49 Caro Checklist

31

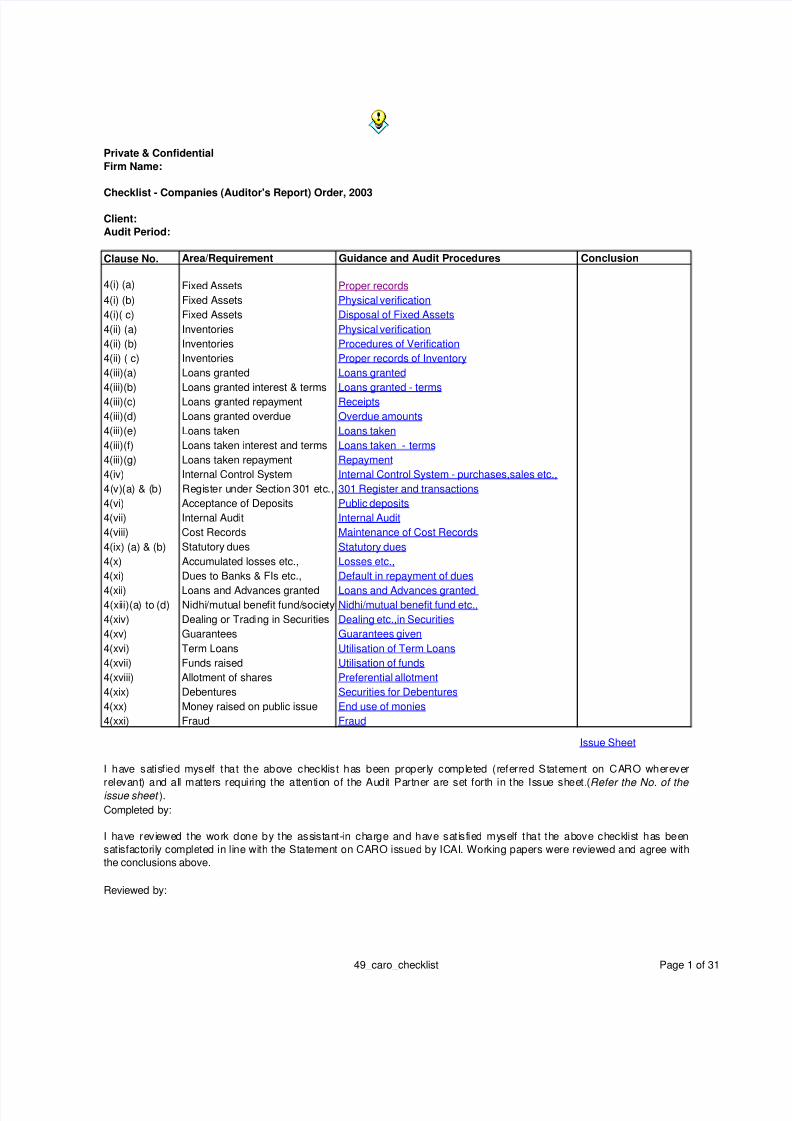

Private & Confidential Firm Name: Checklist - Companies (Auditor's Report) Order, 2003 Client: Audit Period: Clause No. Area/Requirement Guidance and Audit Procedures Conclusion 4(i) (a) Fixed Assets Proper records 4(i) (b) Fixed Assets Physical verification 4(i)( c) Fixed Assets Disposal of Fixed Assets 4(ii) (a) Inventories Physical verification 4(ii) (b) Inventories Procedures of Verification 4(ii) ( c) Inventories Proper records of Inventory 4(iii)(a) Loans granted Loans granted 4(iii)(b) Loans granted interest & terms Loans granted - terms 4(iii)(c) Loans granted repayment Receipts 4(iii)(d) Loans granted overdue Overdue amounts 4(iii)(e) Loans taken Loans taken 4(iii)(f) Loans taken interest and terms Loans taken - terms 4(iii)(g) Loans taken repayment Repayment 4(iv) Internal Control System Internal Control System - purchases,sales etc., 4( v) (a) & ( b) Regi st er u nder Section 301 etc., 301 Register and transactions 4(vi) Acceptance of Deposits Public deposits 4(vii) Internal Audit Internal Audit 4(viii) Cost Records Maintenance of Cost Records 4(ix) (a) & (b) Statutory dues Statutory dues 4(x) Accumulated losses etc., Losses etc., 4(xi) Dues to Banks & FIs etc., Default in repayment of dues 4(xii) Loans and Advances granted Loans and Advances granted 4(xi ii)(a ) to (d) Nidhi /mutu al bene fit fund/ socie ty Nidhi/mutual benefit fund etc., 4(xiv) Dealing or Trading in Securities Dealing etc.,in Securities 4(xv) Guarantees Guarantees given 4(xvi) Term Loans Utilisation of Term Loans 4(xvii) Funds raised Utilisation of funds 4(xviii) Allotment of shares Preferential allotment 4(xix) Debentures Securities for Debentures 4(xx) Money raised on public issue End use of monies 4(xxi) Fraud Fraud Issue Sheet Completed by: Reviewed by: I have sa tis fi ed myself th at the abo ve checklist has been pro pe rl y co mplet ed (r eferred St atement on CARO wherever relevant) and all matters requirin g th e at tention of the Au di t Partner are set forth in th e Is su e sh ee t. (Refer the No. of the issue sheet ). I hav e re vi ewe d th e wor k do ne by th e ass ist an t- in ch ar ge and ha ve sa ti sf ie d my se lf th at th e ab ove ch eck lis t ha s bee n sati sfa ctor il y completed in li ne wi th the St at ement on CARO is sued by ICAI . Wor ki ng papers were revi ewed and agree wi th the conclusions above. 49 caro checklist Page 1 of 31

