Manu Mam Term Paper

39

Havells India Ltd. INTRODUCTION Mr. Qimat Rai Gupta is the Founder Chairman and Managing Director of Havells India Ltd.´ His leadership and vision led him to create QRG Enterprises as one of the players in the power distribution equipment industry as well as make its mark on the global space. His belief in team work, implementation of the decisions, communication and transparency through ethical values, business integrity and technological expertise have made the QRG group and especially Havells India Ltd the largest player low voltage power distribution equipment industry in India and a name to reckon within the global market. The company¶s phenomenal success over the years has been due to Mr. Qimat Rai Gupta¶s mantra, ³Growth through quality, innovation and market consolidation". His focus on research and development has enabled Havells develop products for consumers that offer great value. His constant emphasis on promoting energy conservation and environmental preservation coupled with his philanthropic service to the economically weaker section of the society is his way of giving back in return to the society that has helped this organization realize its true potential. Havells India Ltd is a billion-dollar-plus Indian electrical equipment company with products ranging from industrial & domestic circuit protection switchgear, cables & wires, motors, fans, power capacitors, compact fluorescent lamps (CFL), and luminaries for domestic, commercial & industrial applications, modular switches covering household, commercial and industrial electrical needs. The company is listed on the Bombay Stock Exchange. Havells owns global brands like Crabtree, Sylvania, Concord, Luminance, and Linolite & SLI Lighting. Havells has 91 branches / representative offices and over 8000 professionals in over 50 countries. Its seven manufacturing plants in India are located at

-

Upload

subodh-kumar -

Category

Documents

-

view

217 -

download

0

Transcript of Manu Mam Term Paper

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 1/39

Havells India Ltd.

INTRODUCTION

Mr. Qimat Rai Gupta is the Founder Chairman and Managing

Director of Havells India Ltd.´ His leadership and vision led him tocreate QRG Enterprises as one of the players in the power distribution

equipment industry as well as make its mark on the global space.

His belief in team work, implementation of the decisions,

communication and transparency through ethical values, business

integrity and technological expertise have made the QRG group and

especially Havells India Ltd the largest player low voltage power

distribution equipment industry in India and a name to reckon within

the global market. The company¶s phenomenal success over the yearshas been due to Mr. Qimat Rai Gupta¶s mantra, ³Growth through

quality, innovation and market consolidation". His focus on research

and development has enabled Havells develop products for consumers

that offer great value. His constant emphasis on promoting energy

conservation and environmental preservation coupled with his

philanthropic service to the economically weaker section of the

society is his way of giving back in return to the society that has

helped this organization realize its true potential.

Havells India Ltd is a billion-dollar-plus Indian electrical equipment

company with products ranging from industrial & domestic circuit

protection switchgear, cables & wires, motors, fans, power capacitors,

compact fluorescent lamps (CFL), and luminaries for domestic,

commercial & industrial applications, modular switches covering

household, commercial and industrial electrical needs. The companyis listed on the Bombay Stock Exchange.

Havells owns global brands like Crabtree, Sylvania, Concord,

Luminance, and Linolite & SLI Lighting. Havells has 91 branches /

representative offices and over 8000 professionals in over 50

countries. Its seven manufacturing plants in India are located at

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 2/39

Haridwar, Baddi, Noida, Faridabad, Alwar, Neemrana, and 8

manufacturing plants are located across Europe, Latin America &

Africa. It has a 20,000 strong global distribution network

Products:-� Building Circuit Protection

o Miniature Circuit Breaker (MCB)o Changeover Switch

o Residual Current Circuit Breaker (RCCB)

o Nylon Fuse Baseo Fuse Link and Fuse Base

o RCBOo Distribution Board (DB)

o Indicator Light

� Industrial Circuit Protection

o Air Circuit Breaker o MCCB

o Nylon Fuse Base

o Fuse Link and Fuse Base

� Motors o Inverter Duty Motors with Forced Cooling

o Crane Duty Motorso Brake Motors`

� Capacitors

o Normal Dutyo Heavy Duty

o Super Heavy Dutyo Agriculture Duty

o Motor Run Capacitors

� Lighting

Consumer lighting

o Commercial Lighting

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 3/39

o down Lighter

o Area Lightingo Road Lighting

o Specialty Lamps

� CFL

� Fans

Corporate:-

The QRG Group defines corporate governance strategically, which

encompasses not only what Havells does as a company with their

profits, but also how they make them. Company addresses how thecompany manages its economic, social, and environmental impacts,

as well as its relationships in all key spheres of influence: the

workplace, the marketplace, the supply chain, the community, and the

public policy realm. Their eco responsibility initiative also focuses on

how they run their business, and includes efforts to develop an

alternative-energy strategy, and thus reduce the environmental

impact of their operations.

Corporate Social Responsibility

Havells contributes to socially responsible activities, like providing

mid-day meal in government schools in Alwar district, covering

15000 students per day. Besides this the company has acquired land

for constructing a larger kitchen with all the modern facilities to serve

freshly cooked food to 50000 students in the area. Havells runs a

mobile Medical Van, equipped with a trained doctor and necessary

medicines in the rural areas of Delhi & NCR for the very poor and

needy villagers. They have also set up free medical check-up camps.In the past, the company has also contributed to the society during

various national calamities like the Bihar Flood, Tsunami and Kargil

National Relief Fund etc.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 4/39

Retail initiatives

The company has been promoting its brand through sponsorship of

cricket events like Champions Trophy, Champions League, IPL

Season 2, IPL Season1, and T20 World Cup. The company has also

taken the initiative to reach directly to the consumers through

"Havells Galaxy" ± a one stop shop for all electrical and lighting

needs. This is yet another initiative by Havells targeted at end-users,

architects and Consultants, to showcase Havells products. The

products they offer combine the attributes of elegance, technological

advancement and convenience all in one.

HavellsWorld

Havells announced the opening of its first display & learning centres

µHavells World¶ in the country on 29th March, 2010, New Delhi.

Havells has also opened its first Havells World in Mumbai. Havells

World is targeted at the retailer community, involved in retailing the

Havells electrical and lighting products. The Company aims to

accelerate its growth with this initiative and plans to open 10 such

stores in the country. It will serve as the reference location for all the

retailers to get a comprehensive overview of the entire range of theHavells µproducts.

Giving the consumers, a much wider choice in electrical consumer

products, the Havells World will offer an end to end solution to all

electrical needs from the time electricity enters home to the light

output. Havells World brings to its consumer a wide range in stylish

and high quality low voltage electrical equipments including; Cables,

Wires, Fans, CFLs, LED Lightings, Lighting Fixtures, Crabtree

switches, Motors and Domestic & Industrial Switchgears etc.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 5/39

