Mise en page 1 - Tunisie Valeurs · rESEARCH R E P O R T February 2011 TUNISJerusalemBranch...

24

rESEARCH REPORT February 2011 TUNIS Jerusalem Branch 17, rue de Jérusalem 1002 TUNIS Tel. (216) 71 794 822 Fax (216) 71 798 454 NABEUL Branch 115, av Habib Thameur 8062 NABEUL Tel. (216) 72 272 472 Fax (216) 72 272 505 SOUSSE Branch Imm. Rakoua Bld du 7 Novembre KHEZAMA EST 4051 SOUSSE Tel. (216) 73 273 195 Fax (216) 73 273 199 SFAX Branch Immeuble Inès 2 Avenue 7 Novembre 3027 SFAX EL JADIDA Tel. (216) 74 404 424 Fax (216) 74 402 458 Headquarter Immeuble Integra Centre Urbain Nord 1082 TUNIS MAHRAJENE Tel. (216) 71 189 600 Fax (216) 71 949 325 DJERBA Branch Rue Mohamed Badra, Complexe Chouaref 4180 Houmet Souk DJERBA Tel. (216) 75 623 300 Fax (216) 75 623 308 LA MARSA Branch Résidence Mongi Slim Rue Cherif - Marsa Plage 2078 LA MARSA Tel. (216) 71 983 533 Fax (216) 71 983 083 GRAND TUNIS BRANCHES member of www.tunisievaleurs.com [email protected] RESEARCH DEPARTMENT (216) 71 18 96 00 Securities Brokerage - Asset Management - Primary Dealer - Listing Sponsor

Transcript of Mise en page 1 - Tunisie Valeurs · rESEARCH R E P O R T February 2011 TUNISJerusalemBranch...

rESEARCHR E P O R T

F e b r u a r y 2 0 1 1

TUNIS Jerusalem Branch17, rue de Jérusalem1002 TUNIS

Tel. (216) 71 794 822Fax (216) 71 798 454

NABEUL Branch115, av Habib Thameur8062 NABEUL

Tel. (216) 72 272 472Fax (216) 72 272 505

SOUSSE BranchImm. RakouaBld du 7 NovembreKHEZAMA EST 4051 SOUSSETel. (216) 73 273 195Fax (216) 73 273 199

SFAX BranchImmeuble Inès 2Avenue 7 Novembre3027 SFAX EL JADIDATel. (216) 74 404 424Fax (216) 74 402 458

HeadquarterImmeuble IntegraCentreUrbainNord1082 TUNIS MAHRAJENETel. (216) 71 189 600Fax (216) 71 949 325

DJERBA BranchRue Mohamed Badra,Complexe Chouaref4180 Houmet Souk DJERBATel. (216) 75 623 300Fax (216) 75 623 308

LA MARSA BranchRésidence Mongi SlimRue Cherif - Marsa Plage2078 LAMARSATel. (216) 71 983 533Fax (216) 71 983 083

GRAND TUNIS BRANCHES

member of

www. t u n i s i e v a l e u r s . c [email protected]

RESEARCH DEPARTMENT(216) 71 18 96 00

Securities Brokerage - Asset Management - Primary Dealer - Listing Sponsor

2

Head office - Centre Urbain Nord

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

3

• Management

Fadhel Abdelkefi Chief Executive Officer

Walid Saibi Chief Operating Officer

Slim Abdelkefi Sales Manager

• Research and Corporate Finance

Rym Gargouri Ben Hamadou

Lilia Kamoun

Abderrahman Akkari

Ali M’barek

Mourad Mzali

• Asset Management

Hatem Saighi

Rafii Gannouchi

Mohamed Ali Ben Zina

Aicha Mokaddem

Nefis Sebai

• International Sales

Issam Ayari

Hedi Chemek

• Local Sales

Head Office : Taha El Khazen - Jamel Smida - Khaled Ben Kram

Tunis Jérusalem : Walid Kriaa - Sofien Ben Othman - Omar Boujedra - Rafiaa Abdelkefi

La Marsa : Farida Abbassi - Fares Torjemane

Nabeul : Aziz Salah - Ramzi Dghaies - Slim Chedly

Sousse : Houssem Ben Arfi - Lassaad Ben Anaya - Anis Bhouri Kehila - Narjess Ben Tarjem

Sfax : Adel Ben Ayed - Amine Derbel - Mourad Ksibi - Walid Walha

Djerba : Marwan Awayeb - Noamen Ben Terdayet

OUR TEAM

4

household consumption to drop.With the rapid growth of consumerloans in recent years, householdconsumption has become animportant engine for GDP growth.With Tunisian households’ pessimismgrowing it’s hard to believe thatappetite for consumption wouldcontinue in the near future.

Everything turned upside downfor the ex-ruling families: BenAli, Trabelsi, Materi,...etc arepoised to lose every penny theyhave taken.The most important question nowthat the Ben Alis and other corruptfamilies have left the country is who isgoing to take their businesses?Rapidly, the government has to take adecision to nationalize them as a firststep towards finding a legal solution.Moreover, the government has tomake sure that these companies havethe necessary capital resources tocontinue to grow and people workinginside do not lose their jobs. At alater stage, it is possible for the stateto sell them by public auction wheretransparency and competition areguaranteed.

The banking sector’s exposureon the corrupt families’businesses.Everybody knows that the ex rulingfamilies are present in almost everysector of the economy (tourism, airtransportation, retail sale, finance, cardealership, Telecom, media,construction, real estate, foodbusiness…). It is also no secret thatTunisian banks used to offer “easy”funding to these families. The badnews, however is that nobody knowsexactly how big the exposure of thesebanks is. As an example, the CarthageCement project of Mr BelhassenTrabelsi swallowed 367mTnd of bankdebt (of which 75mTnd were disbursedby BT bank only).

Risk of bad diplomacy withneighboring countries especiallywith Libya where the leader declaredhe is not happy that Ben Ali wascompelled to flee. He fears theIslamists’ threat to hit again at his

Editorial Comments : A transition yearfor the Tunisian economy• The Tunisian economy in2011: Which expectations ?

January 14th 2011 will beundoubtedly remembered as alandmark date in Tunisia’s history. Itwas the day, ex-president Ben Ali’sregime fell apart after it had beenunder pressure of popular riots toend 23 years of a dictator’s reign.

No sooner had the ex-presidentescaped than the country entered adangerous phase of insecurity withstreet fights and pillage all over theplaces. Many government andprivate buildings have suffered severedamages (supermarkets, officebuildings, bank branches, privatehouses, factories…etc). Theconsequence of all these events wasa completed paralysis of theeconomy. As of the date of writingthis report, we can see that thecountry is progressively returning tonormal life. The transition governmentwas appointed to pave the way fordemocratic elections in the fewmonths to come. In light of theseevents, we have good reasons tobelieve that the country’s mostdifficult year for decades lie ahead:

Political uncertainties persistand confidence building willtake time.In such an uncertain politicalenvironment we expect privateinvestments (local and foreign) toslow down with direct consequenceson jobs and foreign currencyreceipts. Rating agency Moody’s hasalready downgraded Tunisia’ssovereign debt from Baa2 to Baa3*and changed outlook from ‘stable’to ‘negative’. Other rating agencieslike Fitch and Standard and Poor’sshould also do the same (for the timebeing they put the country undernegative watch). These actions maychange foreign investors’ look to thecountry and its economy. Worse, itcould jeopardize the whole processof delocalization from the westerncountries to Tunisia and industrialpartnerships are feared to come toan end. In such a difficultenvironment we also expect

country’s frontiers. This would havebad repercussions on economicinterests, among them the Tunisianinvestments in neighboring markets.Clearly 2011 is the year of alldangers, whether on the political levelor on the economy and institutions,the challenges are big and theTunisian economy has to stand upto multiple difficulties:• Reduce unemployment among theyouth.• Improve wealth sharing betweenindividuals and regions by reducingdisparities between the coast and theremote areas located deep inside thecountry.

• Fight the informal economy andreduce ‘the economy of clans’, crackdown on corruption mainly inside theTunisian administration ...etc.

One of the biggest challenges isundoubtedly to reduceunemployment. In the recent years,the jobless rate has been risingrapidly which sparked the wholerevolution in December 2010. Everyyear 140.000 people apply for a jobwhile the current economic growthprovides between 40.000 and45.000 jobs per annum. It is thusclear that the main priority is to set inmotion the necessary economicgrowth in order to create jobs. It isprecisely value added sectors thathave to be targeted througheconomic growth so that theunemployed among the universitygraduates find jobs in the first place.

Second on the agenda would be anequal sharing of wealth between theregions and between individuals. Inthe recent years, investments havepoured in the coastal areas of thecountry to the detriment of otherregions located inside the countryalthough the government hadapproved a number of fiscaladvantages to the companies willingto invest in remote areas. Thetransition government has - for thefirst time in Tunisia’s history- createda fully fledged ministry for economicdevelopment between the regions.The ministry’s primary objective willbe to channel more and more

financial resources to the remoteareas in the countryside. For a betterwealth sharing, we believe that thegovernment should use a better fiscalpolicy to redistribute wealth. At thelevel of companies, we can think ofpromoting salary savings plan toallow a better profit sharing betweenemployees and shareholders.

Last, efforts have to be made to buildconfidence in the Tunisian Institutionsand administrations. According to theworld bank, Tunisia could have lost 2to 3 percentage points in GDPgrowth in the past because ofcorruption, of informal economy andbad corporate and other governance.Tunisia would have reached theeconomic growth of countries likeIndia had it had a reliable economicsystem. In reality, many businesspeople preferred to “stay small” andhide away of the spot lights so thatthey escape the Ben Ali families’appetite. Staying small, stayingdiscreet had thus made the countrylose on economic growth.