-

Upload

papadthedon -

Category

Documents

-

view

221 -

download

0

Transcript of 49 Caro Checklist

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 1/31

Private & Confidential

Firm Name:

Checklist - Companies (Auditor's Report) Order, 2003

Client:

Audit Period:

Clause No. Area/Requirement Guidance and Audit Procedures Conclusion

4(i) (a) Fixed Assets Proper records

4(i) (b) Fixed Assets Physical verification

4(i)( c) Fixed Assets Disposal of Fixed Assets

4(ii) (a) Inventories Physical verification

4(ii) (b) Inventories Procedures of Verification

4(ii) ( c) Inventories Proper records of Inventory

4(iii)(a) Loans granted Loans granted

4(iii)(b) Loans granted interest & terms Loans granted - terms

4(iii)(c) Loans granted repayment Receipts

4(iii)(d) Loans granted overdue Overdue amounts

4(iii)(e) Loans taken Loans taken

4(iii)(f) Loans taken interest and terms Loans taken - terms

4(iii)(g) Loans taken repayment Repayment

4(iv) Internal Control System Internal Control System - purchases,sales etc.,

4(v)(a) & (b) Register under Section 301 etc., 301 Register and transactions

4(vi) Acceptance of Deposits Public deposits

4(vii) Internal Audit Internal Audit

4(viii) Cost Records Maintenance of Cost Records

4(ix) (a) & (b) Statutory dues Statutory dues

4(x) Accumulated losses etc., Losses etc.,

4(xi) Dues to Banks & FIs etc., Default in repayment of dues

4(xii) Loans and Advances granted Loans and Advances granted4(xiii)(a) to (d) Nidhi/mutual benefit fund/society Nidhi/mutual benefit fund etc.,

4(xiv) Dealing or Trading in Securities Dealing etc.,in Securities

4(xv) Guarantees Guarantees given

4(xvi) Term Loans Utilisation of Term Loans

4(xvii) Funds raised Utilisation of funds

4(xviii) Allotment of shares Preferential allotment

4(xix) Debentures Securities for Debentures

4(xx) Money raised on public issue End use of monies

4(xxi) Fraud Fraud

Issue Sheet

Completed by:

Reviewed by:

I have satisfied myself that the above checklist has been properly completed (referred Statement on CARO wherever

relevant) and all matters requiring the attention of the Audit Partner are set forth in the Issue sheet.(Refer the No. of the

issue sheet ).

I have reviewed the work done by the assistant-in charge and have satisfied myself that the above checklist has been

satisfactorily completed in line with the Statement on CARO issued by ICAI. Working papers were reviewed and agree with

the conclusions above.

49_caro_checklist Page 1 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 2/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

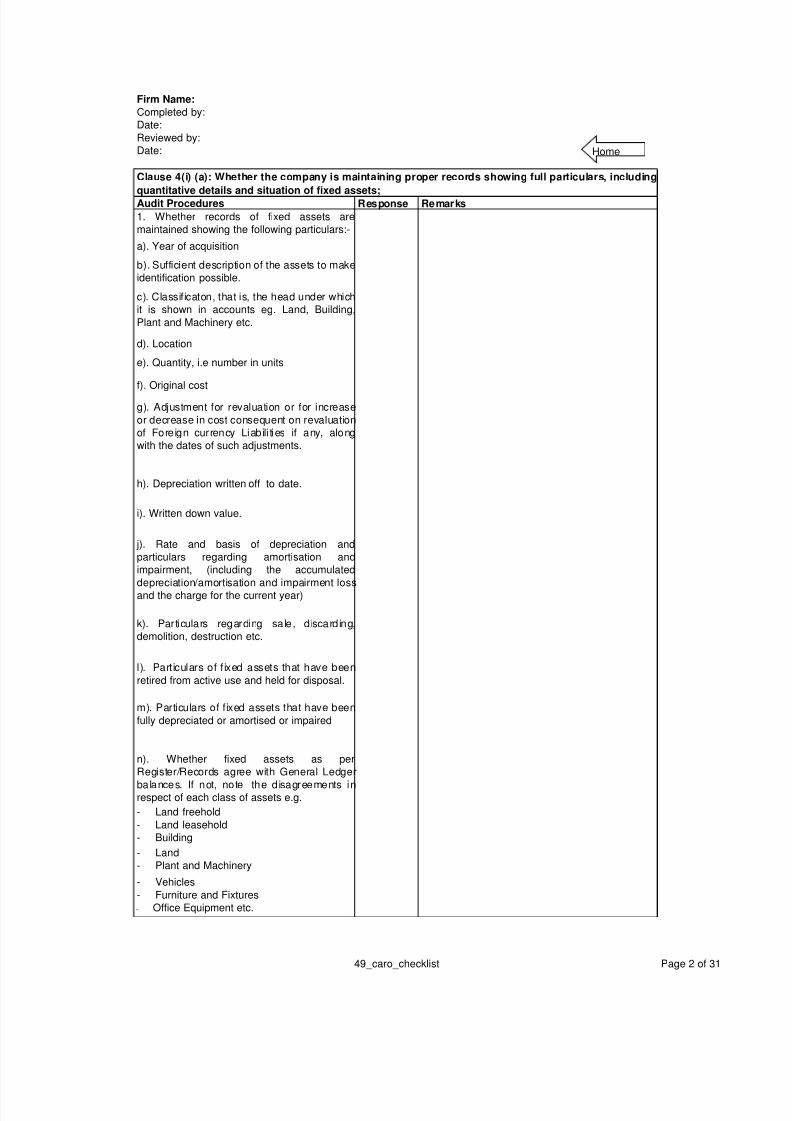

Audit Procedures Response Remarks

1. Whether records of fixed assets are

maintained showing the following particulars:-

a). Year of acquisition

b). Sufficient description of the assets to make

identification possible.