REFRENCES

1. http://en.wikipedia.org/wiki/Havells

2. Wikipedia articles with possible conflicts of interest from June

2010 | Articles needing additional references from July 2010

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 6/39

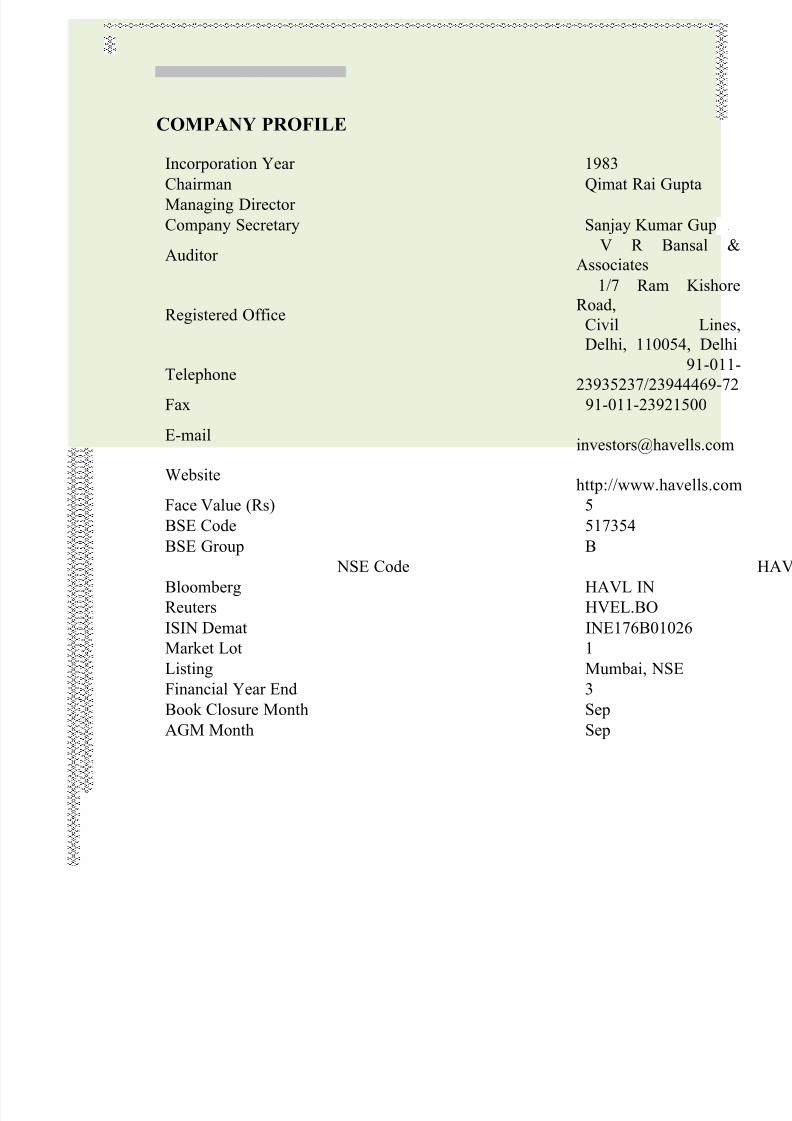

COMPANY PROFILE

Incorporation Year 1983

Chairman Qimat Rai Gupta

Managing Director

Company Secretary Sanjay Kumar Gu

Auditor V R Bansa

Associates

Registered Office

1/7 Ram Ki

Road,

Civil L

Delhi, 110054, D

Telephone91

23935237/239444

Fax 91-011-23921500

E-mailinvestors@havells

Websitehttp://www.havell

Face Value (Rs) 5

BSE Code 517354BSE Group B

NSE Code

Bloomberg HAVL IN

Reuters HVEL.BO

ISIN Demat INE176B01026

Market Lot 1

Listing Mumbai, NSE

Financial Year End 3Book Closure Month Sep

AGM Month Sep

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 7/39

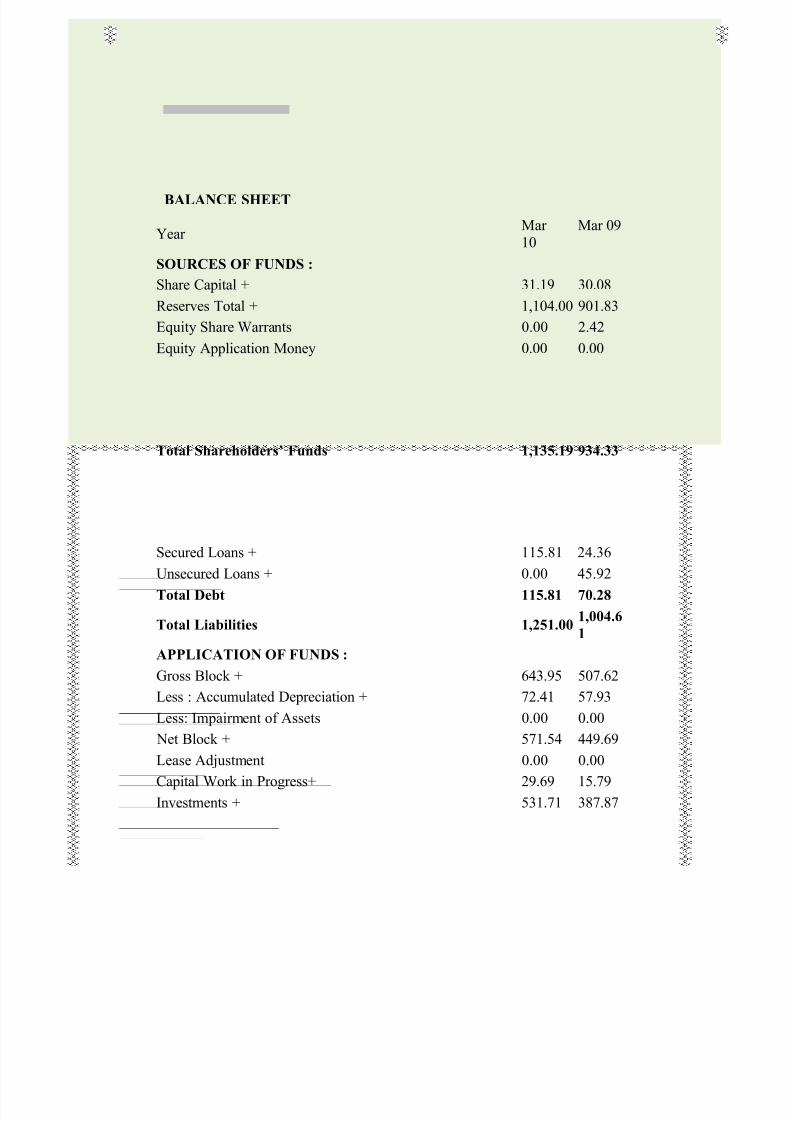

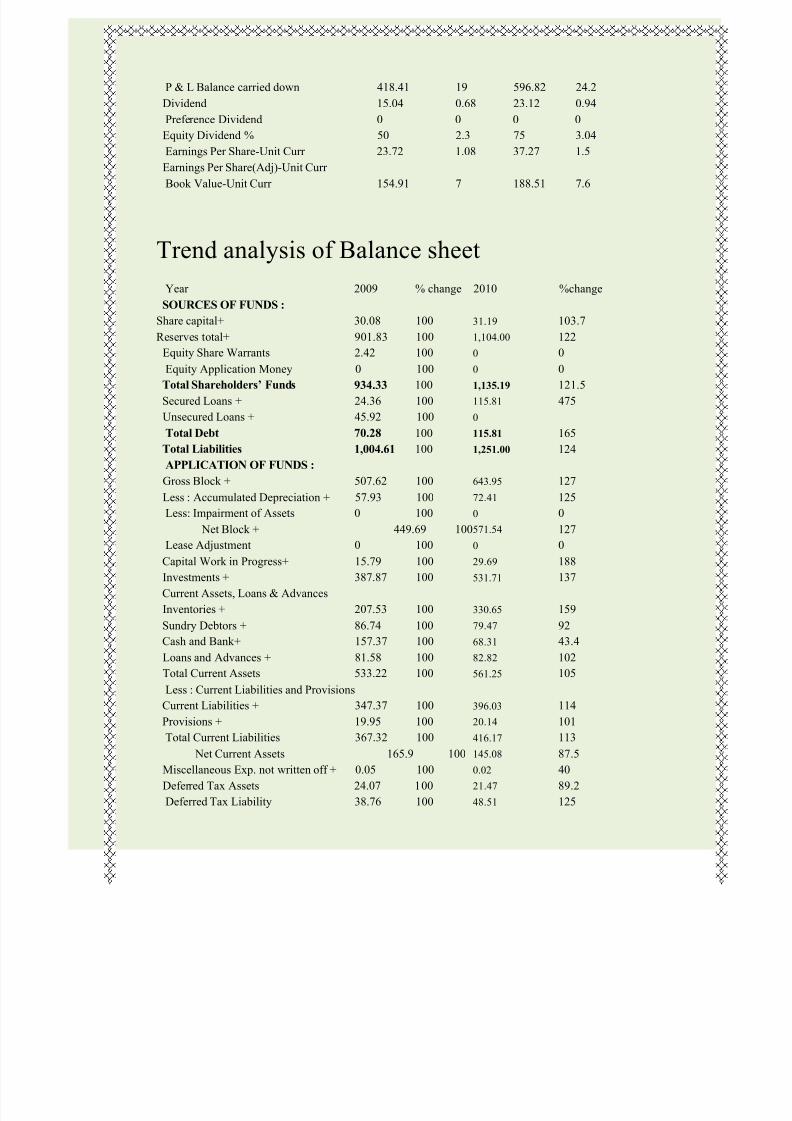

BALANCE SHEET

Year Mar 10

Mar 09

SOURCES OF FUNDS :

Share Capital +

31.19 30.08

Reserves Total +

1,104.00 901.83

Equity Share Warrants 0.00 2.42

Equity Application Money 0.00 0.00

Total Shareholders¶ Funds 1,135.19 934.33

Secured Loans +

115.81 24.36

Unsecured Loans +

0.00 45.92

Total Debt 115.81 70.28

Total Liabilities 1,251.00 1,004.6

1

APPLICATION OF FUNDS :

