyconnected with the business. Thepurposes that a valuation serves are

*Reader and Head, Department ofCommerce, Panihati College ; Life Member:Indian Economic Association & BengalEconomic Association.**Research Scholar, Department ofCommerce, University of Kalyani.

manifold. A valuation may be used fora wide range of purposes. These arelisted as follows:

q From the buyer's point of view, thevaluation tells him the price heshould pay;

q From the seller's point of view, thevaluation will tell him the lowestprice at which he should be preparedto sell;

q In case of listed companies:

- valuation is useful to compare thevalue obtained with the share's priceon the stock market and to decidewhether to sell, buy or hold theshares;

- valuation of several companies maybe used to make portfolio decision;

q When share are offered to public,the valuation is used to justify theprice at which the shares are offeredto the public;

q The valuation is used to comparethe shares' value with that of theother assets;

q Valuation of a company provides afundamental benchmark to identifyand stratify the main value drives;

q The valuation of a company orbusiness unit is a prior step inmaking strategic decisions, such as,the decision to continue in thebusiness, sell, merge, grow or buyother companies;

q In case of strategic planning, thevaluation of the company and thedifferent business units arefundamental for deciding whatproducts/business lines/countries/customers to maintain, grow orabandon. It also provides means formeasuring the impact of thecompany's possible policies andstrategies on value creation anddestruction;

Different Approaches or Methods toBusiness Valuation:

A Business Valuator (or anyonevaluating your business) will use a

Cover Feature

16 the management accountant, January, 2010

variety of business valuation methodsto determine a fair price for yourbusiness, such as:

(1) Asset-Based Approach:

It is used when a company is asset-intensive. The most common assetvaluation techniques are:

Book Value Method:

The book value is simply thebusiness valuation based upon theaccounting books of the business.Assets less liabilities equal the owner'sequity, which is the "Book Value" of thebusiness. The problem with book valuebusiness valuation is that theaccounting records may not accuratelyreflect the true value of the assets inthe business valuation.

Adjusted Book Value:

Two types of adjusted book valuebusiness valuations are Tangible BookValue and Economic Book Value (alsoknown as book value at market).

l Tangible Book Value is based oncomprising the value of tangibleassets only. Assets, such, goodwill,patents, capitalized preliminaryexpenses and deferred revenueexpenses etc are not considered.

l Economic Book Value is the valueof the business that allows a bookvalue analysis that adjusts theassets to their market value. Thisincludes valuation of goodwill, realestate, inventories and other assetsat their market value.

Replacement Value Method:

It is quite closely similar to anadjusted book value analysis. Liabilitiesare deducted from the replacement valueof the assets to determine thereplacement value of the business.Replacement value of an asset is usuallyhigher than its book value.

Liquidation Value Method:

It is lso similar to an adjusted bookvalue analysis. Liabilities are deductedfrom the liquidation value of the assetsto determine the liquidation value of the

business. A liquidation asset-basedapproach determines the net cash thatwould be received if all assets were soldand liabilities paid off.

(2) Income/Earning-Based Approaches:

These valuation methods are bestused for non-asset intensive businesseslike service companies. These businessvaluation methods are predicated on theidea that a business's true value lies inits ability to produce wealth in thefuture. The most common earning valueapproach is Capitalizing Past Earning.

Income Capitalizing Valuation Method:

Earnings are divided by acapitalization rate (a rate of returnrequired to take on the risk of operatingthe business). The earnings figure tobe capitalized should be one that reflectsthe true nature of the business. Whendetermining a capitalization rate oneshould compare with rates available tosimilarly risky investments.

Discounted Earnings ValuationMethod:

It determines the value of a businessbased upon the present value ofprojected future expected earnings,discounted by the required rate of returni.e. the capitalization rate. But thequestion is how well earnings areprojected.

Discounted Cash Flow ValuationMethod:

When an entity is set up toaccomplish a specific project, thistechnique is proved to be the mostuseful in valuing such an affair orbusiness and when a certain time frameis set where an investor wishes to seehis investment returned over a specificperiod of time. In discounted cash flow,the present value of liabilities issubtracted from the combined presentvalue of cash flow and tangible assets,which determines the value of thebusiness.