c). Classificaton, that is, the head under which

it is shown in accounts eg. Land, Building,

Plant and Machinery etc.

d). Location

e). Quantity, i.e number in units

f). Original cost

g). Adjustment for revaluation or for increase

or decrease in cost consequent on revaluation

of Foreign currency Liabili ties if any, along

with the dates of such adjustments.

h). Depreciation written off to date.

i). Written down value.

j). Rate and basis of depreciation and

particulars regarding amortisation and

impairment, (including the accumulated

depreciation/amortisation and impairment loss

and the charge for the current year)

k). Particulars regarding sale, discarding,

demolition, destruction etc.

l). Part iculars of f ixed assets that have been

retired from active use and held for disposal.

m). Particulars of fixed assets that have been

fully depreciated or amortised or impaired

n). Whether fixed assets as per

Register/Records agree with General Ledger

balances. If not, note the disagreements inrespect of each class of assets e.g.

- Land freehold

- Land leasehold

- Building

- Land

- Plant and Machinery

- Vehicles

- Furniture and Fixtures

- Office Equipment etc.

Clause 4(i) (a): Whether the company is maintaining proper records showing full particulars, including

quantitative details and situation of fixed assets;

Home

49_caro_checklist Page 2 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 3/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

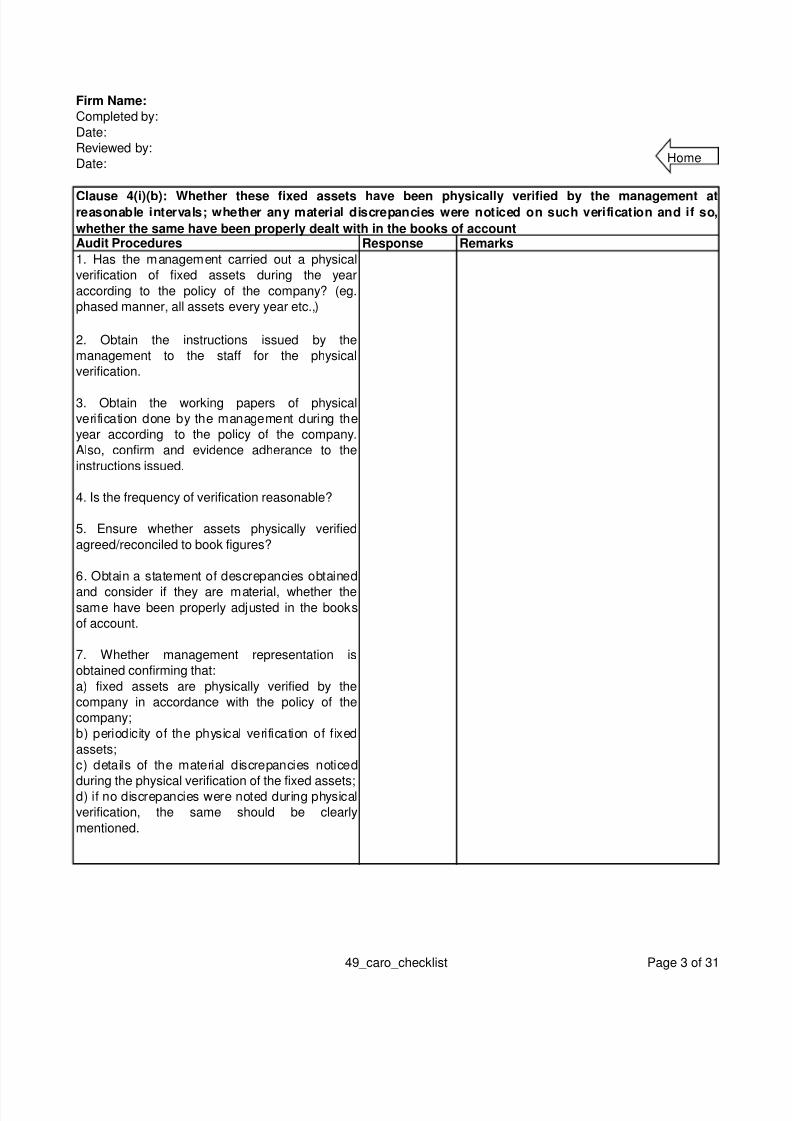

Audit Procedures Response Remarks

1. Has the management carried out a physical

verification of fixed assets during the year

according to the policy of the company? (eg.

phased manner, all assets every year etc.,)

2. Obtain the instructions issued by the

management to the staff for the physical

verification.

3. Obtain the working papers of physical

verification done by the management during the

year according to the policy of the company.

Also, confirm and evidence adherance to the

instructions issued.

4. Is the frequency of verification reasonable?

5. Ensure whether assets physically verified

agreed/reconciled to book figures?

6. Obtain a statement of descrepancies obtained

and consider if they are material, whether thesame have been properly adjusted in the books

of account.

7. Whether management representation is

obtained confirming that:

a) fixed assets are physically verified by the

company in accordance with the policy of the

company;

b) periodicity of the physical verification of fixed

assets;

c) details of the material discrepancies noticed

during the physical verification of the fixed assets;d) if no discrepancies were noted during physical

verification, the same should be clearly

mentioned.