Gross Block + 643.95 507.62

Less : Accumulated Depreciation + 72.41 57.93

Less: Impairment of Assets 0.00 0.00

Net Block + 571.54 449.69

Lease Adjustment 0.00 0.00

Capital Work in Progress+ 29.69 15.79

Investments + 531.71 387.87

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 8/39

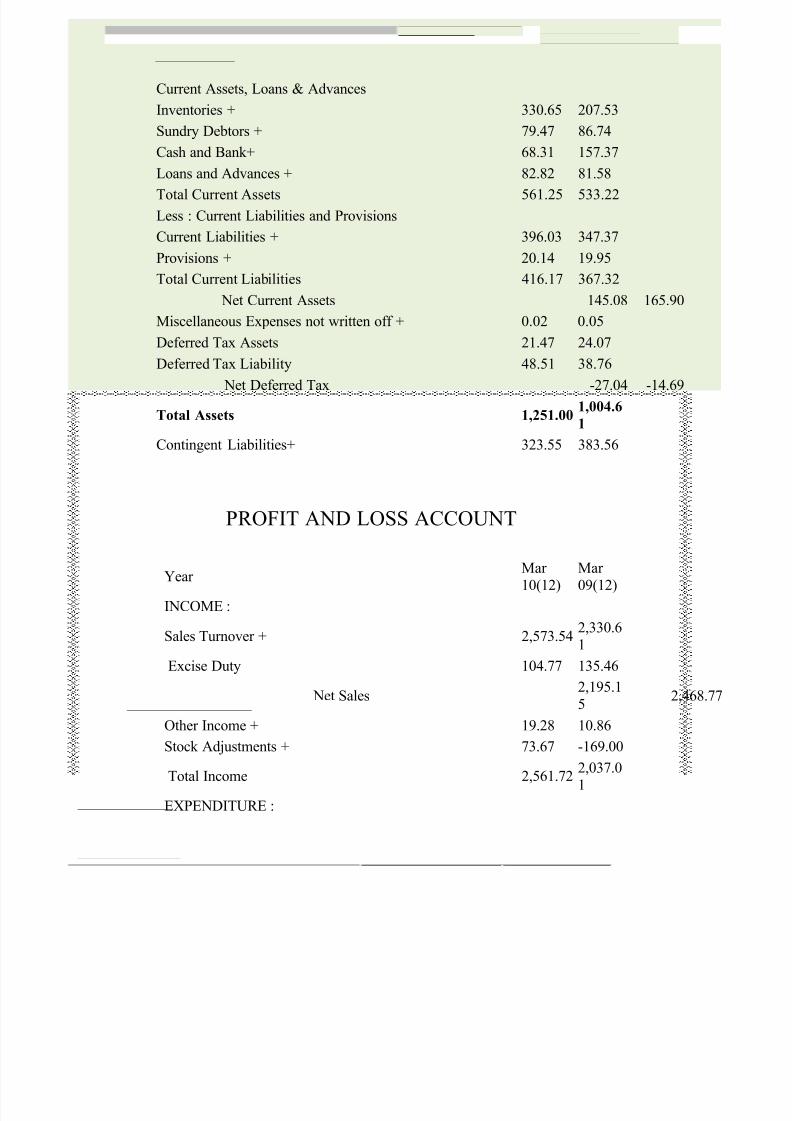

Current Assets, Loans & Advances

Inventories + 330.65 207.53

Sundry Debtors +

79.47 86.74

Cash and Bank+ 68.31 157.37

Loans and Advances + 82.82 81.58Total Current Assets 561.25 533.22

Less : Current Liabilities and Provisions

Current Liabilities + 396.03 347.37

Provisions + 20.14 19.95

Total Current Liabilities 416.17 367.32

Net Current Assets 145.08 165.90

Miscellaneous Expenses not written off +

0.02 0.05

Deferred Tax Assets 21.47 24.07Deferred Tax Liability 48.51 38.76

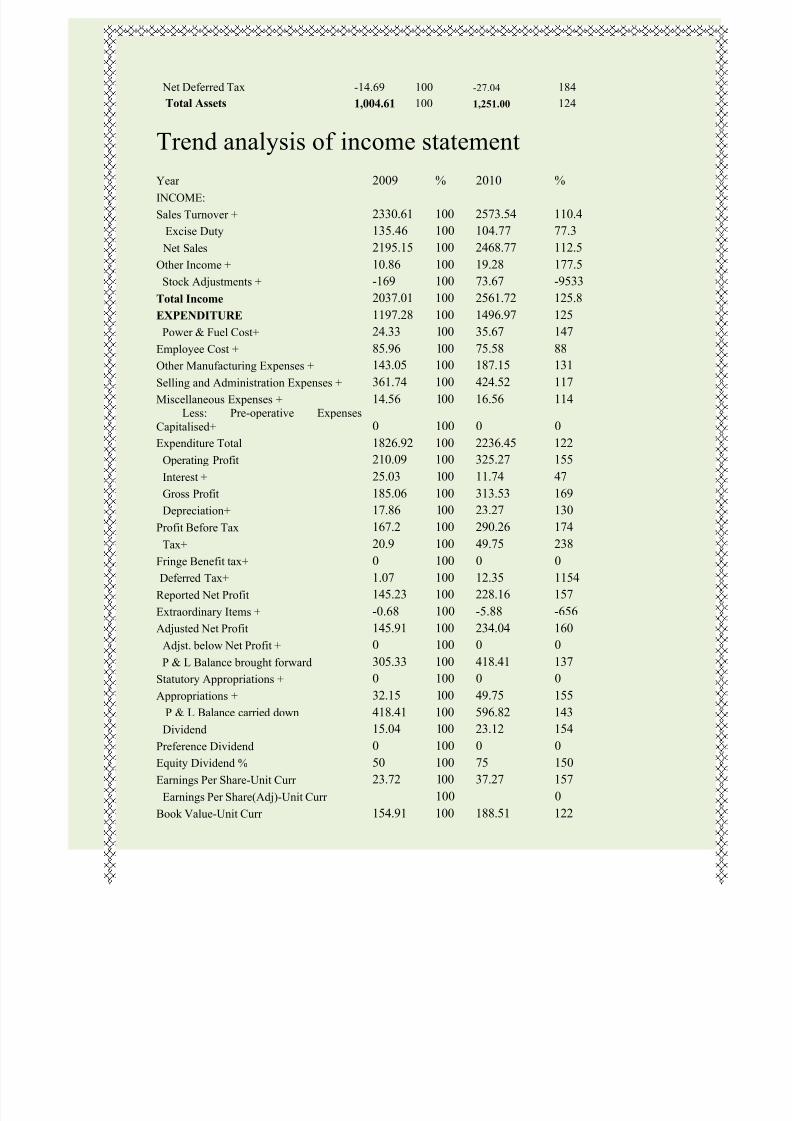

Net Deferred Tax -27.04 -14.69

Total Assets 1,251.00 1,004.6

1

Contingent Liabilities+ 323.55 383.56

PROFIT AND LOSS ACCOUNT

Year Mar 10(12)

Mar 09(12)

INCOME :

Sales Turnover + 2,573.542,330.61

Excise Duty 104.77 135.46

Net Sales 2,4682,195.15

Other Income + 19.28 10.86

Stock Adjustments + 73.67 -169.00

Total Income 2,561.722,037.01

EXPENDITURE :

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 9/39

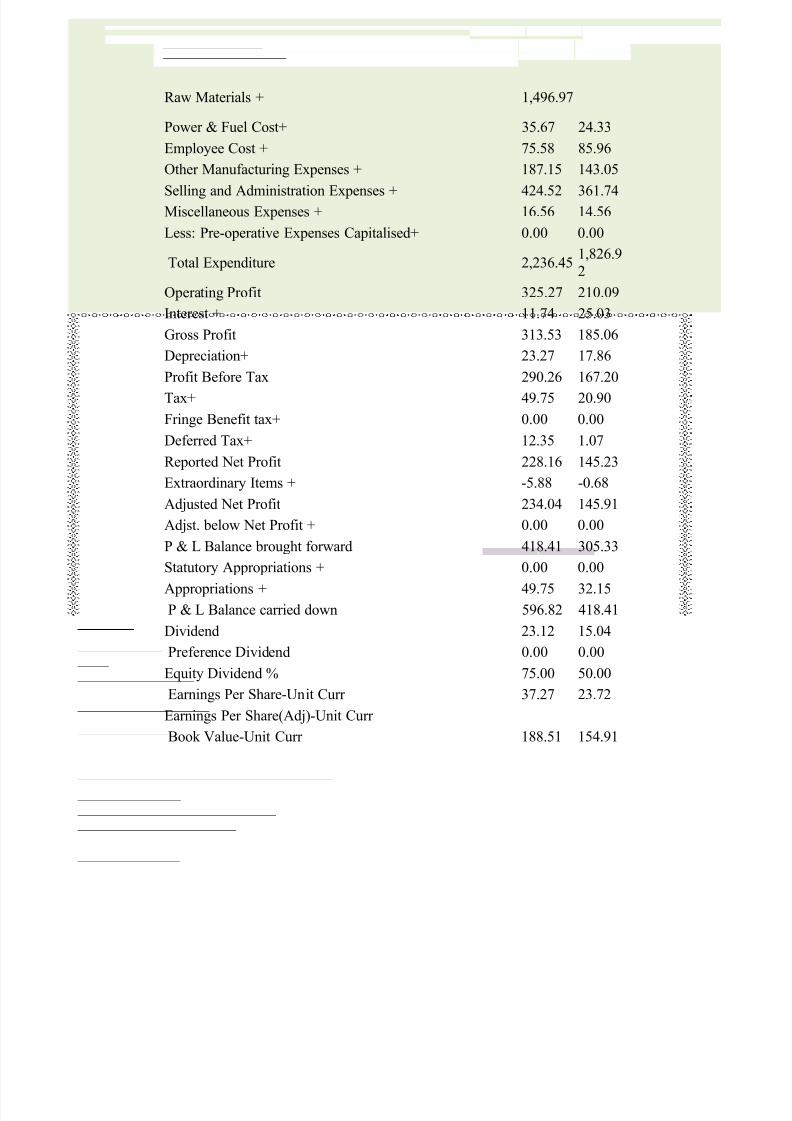

Raw Materials + 1,496.97

Power & Fuel Cost+ 35.67 24.33

Employee Cost + 75.58 85.96

Other Manufacturing Expenses + 187.15 143.05Selling and Administration Expenses + 424.52 361.74

Miscellaneous Expenses + 16.56 14.56

Less: Pre-operative Expenses Capitalised+ 0.00 0.00

Total Expenditure 2,236.451,826.9

2

Operating Profit 325.27 210.09

Interest + 11.74 25.03

Gross Profit 313.53 185.06

Depreciation+ 23.27 17.86

Profit Before Tax 290.26 167.20

Tax+ 49.75 20.90

Fringe Benefit tax+ 0.00 0.00

Deferred Tax+ 12.35 1.07

Reported Net Profit 228.16 145.23

Extraordinary Items + -5.88 -0.68

Adjusted Net Profit 234.04 145.91

Adjst. below Net Profit + 0.00 0.00

P & L Balance brought forward 418.41 305.33

Statutory Appropriations + 0.00 0.00

Appropriations + 49.75 32.15

P & L Balance carried down 596.82 418.41

Dividend 23.12 15.04

Preference Dividend 0.00 0.00

Equity Dividend % 75.00 50.00

Earnings Per Share-Unit Curr 37.27 23.72Earnings Per Share(Adj)-Unit Curr

Book Value-Unit Curr 188.51 154.91

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 10/39

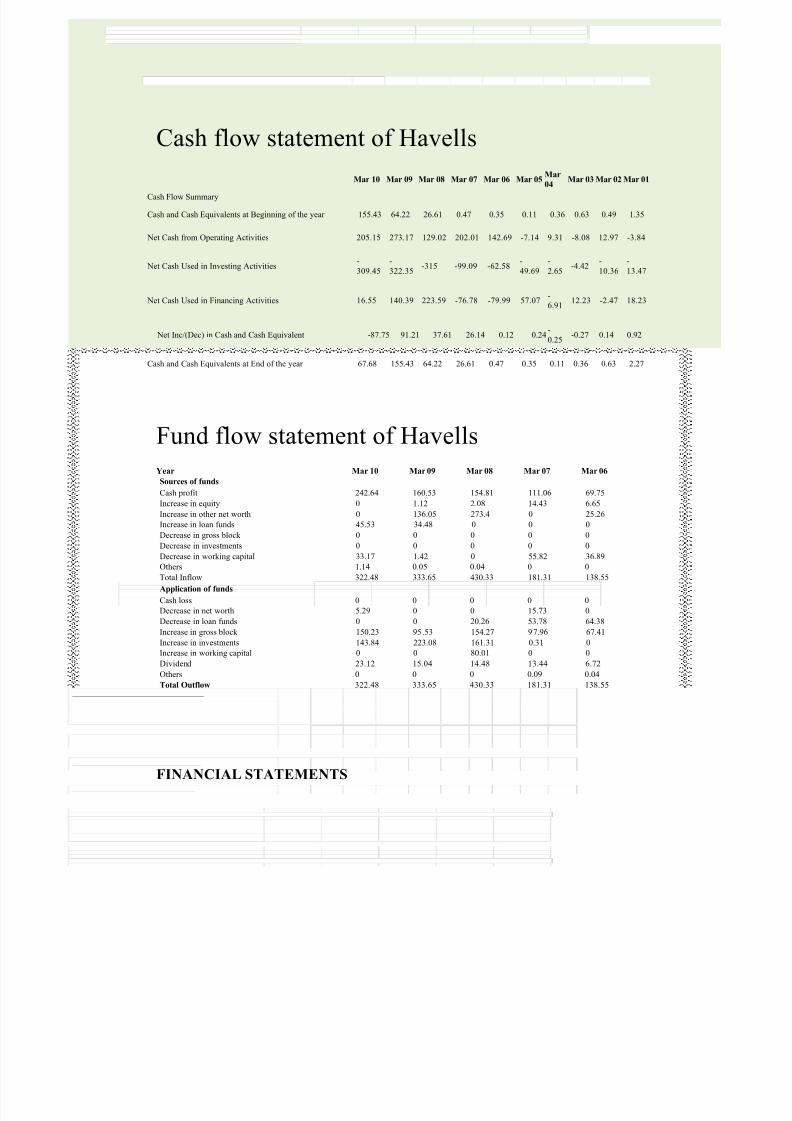

Cash flow statement of Havells

Mar 10 Mar 09 Mar 08 Mar 07 Mar 06 Mar 05 Mar04

Mar 03 Mar 02 Mar 01

Cash Flow Summary

Cash and Cash Equivalents at Beginning of the year 155.43 64.22 26.61 0.47 0.35 0.11 0.36 0.63 0.49 1.35