It is highly risky today to make anyforecasts on economic growth in2011. IMF forecasts are still showinga 4.8% growth of GDP. We think it isnot realistic. There is a clear puncturein Tunisia’s main wheels for growth.Strategic sectors will be badly hit(Tourism*, Trade and Finance…).Even exporting companies whichstayed away of the recent trouble willdepend much on the recovery in theEU markets

The exit from crisis will dependmuch on the political process.Once political stability is backand household confidence isback Tunisian people will easilyadaptIt is likely that the presidentialelections which are taking place in sixmonths would mark the end of theliberal model that the formergovernment used to lean upon.Tunisia is likely to turn moresocialist**. In such scenario, Tunisiawill have to review its strategicchoices and orientation. We willmake an assessment in six months!

* With a credit rating at Baa3, Tunisia is still anInvestment Grade

* The political parties poised to participate in the next elections have all a socialist orientation.** A 20% drop in Tourism transtates into 1% drop in Tunisia’s GDP growth.

Written on January 31st 2011

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

5

Macro Data

Production 2005 2006 2007 2008 2009 2010e

GDP (price 1990) Million Tnd 21 362 22 580 24 002 25 082 25 860 26 817

GDP growth % 3.9% 5.7% 6.3% 4.5% 3.1% 3,7%

GDP (current price) Million Tnd 37 664 45 756 49 874 55 297 58 768 63 397

Consumption Million Tnd 29 536 35 889 38 939 42 639 45 922 49 963

National savings Million Tnd 7 756 9 865 10 709 12 228 12 941 13 705

Private fixed investments Million Tnd 8 395 10 333 11 490 13 001 14 052 15 387

Balance of Payments 2005 2006 2007 2008 2009 2010e

Exports (goods and services) Million Tnd 14 286 15 558 19 409 23 637 19 469 22 953

Imports (goods and services) Million Tnd 16 972 20 003 24 438 30 241 25 878 31 140

Trade Balance (goods and services) Million Tnd - 2 686 - 4 445 - 5 029 - 6 605 - 6 408 -8 187

Coverage rate (goods) % 79.8% 77.8% 79.4% 78.2% 75.2% 73,7%

3% 3%

4%

2%

5%

3%

5%

4%4,5%

2002 2003 2004 2005 2006 2007 2008 2009 2010e

Inflation (Consumer price index)

Budget deficit

including privatisation

583,1

1015

800,4

973,1

551904,1

220,1

1588,7

1353

1,9%

3,2%

2,3%

2,6%

1,3%

1,8%

0,4%

2,7%

2,1%

0%

1%

1%

2%

2%

3%

3%

4%

0

200

400

600

800

1000

1200

1400

1600

1800

2002 2003 2004 2005 2006 2007 2008 2009 2010

as % of GDPin mTnd

Indebtedness 2005 2006 2007 2008 2009 2010e

Debt outstanding Million Tnd 21 949 22 221 22 829 23 927 25 190 25 220

Including foreign debt Million Tnd 14 026 13 285 13 300 14 560 14 716 15 757

Cost of foreign debt Million Tnd 2 716 3 881 3 921 3 276 3 184 3 155

Fx rate 2005 2006 2007 2008 2009 2010

$/Tnd (end of period) 1.363 1.297 1.221 1.310 1.317 1.438

€ / Tnd (end of period) 1.611 1.709 1.797 1.841 1.899 1.922

Written on January 31st 2011

Source : IMF and Central Bank of Tunisia

6

■ 2010 : The year of all records:Tunis Stock Exchange has gained another 19% in 2010, thus closing the 8th year ina row of positive performance. Along with these performances we should point out:• The rising traded volumes with an average trading per day of 10.4mTnd against6.8mTnd in 2009

• The record number of new listings with a total of 5 companies (insurance SALIM,reinsurance Tunis Ré, Carthage Cement, car dealer ENNAKL and Modern Leasing)thus boosting the market with an additional 260mTnd of “fresh money” in theprimary market and an additional 730mTnd in the total market capitalization

Under pressure of an unprecedented political crisis, the Tunisian market has made abad start in 2011. Year to date performance is already at -11% while trading volumesdropped to a daily average of 7.8mTnd (against 10mTnd in 2010). The Tunisian capitalmarket authorities suspended trading for 2 weeks in a row.Before we come to the events of 2011, we will highlight the main landmarks in2010:

Snapshots financial Act 2011:• Capital gains realized on sharesbought before January 2011continue to be exempt oftaxation whatever the sell date.

• Taxes are applicable on sharesbought starting from January1st 2011. However, taxes areapplicable on capital gainsrealized before the expiration ofthe second year following thebuy transaction year .

• For individual investors, capitalgains (net of capital losses) aresubject to a 10% tax. Capitalgains below or equal to 10,000Dinars per year continue to beexempt of taxation.

• For Tunisian institutionalinvestors, taxes are calculatedlike corporate tax (30 to 35%)for capital gains on shares heldless than the period indicatedabove. For longer periods notaxes are applicable

• Dividends continue to beexempt of taxes for bothindividual and institutionalinvestors.

• Capital gains realized oncollective investment schemesshares continue to be exempt oftaxation for individual investors.

• Fiscal advantages linked tosalary accounts (CEA accountsequivalent to the 401Kaccounts) are applicable.

• Foreign investors are subject toa withholding tax on the saleproceeds of 5% for institutionalsand 2.5% for individuals .However, taxes are applicableon capital gains realized beforethe expiration of the secondyear following the buytransaction year (see nextpage).

• Bandsaw performance andinvestors started to worry that thefinancial act 2011 would have anegative impact. The market startedto weaken in October when the drafton the new fiscal law for 2011 wasannounced. (see summary opposite).Just for the month of October,Tunindex lost 10%, which means 1/3of its aggregate performance. Sincethat date and on the following threemonths, the market did not manageto turn around.

As far as the new fiscal law isconcerned, we should underline fromthe start that the new taxes arerelated to a specific period of timeduring which shares are held*. This

means that the market authority iswilling to reduce speculation for shortperiods rather than make money oncapital gains. For foreign investors, wethink that the taxation system is«tougher». In essence, when capitalgains are realized during a specificperiod of time (when capital gains arerealized before the expiration of thesecond year following the buytransaction year) there is awithholding tax of 2.5% which isapplicable on the sale proceedsfor individual investors and 5% forinstitutionals. However, taxes are notapplicable when companies areregistered in countries with whichTunisia has signed a non-doubletaxation treaty.

However, we have seen 3 mainperiods during the year :

• Consolidation in the first half :The first 6 months of the year 2010have seen consolidation of pastperformances with Tunindex gaining15% and corporate earningscontinued to grow.

• Rally in the thirds quarter with aliquidity driven performance : It ishighly exceptional that the 3 monthsin summer (June, July and August)have seen a significant rally. Thelisting of Carthage Cement (June)then Ennakl (July) have fuelled theinflow of liquidity and trading peakedto exceptional levels. The summerrally was also fueled by corporateearnings’ growth with an average35% of profit growth. As of the dateof writing only the flag carrier Tunisairdidn’t publish its interim figures as atJune 30th 2010.

As at end of September Tunindexwas already flying +32% and the totalmarket capitalization was hoveringaround17 Billion Dinars.

2010 Roundup and Outlook 2011

-12%

12%

7%

21%

44%

12%11%

48%

19%

2003 2004 2005 2006 2007 2008 2009 2010

Tunindex changesince 2002

2002

In 2010, Tunindex hasreported an 8th positiveperformance in a row

2005 2006 2007 2008 2009 2010

Number of new listings 3 3 3 2 2 5

Value in the primary market (mTnd) 20 14 37 203 104 264

4 200

4 400

4 600

4 800

5 000

5 200

5 400

5 600

5 800

dec

.-09

jan

.-10

feb

.-10

mar

-10

apr.

-10

may

-10

jun

-10

jul.-

10

aug

-10

sep

-10

oct

-10

no

v-1

0

dec

-10

dec

-10

Q1 2010 : +9%

Q2 2010 : +5%

Q3 2010 : +16%

Q4 2010 : -10%

* capital gains realized before the expiration of the second year following the buy transaction year.

Written on January 31st 2011

7

-22%

-20%

-19%

-19%

-17%

-17%

-17%

-16%

-15%

-15%

-15%

-14%

-14%

-14%

-14%

-13%

-13%

-12%

-12%

-11%

-11%

-11%

-11%

-11%

-11%

-11%

-11%

-11%

-10%

-10%

-10%

-10%

-10%

-9%

-9%

-9%

-8%

-7%

-7%

-6%

-6%

-6%

-5%

-5%

Ennakl

Adwya

Attijari Bank

Sotetel

TUNIS RE

Carthage Cement

ATL

SOPAT

Attijari Leasing

Somocer

SIMPAR

CIL

Servicom

Monoprix

SFBT

Essoukna

BNA

STAR

UIB

ASSAD

SIPHAT

BT

ATB

STB

Marché

Sotuver

SPDIT

El Wifeck Leasing

SITS

UBCI

Tuninvest

Tunisie Leasing

Magasin Général

ARTES

Ciments de Bizerte

SALIM

PGH

Tunisair

GIF

Modern Leasing

BH

Amen Bank

TPR

BIAT

Stocks performance as at14/01/2011

■ Outlook 2011 : Lack ofvisibility and prudence is highlyrecommended...Trading has been suspended sinceJanuary 17th after the market hadalready lost 11% over the first twoweeks. Indeed, the market has lostall the aggregate gains of the year2010 during the short autumnperiod. Tunindex is thus down toits level of one year back !Trading resumed thinly on January31st for shorter trading sessions( just 1hour and 40 minutes oftrading per session), then returned tonormal trading hours one week later.