Discount Rate:

In order to compute net present

value, it is necessary to discount futurebenefits and costs. This discountingreflects the time value of money.Benefits and costs are worth more ifthey are experienced sooner. All futurebenefits and costs, including non-monetized benefits and costs, shouldbe discounted. The higher the discountrate, the lower is the present value offuture cash flows. For typical invest-ments, with costs concentrated in earlyperiods and benefits following in laterperiods, raising the discount rate tendsto reduce the net present value.

Estimating the Discount Rate

Use of a discount rate to quantifysystematic and unsystematic risk is partof the Capital Asset Pricing Model(CAPM). CAPM is firmly grounded ineconomic theory, and many textscontain summaries. However, it is alsobased on publicly-traded markets, whichare not applicable to privately-heldfirms. Alternatively, some practitionersmay use a "build-up" method.Although the use of this term is notconsistent, some "build up" methodsdo not include a "beta." This approachis not founded in economic theory andis instead based heavily on professionaljudgement. Damadoran (2002)recommends the CAPM approach,noting the failure of more contemporarymodels to significantly improve uponCAPM. Different methods forestimating a discount rate exist.

(3) Market Valuation Approaches:

Market value approaches tobusiness valuation attempt to establishthe value of the business by comparingit to similar businesses that haverecently sold. Obviously, this methodis only going to work well if there are asufficient number of similar businessesto compare. This approach comparessimilar companies on a set of variables.For instance the value of a businesscould be determined by using an"industry average" figure, such assales, times a multiplier. This industryaverage number is based on what

Cover Feature

the management accountant, January, 2010 17

comparable businesses have sold forrecently. As a result, an industry-specific formula is devised, usuallybased on a multiple of gross sales.

Price Earnings Multiple ValuationMethods:

The price-earnings ration (P/E) issimply the price of a company's shareof common stock in the public marketdivided by its earnings per share.Multiply this multiple by the net incomeand you will have a value for thebusiness. If the business has noincome, there is no business valuation.

Dividend Capitalization ValuationMethod:

Dividend paying capacity based onaverage net income and on average cashflow is used.

To determine dividend-payingcapacity, near term capital needs,expansion plans, debt repayment,operation cushion, contractualrequirements, past dividend payinghistory of a business and dividends ofa comparable company should beinvestigated. After analyzing thesefactors, percent of average net incomeand of average cash flow that can beused for the payment of dividends canbe estimated.

Sales Multiple Valuation Method:

This method is easy to understandand use. The sales multiple is often usedas the business valuation benchmark.The information required is annual salesand an industry multiplier, which isusually a range of .25 to 1 or higher. Theindustry multiplier can be found invarious financial publications, as wellas analyzing sales of similar concerns.

Profit Multiple Valuation Method:

Profit and sales multiples are themost widely used business valuationbenchmarks used in valuing a business.The information needed is pretax profitsand a market multiplier, which may be 1,2, 3, or 4 and usually a ceiling of 5. Themarket multiplier can be found in variousfinancial publications, as well as

analyzing the sale of comparablebusinesses.

The above mentioned three mainapproaches are recognized by theInternal Revenue Service, accountingand appraisal authorities, andbusiness valuation authorities.However, much recent research in theunderlying economics of businessvaluation, as well as the trend inprofessional practice, has underminedthis easy classification. In particular,there has been severe criticism of theimproper use of accounting-basedhistorical cost figures to estimatemarket value, the reliance onaccounting income statements as thefundamental basis for forecastingfuture revenue, and the naiveapplication of CAPM models to thediscount rates for private firms.

What is Market Value or Fair Value?