Net Cash from Operating Activities 205.15 273.17 129.02 202.01 142.69 -7.14 9.31 -8.08 12.97 -3.84

Net Cash Used in Investing Activities-

309.45

-

322.35-315 -99.09 -62.58

-

49.69

-

2.65-4.42

-

10.36

-

13.47

Net Cash Used in Financing Activities 16.55 140.39 223.59 -76.78 -79.99 57.07-

6.9112.23 -2.47 18.23

Net Inc/(Dec) in Cash and Cash Equivalent -87.75 91.21 37.61 26.14 0.12 0.24-

0.25-0.27 0.14 0.92

Cash and Cash Equivalents at End of the year 67.68 155.43 64.22 26.61 0.47 0.35 0.11 0.36 0.63 2.27

Fund flow statement of Havells

Year Mar 10 Mar 09 Mar 08 Mar 07 Mar 06

Sources of funds

Cash profit 242.64 160.53 154.81 111.06 69.75

Increase in equity 0 1.12 2.08 14.43 6.65

Increase in other net worth 0 136.05 273.4 0 25.26

Increase in loan funds 45.53 34.48 0 0 0

Decrease in gross block 0 0 0 0 0

Decrease in investments 0 0 0 0 0

Decrease in working capital 33.17 1.42 0 55.82 36.89

Others 1.14 0.05 0.04 0 0

Total Inflow 322.48 333.65 430.33 181.31 138.55

Application of funds

Cash loss 0 0 0 0 0

Decrease in net worth 5.29 0 0 15.73 0

Decrease in loan funds 0 0 20.26 53.78 64.38

Increase in gross block 150.23 95.53 154.27 97.96 67.41

Increase in investments 143.84 223.08 161.31 0.31 0

Increase in working capital 0 0 80.01 0 0

Dividend 23.12 15.04 14.48 13.44 6.72

Others 0 0 0 0.09 0.04

Total Outflow 322.48 333.65 430.33 181.31 138.55

FINANCIAL STATEMENTS

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 11/39

Financial statement may refer to any statement or document which discloses

financial information relating to business concern but technically financial

statement includes income statement or profit & loss account and balance sheet.

Financial statements

Income statement or trading & p/l account

Position statement or balance sheet

Statement of retained earning

Statement of changes in financial position

Tools and techniques of analysis and interpretation:-

1. Comparative financial statement or analysis ,

2. Common ±size statement or analysis

3. Trend analysis

4. Ratio analysis

5. Fund flow statement

6. Cash flow statement

7. Cost Analysis

Comparative financial statement or analysis: -

It is an important horizontal Technique in which financial data of two or more

period (year) are presented in a comparative from.

a) A comparative income statement show the comparison of various items

of cost ,expenses and final the result in form of net profit and net loss.

Percent change =absolute change /figure of the previous year *100

b) A comparative balance sheet reveals the position of assets and liabilities

on two or more different data along with changes in these items.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 12/39

Common ±size statement or analysis:-

Common size financial statement facilities both of analysis i.e.; horizontal as

well as vertical. This statement indicates the relationship of various items in

terms of percentage with some common or basis items .it expressed the net sale

in term of percentage.

Trend analysis:-

This analysis is an important tool of horizontal financial analysis .under this

method ratio are calculated for selected items of the financial statement takingthe figure of the base year as 100 and for this purpose the following formula

may be used

Trend ratio =current year amount /base year amount *100

Ratio analysis:-

Ratio analysis is also an important method of analysis of financial statement .it

is adopted to establish meaningful mathematical relation between two items or

two group of items show in financial statement.

Fund flow statement:-

Financial statement can also be analyzed by preparing fund flow statement and

in that case it is known as fund flow analysis .This statement is prepared in

order to reveal the source from which funds are obtained the uses to which they

are being put. Here fund stand for working capital.

Cash flow statement:-

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 13/39

This technique is very useful in the management of cash and analysis of short

term liquidity .under this method a statement is prepared to show the inflow and

outflow of cash related to various activities in the concern during a specific

period.

OBJECTIVE OF ANALYSIS AND INTERPRETATION:-

To determine and examine the current earning capacity and to estimate

future prospects.

To estimate overall as well as segment wise performance efficiency and

managerial ability in a business concern

To determine long term as well as segment wise performance efficiency

and managerial ability in a business concern.

To forecast the future result and prepare the budgets

To make inter-firm comparison on the basis of operational efficiency

and financial positive of various firms engaged in the same industry

To identify financial weaknesses of the firm and to suggest rem edial

measures.

To determine the growth prospects of different division as well of thefirm as a whole.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 14/39

RESEARCH METHOLOGY:-

STUDY: -

This Research is based on analysis and interpretation of financial statement, to

know the financial position of the company, identify financial weakness of thefirm and to suggest remedial.

DATA COLLECTION:-

Primary data

Secondary data

Primary data:-

Primary data are those which are collated a fresh and for the first time & thus

happen to be original in character. Primary data is obtained by the study

specially designed to fulfil the data needs to problem hand. Such data are

original in characters generated by the way of conducting survey

Secondary data:-

Secondary data are those which have already been collected by someone else

and which have already been passed through the statistical process. Secondary

data consists of not only published records and reports but also unpublished

records.

We are using secondary data in our research.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 15/39

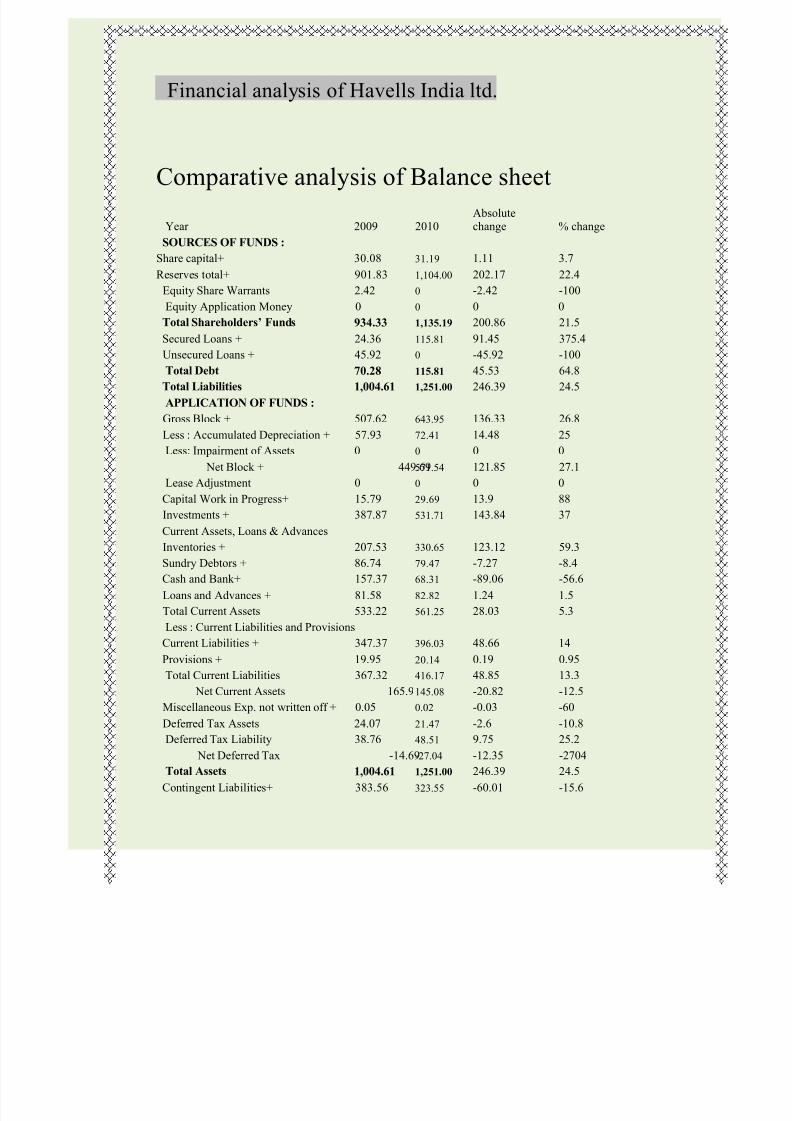

Financial analysis of Havells India ltd.

Comparative analysis of Balance sheet

Year 2009 2010Absolutechange % change

SOURCES OF FUNDS :

Share capital+

30.08 31.19 1.11 3.7

Reserves total+ 901.83 1,104.00 202.17 22.4

Equity Share Warrants 2.42 0 -2.42 -100

Equity Application Money 0 0 0 0

Total Shareholders¶ Funds 934.33 1,135.19 200.86 21.5

Secured Loans + 24.36 115.81 91.45 375.4

Unsecured Loans + 45.92 0 -45.92 -100

Total Debt 70.28 115.81 45.53 64.8

Total Liabilities 1,004.61 1,251.00 246.39 24.5

APPLICATION OF FUNDS :

Gross Block + 507.62 643.95 136.33 26.8

Less : Accumulated Depreciation + 57.93 72.41 14.48 25

Less: Impairment of Assets 0 0 0 0

Net Block + 449.69571.54 121.85 27.1

Lease Adjustment 0 0 0 0

Capital Work in Progress+ 15.79 29.69 13.9 88

Investments + 387.87 531.71 143.84 37Current Assets, Loans & Advances

Inventories + 207.53 330.65 123.12 59.3

Sundry Debtors + 86.74 79.47 -7.27 -8.4

Cash and Bank+ 157.37 68.31 -89.06 -56.6

Loans and Advances + 81.58 82.82 1.24 1.5

Total Current Assets 533.22 561.25 28.03 5.3

Less : Current Liabilities and Provisions

Current Liabilities + 347.37 396.03 48.66 14

Provisions + 19.95 20.14 0.19 0.95

Total Current Liabilities 367.32 416.17 48.85 13.3

Net Current Assets 165.9145.08 -20.82 -12.5Miscellaneous Exp. not written off + 0.05 0.02 -0.03 -60