Given the many uncertaintiessurrounding the Tunisian economy,we expect the market to continueto evolve in a band saw. Therebound is likely to come in the2nd Half of the year conditioned bya return to political stability. Withfinancial indicators published in themeantime, we should have bettervisibility to make comments on theoutlook for 2011 althoughslowdown is looming.In our views, we believe there aredifferent types of companies eachsuffering the setbacks of thepolitical crisis differently :• The companies belonging to theex-ruling families where the BenAlis and allies are directshareholders (Ennakl, CarthageCement, Monoprix, Adwya, BT,BIAT). On these companies wehave no visibility on their future(i.e. whether their stakes will befrozen?, nationalised? And what isthe impact on management…)although stocks in thesecompanies would be severelycorrecting in the stock exchange .• The banking sector will be the“big loser” in this crisis becausemost of the Tunisian banks (STB,BH and BNA in the first place) have

significant exposure on the ex-ruling families and their loans arelikely to turn bad. Private bankslike BIAT and BT could have been“forced” to finance a number ofprojects where they are not backedby sufficient guarantees. It ishowever difficult to measure, today,the impact of all this on the banks’non performing loans and provideexact figures .

Other companies are also likely tosuffer from the economicslowdown. At a first glance, theseare the companies to suffer:• Tunisair : as we expect theTourism sector to be hard hit.• Magasin Général : Although weconsider the sector as defensive,retail sale companies will suffer biglosses from pillage and otherdestructions estimated so far ataround 50mTnd according to thecompany’s management.• ARTES : The reason being thedecreasing car import quotas(subsequent to the gap in tradedeficit).• Real estate developers and ingeneral those companies linked tothe construction sector (likeCiments de Bizerte, SOMOCERand to a lesser extent TPR andSERVICOM).• The Leasing companies : as thesector is highly sensitive to theeconomic environment and to thegood collection of bills. We willhave to watch the sector’s assetquality for the months to come andto the cost of risk.• The insurance companies : Thelosses deriving from the pillagesand other destructions, willcertainly have a price to be paid bythe insurance companies. They willhave to refund commercial offices,factories and other public andprivate assets destroyed during

the violent events of the beginningof the year. Part of the losses willbe obviously refunded byreinsurance companies but it ishard for the time being to say howbig the losses/refunds are.

The best case scenario in ourviews is a market rebound withinthe end of the first half of 2011lifted by good corporate earningsfor fiscal year 2010. Reasonably,listed companies should be readyto issue their audited figures for2010 by the end of the first half of2011. However, we believe that theoptimist scenario can not beapplied to all the listed companies.Some of them will suffer theconsequences of reviewing downtheir growth prospects for 2011.For the time being we prefer to beon the safe side by recommendingdefensive stocks with high yieldand operating in the consumersectors. Our best picks are thusSFBT, SOTUVER, PGH, ASSAD,SOPAT and SPDIT. Other stockswith good fundamentals andattractive valuation are also highlyrecommended (TPR andTuninvest).We will obviously have to makeupdates depending on the courseof events in the near future and ourstock recommendation will thuschange accordingly.

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

Written on January 31st 2011

8

0

1

2

3

4

5

6

15

17

19

21

23

25

27

29

31Volume (mTnd)Price (Tnd)

+55%

Mar-10 May-10 Jul-10 Oct-10 Dec-10

a new commercial strategy revolvingaround a strong network (thecompany has already opened 6 newbranches nationwide in 2010 and isplanning to open another 15branches in 2011). In light of thecompany’s financial indicators as atDecember 31st 2010, we believe thatSalim will be able to meet its businessplan forecasts: a 25% growth of netprofit at 4.2mTnd.

At the time of listing, Salim’s IPO wasa great success with a 27 timesoversubscription, the share price hasclimbed 55% ever since.

From a stock market stand point,Salim’s market cap stands at 60mTndwhich is almost twice its Restated NetAsset Value, a key indicator in thistype of business. We thus downgradethe stock, at the time we write thisreport, from «Buy» to «Hold» withpositive outlook . We have 2arguments for the downgrading : (1)The acquisition by Mr. BelhassenTrabelsi (part of the ex-ruling family) ofa 9.98% stake in the capital of thecompany in late 2010 (2) The verylikely increase in claims’ ratesubsequent to the violent events thatTunisia has recently seen .

Salim insurances was initially listed inthe over-the-counter market, thenwas transferred to the main market inthe first half of 2010. At that time anIPO was launched to increase thecapital of the company by 9.9mTndaimed at strengthening its financialbase to develop its commercialstrategy and restructure its portfolio.

SALIM’s market share now stands at3.2% and it is ranked 11th in thesector. Unlike its peers, most of itssales are made of life insuranceproducts (47%) thanks to a largenetwork of branches belonging to itsmother company BH Bank.

BH BANK network currently provides60% of Salim’s total turnover . Thecompany aims to reduce dependenceon its mother company by bringingthe rate to 40% by 2013. Thecompany’s strategy to reach its goalin to diversify its product range byintroducing more profitable segmentslike car insurance and other segments(Fire, accidents and Miscellaneous).The restructuring of Salim’s portfolioshould thus bring more business inthe ‘Non Life’ which is generally aloss making business.Therestructuring will be accompanied by

• Robust Stock but external risk may hurt • Strengthen fundamentals through listing in theExchange

Listing date 01/04/2010

Value at listing (in mTnd) 39,9Current mkt cap (in mTnd) 60P/E 10e 14,2P/B 10e 1,9Yield 10e 3,1%ROE 10e 19,6%

SALIM

Volume (mTnd)Price (Tnd)

May-10 Jul-10 Sep-10 Nov-10 Jan-11

0

1

2

3

4

5

6

0

2

4

6

8

10

12

14

16

18

20

+81%

From a market stand point, the stockhas been one of the favourite stockssince it was first listed (itrallied+118%) in few months (end ofDecember 2010).Like all the otherstocks, Tunis Ré fell sharply in thefirst 2 weeks of January. It currentlytrades at 12.23Tnd, which means atotal market cap of 110mTnd and amultiple of Restated Net Asset Valueof 1.5x. While the stock came off to areasonable level, we will keep ourrecommendation unchanged «Hold(+)» given the company's lowprofitability (11% ROE). Having saidthat, we will watch the company’sability to meet its business plantargets. Tunis Ré intends to raisemore capital with another rights issuefor 30mTnd scheduled for 2011 toincrease its share capital to 75mTndthen another raising is planned for2012 to reach 100mTnd.

The capital raising will certainly helpthe company strengthen its capitalbase to consolidate its position in thelocal market then develop itsbusiness internationally by enlargingits product range.

Set up by the Tunisian state in 1981,TUNIS RE is a pioneer company inthe Tunisian reinsurance sector . It isthe only company in Tunisiaspecialising only in reinsurance (21%of market share), the other ninecompanies are originally generalinsurance companies with anaccessory reinsurance segment. Therisk that TUNIS RE bears is moderatein the sense that the companytransfers 52% of its portfolio to otherreinsurance companies abroad.

Listed in April 2010, TUNIS RE hasraised in the IPO 14mTnd by rightsissue. The move was aimed tostrengthen its capital base andimprove its rating (B+ by AM Best,«Grade»). Although it is hard to makeforecasts in this type of business ,given the high volatility in claims, wethink that the company is in aposition to meet its business planforecasts of total sales at 67mTnd(+11% compared with 2009) and anet profit of 6.4mTnd (+27%compared with 2009). The reasonsbehind these good performances are(1) selective growth policy, (2) goodcontrol over the general expenses(3) profitable financial placements.

Listing date 01/05/2010

Value at listing (in mTnd) 63Current mkt cap (in mTnd) 110P/E 10e 17,2P/B 10e 1,6Yield 10e 3,1%ROE 10e 11,0%

TUNIS RE

New Listings in 2010

* AM BEST : Rating agency, specialising inInsurance

Written on January 31st 2011

9

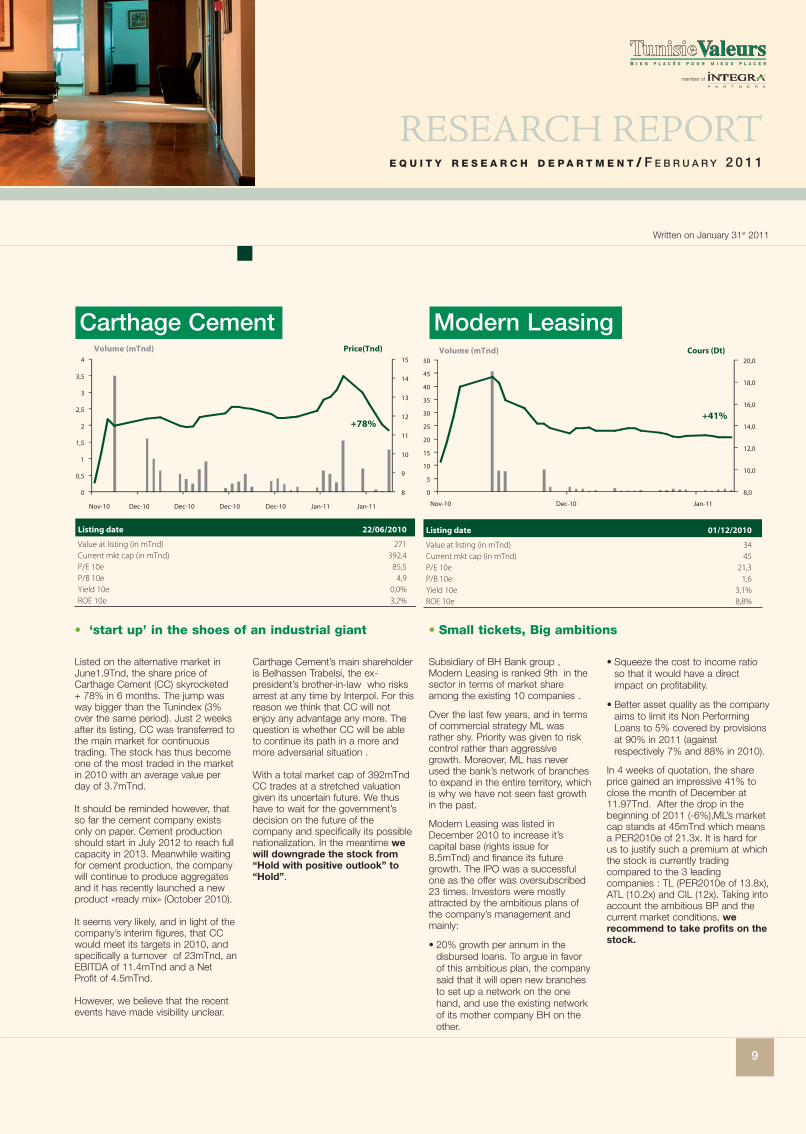

• ‘start up’ in the shoes of an industrial giant • Small tickets, Big ambitions

Volume (mTnd) Price(Tnd)

8

9

10

11

12

13

14

15

0

0,5

1

1,5

2

2,5

3

3,5

4

Nov-10 Dec-10 Dec-10 Dec-10 Dec-10 Jan-11 Jan-11

+78%

Volume (mTnd) Cours (Dt)

8,0

10,0

12,0

14,0

16,0

18,0

20,0

0

5

10

15

20

25

30

35

40

45

50

+41%

Nov-10 Dec-10 Jan-11

Carthage Cement’s main shareholderis Belhassen Trabelsi, the ex-president’s brother-in-law who risksarrest at any time by Interpol. For thisreason we think that CC will notenjoy any advantage any more. Thequestion is whether CC will be ableto continue its path in a more andmore adversarial situation .