The value of an asset if it were to besold on the open market at its currentmarket price. When land is involved itmay be necessary to distinguishbetween the market value in its presentuse and that in some alternative use;for example, a factory site may have amarket value as a factory site, and be sovalued in the company's accounts,which may be less than its market valueas building land. Market value is oftendifferent from book value because themarket takes into account future growthpotential. Most investors who usefundamental analysis to pick stockslook at a company's market value andthen determine whether or not themarket value is adequate or if it'sundervalued in comparison to its bookvalue, net assets or some other measure.The value of a company obtained bymultiplying the number of its issuedordinary shares by their market price.This may differ widely from the bookvalue of the company. Fair value is theamount of money for which it isassumed an asset or liability could beexchanged in an arm's lengthtransaction between informed and

willing parties. The concept is essentialin acquisition accounting.

Conclusion:

Business valuation methodologycontinues to evolve over time. Forexample, a century ago, the mostcommon business valuation methodsrelated to asset values and dividendyields. These business valuationmethods are given far less weight today.A half-century ago, the price/earningsmultiple and the multiple of price to cashflow per share were important businessvaluation components. While the price/earnings multiple continues to be animportant valuation component, theprice/cash flow multiple is no longergenerally accepted. The DCF(Discounted Cash Flow) method hasbecome a widely used businessvaluation method. The DCF method isconceptually useful, but it hassignificant application limitations. Themethod is based on the premise that thevalue of a business is the present valueof its future net cash flow. Projected netcash flow is discounted to present valueusing a cost of capital that is intendedto reflect the risks of the business.Because cash flow projections are madefor only a limited period, the value of abusiness at the end of the discreteprojection period is calculated. Thetheory of a DCF analysis assumes thevalidity of the financial projections, butfinancial projection accuracy is asimplifying assumption that does notoften comport with the real world.Moreover, a DCF analysis is also highlydependent on the selected discountrate, as well as the methodology usedfor estimating the terminal value. Often,the terminal value is based on theprojected financial results for the yearafter the discrete projection period.Terminal value is based on the final yearof a projection, which is necessarily farless predictable than projections forearlier years. Valuation is an importantconsideration, but the decision makersshould also consider the structural

Cover Feature

18 the management accountant, January, 2010

fairness of the transaction and otherfactors. A fairness conclusion renderedto the board of directors should weighthe overall impact of a transaction onshareholders. An analyst rendering afairness opinion should recognize thatshareholders are the ultimatebeneficiaries of the fairness conclusionand that the shareholders will beconsidering the fairness opinion inarriving at their transaction decisions.The CAPM is widely accepted forfinancial analysis, portfoliomanagement, corporate planning, andother applications. However, itsreliability in calculating the appropriatediscount rate for an individual companyis subject to question. Many of thefactors used in estimating the discountrate, such as beta, the company-specificrisk premium, and the small company/size adjustment risk premium, aresubject to the judgment of the analyst.Under the CAPM, a company's cost of

equity is determined by adding the risk-free rate of return to a measure of theequity risk premium. A company'sequity risk premium is calculated bymultiplying the equity risk premium forthe market as a whole by a factor calledbeta. Beta is a measure of the volatilityof an individual security's return relativeto the total market return. Ideally,valuation analysts should use aforward-looking beta. In practice,though, historical betas are commonlyused because projected betas are notreadily available. An analyst shouldtest the reasonableness of thecalculated cost of capital, based on theanalyst's professional judgement andexperience as to the rates of returnrequired in the marketplace.

Bibliography:

1. Waldron D and D Hubbard, (1991)"Valuation Methods and Estimates inRelationships to Investing VersusConsulting" Entrepreneurship: Theory

and Practice, Fall Volume 16,November 1.

2. Shanno P Prat (2001) "The MarketApproach to valuing Business" JohnWiley & Sons Inc.

3. Barth, M.E., W.H. Beaver and W.R.Landsman (2001). "The Relevance ofthe Value Relevance Literature forAccounting Standard Setting: AnotherView." Journal of Accounting andEconomics 31: 77-104.

4. Magni, C. A. (2007). Project valuationand investment decisions: CAPMversus arbitrage. Applied FinancialEconomics Letters, 3(1) (March), 137-140.