Deferred Tax Assets 24.07 21.47 -2.6 -10.8

Deferred Tax Liability 38.76 48.51 9.75 25.2

Net Deferred Tax -14.69-27.04 -12.35 -2704

Total Assets 1,004.61 1,251.00 246.39 24.5

Contingent Liabilities+ 383.56 323.55 -60.01 -15.6

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 16/39

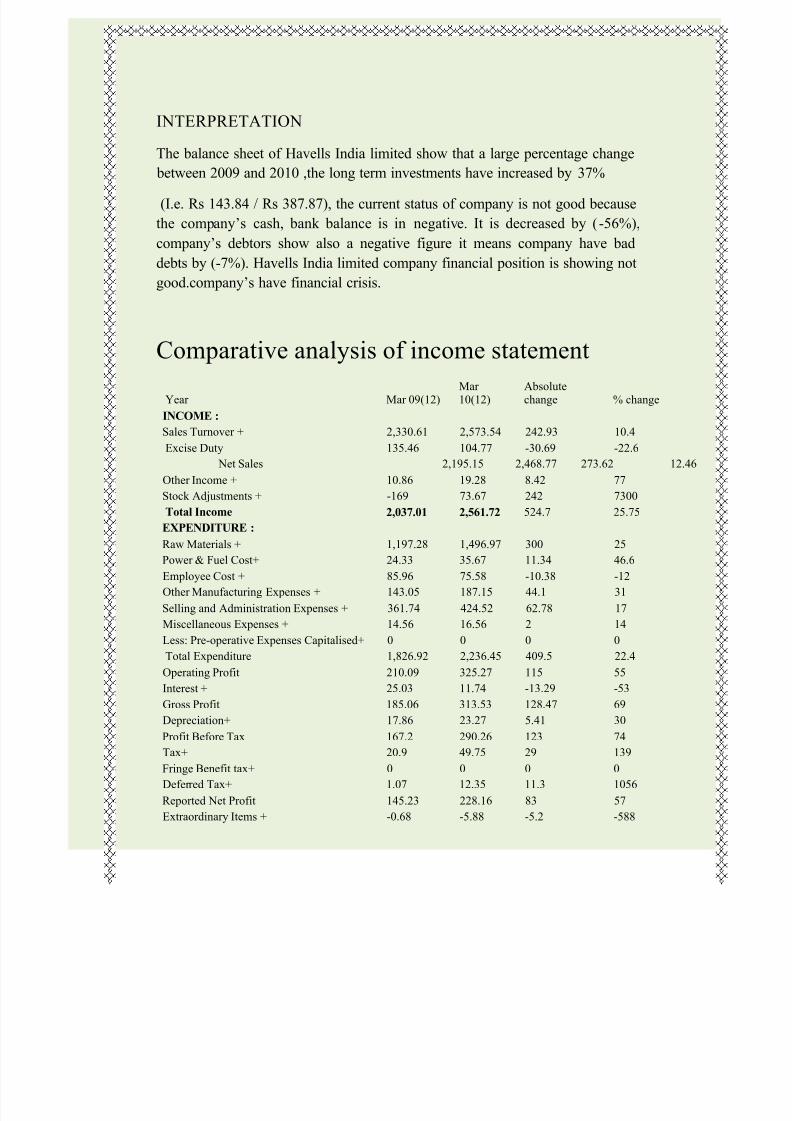

INTERPRETATION

The balance sheet of Havells India limited show that a large percentage change

between 2009 and 2010 ,the long term investments have increased by 37%

(I.e. Rs 143.84 / Rs 387.87), the current status of company is not good because

the company¶s cash, bank balance is in negative. It is decreased by (-56%),

company¶s debtors show also a negative figure it means company have bad

debts by (-7%). Havells India limited company financial position is showing not

good.company¶s have financial crisis.

Comparative analysis of income statement

Year Mar 09(12)Mar 10(12)

Absolutechange % change

INCOME :

Sales Turnover + 2,330.61 2,573.54 242.93 10.4

Excise Duty 135.46 104.77 -30.69 -22.6

Net Sales 2,195.15 2,468.77 273.62 12.46

Other Income + 10.86 19.28 8.42 77

Stock Adjustments + -169 73.67 242 7300

Total Income 2,037.01 2,561.72 524.7 25.75

EXPENDITURE :

Raw Materials + 1,197.28 1,496.97 300 25

Power & Fuel Cost+ 24.33 35.67 11.34 46.6

Employee Cost + 85.96 75.58 -10.38 -12

Other Manufacturing Expenses + 143.05 187.15 44.1 31

Selling and Administration Expenses + 361.74 424.52 62.78 17

Miscellaneous Expenses + 14.56 16.56 2 14

Less: Pre-operative Expenses Capitalised+ 0 0 0 0

Total Expenditure 1,826.92 2,236.45 409.5 22.4

Operating Profit 210.09 325.27 115 55

Interest + 25.03 11.74 -13.29 -53

Gross Profit 185.06 313.53 128.47 69

Depreciation+ 17.86 23.27 5.41 30

Profit Before Tax 167.2 290.26 123 74

Tax+ 20.9 49.75 29 139

Fringe Benefit tax+ 0 0 0 0

Deferred Tax+ 1.07 12.35 11.3 1056

Reported Net Profit 145.23 228.16 83 57

Extraordinary Items + -0.68 -5.88 -5.2 -588

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 17/39

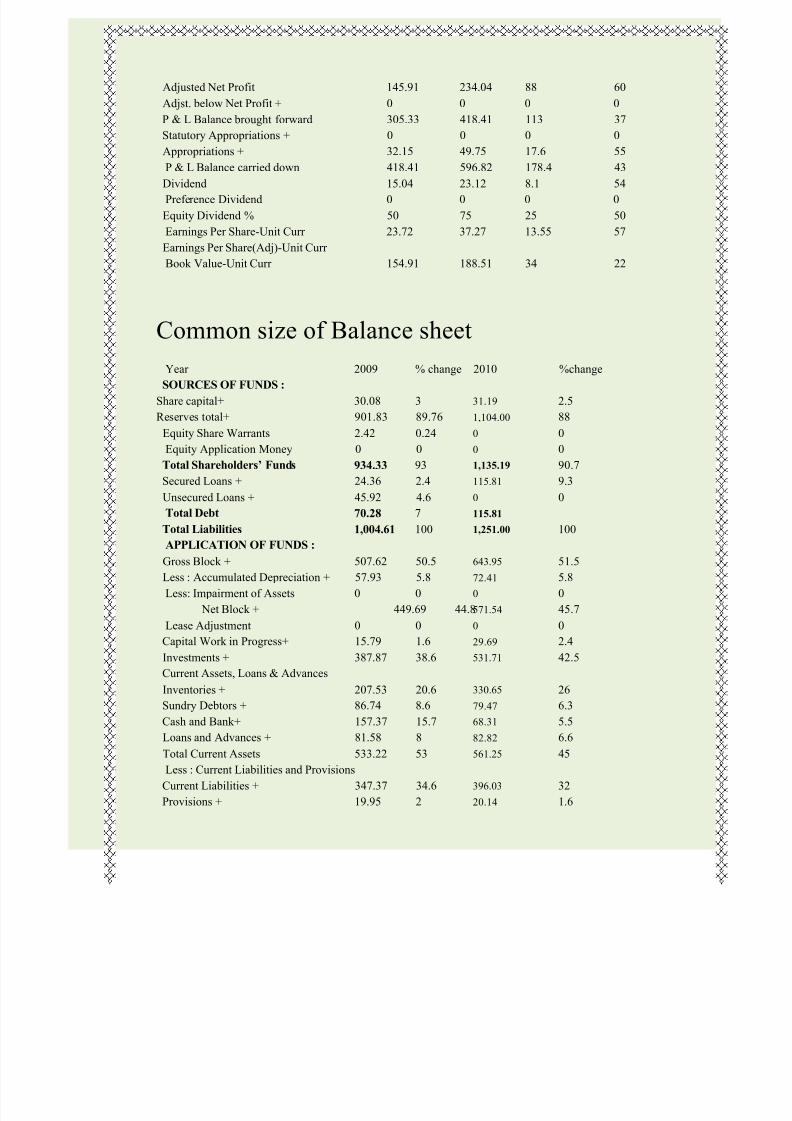

Adjusted Net Profit 145.91 234.04 88 60

Adjst. below Net Profit + 0 0 0 0

P & L Balance brought forward 305.33 418.41 113 37

Statutory Appropriations + 0 0 0 0

Appropriations + 32.15 49.75 17.6 55

P & L Balance carried down 418.41 596.82 178.4 43Dividend 15.04 23.12 8.1 54

Preference Dividend 0 0 0 0

Equity Dividend % 50 75 25 50

Earnings Per Share-Unit Curr 23.72 37.27 13.55 57

Earnings Per Share(Adj)-Unit Curr

Book Value-Unit Curr 154.91 188.51 34 22

Common size of Balance sheet

Year 2009 % change 2010 %change

SOURCES OF FUNDS :

Share capital+

30.08 3 31.19 2.5

Reserves total+ 901.83 89.76 1,104.00 88

Equity Share Warrants 2.42 0.24 0 0

Equity Application Money 0 0 0 0

Total Shareholders¶ Funds 934.33 93 1,135.19 90.7

Secured Loans + 24.36 2.4 115.81 9.3

Unsecured Loans + 45.92 4.6 0 0

Total Debt 70.28 7 115.81

Total Liabilities 1,004.61 100 1,251.00 100

APPLICATION OF FUNDS :