With a total market cap of 392mTndCC trades at a stretched valuationgiven its uncertain future. We thushave to wait for the government’sdecision on the future of thecompany and specifically its possiblenationalization. In the meantime wewill downgrade the stock from“Hold with positive outlook” to“Hold”.

Listed on the alternative market inJune1.9Tnd, the share price ofCarthage Cement (CC) skyrocketed+ 78% in 6 months. The jump wasway bigger than the Tunindex (3%over the same period). Just 2 weeksafter its listing, CC was transferred tothe main market for continuoustrading. The stock has thus becomeone of the most traded in the marketin 2010 with an average value perday of 3.7mTnd.

It should be reminded however, thatso far the cement company existsonly on paper. Cement productionshould start in July 2012 to reach fullcapacity in 2013. Meanwhile waitingfor cement production, the companywill continue to produce aggregatesand it has recently launched a newproduct «ready mix» (October 2010).

It seems very likely, and in light of thecompany’s interim figures, that CCwould meet its targets in 2010, andspecifically a turnover of 23mTnd, anEBITDA of 11.4mTnd and a NetProfit of 4.5mTnd.

However, we believe that the recentevents have made visibility unclear.

Listing date 22/06/2010

Value at listing (in mTnd) 271Current mkt cap (in mTnd) 392,4P/E 10e 85,5P/B 10e 4,9Yield 10e 0,0%ROE 10e 3,2%

Carthage Cement

• Squeeze the cost to income ratioso that it would have a directimpact on profitability.

• Better asset quality as the companyaims to limit its Non PerformingLoans to 5% covered by provisionsat 90% in 2011 (againstrespectively 7% and 88% in 2010).

In 4 weeks of quotation, the shareprice gained an impressive 41% toclose the month of December at11.97Tnd. After the drop in thebeginning of 2011 (-6%),ML’s marketcap stands at 45mTnd which meansa PER2010e of 21.3x. It is hard forus to justify such a premium at whichthe stock is currently tradingcompared to the 3 leadingcompanies : TL (PER2010e of 13.8x),ATL (10.2x) and CIL (12x). Taking intoaccount the ambitious BP and thecurrent market conditions, werecommend to take profits on thestock.

Subsidiary of BH Bank group ,Modern Leasing is ranked 9th in thesector in terms of market shareamong the existing 10 companies .

Over the last few years, and in termsof commercial strategy ML wasrather shy. Priority was given to riskcontrol rather than aggressivegrowth. Moreover, ML has neverused the bank’s network of branchesto expand in the entire territory, whichis why we have not seen fast growthin the past.

Modern Leasing was listed inDecember 2010 to increase it’scapital base (rights issue for8.5mTnd) and finance its futuregrowth. The IPO was a successfulone as the offer was oversubscribed23 times. Investors were mostlyattracted by the ambitious plans ofthe company’s management andmainly:

• 20% growth per annum in thedisbursed loans. To argue in favorof this ambitious plan, the companysaid that it will open new branchesto set up a network on the onehand, and use the existing networkof its mother company BH on theother.

Listing date 01/12/2010

Value at listing (in mTnd) 34Current mkt cap (in mTnd) 45P/E 10e 21,3P/B 10e 1,6Yield 10e 3,1%ROE 10e 8,8%

Modern Leasing

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

Written on January 31st 2011

10

Volume (mTnd)Price (Dt)

Jul-10 Aug-10 Sept-10 Oct-10 Nov-10 Dec.-10 Jan-11

0

5

10

15

20

25

30

35

40

45

0

2

4

6

8

10

12

14

16

18

20

-14%

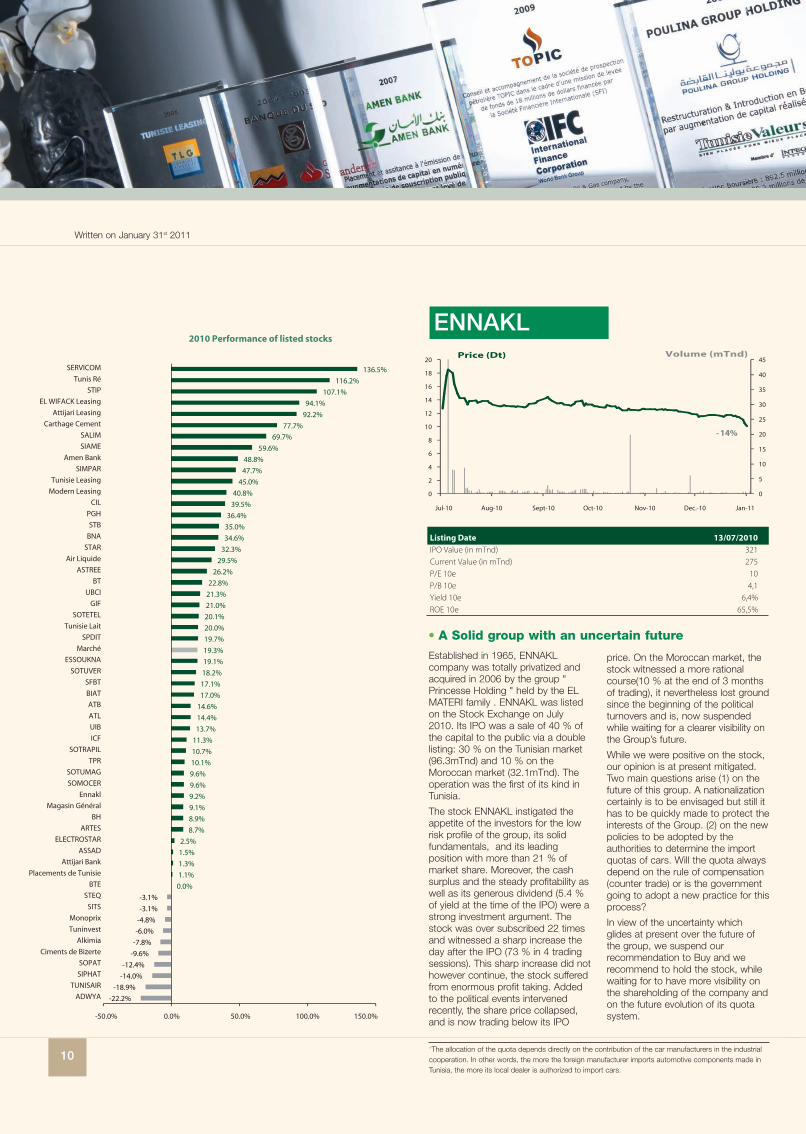

price. On the Moroccan market, thestock witnessed a more rationalcourse(10 % at the end of 3 monthsof trading), it nevertheless lost groundsince the beginning of the politicalturnovers and is, now suspendedwhile waiting for a clearer visibility onthe Group’s future.

While we were positive on the stock,our opinion is at present mitigated.Two main questions arise (1) on thefuture of this group. A nationalizationcertainly is to be envisaged but still ithas to be quickly made to protect theinterests of the Group. (2) on the newpolicies to be adopted by theauthorities to determine the importquotas of cars. Will the quota alwaysdepend on the rule of compensation(counter trade) or is the governmentgoing to adopt a new practice for thisprocess?

In view of the uncertainty whichglides at present over the future ofthe group, we suspend ourrecommendation to Buy and werecommend to hold the stock, whilewaiting for to have more visibility onthe shareholding of the company andon the future evolution of its quotasystem.

Established in 1965, ENNAKLcompany was totally privatized andacquired in 2006 by the group "Princesse Holding " held by the ELMATERI family . ENNAKL was listedon the Stock Exchange on July2010. Its IPO was a sale of 40 % ofthe capital to the public via a doublelisting: 30 % on the Tunisian market(96.3mTnd) and 10 % on theMoroccan market (32.1mTnd). Theoperation was the first of its kind inTunisia.

The stock ENNAKL instigated theappetite of the investors for the lowrisk profile of the group, its solidfundamentals, and its leadingposition with more than 21 % ofmarket share. Moreover, the cashsurplus and the steady profitability aswell as its generous dividend (5.4 %of yield at the time of the IPO) were astrong investment argument. Thestock was over subscribed 22 timesand witnessed a sharp increase theday after the IPO (73 % in 4 tradingsessions). This sharp increase did nothowever continue, the stock sufferedfrom enormous profit taking. Addedto the political events intervenedrecently, the share price collapsed,and is now trading below its IPO

Listing Date 13/07/2010

IPO Value (in mTnd) 321Current Value (in mTnd) 275P/E 10e 10P/B 10e 4,1Yield 10e 6,4%ROE 10e 65,5%

ENNAKL

*The allocation of the quota depends directly on the contribution of the car manufacturers in the industrialcooperation. In other words, the more the foreign manufacturer imports automotive components made inTunisia, the more its local dealer is authorized to import cars.