5. Fernández, P. (2002). ValuationMethods and Shareholders ValueCreation. San Diego: Academic Press.

6. Damodaran, A. (1999). AppliedCorporate Finance: A User's Manual.New York: Wiley.

7. Fernandez, Pablo (2002), ValuationMethods and Shareholder ValueCreation, Academic Press.q

is constant in nature. Obliterationshould be welcomed if it is for betterand the managers of publicorganisations should take decisions.As if it is a private organization that thecapital is optimally utilized and result inmaximizing the shareholders' value.

Conclusion

Shareholders' value based measureslike Economic Value Added (EVA),Market Value Added (MVA) are beingintroduced and greater attention isbeing paid to getting the accountantsand the finance executives involved inplanning, decision making andperformance evaluation in recent timesas these metrics explicitly discloses thevalue of the firms. These value basedmetrics are widely used by themanagement of a business in order tolook for a way to link earnings andrelated investment, not just for thecompany as a whole, but for theindividual parts of the business as MVA

and EVA are an effective measure of thequality of managerial decisions as wellas a reliable indicator of an enterprise'svalue growth in future. So, managementof business has now startedinvestigating ways to link its owninterest to the interest of theshareholders. Due to the abovedevelopments, economic value added(EVA) and market value added (MVA)are given the most attention and mostof the companies in India, either MNCor Indian have now adopted use ofabove first class metrics in recent times.

References:

l Singh K.P. and Garg M.C, "EconomicValue Added (EVA) in IndianCorporates", First Edition, Deep &Deep Publications Pvt Ltd, New Delhi,2004.

l Sony Agarwal, "Value AddedStatement", First Edition, RBSAPublishers, Jaipur, 2004.

l Anand, Manoj, Garg, Ajay, and Arora,Asha, "Economic Value Added:Business performance measure ofshareholders' value", The ManagementAccountant, May 1999, Vol. 34, No. 3,pp. 351-356.

l Niranjan, Swain, Mishra, C.S andMukesh Kumar, "Market Response toEconomic Value Maximization: A Studyof Indian Chemical Industry", TheICFAI Journal of Applied Finance, Vol.8, No. 4, July 2002, p. 3

l Banerjee, Ashok and Jain, "EconomicValue Added and Shareholder Wealth:An Empirical Study of Relationship",Paradigm, Vol. 3, No. 1, January-June,1999, p.114.

l www.eva.com

l Ghosh T.P, "Economic Value Added -A Tool for Business Planning", FirstEdition, The Institute of Cost and WorksAccountants of India (ICWAI),Kolkatta, 1999.q

Contd. from Page 14

Cover Feature

the management accountant, January, 2010 19

Tools and Techniques ofBusiness ValuationBusiness valuation is a process and a set of procedures used to estimate theeconomic value of an owner's interest in a business. Valuation is used by financialmarket participants to determine the price they are willing to pay or receive toconsummate a sale of a business. In addition to estimating the selling price of abusiness, the same valuation tools are often used by business appraisers toresolve disputes related to estate and gift taxation, divorce litigation, allocatebusiness purchase price among business assets, establish a formula for estimatingthe value of partners' ownership interest for buy-sell agreements, and manyother business and legal purposes. An attempt has been made in this article toprovide knowledge regarding the various tools and techniques that are used inthe valuation of a business, starting with simple financial statements and the useof ratios, and going on to discounted free cash flow and option-based methods.

Dr. Tanuja Talwar*Pooja Sareen**

*Lecturer, Postgraduate Department ofCommerce in Govt. College, Chandigarh.**Guest Faculty, Postgraduate Departmentof Commerce in Govt. College, Chandigarh.