Gross Block + 507.62 50.5 643.95 51.5

Less : Accumulated Depreciation + 57.93 5.8 72.41 5.8

Less: Impairment of Assets 0 0 0 0

Net Block + 449.69 44.8571.54 45.7

Lease Adjustment 0 0 0 0

Capital Work in Progress+ 15.79 1.6 29.69 2.4

Investments + 387.87 38.6 531.71 42.5

Current Assets, Loans & Advances

Inventories + 207.53 20.6 330.65 26Sundry Debtors + 86.74 8.6 79.47 6.3

Cash and Bank+ 157.37 15.7 68.31 5.5

Loans and Advances + 81.58 8 82.82 6.6

Total Current Assets 533.22 53 561.25 45

Less : Current Liabilities and Provisions

Current Liabilities + 347.37 34.6 396.03 32

Provisions + 19.95 2 20.14 1.6

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 18/39

Total Current Liabilities 367.32 36.6 416.17 33

Net Current Assets 165.9 16.5 145.08 12

Miscellaneous Exp. not written off + 0.05 0.005 0.02 0.002

Deferred Tax Assets 24.07 2.4 21.47 1.7

Deferred Tax Liability 38.76 4 48.51 3.8

Net Deferred Tax -14.69 -1.5 -27.04 -2.16Total Assets 1,004.61 100 1,251.00 100

Contingent Liabilities+ 383.56 38.18 323.55 26

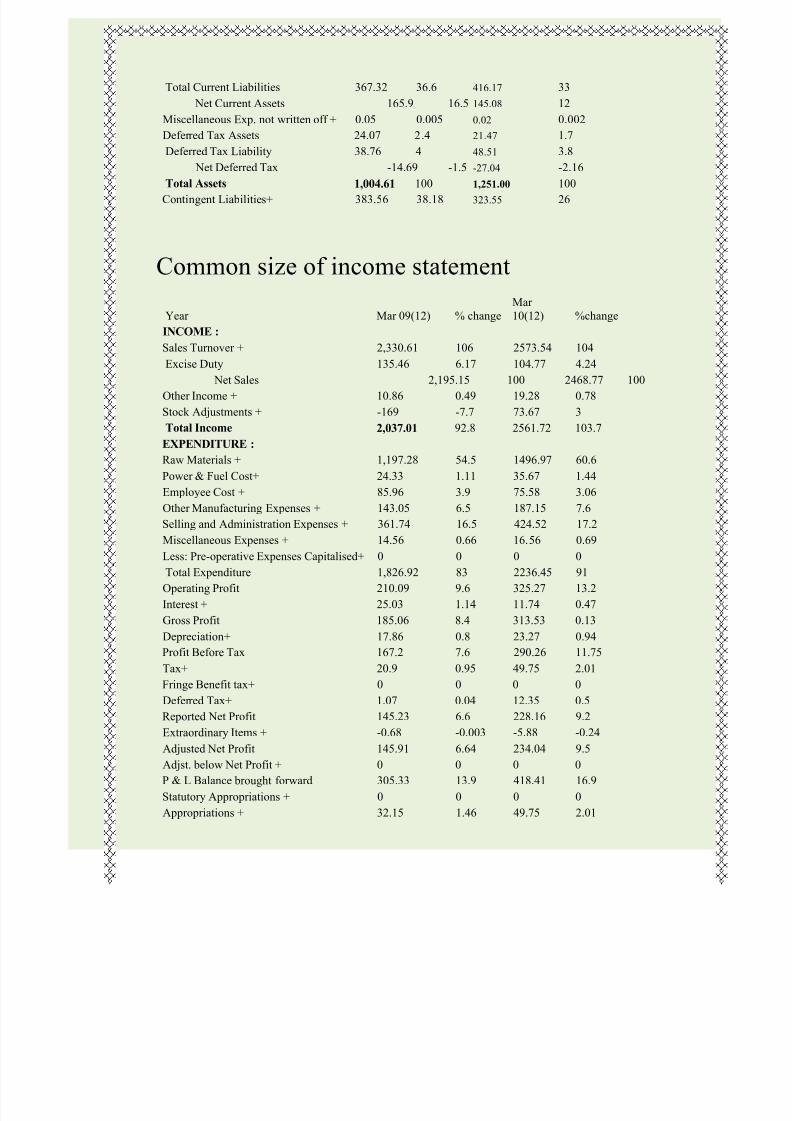

Common size of income statement

Year Mar 09(12) % change

Mar

10(12) %change

INCOME :

Sales Turnover + 2,330.61 106 2573.54 104Excise Duty 135.46 6.17 104.77 4.24

Net Sales 2,195.15 100 2468.77 100

Other Income + 10.86 0.49 19.28 0.78

Stock Adjustments + -169 -7.7 73.67 3

Total Income 2,037.01 92.8 2561.72 103.7

EXPENDITURE :

Raw Materials + 1,197.28 54.5 1496.97 60.6

Power & Fuel Cost+ 24.33 1.11 35.67 1.44

Employee Cost + 85.96 3.9 75.58 3.06

Other Manufacturing Expenses + 143.05 6.5 187.15 7.6

Selling and Administration Expenses + 361.74 16.5 424.52 17.2

Miscellaneous Expenses + 14.56 0.66 16.56 0.69

Less: Pre-operative Expenses Capitalised+ 0 0 0 0

Total Expenditure 1,826.92 83 2236.45 91

Operating Profit 210.09 9.6 325.27 13.2

Interest + 25.03 1.14 11.74 0.47

Gross Profit 185.06 8.4 313.53 0.13

Depreciation+ 17.86 0.8 23.27 0.94

Profit Before Tax 167.2 7.6 290.26 11.75

Tax+ 20.9 0.95 49.75 2.01

Fringe Benefit tax+ 0 0 0 0

Deferred Tax+ 1.07 0.04 12.35 0.5

Reported Net Profit 145.23 6.6 228.16 9.2

Extraordinary Items + -0.68 -0.003 -5.88 -0.24

Adjusted Net Profit 145.91 6.64 234.04 9.5

Adjst. below Net Profit + 0 0 0 0

P & L Balance brought forward 305.33 13.9 418.41 16.9

Statutory Appropriations + 0 0 0 0

Appropriations + 32.15 1.46 49.75 2.01

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 19/39

P & L Balance carried down 418.41 19 596.82 24.2

Dividend 15.04 0.68 23.12 0.94

Preference Dividend 0 0 0 0

Equity Dividend % 50 2.3 75 3.04

Earnings Per Share-Unit Curr 23.72 1.08 37.27 1.5

Earnings Per Share(Adj)-Unit Curr Book Value-Unit Curr 154.91 7 188.51 7.6

Trend analysis of Balance sheet

Year 2009 % change 2010 %change

SOURCES OF FUNDS :

Share capital+

30.08 100 31.19 103.7

Reserves total+ 901.83 100 1,104.00 122

Equity Share Warrants 2.42 100 0 0

Equity Application Money 0 100 0 0

Total Shareholders¶ Funds 934.33 100 1,135.19 121.5

Secured Loans + 24.36 100 115.81 475

Unsecured Loans + 45.92 100 0

Total Debt 70.28 100 115.81 165

Total Liabilities 1,004.61 100 1,251.00 124

APPLICATION OF FUNDS :

Gross Block + 507.62 100 643.95 127

Less : Accumulated Depreciation + 57.93 100 72.41 125

Less: Impairment of Assets 0 100 0 0

Net Block + 449.69 100571.54 127

Lease Adjustment 0 100 0 0

Capital Work in Progress+ 15.79 100 29.69 188

Investments + 387.87 100 531.71 137

Current Assets, Loans & Advances

Inventories + 207.53 100 330.65 159

Sundry Debtors + 86.74 100 79.47 92

Cash and Bank+ 157.37 100 68.31 43.4

Loans and Advances + 81.58 100 82.82 102

Total Current Assets 533.22 100 561.25 105

Less : Current Liabilities and ProvisionsCurrent Liabilities + 347.37 100 396.03 114

Provisions + 19.95 100 20.14 101

Total Current Liabilities 367.32 100 416.17 113

Net Current Assets 165.9 100 145.08 87.5

Miscellaneous Exp. not written off + 0.05 100 0.02 40

Deferred Tax Assets 24.07 100 21.47 89.2

Deferred Tax Liability 38.76 100 48.51 125

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 20/39

Net Deferred Tax -14.69 100 -27.04 184

Total Assets 1,004.61 100 1,251.00 124

Trend analysis of income statement

Year 2009 % 2010 %

INCOME:

Sales Turnover +

2330.61 100 2573.54 110.4

Excise Duty 135.46 100 104.77 77.3

Net Sales 2195.15 100 2468.77 112.5

Other Income + 10.86 100 19.28 177.5

Stock Adjustments + -169 100 73.67 -9533

Total Income 2037.01 100 2561.72 125.8

EXPENDITURE 1197.28 100 1496.97 125

Power & Fuel Cost+ 24.33 100 35.67 147

Employee Cost + 85.96 100 75.58 88Other Manufacturing Expenses + 143.05 100 187.15 131

Selling and Administration Expenses + 361.74 100 424.52 117

Miscellaneous Expenses + 14.56 100 16.56 114Less: Pre-operative Expenses

Capitalised+ 0 100 0 0

Expenditure Total 1826.92 100 2236.45 122

Operating Profit 210.09 100 325.27 155

Interest + 25.03 100 11.74 47

Gross Profit 185.06 100 313.53 169

Depreciation+ 17.86 100 23.27 130

Profit Before Tax 167.2 100 290.26 174

Tax+ 20.9 100 49.75 238

Fringe Benefit tax+ 0 100 0 0

Deferred Tax+

1.07 100 12.35 1154

Reported Net Profit 145.23 100 228.16 157

Extraordinary Items + -0.68 100 -5.88 -656

Adjusted Net Profit 145.91 100 234.04 160

Adjst. below Net Profit +

0 100 0 0

P & L Balance brought forward 305.33 100 418.41 137

Statutory Appropriations + 0 100 0 0

Appropriations + 32.15 100 49.75 155P & L Balance carried down 418.41 100 596.82 143

Dividend 15.04 100 23.12 154

Preference Dividend 0 100 0 0

Equity Dividend % 50 100 75 150

Earnings Per Share-Unit Curr 23.72 100 37.27 157

Earnings Per Share(Adj)-Unit Curr 100 0

Book Value-Unit Curr 154.91 100 188.51 122

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 21/39

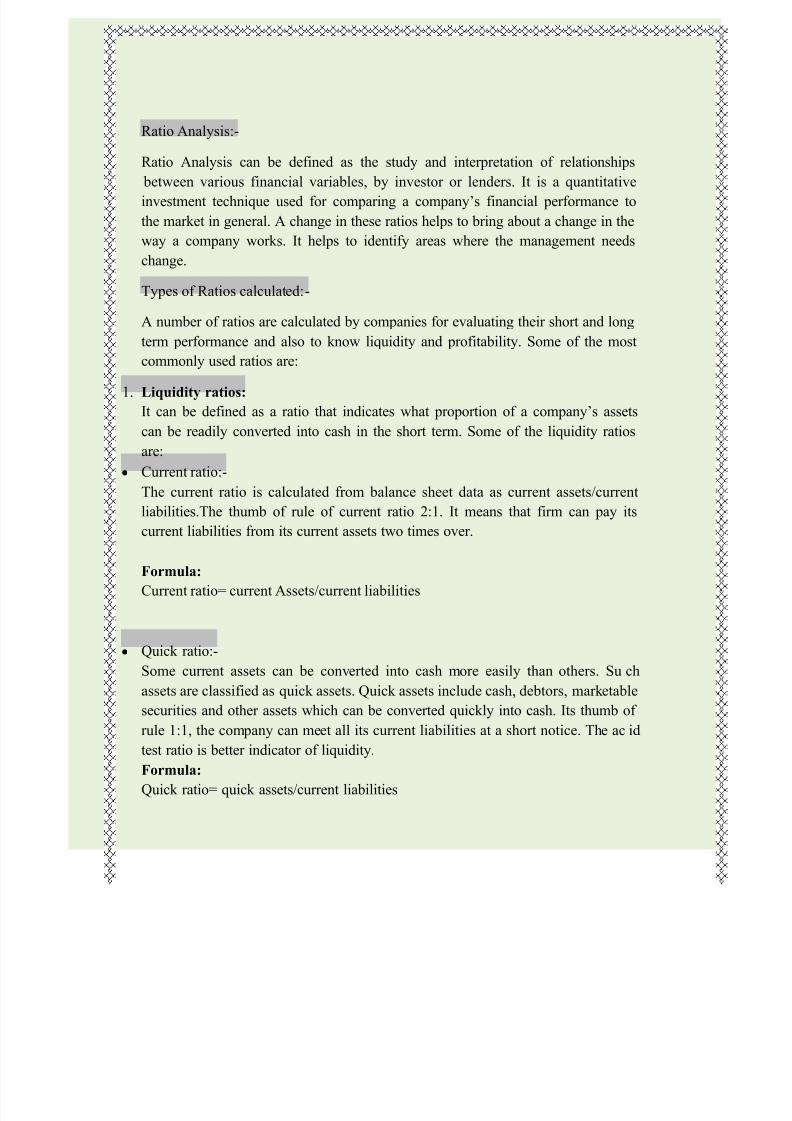

Ratio Analysis:-

Ratio Analysis can be defined as the study and interpretation of relationships

between various financial variables, by investor or lenders. It is a quantitative

investment technique used for comparing a company¶s financial performance to

the market in general. A change in these ratios helps to bring about a change in the

way a company works. It helps to identify areas where the management needs

change.