-22.2%

-18.9%

-14.0%

-12.4%

-9.6%

-7.8%

-6.0%

-4.8%

-3.1%

-3.1%

0.0%

1.1%

1.3%

1.5%

2.5%

8.7%

8.9%

9.1%

9.2%

9.6%

9.6%

10.1%

10.7%

11.3%

13.7%

14.4%

14.6%

17.0%

17.1%

18.2%

19.1%

19.3%

19.7%

20.0%

20.1%

21.0%

21.3%

22.8%

26.2%

29.5%

32.3%

34.6%

35.0%

36.4%

39.5%

40.8%

45.0%

47.7%

48.8%

59.6%

69.7%

77.7%

92.2%

94.1%

107.1%

116.2%

136.5%

-50.0% 0.0% 50.0% 100.0% 150.0%

ADWYA

TUNISAIR

SIPHAT

SOPAT

Ciments de Bizerte

Alkimia

Tuninvest

Monoprix

SITS

STEQ

BTE

Placements de Tunisie

Attijari Bank

ASSAD

ELECTROSTAR

ARTES

BH

Magasin Général

Ennakl

SOMOCER

SOTUMAG

TPR

SOTRAPIL

ICF

UIB

ATL

ATB

BIAT

SFBT

SOTUVER

ESSOUKNA

Marché

SPDIT

Tunisie Lait

SOTETEL

GIF

UBCI

BT

ASTREE

Air Liquide

STAR

BNA

STB

PGH

CIL

Modern Leasing

Tunisie Leasing

SIMPAR

Amen Bank

SIAME

SALIM

Carthage Cement

Attijari Leasing

EL WIFACK Leasing

STIP

Tunis Ré

SERVICOM

2010 Performance of listed stocks

Written on January 31st 2011

• A Solid group with an uncertain future

11

In the date of January 26th, the following 28 listed stocks with a marketcapitalization greater than 100mTnd, represent more than 90 % of the totalcapitalization of the market.

Comments• One of the most diversified private groups in Tunisia present in about ten businesses (poultry farming, food-processing, industry, services, business,ceramic, wood, civil engineering works, steel, real estate) and in various countries of the Maghreb (Tunisia, Algeria, Libya, Morocco).

• Leader's position on several markets and a portfolio of prestigious brands : Mazrâa, the margarine Jadida, the ice creams Selja and OLA, ChemiaSherazad, ceramic Carthago, refrigerators Mont Blanc …

• An increasing profitability thanks to the variety of the businesses and to the development of new activities. The EBITDA should increase by 14 % in 2010to exceed the threshold of 180mTnd.

• A gearing that exceeds the 100 %, but the situation is temporary because of the heavy committed investments (more of 400mTnd in 3 years). The groupshould get out of debt thanks to the increase of free cash flows of the new projects.

• A strong sector-based and regional diversification which grants to the stock a double profile: defensive and growth, in short it is a shelter stock in anunstable market. We recommend to “Buy” PGH.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

PGH Holding 1 433mTnd 358kTnd 15.9x 2.8x 3.2% 18.3%

Comments• The activity of the bank performed well in 2010 with a confirmation of the strong growth of 2009. Loans should thus show a 12.1 % growth rate.• As for Deposits, their growth should border the 6% with the preservation of a strong growth of the checking deposits (14 %) what should maintain theadvantageous cost of the resources of the bank.

• A consolidation of the market share of the bank with 13% of total Loans in the sector.• A rate of NPL’s which should border according to our forecasts the 10 %, covered at 72% by provisions.• A strengthened net profit estimated at 75mTnd for 2010 corresponding to a PE2010 of 15.7x• After the last events in Tunisia, and given the family tie which binds the majority shareholders of the BIAT (Group MABROUK) with the ex President BenAli, we remain attentive as for the impact of the investigations which could affect the participation of the MABROUKs in the bank

• We must however stress the fact that we remain confident as for the fundamentals of the bank and its advantages facing the competition. This brings usto renew our recommendation " to Hold BIAT with positive outlook ".

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

BIAT Banking 1 178mTnd 937kTnd 15.7x 2.0x 2.9% 14.6%

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

Written on January 31st 2011

12

Comments• 2010 was a year of very strong growth at the levels of the disbursed loans and deposits for the bank. These should post respectively growth of around25 % and 28% at the end of the fiscal year.

• A detailed audit of these new loans should be launched to determine the impact of the commitments to the members of the ex regime on the ratios ofthe bank, knowing that one of these members, Belhassen Trabelsi, holds a 12.98 % in BT.

• Except exceptional reserves, the bank should post a net profit of 80mTnd.• We revise our buy recommendation to Hold with positive outlook. This downgrade is due to our reserves as for the state of the recentcommitments of the bank.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

BT Banking 1 159mTnd 543kTnd 14.1x 1.1x 2.9% 8.1%

Comments• Despite the will of the management to increase the credit activity versus the bond trading activity, the interest revenues stagnated at 28 % of the bank’sNBI (practically the same level as that of the 2009).

• Considerable investments in the expansion of the branch network. The bank accounts today for 109 branches.• An improving quality of assets with an NPL level at 8.7 % and covered by provisions at 73 %.• A strong dependence on the Treasury bills trading activity which puts the bank in a dangerous position in case of an unfavorable move in the interestrates.

• An estimated net profit in 2010 of 53mTnd, therefore the bank is trading at a PE 010 of 13.4x.• We revise our recommendation from "Buy" "to ‘Hold’.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

ATB Banking 710mTnd 13kTnd 13.4x 1.7x 2.3% 17.3%

Comments• 2010 should once again be a year of very strong growth for the bank. A considerable growth of the deposits and the loans which should respectivelyborder the 18 and 26 %.

• A rate of NPL’s should reach the 10 % covered by provisions at 74%.• Additional efforts of collection are required to decrease the amount of the non performing loans which does not seem to decrease year by year.• A net profit of 55mTnd is expected for 2010 representing a 26 % growth compared to 2009.• The strong growth of the activity of the bank should in our opinion cause some difficulties as for the quality of loans view of the recent events.• On the basis of the projected profits on 2010, the bank is trading at a PE2010 of 12.1x, which places the bank in acceptable valuation ranges.• Given events that shook the country, and in view of their impact on the banking system, we revise our recommendation from "Buy" to Hold " withpositive outlook ". This recommendation could be revised further to the communication of the bank on the state of its exposure to businesses relatedto the ex regime.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

AMEN BANK Banking 732mTnd 209kTnd 12.1 1.7 2.3% 17.3%

13

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

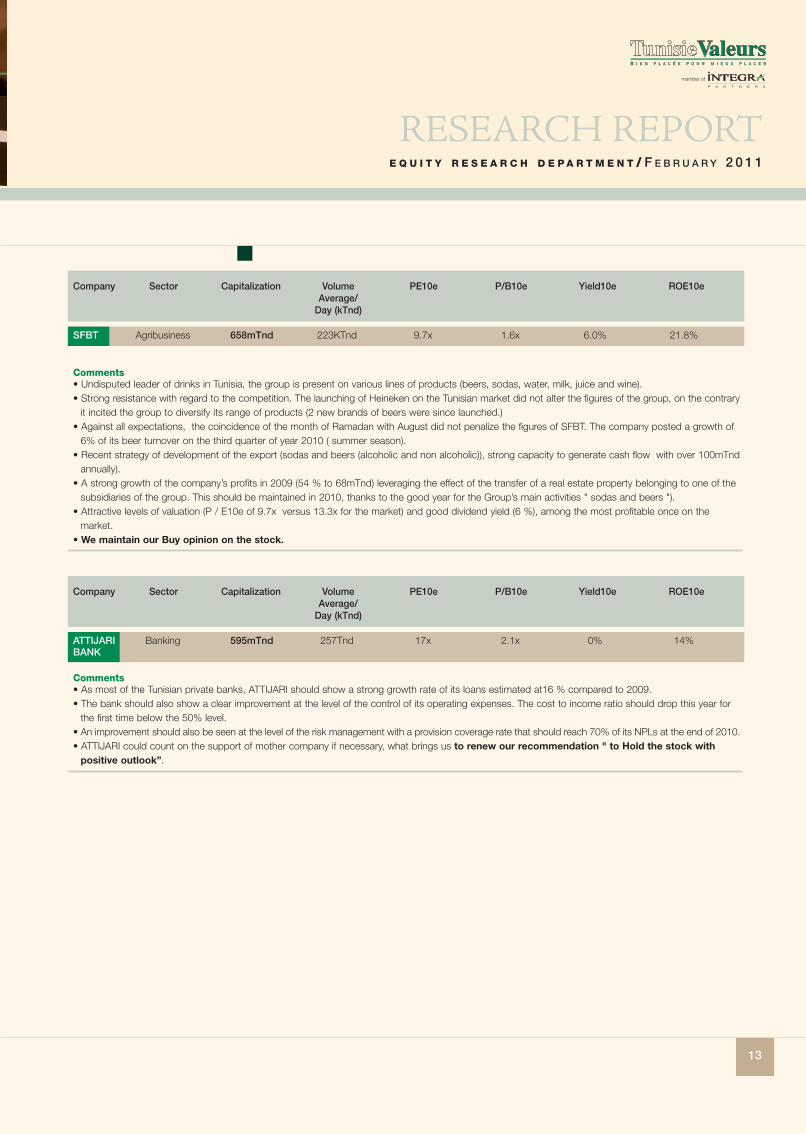

Comments• Undisputed leader of drinks in Tunisia, the group is present on various lines of products (beers, sodas, water, milk, juice and wine).• Strong resistance with regard to the competition. The launching of Heineken on the Tunisian market did not alter the figures of the group, on the contraryit incited the group to diversify its range of products (2 new brands of beers were since launched.)

• Against all expectations, the coincidence of the month of Ramadan with August did not penalize the figures of SFBT. The company posted a growth of6% of its beer turnover on the third quarter of year 2010 ( summer season).