Introduction

Business Valuation has become anintrinsic part of the corporatelandscape. The corporate

landscape has witnessed dynamicchanges in the recent years as mergersand acquisitions, corporate restruc-turings, and share repurchases arehappening in record numbers. At thecore of the dynamics of all theseactivities stands some notion ofvaluation. The valuation methods arenot only necessary for accountingpurposes but they also serve asroadmaps for the investors, venturecapitalists and corporate acquirers inorder to know the true value of acompany's assets. How a business isvalued depends on the purpose, so themost interesting part of implementingvarious methods will be to see how theywork in different contexts -- such asvaluing a private company, valuing anacquisition target, and valuing acompany in distress. Although there arenumerous individual valuationtechniques, we will discuss the

following prominent techniques ofbusiness valuation :

(1) Cash to Market Value Method

It is one of the premier screens forferreting out companies with more cashon hand than their current market value.Firstly look at a company's cash andequivalents and short-terminvestments. Dividing this number bythe number of shares outstanding givesa quick measure that tells us how muchof the current share price consists ofjust the cash that the company has onhand. Buying a company with a lot ofcash can yield a lot of benefits -- cashcan fund product development andstrategic acquisitions and can pay high-caliber executives. Even a company thatmight seem to have limited futureprospects can offer tremendous promiseif it has enough cash on hand.

(2) Working Capital to MarketCapitalization

Another measure of value is acompany's current working capitalrelative to its market capitalization.Working capital is what is left aftercompany's current liabilities aresubtracted from its current assets .Working capital represents the fundsthat a company has ready access to for

use in conducting its everydaybusiness. If we buy a company for closeto its working capital, we haveessentially bought a Re of assets for aRe of stock price -- not a bad deal, either.Just as cash funds all sorts of goodthings, so does working capital.

(3) Price to Book Value MethodBook value is literally the value of a

company that can be found on theaccounting ledger. To calculate bookvalue per share, take a company'sshareholder's equity and divide it by thecurrent number of shares outstanding.If you then take the stock's current priceand divide by the current book value,you have the price-to-book ratio.

Stock's current pricePrice to Book Value =-----------------------

Current book value

Book value is a relativelystraightforward concept. The closer tobook value we can buy something at,the better it is. Book value is actuallysomewhat skeptically viewed in this dayand age, since most companies havelatitude in valuing their inventory, aswell as inflation or deflation of real estatedepending on what tax consequencesthe company is trying to avoid.However, with financial companies likebanks, consumer loan concerns,brokerages and credit card companies,the book value is extremely relevant. Forinstance, in the banking industry,takeovers are often priced based onbook value, with banks or savings &loans being taken over at multiples ofbetween 1.7 to 2.0 times book value.Another use of shareholder's equity isto determine return on equity .

(4) Return on Equity (ROE)Return on equity is a measure of

how much earnings a companygenerates in four quarters compared toits shareholder's equity. It is measuredas a percentage. For instance, if XYZCorp. made a return of Rs one million inthe past year and has a shareholder'sequity of ten million, then the ROE is10%. Some use ROE as a screen to findcompanies that can generate largeprofits with little in the way of capital

Cover Feature

20 the management accountant, January, 2010

investment. Coca Cola, for instance,does not require constant spending toupgrade equipment -- the syrup-makingprocess does not regularly move aheadby technological leaps and bounds.High ROE companies are very attractiveto investors .(5) Earnings Per Share (EPS)

Earnings per share measures theprofit available to equity shareholderson a per share basis, i.e., the amountthat they can get on every share held.EPS is calculated by simply dividing thetotal amount of the earnings a companyreports by the number of shares itcurrently has outstanding. Thus, if XYZCorp. has 1million shares outstandingand has earned Rs.1million in the past12 months, it has EPS of Rs1.00.

Rs1,000,000EPS= -------------- = Re.1.00 1,000,000 shares

The earnings per share alone meansabsolutely nothing, though. To look ata company's earnings relative to itsprice, we can employ the price /earningratio.(6) Price/Earnings (P/E) Ratio.

The P/E ratio takes the stock priceand divides it by the last four quarters'worth of earnings. For instance, if, inour example above, XYZ Corp. wascurrently trading at Rs15 a share, itwould have a P/E of 15.