Clause 4(i)(b): Whether these fixed assets have been physically verified by the management atreasonable intervals; whether any material discrepancies were noticed on such verification and if so,

whether the same have been properly dealt with in the books of account

Home

49_caro_checklist Page 3 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 4/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

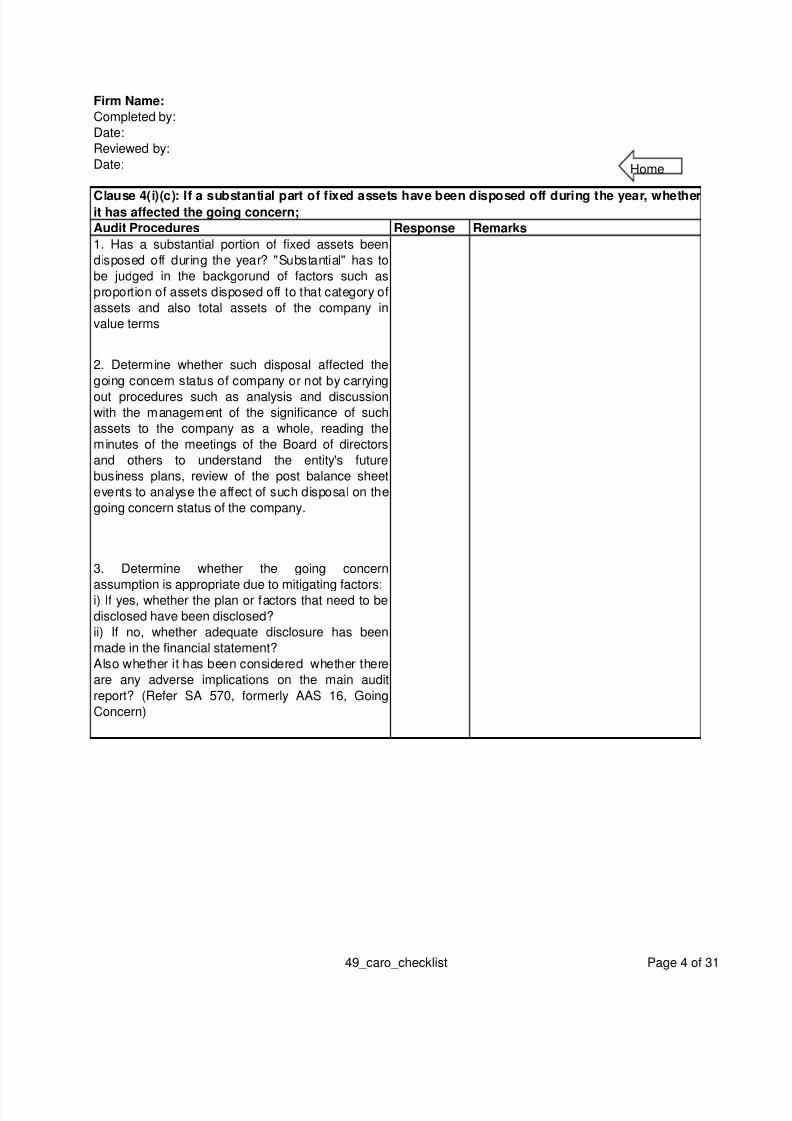

1. Has a substantial portion of fixed assets been

disposed off during the year? "Substantial" has to

be judged in the backgorund of factors such as

proportion of assets disposed off to that category of

assets and also total assets of the company in

value terms

2. Determine whether such disposal affected the

going concern status of company or not by carrying

out procedures such as analysis and discussionwith the management of the significance of such

assets to the company as a whole, reading the

minutes of the meetings of the Board of directors

and others to understand the entity's future

business plans, review of the post balance sheet

events to analyse the affect of such disposal on the

going concern status of the company.

3. Determine whether the going concern

assumption is appropriate due to mitigating factors:i) If yes, whether the plan or factors that need to be

disclosed have been disclosed?

ii) If no, whether adequate disclosure has been

made in the financial statement?

Also whether it has been considered whether there

are any adverse implications on the main audit

report? (Refer SA 570, formerly AAS 16, Going

Concern)

Clause 4(i)(c): If a substantial part of fixed assets have been disposed off during the year, whetherit has affected the going concern;

Home

49_caro_checklist Page 4 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 5/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