• Recent strategy of development of the export (sodas and beers (alcoholic and non alcoholic)), strong capacity to generate cash flow with over 100mTndannually).

• A strong growth of the company’s profits in 2009 (54 % to 68mTnd) leveraging the effect of the transfer of a real estate property belonging to one of thesubsidiaries of the group. This should be maintained in 2010, thanks to the good year for the Group’s main activities " sodas and beers ").

• Attractive levels of valuation (P / E10e of 9.7x versus 13.3x for the market) and good dividend yield (6 %), among the most profitable once on themarket.

• We maintain our Buy opinion on the stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

SFBT Agribusiness 658mTnd 223KTnd 9.7x 1.6x 6.0% 21.8%

Comments• As most of the Tunisian private banks, ATTIJARI should show a strong growth rate of its loans estimated at16 % compared to 2009.• The bank should also show a clear improvement at the level of the control of its operating expenses. The cost to income ratio should drop this year forthe first time below the 50% level.

• An improvement should also be seen at the level of the risk management with a provision coverage rate that should reach 70% of its NPLs at the end of 2010.• ATTIJARI could count on the support of mother company if necessary, what brings us to renew our recommendation " to Hold the stock withpositive outlook”.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

ATTIJARI Banking 595mTnd 257Tnd 17x 2.1x 0% 14%BANK

14

Comments• Remarkable increase of the loans’ growth estimated at 36.8 % to 1594mTnd. The bank remains nevertheless trailing at the last place among the listedbanks in terms of loans market share with 4.3%

• The bank accounts for 28 % of its NBI from the commissions margins, one of the highest in the banking system.• A relatively clean loan book with about 8.2 % of NPL’s in 2009 (versus a sector-based average of 12.5 %) and a coverage rate of 74.5 % (64.5 % for thesector).

• A cost to income ratio of 60.5 % versus a sector average of 46.5 %. Efforts remain necessary to improve the operational efficiency of the bank.• Despite an increasing net profit in 2010 estimated at 26mTnd the valuation remains among the highest of the sector (with a PE 2010 of 21.2x).• We recommend to Hold the stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

UBCI Banking 550mTnd 50kTnd 21.2x 2.6x 3.5% 14%

Comments• BH Bank has not reported the same pace of growth in the last few years as its peers in particular the private ones. In 2010, the loan book should growby 10.9 %, as for the deposits, they should increase by 3% according to the published indicators. These levels will be well below the sector’s average.

• The NBI of the BH still suffers from its strong dependence of the interest income (72 % of the NBI). We do not think that in the short term, themanagement is capable of balancing this deficiency.

• In spite of the increase in 2009 in the cost to income ratio (43%), it stays below the sector’s average and should remain at the same level in 2010.• We think that the real estate sector will start progressively slowing down in the years to come, which will affect the activity of the bank. BH will have to rechannel its activity towards the other sectors of the economy. This slowing down would come because of a possible change in the mindset. i.e.investors would not look at real estate anymore as a refuge and they should re-channel their investments towards more productive sectors given theimproving business context.

• 2010 profits should hover around 60mTnd, unless additional provisions need to be made to cover the potential risks on loans to ex regime.• We revise down our recommendation " to hold the stock with positive outlook ". This recommendation could be revised further to thecommunication of the bank on the state of its loan book and its future prospects.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

BH Banking 498mTnd 191kTnd 8.2x 1.1x 2.3% 15%

15

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

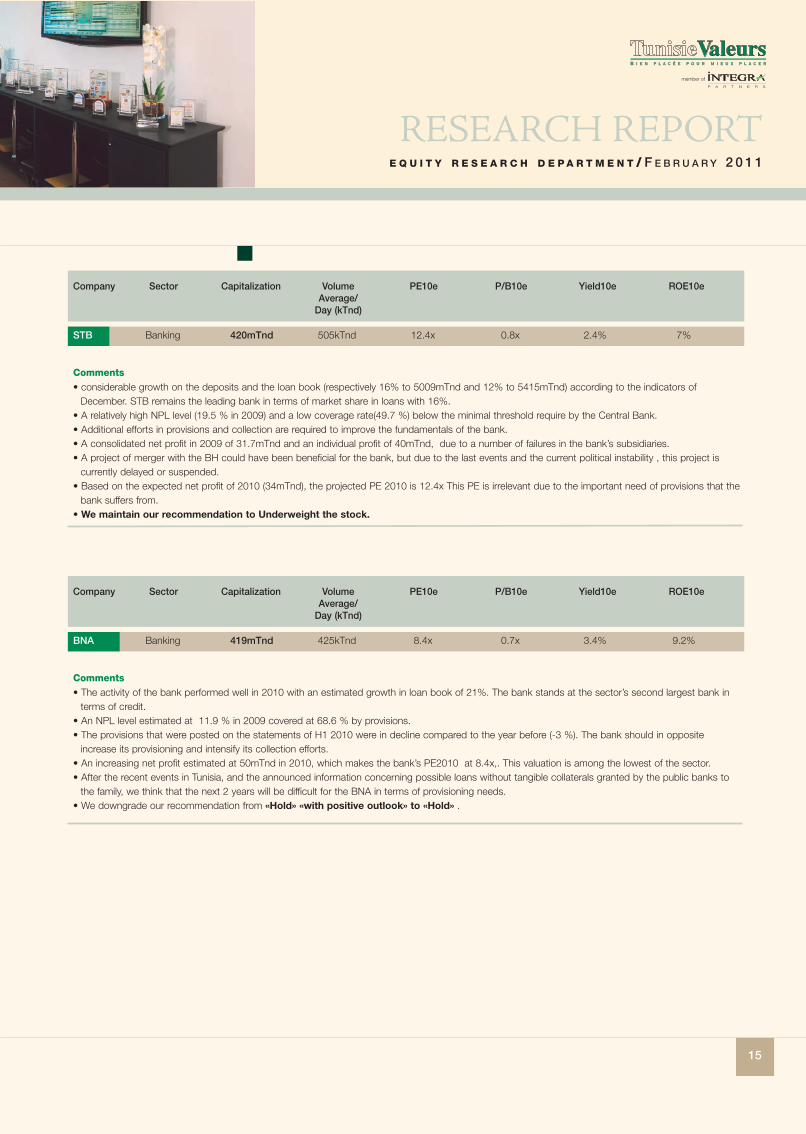

Comments• considerable growth on the deposits and the loan book (respectively 16% to 5009mTnd and 12% to 5415mTnd) according to the indicators ofDecember. STB remains the leading bank in terms of market share in loans with 16%.

• A relatively high NPL level (19.5 % in 2009) and a low coverage rate(49.7 %) below the minimal threshold require by the Central Bank.• Additional efforts in provisions and collection are required to improve the fundamentals of the bank.• A consolidated net profit in 2009 of 31.7mTnd and an individual profit of 40mTnd, due to a number of failures in the bank’s subsidiaries.• A project of merger with the BH could have been beneficial for the bank, but due to the last events and the current political instability , this project iscurrently delayed or suspended.

• Based on the expected net profit of 2010 (34mTnd), the projected PE 2010 is 12.4x This PE is irrelevant due to the important need of provisions that thebank suffers from.

• We maintain our recommendation to Underweight the stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

STB Banking 420mTnd 505kTnd 12.4x 0.8x 2.4% 7%

Comments• The activity of the bank performed well in 2010 with an estimated growth in loan book of 21%. The bank stands at the sector’s second largest bank interms of credit.

• An NPL level estimated at 11.9 % in 2009 covered at 68.6 % by provisions.• The provisions that were posted on the statements of H1 2010 were in decline compared to the year before (-3 %). The bank should in oppositeincrease its provisioning and intensify its collection efforts.

• An increasing net profit estimated at 50mTnd in 2010, which makes the bank’s PE2010 at 8.4x,. This valuation is among the lowest of the sector.• After the recent events in Tunisia, and the announced information concerning possible loans without tangible collaterals granted by the public banks tothe family, we think that the next 2 years will be difficult for the BNA in terms of provisioning needs.

• We downgrade our recommendation from «Hold» «with positive outlook» to «Hold» .

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

BNA Banking 419mTnd 425kTnd 8.4x 0.7x 3.4% 9.2%

16

Comments• Future cement plant of an annual capacity of 2.3 million tons a year situated in a strategic place «Ressas» (at 25km of the city center, 25 km of bothports: Radès and Goulette and at 20km of the Lake of Tunis).

• Starting the production on July, 2012• No visibility on the future of the one of the main shareholders of the company, Belhassen Trabelsi.• A high valuation level, and an uncertain future for the company. We recommend to Hold the stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

Carthage Cement 392mTnd 1789kTnd 85.5x 4.9x 0% 3.2%Cement

Comments• The insurance sector’s leader with more than 20 % of market share• Allied to a famous strategic partner GROUPAMA (first mutual insurance company in France and 15th largest European insurer with presence in 14countries) that has the option to increase its shareholding position in the company in 2013.

• A wide network of branches (189)• A solid financial position allowing a technical risk coverage by provisions above145 %.• A solvency margin way higher than to the statutory standards (4x)• A level of valuation that still attractive, the capitalization of the company represents 1.4x Restated Net Asset Value. It is however advisable to underlinethat this multiple is subject to modifications since 12 % of the company’s investments(70mTnd) are made of listed stocks which witnessed suddenmovements between 2010 (the index jumped by 19 % in 2010 and lost 11 % since the beginning of 2011). At this moment we cannot estimate thisimpact due to the absence of detailed information on the company’s listed portfolio.

• Unstable situation, further to the dismissal of the very unpopular CEO by the employees and whom GROUPAMA wanted to replace since it entered thecapital of STAR.