Rs.15 Share priceP/E=-------------------------- = Rs.15

Rs.1.00 EPSIt represents the price currently

being paid by the market for each Re ofcurrently reported EPS. It measuresinvestors expectations and marketappraisal of the performance of the firm.(7) The Price-to-Sales Ratio

Every time a company sells acustomer something, it is generatingrevenues. Revenues are the salesgenerated by a company for peddlinggoods or services. Whether or not acompany has made money in the lastyear, there are always revenues. Evencompanies that may be temporarilylosing money, have earnings depresseddue to short-term circumstances (like

product development or higher taxes),or are relatively new in a high-growthindustry are often valued off of theirrevenues and not their earnings.Revenue-based valuations are achievedusing the price/sales ratio,PSR.Theprice/sales ratio takes intoconsideration the current marketcapitalization of a company and dividesit by the last 12 months trailingrevenues. The market capitalization isthe current market value of a company,arrived at by multiplying the currentshare price times the sharesoutstanding. This is the current price atwhich the market is valuing thecompany. For instance, if in our example,company XYZ Corp. has ten millionshares outstanding, priced at Rs10 ashare, then the market capitalization isRs100 million.Some investors are evenmore conservative and add the currentlong-term debt of the company to thetotal current market value of its stock toget the market capitalization. The logichere is that if we were to acquire thecompany, we would acquire its debt aswell. This avoids comparing PSRsbetween two companies where one hastaken out enormous debt that it hasused to boast sales and one that haslower sales but has not added any nastydebt either.Market Capitalization = (SharesOutstanding * Current Share Price)

+ Current Long-term DebtThe next step in calculating the PSR

is to add up the revenues from the lastfour quarters and divide this numberinto the market capitalization. Say XYZCorp. had Rs200 million in sales overthe last four quarters and currently hasno long-term debt. The PSR would be:

(10mnshares*10/share)+0debtPSR = ------------------------------------- = 0.5

Rs200 million revenuesThe PSR is a measurement that

companies often consider when makingan acquisition. The PSR is often usedwhen a company has not made moneyin the last year. PSR measures how muchwe are paying for a Re of sales insteadof a Re of earnings. We can use the PSRin conjunction with the P/E in order to

confirm value. If a company has a lowP/E but a high PSR, it can warn aninvestor that there are potentially someone-time gains in the last four quartersthat are pumping up earnings per share.(8) Discounted Cash Flows Method

It is the most common measurementfor valuing public and privatecompanies used by investment bankers.Cash flow is literally the cash that flowsthrough a company during the courseof a quarter or the year after taking outall fixed expenses. Cash flow is normallydefined as earnings before interest,taxes, depreciation and amortization(EBITDA).In a private or public marketacquisition, the price-to-cash flowmultiple is normally in the 6.0 to 7.0range. When this multiple reaches the8.0 to 9.0 range, the acquisition isnormally considered to be expensive.In a leveraged buyout (LBO), the buyernormally tries not to pay more than 5.0times cash flow because so much of theacquisition is funded by debt.

Free Cash Flow goes one stepfurther. A company cannot drain all itscash flow, to survive and grow it mustinvest in capital and hold enoughinventory and receivables to supportits customers. So after adding back inthe non-cash items, we subtract out newcapital expenditures and additions toworking capital.

The premise of the discounted freecash flow method is that company valuecan be estimated by forecasting futureperformance of the business andmeasuring the surplus cash flowgenerated by the company. The surpluscash flows and cash flow shortfalls arediscounted back to a present value andadded together to arrive at a valuation.The discount factor used is adjustedfor the financial risk of investing in thecompany. The mechanics of the methodfocus investors on the internaloperations of the company and itsfuture.