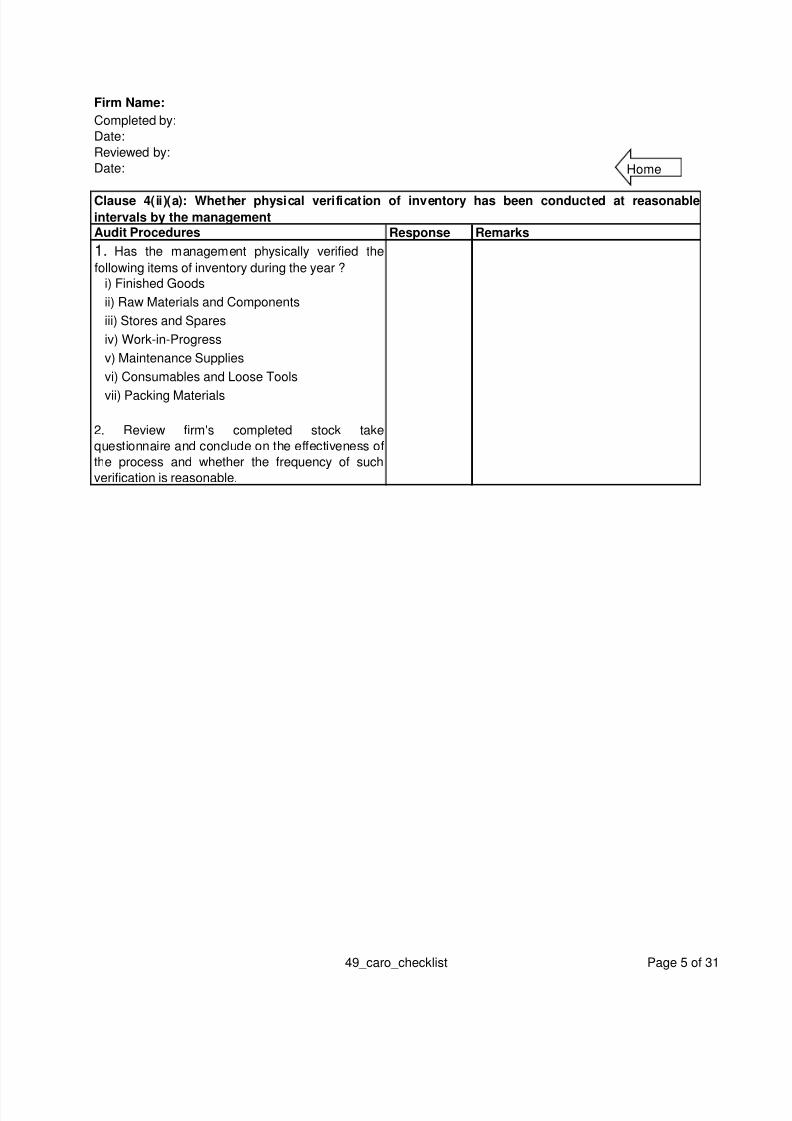

1. Has the management physically verified the

following items of inventory during the year ?

i) Finished Goods

ii) Raw Materials and Components

iii) Stores and Spares

iv) Work-in-Progress

v) Maintenance Supplies

vi) Consumables and Loose Tools

vii) Packing Materials

2. Review firm's completed stock take

questionnaire and conclude on the effectiveness of

the process and whether the frequency of such

verification is reasonable.

Clause 4(ii)(a): Whether physical verification of inventory has been conducted at reasonable

intervals by the management

Home

49_caro_checklist Page 5 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 6/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

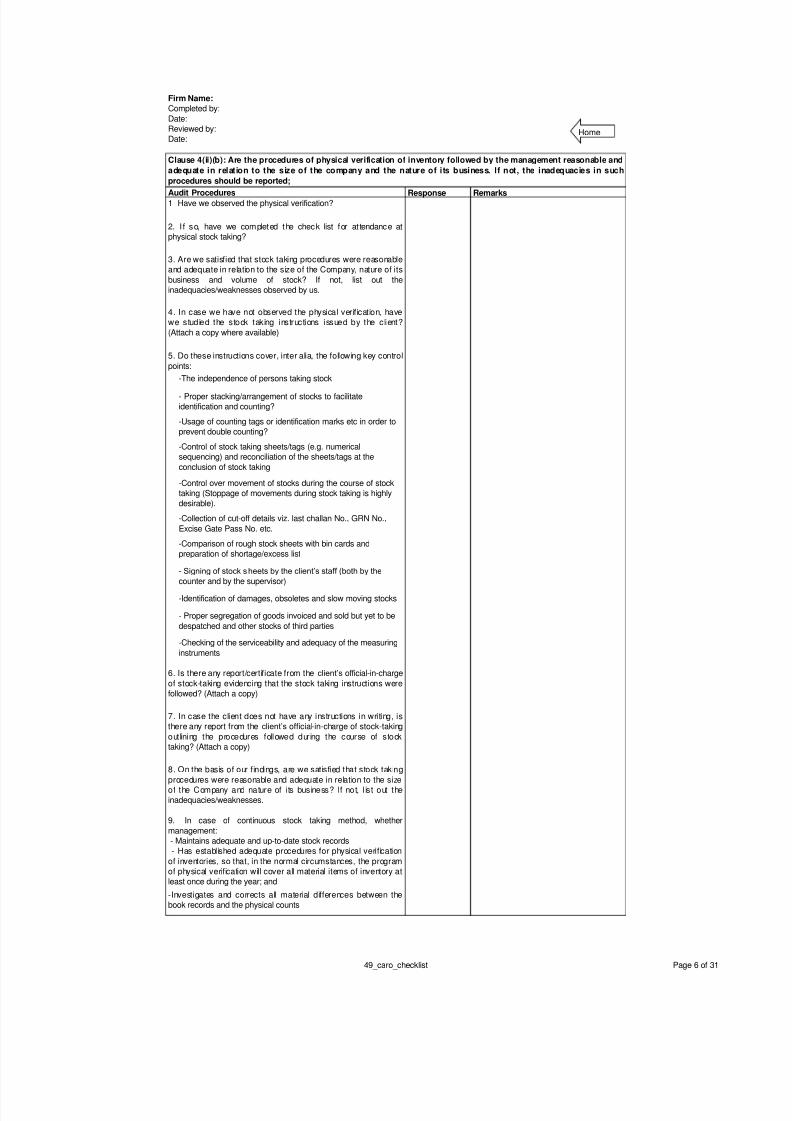

Audit Procedures Response Remarks1 Have we observed the physical verification?

2. I f so, have we completed the check list for at tendance at

physical stock taking?

3. Are we satisfied that stock taking procedures were reasonable

and adequate in relation to the size of the Company, nature of its

business and volume of stock? If not, list out the

inadequacies/weaknesses observed by us.

4. In case we have not observed the physical verification, have

we studied the stock taking instructions issued by the client?

(Attach a copy where available)

5. Do these instructions cover, inter alia, the following key control

points:

-The independence of persons taking stock

- Proper stacking/arrangement of stocks to facilitate

identification and counting?

-Usage of counting tags or identification marks etc in order to

prevent double counting?