• Damages to many properties during the latest events. At this date, we are not capable of estimating their impact on the figures of STAR. We will keepour recommendation unchanged “Buy” on the stock till we have more visibility on the various aspects that might affect the company.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

STAR Insurance 382mTnd 372kTnd 10.8x 1.7x 1.2% 18.3%

17

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

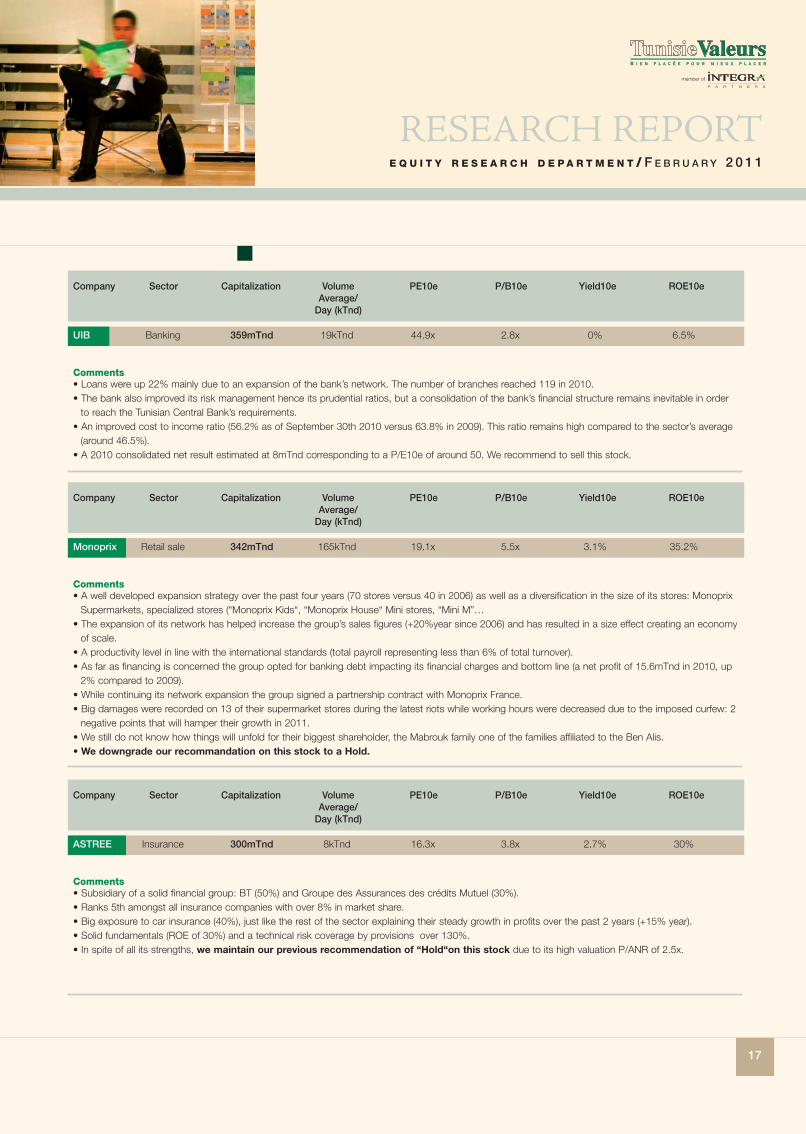

Comments• Loans were up 22% mainly due to an expansion of the bank’s network. The number of branches reached 119 in 2010.• The bank also improved its risk management hence its prudential ratios, but a consolidation of the bank’s financial structure remains inevitable in orderto reach the Tunisian Central Bank’s requirements.

• An improved cost to income ratio (56.2% as of September 30th 2010 versus 63.8% in 2009). This ratio remains high compared to the sector’s average(around 46.5%).

• A 2010 consolidated net result estimated at 8mTnd corresponding to a P/E10e of around 50. We recommend to sell this stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

UIB Banking 359mTnd 19kTnd 44.9x 2.8x 0% 6.5%

Comments• A well developed expansion strategy over the past four years (70 stores versus 40 in 2006) as well as a diversification in the size of its stores: MonoprixSupermarkets, specialized stores (“Monoprix Kids“, “Monoprix House“ Mini stores, “Mini M”…

• The expansion of its network has helped increase the group’s sales figures (+20%year since 2006) and has resulted in a size effect creating an economyof scale.

• A productivity level in line with the international standards (total payroll representing less than 6% of total turnover).• As far as financing is concerned the group opted for banking debt impacting its financial charges and bottom line (a net profit of 15.6mTnd in 2010, up2% compared to 2009).

• While continuing its network expansion the group signed a partnership contract with Monoprix France.• Big damages were recorded on 13 of their supermarket stores during the latest riots while working hours were decreased due to the imposed curfew: 2negative points that will hamper their growth in 2011.

• We still do not know how things will unfold for their biggest shareholder, the Mabrouk family one of the families affiliated to the Ben Alis.• We downgrade our recommandation on this stock to a Hold.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

Monoprix Retail sale 342mTnd 165kTnd 19.1x 5.5x 3.1% 35.2%

Comments• Subsidiary of a solid financial group: BT (50%) and Groupe des Assurances des crédits Mutuel (30%).• Ranks 5th amongst all insurance companies with over 8% in market share.• Big exposure to car insurance (40%), just like the rest of the sector explaining their steady growth in profits over the past 2 years (+15% year).• Solid fundamentals (ROE of 30%) and a technical risk coverage by provisions over 130%.• In spite of all its strengths, we maintain our previous recommendation of “Hold“on this stock due to its high valuation P/ANR of 2.5x.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

ASTREE Insurance 300mTnd 8kTnd 16.3x 3.8x 2.7% 30%

18

Comments• One of the two public cement companies in the country with a production capacity of 1 Million tons/year.• The original project of doubling its production has been dropped (while it was the main argument of the 2009 IPO). A strategic change that puts a bigquestion mark on the “size” effect of SCB.

• The company did not meet its Business Plan’s forecasts in neither turnover nor profitability• A high valuation level with regards to the company’s future outlook• A difficult 2011 year with a possible slowdown of the building activity.• We recommend to Sell the stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

Ciments Cement 297mTnd 67kTnd 35x 1.8x 0.9% 5.3%de Bizerte

Comments• Third main actor of the retail sector: a market with a large growth potential that is equally split between the 3 private groups.• A consolidated turnover of 525mTnd in 2010. The reacquisition of PROMOGRO in 2009 has given Magasin General a new dimension.• A successful commercial strategy with a remodeling of the stores and a revision of the product mix. The group’s commercial margin should reach around15% in 2010 (12.9% in 2009).

• Magasin General will soon launch a new brand “10 sur 10” after the acquisition of stores belonging to the bankrupt retailer BATAM (20 stores)specializing in electrical appliances.

• A capitalization that today has surpassed the amount paid by the main shareholders for their control stakes in both MG and PROMOGRO.• An expected business slowdown in 2011 due to the shutting down of a few stores as well as important damages on several other stores during thelatest riots (estimated at 50mTnd). We revise down our growth forecast for 2011.

• Our recommendation is a “Hold” for this stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

Magasin Retail sale 292mTnd 114kTnd 38.4x 7.8x 0% 18.6%Général

19

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

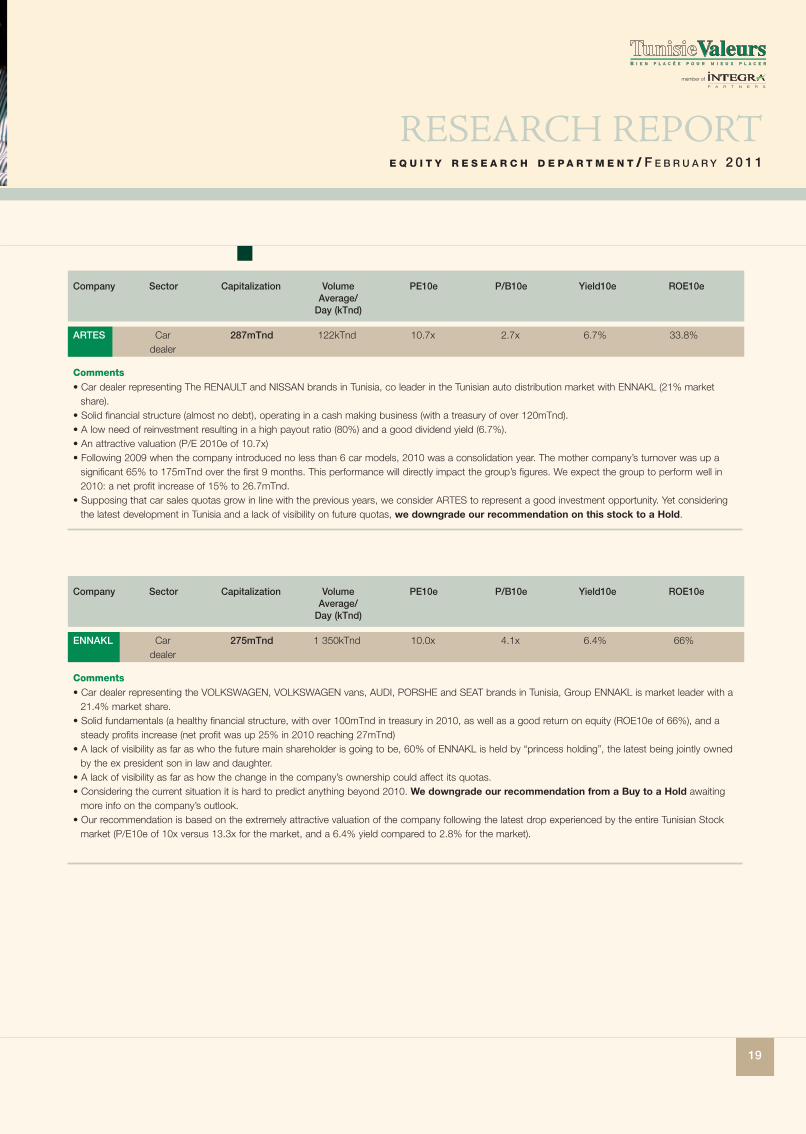

Comments• Car dealer representing The RENAULT and NISSAN brands in Tunisia, co leader in the Tunisian auto distribution market with ENNAKL (21% marketshare).