The discounted cash flow methodcan be applied in six distinct steps. Sincethe method is based on forecasts, agood understanding of the business,its market and its past operations is a

Cover Feature

the management accountant, January, 2010 21

must. The steps in the discounted cashflow method are as follows:l Develop debt free projections of the

company's future operations. Thisis clearly the critical element in thevaluation.

l Quantify positive and negative cashflow in each year of the projections.The cash flow being measured is thesurplus cash generated by thebusiness each year. In years whenthe company does not generatesurplus cash, the cash shortfall ismeasured.

l Estimate a terminal value for the lastyear of the projections. Estimate howmuch value will be contributed tothe company by the cash flowsgenerated after the last year in theprojections.

l Determine the discount factor to beapplied to the cash flows. Thisdiscount factor should reflect thebusiness and investment riskinvolved.

l Apply the discount factor to thecash flow surplus and shortfall ofeach year and to the terminal value.The amount generated by each ofthese calculations will estimate thepresent value contribution of eachyear's future cash flow. Addingthese values together estimates thecompany's present value assumingit is debt free.

l Subtract present long term and shortterm borrowings from the presentvalue of future cash flows toestimate the company's presentvalue.

(9) Option-Based MethodsExecutives continue to grapple with

issues of risk and uncertainty inevaluating investments andacquisitions. Despite the use of netpresent value (NPV) and othervaluation techniques, executives areoften forced to rely on instinct whenfinalizing risky investment decisions.Given the shortcomings of NPV, realoptions analysis has been suggestedas an alternative approach, one thatconsiders the risks associated with an

investment while recognizing the abilityof corporations to defer an investmentuntil a later period or to make a partialinvestment instead. In short, investmentdecisions are often made in a way thatleaves some options open. The simpleNPV rule does not give the correctconclusion if uncertainty can be"managed." In acquisitions and otherbusiness decisions, flexibility isessential -- more so the more volatilethe environment -- and the value offlexibility can be taken into accountexplicitly, by using the real-optionsapproach.

Financial options are extensivelyused for risk management in banks andfirms. Real or embedded options areanalogs of these financial options andcan be used for evaluating investmentdecisions made under significantuncertainty. Real options can beidentified in the form of opportunity toinvest in a currently availableinnovative project with an additionalconsideration of the strategic valueassociated with the possibility of futureand follow-up investments due toemergence of another relatedinnovation in future, or the possibilityof abandoning the project.

The option is worth somethingbecause the future value of the asset isuncertain. Uncertainty increases thevalue of the option, because if theuncertainty is interpreted as thevariance, there are possibilities tohigher profits. The loss on the option isequal to the cost of acquiring it. If theproject turns out to be non-profitablewe always have the choice of non-exercising. More and more, the realoptions approach is finding its place incorporate valuation.Conclusion

The firms that face an importantinvestment, acquisition, or growthdecisions, particularly in a rapidlychanging competitive environment,effective management requires anunderstanding of value creation and acommand over valuation analysis.While valuing a business we should notrely on any one method rather we

should select combination of methodsthat can help us to take betterdecisionWe all know very well that onewrong decision can destroy the valuecreated over the years. Financial expertsbelieve that business valuations usingany method should not be too high ortoo low because that could be costly,resulting in either overpayment or lostopportunities. It is the need of the hourthat the executives belonging to financeor non finance background mustpossess thorough understanding of allthe available valuation techniquesbecause they play an important role inthe various strategic decisions taken bythe corporates.

Referencesl Anderson, Patrick Lee., Business

Economics and Finance, Chapman &Hall/CRC, 2005.

l Anderson, Patrick L., "NewDevelopments in Business Valuation."Developments in Litigation Economics.Ed.s P.A. Gaughan and R.J. Thornton,Burlington: Elsevier, 2005.

l Damodaran, Avanish. InvestmentValuation, New York, Wiley, 1996.

l Fishman, Pratt, Morrison, Standards ofValue: Theory and Applications, JohnWiley & Sons, Inc., NJ, 2007.

l Gaughan, Patrick A., MeasuringBusiness Interruption Losses, JohnWiley & Sons, Inc., NJ, 2004.

l Hitchner, James R., ed., FinancialValuation, McGraw-Hill, 2003.

l Mercer, Christopher, "Fair MarketValue vs. The Real World," ValuationStrategies, March 1999; reprint