-Control of stock taking sheets/tags (e.g. numerical

sequencing) and reconciliation of the sheets/tags at the

conclusion of stock taking

-Control over movement of stocks during the course of stock

taking (Stoppage of movements during stock taking is highly

desirable).

-Collection of cut-off details viz. last challan No., GRN No.,

Excise Gate Pass No. etc.

-Comparison of rough stock sheets with bin cards and

preparation of shortage/excess list

- Signing of stock sheets by the client’s staff (both by the

counter and by the supervisor)

-Identification of damages, obsoletes and slow moving stocks

- Proper segregation of goods invoiced and sold but yet to be

despatched and other stocks of third parties

-Checking of the serviceability and adequacy of the measuring

instruments

6. Is there any report/certificate from the client’s official-in-charge

of stock-taking evidencing that the stock taking instructions were

followed? (Attach a copy)

7. In case the client does not have any instructions in writing, is

there any report from the client’s official-in-charge of stock-taking

outlining the procedures followed during the course of stock

taking? (Attach a copy)

8. On the basis of our findings, are we satisfied that stock taking

procedures were reasonable and adequate in relation to the size

of the Company and nature of i ts business? If not, l ist out the

inadequacies/weaknesses.

9. In case of continuous stock taking method, whether

management:

- Maintains adequate and up-to-date stock records

- Has established adequate procedures for physical verification

of inventories, so that, in the normal circumstances, the program

of physical verification will cover all material items of inventory at

least once during the year; and

-Investigates and corrects all material differences between the

book records and the physical counts

Clause 4(ii)(b): Are the procedures of physical verification of inventory followed by the management reasonable and

adequate in relation to the size of the company and the nature of its business. If not, the inadequacies in such

procedures should be reported;

Home

49_caro_checklist Page 6 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 7/31

Firm Name:

Completed by:Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

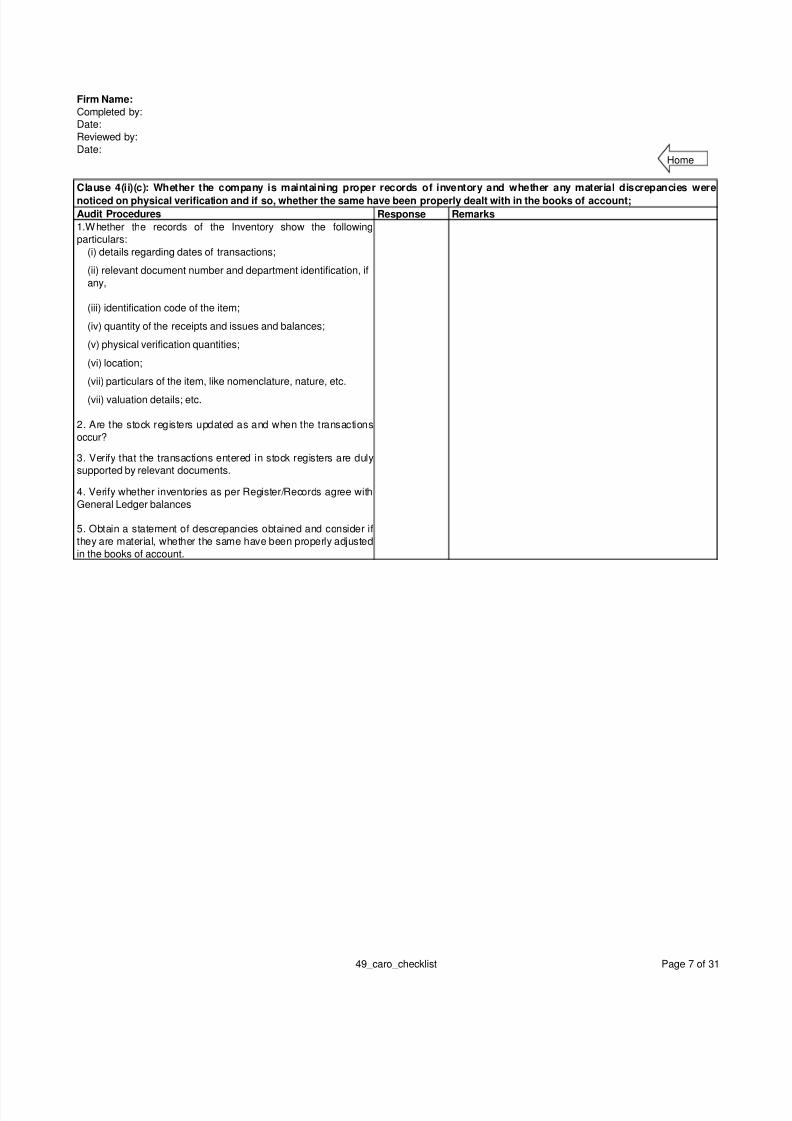

1.Whether the records of the Inventory show the followingparticulars:

(i) details regarding dates of transactions;

(ii) relevant document number and department identification, if

any,

(iii) identification code of the item;

(iv) quantity of the receipts and issues and balances;

(v) physical verification quantities;

(vi) location;

(vii) particulars of the item, like nomenclature, nature, etc.

(vii) valuation details; etc.

2. Are the stock registers updated as and when the transactions

occur?

3. Verify that the transactions entered in stock registers are dulysupported by relevant documents.

4. Verify whether inventories as per Register/Records agree with

General Ledger balances

5. Obtain a statement of descrepancies obtained and consider if

they are material, whether the same have been properly adjusted

in the books of account.

Clause 4(ii)(c): Whether the company is maintaining proper records of inventory and whether any material discrepancies were

noticed on physical verification and if so, whether the same have been properly dealt with in the books of account;

Home

49_caro_checklist Page 7 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 8/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response

1. Has the company granted any loans to

companies, firms and other parties covered in the

Register maintained under Section 301 of the Act?