Types of Ratios calculated:-

A number of ratios are calculated by companies for evaluating their short and long

term performance and also to know liquidity and profitability. Some of the mostcommonly used ratios are:

1. Liquidity ratios:

It can be defined as a ratio that indicates what proportion of a company¶s assets

can be readily converted into cash in the short term. Some of the liquidity ratios

are:

y Current ratio:-

The current ratio is calculated from balance sheet data as current assets/current

liabilities.The thumb of rule of current ratio 2:1. It means that firm can pay its

current liabilities from its current assets two times over.

Formula:

Current ratio= current Assets/current liabilities

y Quick ratio:-

Some current assets can be converted into cash more easily than others. Su ch

assets are classified as quick assets. Quick assets include cash, debtors, marketablesecurities and other assets which can be converted quickly into cash. Its thumb of

rule 1:1, the company can meet all its current liabilities at a short notice. The ac id

test ratio is better indicator of liquidity.

Formula:

Quick ratio= quick assets/current liabilities

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 22/39

y Absolute liquid ratio:-

Absolute liquidity is represented by cash and near cash items. It is a ratio of

absolute liquid assets to current liabilities. In the computation of this ratio only theabsolute liquid assets are compared with the liquid liabilities. The absolute liquid

assets are cash, bank and marketable securities. It is to be observed that

receivables (debtors/accounts receivables and bills receivables) are eliminated

from the list of liquid assets in order to obtain absolute4 liquid assets since there

may be some doubt in their liquidity.

Formula:

Absolute liquid ratio=Absolute liquid assets/current

Liabilities

2. Profitability ratios:

It can be defined as a ratio that explains the profitability of a company during a

specific period of time. It explains how profitable a company is. These ratios can

be compared during different financial years to see the overall performance of a

company. Some of the profitability ratios are:

y Gross Profit ratio:-

The basic components for the calculation of gross profit ratio are gross profit and

net sales. Net sales mean that sale minus sales returns. Gross profit would be the

difference between net sales and cost of goods sold. Cost of goods sold in the case

of a trading concern would be equal to opening stock plus purchases , minus

closing stock plus all direct expenses relating to purchases. In the case of

manufacturing concern, it would be equal to the sum of the cost of raw materials,

wages, direct expenses and all manufacturing expenses. In other words, generally

the expenses charged to profit and loss account or operating expenses are excluded

from the calculation of cost of goods sold.

Formula:

Gross profit ratio=gross profit/Net sales*100

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 23/39

y Net profit ratio:-

This ratio is used by investors, creditors, and lenders to judge the profit earnings

capacity of the organisation. It indicates the overall profitability of the

organisation after meeting all expenses, charges, depreciation, etc.

Formula:

Net profit ratio= Net profit /Net sales*100

y Operating ratio:

Operating ratio indicates the relationship between operating expenses and sales.

This ratio indicates operating efficiency of the organisation and is important to the

management in evaluating its own efficiency.

Formula:

Operating ratio=Operating costs/Net sales*100

y Return on Investment(ROI):-

This ratio measure the percentage returns to the company on the funds it had

employed and is a good indication of the profitability of the organisation. It is also

a useful overall measure of the ability of the management.

Formula:

Return on investment= net profit/shareholder¶sFunds*100

y Return on Equity(ROE):-

Return on equity is the single measure that summarises the financial health of a

company. Number of pennies earned during the year on each dollar. As a very

rough rule of thumb, return on equity consistently above 15% is a sign of good

health of the company; ROE consistently below 15% is sign of trouble.

Formula:

Return on equity= (Net profit-preference dividend)/equityShareholders*100

y Earnings Per Share:-

Earnings per share (EPS) are such a fundamental number that we usually forget

that is a financial ratio. The necessary adjustments for dilutive securities. It net

income attribute to each share of common stock.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 24/39

Formula:

Earnings per share= (Net profit-preference dividend)

/no. of equity share outstanding

3. Some other ratios are:

y Inventory turnover ratio:-

Stock turnover ratio and inventory turnover ratio are the same. This ratio is a

relationship between the cost of goods sold during a particular period of time andthe cost of average inventory during a particular period. It is expressed in number

of times. Stock turnover ratio / Inventory turnover ratio indicates the number of time the stock has been turned over during the period and evaluates the efficiencywith which a firm is able to manage its inventory. This ratio indicates whether

investment in stock is within proper limit or not.

Formula:

Inventory turnover ratio=COGS/Average stock

Inventory conversion ratio=365/ITR

y Debtor¶s turnover ratio:-

Debtor¶s turnover ratio or accounts receivable turnover ratio indicates the

velocity of debt collection of a firm. In simple words it indicates the number of times average debtors (receivable) are turned over during a year.

Formula:

Debtor¶s turnover ratio=Net credit sales/Average debtors

Debtor¶s collection period=365/DTR

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 25/39

y Creditors turnover ratio:

This ratio is similar to the debtor turnover ratio. It compares creditors with thetotal credit purchases.

Formula:

Creditors turnover ratio=Net credit purchase/Average creditor

Average payment period=365/CTR

y Solvency ratio:

Debt-to-Equity ratio indicates the relationship between the external equities or

outsiders funds and the internal equities or shareholders funds.

Formula:Debt to equity ratio= total debt /equity

y interest coverage ratio:

Interest coverage ratio is also known as debt service ratio or debt service

coverage ratio.

Formula:

Interest coverage ratio=Earnings before interest tax/ interest

Charges

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 26/39

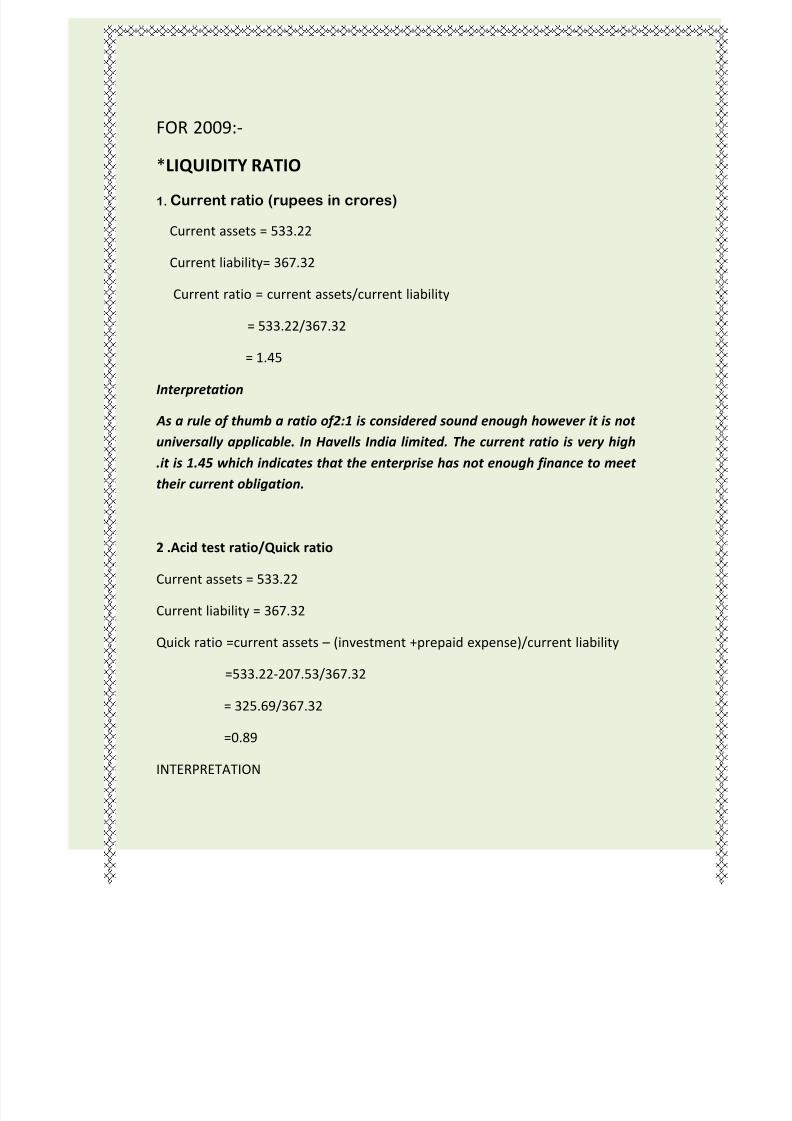

FOR 2009:-

*LIQUIDITY RATIO1. Current ratio (rupees in crores)

Current assets = 533.22

Current liability= 367.32

Current ratio = current assets/current liability

= 533.22/367.32

= 1.45

Interpretation

As a rule of thumb a ratio of2:1 is considered sound enough however it is not

universally applicable. In Havells India limited. The current ratio is very high

.it is 1.45 which indicates that the enterprise has not enough finance to meet

their current obligation.

2 .Acid test ratio/Quick ratio

Current assets = 533.22

Current liability = 367.32

Quick ratio =current assets (investment +prepaid expense)/current liability

=533.22-207.53/367.32

= 325.69/367.32

=0.89

INTERPRETATION

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 27/39

Current ratio and test ratio indicate the ability of the enterprise to meet its

current liability however the acid test ratio is better indicator of liquidity. Acid

test ratio of Havells India limited is 0.89.the acid test ratio of company is not

too much .it means company has not too much financial resources .so

Company cannot easily meet their current liability.