• Solid financial structure (almost no debt), operating in a cash making business (with a treasury of over 120mTnd).• A low need of reinvestment resulting in a high payout ratio (80%) and a good dividend yield (6.7%).• An attractive valuation (P/E 2010e of 10.7x)• Following 2009 when the company introduced no less than 6 car models, 2010 was a consolidation year. The mother company’s turnover was up asignificant 65% to 175mTnd over the first 9 months. This performance will directly impact the group’s figures. We expect the group to perform well in2010: a net profit increase of 15% to 26.7mTnd.

• Supposing that car sales quotas grow in line with the previous years, we consider ARTES to represent a good investment opportunity. Yet consideringthe latest development in Tunisia and a lack of visibility on future quotas, we downgrade our recommendation on this stock to a Hold.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

ARTES Car 287mTnd 122kTnd 10.7x 2.7x 6.7% 33.8%dealer

Comments• Car dealer representing the VOLKSWAGEN, VOLKSWAGEN vans, AUDI, PORSHE and SEAT brands in Tunisia, Group ENNAKL is market leader with a21.4% market share.

• Solid fundamentals (a healthy financial structure, with over 100mTnd in treasury in 2010, as well as a good return on equity (ROE10e of 66%), and asteady profits increase (net profit was up 25% in 2010 reaching 27mTnd)

• A lack of visibility as far as who the future main shareholder is going to be, 60% of ENNAKL is held by “princess holding”, the latest being jointly ownedby the ex president son in law and daughter.

• A lack of visibility as far as how the change in the company’s ownership could affect its quotas.• Considering the current situation it is hard to predict anything beyond 2010. We downgrade our recommendation from a Buy to a Hold awaitingmore info on the company’s outlook.

• Our recommendation is based on the extremely attractive valuation of the company following the latest drop experienced by the entire Tunisian Stockmarket (P/E10e of 10x versus 13.3x for the market, and a 6.4% yield compared to 2.8% for the market).

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

ENNAKL Car 275mTnd 1 350kTnd 10.0x 4.1x 6.4% 66%dealer

20

Comments• 59.11% owned by Air Liquide International, world leader in the gaz industry (industrial and medical gaz as well as all services associated to these gazes).• Sales growth of 4.6% to 24mTnd compared to 2009.• A 2010 consolidated turnover of around 57mTnd and a consolidated net result of 11.5mTnd (+6.5% compared to 2009)• The launch of a new installation in charge of the conditioning of ultra pure gazes as well as mixed gazes in order to be able to create a new azote andoxygen production unit that will help the group’s growth.

• An attractive return on equity (ROE of 37.3%).• Even though the free float represents 10.73% of the company’s capital, the stock remains illiquid.• Considering its high valuation (P/E 2010e of 22.8). We recommend a Hold for this stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

Air Chemicals 262mTnd 9kTnd 22.8 6.3 3.6% 37.3%Liquide

Comments• A well diversified financial group (leasing + factoring + fleet management) operating in both Tunisia and Algeria.• Tunisie Leasing has historically been market leader (today it has over 20% of market share in Tunisia).• Its Algerian subsidiary has been operational for the past three years. Nevertheless the company’s growth potential is enormous in this neighboringmarket, where the company’ strategy is now to expand its network.

• Good risk management resulting in an excellent portfolio quality: 5% in NPLs, and a coverage ratio of 88%.• The company’s good risk management allows us to believe in the company’s potential in spite of the deteriorating economic environment.• The group is planning to further expand its business into Libya.• We recommend to Buy the stock

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

TL Leasing 220mTnd 182kTnd 13.8x 2.7x 2.7% 25%

21

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

Comments• Market leader in the aluminum business with 80% market share.• A recovery in sales in 2010 (+25%) in both the local market as well as exports following a tough 2009 crisis year.• The company recorded a good gross margin in 2010 almost reaching the 40% level, in spite of the a sharp increase (+35%) of the world aluminumprices over the past year.

• Investments made into new machinery in 2010 that should allow the company to increase its productivity by 50% during the following 3 years.• A solid financial structure (negative gearing).• A comfortable cash flow resulting in a good dividend yield (4.6%, one of the highest in the industrial sector).• Its Libyan project has been postponed until a new partner is found, while the Algerian project is at an advanced stage. The Algerian factory should startproduction in 2011.

• Solid fundamentals as well as an Algerian exposure: these two points are not reflected into the current share price. We recommend to Buy the stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

TPR Aluminum 202mTnd 161kTnd 11.5x 2.4x 4.6% 26%Profiles

Comments• Air transport group with 9 subsidiaries amongst which a handling subsidiary, a catering subsidiary, a local air company, and a Mauritanian air company,«Airways».

• Direct exposure to the fuel price volatility that conditions the group’s profitability.• Big delays in issuing their financial statements each and every past year (5 months over the deadline in 2010).• 2011 will be a difficult year for the tourism sector.• Persisting problems with Mauritania Airways, that has just been suspended from flying in and out of the European Union (this subsidiary is 51% ownedby Tunisair).

• The soon to be implied open sky rules will result in a fierce competition.• The company is planning to buy new planes (a cost of 2000mTnd) that will surely put a dent into the group’s cash flow.• The share price is trading at a significant discount, yet the company’s outlook remains uncertain. We recommend a Hold on this stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

Tunisair Air 198mTnd 91kTnd 3.5x 0.3x 0% 9.2%transport

22

Comments• This fund is mostly invested in SFBT group (60% of the fund is invested into the group’s subsidiaries or in commercial paper to finance SFBT Group).• The fund is anticipating two exceptional years (2010 and 2011) due to a substantial increase in received dividends from real estate company «Dame» ,subsidiary of SFBT group, (with SPDIT owning 43% of its capital). We expect this dividend to be around 0.5Tnd/share, which corresponds to a payout of78% (versus 0.340Tnd/share in 2009).

• The share price trades at a 13% discount compared to its re-evaluated net asset value (that we estimate at 194mTnd). We believe that we are have herea good investment opportunity with a good dividend yield of 7.9% in 2010.

• We upgraded our recommendation from a Hold to a Buy on this stock

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

SPDIT Private and Listed 170mTnd 39kTnd 9.9x 0.9x 7.9% 35.8%Equities Fund

Comments• Pioneer and market leader in the reinsurance sector (21.6% in market share).• The only pure reinsurance company in Tunisia, all its competitors are insurance companies that occasionally do reinsurance policies.• A well diversified portfolio, with a well balanced geographical exposure (30% of Tunis Re’s turnover comes from reinsuring foreign companies based inthe Middle East, Maghreb, Africa, Europe, and Asia).

• A solid financial structure: A coverage ratio of technical provisions of 125%.• The company suffers a number of weaknesses with the main two points are:(1) Its capital needs have impacted its rating. Tunis Re is currently rated at B+ by AM Best making it difficult to access new markets. As a result thecompany has undergone a capital increase during its IPO in order to strengthen its shareholders equity. It is now planning to proceed to a second capitalincrease during this year hoping to raise a further 62mTnd(2) A low profitability, with a ROE of 11% which is poised to drop further down following the upcoming capital increase.

• All together, and considering a stock market performance of more than 80% since its IPO, we recommend a Hold on this stock with positiveoutlook, awaiting to see how things will unfold after the capital increase.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

TUNIS RÉ Insurance 110mTnd 441kTnd 17.2x 1.9x 3.1% 11.0%

23

E Q U I T Y R E S E A R C H D E PA R T M E N T / F E B R U A R Y 2 0 1 1

RESEARCH REPORT

member of

Comments• Market leader in the auto batteries business with more than 60% market share.• The company was able to preserve its margins in spite of the lead price volatility (gross margin exceeding 40%).• A solid financial structure (gearing of 45%), enabling the company to benefit from a positive leverage effect and at the same time improving its profitability(33%).

• A positive outlook due to (1) investments done over the past few years allowing the company to benefit from its production capacity, (2) the Algeriansubsidiary’s growth potential (3) as well as the group’s ambitions to expand in the region. Nevertheless the company’s regional outlook remainsdependent on the social/economical environment in our neighboring countries, Algeria and Libya.

• An attractive valuation (PE 10e equal to 11.4x and a yield of 3.7%).• We recommend to Buy stock

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

ASSAD Car 109mTnd 93kTnd 11.4x 2.7x 3.7% 32.7%parts

Comments• Lost market share in 2009 due to a business growth lower than the sector’s average. The company ranks 3rd in terms of market share and ATL iscurrently its main competitor.

• Loans are up at an average of 15%/year since 2007, while preserving its portfolio quality (6.5% in NPLs, 94% coverage ratio).• A good productivity: the lowest cost to income ratio in the sector (30%).• The company’s valuation has become attractive following the sharp share price drop during the month of January. We will keep our recommendationunchanged “Buy” on this stock.

Company Sector Capitalization Volume PE10e P/B10e Yield10e ROE10eAverage/Day (kTnd)

CIL Leasing 100.4mTnd 144kTnd 12x 2.5x 3.2% 29%

Securities Brokerage - Asset Management - Primary Dealer - Listing SponsorRESEARCH DEPARTMENT : (216) 71 18 96 00

F e b r u a r y 2 0 1 1

www. t u n i s i e v a l e u r s . c [email protected]

E q u i t y R e s e a r c h D e p a r t m e n t

Conc

eptio

n,ré

alis

atio

net

impr

essi

onw

ww

.sim

pact

.com

.tn

member of

Historical Head Office – City of Belvédère

![Adagio en Sol mineur [J.M.E.16] - Free-scores.com · Jawher Matmati Arrangeur, Compositeur, Interprete, Editeur Tunisie A propos de l'artiste Né le 29 Janvier 1993 à Tunis, il a](https://static.fdocuments.nl/doc/165x107/60cdd979b3caaa6c18051e24/adagio-en-sol-mineur-jme16-free-jawher-matmati-arrangeur-compositeur-interprete.jpg)