2. Obtain a statement containing the name of the

company, firm or other Party, nature of relationship,amounts and dates of loans granted, amounts and

dates of loans refunded, amounts and dates of

interest received, closing balance at year end,

particulars of instalments (amount and period

outstanding for) of overdue principal and interest

together with the details regarding the rate of

interest, if any, and brief terms and conditions like

security, repayment particulars (principal and

interest) etc.,

3. Examine the above statement with necessary

documents and records on a reasonable test check

basis.

4. Report information as per the table below in the

case of all loans granted.

5. Check and conclude that the rate of interest and

other terms and conditions are not prima facie

prejudicial to the interest of the company or

otherwise by consideration of factors such as loan

agreements, borrower's financial standing, its ability

to lend, nature of security, the availability of

alternative sources of finance, the urgency of

borrowing, purpose of the loan, prevailing market

rates of interest etc.,Number of Parties Amount

involved

(In Rupees)

Year end

balance

(In

Ru ees

Notes:

1. The requirement of this clause also covers advances which are in the nature of loans.

2. Loan transactions that have been squared up during the year also would get covered under the requirement.

Clause 4(iii)(a) : Has the company granted any loans, secured or unsecured to companies, firms or other

parties covered in the register maintained under section 301 of the Act. If so, give the number of parties

and amount involved in the transactions; and

Clause 4(iii)(b) Whether the rate of interest and other terms and conditions of loans given by the

company, secured or unsecured, are prima facie prejudicial to the interest of the company; and

Remarks

Home

49_caro_checklist Page 8 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 9/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response

1. The regularity of receipt of principal

amount and interest should be considered

in the light of procedures such as review of

receipt schedule, loan agreements and

other relevant documents, actual dates of

receipt of principal and interest.

2. The following particulars should be

considered in reporting the irregularity of

receipt of principal and interest-

Name of the Party Overdue

Princi al

Overdue

Interest

Year end Balance

Notes:

2. Where no stipulations have been made for repayment of the loan, the auditor should state his inability to make

comments in the absence of terms of repayment.

1. If a due date for receipt of interest is not specified, it would be reasonable to assume that it falls due on each

anniversary of the loan.

Clause 4(iii)(c): Whether receipt of principal amount and interest are also regular; andRemarks

(In Rupees)

Home

49_caro_checklist Page 9 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 10/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response

1. Obtain a statement with the names of the companies,

firms or other parties, amount of loan granted,

outstanding amount at the year end and steps taken for

the recovery.

2. The reasonableness of steps taken by the company

for recovery should be judged in the light of factors such

as issue of reminders, sending advocate's notice,

management's representations, follow up with theborrowers, etc., as the case may be.

3. If not satisfied about the reasonability of steps taken,

consider the name of the party, overdue amount of

principal and interest for reporting.

4.Obtain management's representation regarding steps

that have been taken for recovery of overdue amounts

exceeding rupees one lakh

Clause 4(iii)(d): If overdue amount is more than one lakh, whether reasonable steps have been

taken by the company for recovery of the principal and interest;Remarks

Home

49_caro_checklist Page 10 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 11/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response

1.Has the company taken any loans from companies,

firms and other parties covered in the Register

maintained under Section 301 of the Act?

2. Obtain a statement containing the name of the

company, firm or other Party, nature of relationship,

amounts and dates of loans taken, amounts and datesof loans repaid, amounts and dates of interest paid,

closing balance at year end, particulars of instalments

(amount and period outstanding for) of overdue

principal and interest together with the details

regarding the rate of interest, if any, and brief terms

and conditions like security, repayment particulars

(principal and interest) etc.,

3. Examine the above statement with necessary

documents and records on a reasonable test check

basis.

4. Report information as per the table below in the

case of loans all loans taken.

5. Check and conclude that the rate of interest and

other terms and conditions are not prima facie

prejudicial to the interest of the company or otherwise

by consideration of factors such as loan agreements,

nature of security, the availability of alternative sources

of finance, the urgency of borrowing, purpose of the

loan, prevailing market rates of interest etc.,

Number of Parties Amountinvolved

In Ru ees

Year end balance(In Rupees)

Notes:

1. The requirement of this clause also covers advances which are in the nature of loans.

2. Loan transactions that have been squared up during the year also would get covered under the requirement.

Clause 4(iii)(e): Has the company taken any loans, secured or unsecured from companies, firms or otherparties covered in the register maintained under section 301 of the Act. If so, give the number of parties

and the amount involved in the transactions; and

Clause 4(iii)(f): Whether the rate of interest and other terms and conditions of loans taken by the

company, secured or unsecured, are prima facie prejudicial to the interest of the company; and

Remarks

Home

49_caro_checklist Page 11 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 12/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response

1. The regularity of payment of principal

amount and interest should be considered

in the light of procedures such as review of

repayment schedule, loan agreements and

other relevant documents, actual dates of

payment of principal and interest.

2. The following particulars should be

considered in reporting the irregularity of

principal and interest: (in Rupees)

Name of the Party OverduePrincipal

OverdueInterest

Year end Balance

Notes:

1. If a due date for payment of interest is not specified, it would be reasonable to assume that it falls due on each

anniversary of the loan.

2. Where no stipulations have been made for repayment of the loan, inability to make comments under the clause

should be stated.