3. Absolute liquid ratio

Absolute liquid assets =cash in hand + cash in bank +marketable securities

Cash and bank =157.37

Current liability=367.32

Absolute liquid ratio =absolute liquid assets/current liability

=157.37/533.22

=0.29

INTERPRETATION

Absolute liquidity is represented by cash and near cash item .the absolute

liquid ratio are cash, bank and marketable securities .A standard of 0.5:1

absolute liquidty is considered. The ratio of absolute liquid ratio is 0.29 which

show that company has too much liquidty assets which is good for the

company .it show a good financial position in the market.

*profitability ratio

1. Gross profit ratio

Gross profit =185.06

Net sales = 2195.15

Gross profit ratio =gross profit/net sales*100

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 28/39

=185.06/2195.15*100

=8.43%

INTERPRETATION

Gross profit ratio indicates what extent the selling price of goods perunit may be reduced without incurring losses on operation. It reflects

the efficiency with which a firm produced its product. The ratio of

company is 8.43 which show that company production is good according

to their ratio.

2. Net profit ratio

Net profit= 145.23

Net sales =2195.15

Net profit ratio=net profit/net sales*100

=145.23/2195.15*100

=6.6%

INTERPRETATION

Actually the business totally depends on the profit of the company.

Business is only run success if it earns profit. So net profit ratio of this

company is 6.6% which show that company is not earns a huge net

profit.

3. Operating ratio

Operating cost =COGS + operating expenses

=2010.09+361.74+14.56=2386.39

Net sales = 2195.15

Operating ratio=operating cost /net sales*100

=2386.39/2195.15*100

=108.7%

INTERPRETATION

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 29/39

Operating ratio indicate the relationship between operating e xpenses

and sales. The ratio indicates operating efficiency of the organisation

and it is important to the management to evaluating its own efficiency.

The ratio of reliance power is 108.7%which indicate the

efficiency of the organisation is good but not better management shouldtake more steps towards their utilisation of their resources.

4. Return on investment

Net profit =145.23

Shareholder fund=934.33

Return on investment=net profit/shareholder fund*100

=145.23/934.33*100

=15.54%

INTERPRETATION

Through this ratio company can measure the percentage return to the

company on the fund .it is also a good indication of the profitability of

the organisation.

The company has ratio of RETURN OF INVESTMENT is 15.54% this

percentage sufficient for the company because profit is a function of

accounting and operating policies of an enterprise.

5. Return on equity

Net profit=145.23

Preference share dividend=0

Share holder fund=934.33

Return on equity =Net profit-Preference dividend/Shareholder fund*100

=145.23-0/934.33*100

=15.54%

INTERPRETATION

Return on equity measure a corporation ,s profitability by revealing how much

profit a company generate with the money shareholder have invested. The

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 30/39

ratio of ROE is15.54% indicating good performance in generating profit from

that amount which is invested by the shareholder.

6. Earnings per share =Net profit-preference dividend/No. Of equity

share outstanding

*Activity /turnover ratio

1. Inventory turnover ratio

COG

S=net sales-gross profit

=2195.15-185.06

=2010.09

Average stock= 207.53

Inventory turnover ratio=COGS/average stock

= 2010.09/ 207.53 =10

INTERPRETATION

Inventory turnover ratio indicate that how many times a company, s inventory

is sold and replaced over a period. A high ratio implies either strong sales or

effective buying. But company ITR is 10 which show that company has good

turnover implies good sales.

2. Debtors turnover ratio=net credit annual sales/average

debtors

Net credit sales= 2195.15

Average debtor= 86.74

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 31/39

Debtor turnover ratio=2195.15/86.74

=25.31

3. Creditors turnover ratio =net credit purchase/average creditor

Average payment period=365/CTR

NOTE there is no any credit purchase by the company so we could not find.

*solvency ratio

1. Debt to equity ratio

Debt=70.28

Equity= 30.08

Debt to equity ratio= total debt/equity

=70.28/30.08

=2.3

INTERPRETATION

Through this ratio company find out financial power of the

company. A high debt to equity ratio generally means that a company has been

aggressive in financial its growth with debt. If company debt may increase

more than it may lead to bankruptcy.

Company debt to equity ratio is not much which indicates that company

took debt according to their need.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 32/39

*coverage ratio

1. Inertest coverage ratio

EBIT=167.20

Interest charges= 25.03

Interest coverage ratio=earnings before interest tax/interest charges

=167.20/25.03

=6.7

INTERPRETATION

Interest coverage ratio determines that how easily a company can pay interest

on outstanding debt. The lower the ratio, the company is burden by debt

expense. But the Havells India limited has interest coverage ratio is 6.7. Which

show that company has not much debt or if company has any debt it can easily

met by the company.

CALCULATION FOR 2010

*LIQUIDITY RATIO

1. Current ratio (rupees in crores)

Current assets = 561.25

Current liability= 416.17

Current ratio = current assets/current liability

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 33/39

= 561.25 / 416.17

= 1.35

Interpretation

Generally as a rule of thumb a ratio of2:1 is considered sound enough

however it is not universally applicable. In Havells India limited. The current

ratio is very low .it is 1.35 which indicates that the enterprise has not more

finance than it need .the ratio show that company has not much finance.

Thus, a high current ratio means the enterprise has more finance so they can

use efficiently. But company has low current ratio.

2 .Acid test ratio/Quick ratio

Current assets = 561.25

Current liability = 416.17

Quick ratio =current assets (investment +prepaid expense)/current liability

=561.25-330.65/416.17

= 231/416.17

= 0.56

INTERPRETATION

Current ratio and test ratio indicate the ability of the enterprise to meet its

current liability however the acid test ratio is better indicator of liquidity. Acid

test ratio of havells India limited is 0.56.the acid test ratio of company is not

too much. It means company has not too much finance available.

2. Absolute liquid ratio

Cash and bank = 68.31

Current liability= 416.17

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 34/39

Absolute liquid assets =cash in hand + cash in bank +marketable securities

=68.31

Absolute liquid ratio =absolute liquid assets/current liability

= 68.31 / 416.17

= 0.16

INTERPRETATION

Absolute liquidity is presented by cash and near cash item .the absolute liquid

ratio are cash, bank and marketable securities .A standard of 0.5:1 absolute

liquidity is considered. The ratio of absolute liquid ratio is 0.16. Which show

that company has not good liquid assets.

*profitability ratio

3. Gross profit ratio

Gross profit = 313.53

Net sales = 2468.77

Gross profit ratio =gross profit/net sales*100

= 313.53 / 2468.77 * 100

= 12.7%

INTERPRETATION

Gross profit ratio indicate what extent the selling price of goods per unit

may be reduced without incurring losses on operation .it reflect the

efficiency with which a firm produced its product. The ratio of company

is 12.7%. Which show that company production is good according to

their ratio.

4. Net profit ratio

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 35/39

Net profit= 228.16

Net sales =2468.77

Net profit ratio=net profit/net sales*100

= 228.16 / 2468.77 * 100= 9.24%

INTERPRETATION

Actually the business totally depend on the profit of the company .Business is

only run success if it earn profit. So net profit ratio of this company is 9.24%

which show that company earn a normal net profit .it is good for the company.

3. Operating ratio

Operating cost =COGS+ operating expenses

=2155.24+424.52+16.56

= 2596.32

Net sales = 2468.77

Operating ratio=operating cost /net sales*100

= 2596.32 / 2468.77 *100

= 105%

INTERPRETATION

Operating ratio indicate the relationship between operating expenses

and sales. The ratios indicate operating efficiency of the organisation

and it is important to the management to evaluating its own efficiency.

The ratio of havells India limited is 105%which indicate

the efficiency of the organisation is good but not better management

should take more steps towards their utilisation of their resources.

4. Return on investment

Net profit =228.16

Shareholder fund= 1135.19

Return on investment=net profit/shareholder fund*100

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 36/39

= 228.16 / 1135.19 *100

= 20 %

INTERPRETATION

Through this ratio company can measure the percentage return to thecompany on the fund .it is also a good indication of the profitability of

the organisation.

The company has ratio of RETURN OF INVESTMENT is 20% this

percentage sufficient for the company because profit is a function of

accounting and operating policies of an enterpr ise.

5. Return on equity

Net profit=228.16

Preference share dividend=0

Share holder fund= 1135.19

Return on equity =Net profit-Preference dividend/Shareholder fund*100

= 228.16 -0 / 1135.19 *100

= 20 %

INTERPRETATION

Return on equity measure a corporation ,s profitability by prevailing

how much profit a company generate with the money shareholder have

invested. The ratio of ROE is indicating good performance in generating

profit from that amount which is invested by the shareholder.

6. Earnings per share =Net profit-preference dividend/No. Of equity

share outstanding

*Activity /turnover ratio

1. Inventory turnover ratio

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 37/39

COGS=net sales-gross profit

= 2468.77 313.53

= 2155.24

Average stock= 330.65

Inventory turnover ratio=COGS / average stock

= 2155.24 / 330.65 = 6.5

INTERPRETATION

Inventory turnover ratio indicate that how many times a company, s inventory

is sold and replaced over a period. A high ratio implies either strong sales or

effective buying. But company ITR is 6.5 which show that company has high

turnover implies good sales.

3. Debtors turnover ratio=net credit annual sales/average

debtors

Net credit sales= 2468.77

Average debtor= 79.47

Debtor turnover ratio=2468.77 / 79.47

= 31

3. Creditors turnover ratio =net credit purchase/average creditor

Average payment period=365/CTR

NOTE there is no any credit purchase by the company so we could not find.

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 38/39

*solvency ratio

1. Debt to equity ratio

Debt= 115.81

Equity= 31.19

Debt to equity ratio= total debt/equity

= 115.81 / 31.19

= 3.7

INTERPRETATION

Through this ratio company find out financial power of the company. A high

debt to equity ratio generally means that a company has been aggressive in

financial its growth with debt. If company debt may increase more than it may

lead to bankruptcy.

Company debt to equity ratio is not much which indicates that company

took debt according to their need.

*coverage ratio

3. Inertest coverage ratio

EBIT= 290.26

Interest charges= 11.74

Interest coverage ratio=earnings before interest tax/interest charges=290.26 / 11.74

= 24.7

INTERPRETATION

8/7/2019 Manu Mam Term Paper

http://slidepdf.com/reader/full/manu-mam-term-paper 39/39

Interest coverage ratio determine that how easily a company can pay interest

on outstanding debt .the lower the ratio ,the company is burden by debt

expense. But the reliance power company has interest coverage ratio is 24.7

which show that company has no any debt or if company has any debt it can

easily meet by the company.