Clause 4(iii)(g) Whether payment of the principal amount and interest are also regular.Remarks

Home

49_caro_checklist Page 12 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 13/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. On the basis of our understanding,

documentation and validation thereof in the

Myclient file-control activities in the areas of

Inventory cycle, property, plant and equipment

cycle, revenue and receivables cycle, review

of internal audit reports, are we satisfied that

there is an adequate internal control system

commensurate with the size of the company

and the nature of its business for the

purchase of inventory and fixed assets and

for the sale of goods and services?

If not document the inadequacies and

weaknesses thereof and consider implications

for reporting.

2. Review the reports of internal audit,

minutes of the Board, Audit committee,

management committee, if any and any other

relevant internal reports to identify major

weaknesses in internal controls and whether

there is any continuing failure to correct such

weaknesses.

3. In the case of continuing failure to correct

any major weakness identified, report the

weakness and steps taken by the

management to correct such weakness, if

addressed subsequent to the balance sheet

date or the fact of failure to correct such

weakness.

4. Consider the implications of such control

weaknesses on the nature, extent and timing

of audit procedures in those areas and

implications, if any, on the adequacy or

reliability of the books of account and the

overall report.Notes:

1. Ordinarily, any weakness in internal controls that exposes the company to a risk of significant loss

or the risk of a material misstatement in the financial statements may be considered as a

major weakness.

2. Continuing failure should be judged with reference to the weakness that existed at the time of

previous year's audit.

3. If any major weakness is corrected by the date on which the audit report is issued, the fact of such

correction subsequently must also be reported.

Clause 4(iv): Is there an adequate internal control system commensurate with the size of thecompany and the nature of its business, for the purchase of inventory and fixed assets and for

the sale of goods and services. Whether there is a continuing failure to correct major

weaknesses in internal control system.

Home

49_caro_checklist Page 13 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 14/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1.Has the company entered into any contracts or

arrangements that need to be entered into the register

maintained under Section 301 of the Act?

2. Are particulars of contracts or arrangements referred to

in Section 301 entered into the register maintained under

that section?

3. Obtain a list containing the name of the party, nature of

relationship, description of transaction and amount and

date of each such transaction individually and for al l the

transactions during the year.

4. Check the list for completeness of information with

reference to: knowledge from previous year's audit,

review of entity's procedures for identification of entries to

be made in 301 register, inquiries as to the affiliation of

directors and key management personnel, officers with

other entities, review of shareholders records to identify

the principal shareholders, review of entity's income tax

returns, review of joint venture and other relevant

agreements, minutes of board meetings, Form 24AAssubmitted etc.,

5. In respect of transactions exceeding the value of rupees

five lakhs in respect any party and in any one financial

year made under such contract or arrangements examine

information such as price l ists, quotations and records

relating to prices for similar transactions with other parties

at the relevant time.

6. In cases where transactions are entered with sole

suppliers, examine the reasonableness of prices paid

with reference to list prices of the supplier concerned,

other trade terms of the supplier, etc. and where required,

consider the same appropriately in the report.

7. The reasonableness of the prices should be determined

taking into account factors such as delivery period, quality

of the product, quantity, credit terms, past performance of

the party etc.,

Notes: 1. The requirement of this clause does not cover transactions with subsidiaries per se unless one or more of the

directors of the company are interested in the subsidiary in terms of Section 297/299 of the Companies Act, 1956.

Clause 4(v) (a): Whether the particulars of contracts or arrangements referred to in section 301 of the Act have beenentered in the register required to be maintained under that section; and

Clause 4(v)(b): Whether transactions made in pursuance of such contracts or arrangements have been made at

prices which are reasonable having regard to the prevailing market prices at the relevant time;

(This information is required only in case of transactions exceeding the value of five lakhs rupees in respect of any

party and in any one financial year).

Home

49_caro_checklist Page 14 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 15/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Has the Company accepted any deposits from

public within the meaning of Section 58A, 58AA

and rules framed thereunder?

2. Obtain a general understanding of Section 58A,

58AA and the relevant rules and ascertain the

system and procedures of the company to ensure

compliance with the provisions of the said sections

and the rules made thereunder.

3. Check the compliance with the requirements of

the Act and the rules framed thereunder by

completing the firm's checklist on Acceptance of

Deposit Rules and Companies Act 1956.

4. Examine the internal controls in place for

identifying defaults in repayment of deposits made

by small investors or part or any interest thereon.

Based on the understanding so gained, perform a

reasonable test check of the deposits received

from small investors.

5. Enquire of the management possible instances

of non-compliances with Section 58A, 58AA and

relevant rules and about any order passed by the

CLB, National Company Law Tribunal, RBI, or any

Court, or any other Tribunal on contraventions.

6. Examine the correspondence and documents

filed with the Registrar of Companies, Company

Law Board, National Company Law Tribunal, RBI,

legal correspondence for orders passed and thesteps taken by the company to comply with the

order.

Clause 4(vi): In case the company has accepted deposits from the public, whether the directives issued by the

Reserve Bank of India and the provisions of sections 58A, 58AA or any other relevant provisions of the Act and

the rules framed there under, where applicable, have been complied with. If not, the nature of contraventions

should be stated; If an order has been passed by Company Law Board or National Company Law Tribunal or

Reserve Bank of India or any Court or any other Tribunal whether the same has been complied with or not?

Home

49_caro_checklist Page 15 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 16/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Is the company a listed company or having paid up

capital and reserves exceeding Rs. 50 lakhs as at the

commencement of the financial year concerned or having

an average annual turnover exceeding five crores rupees

for a period of three consecutive financial years

immediately preceding the financial year?

2. Consider the following factors to determine whether the

internal audit system is commensurate with the size of theand the nature of its business-

-Size of the internal audit department; and whether the

company has a separate internal audit department or an

outside professional firm is engaged;

- Internal Audit Plan and adequacy of areas of coverage

-Qualifications of the internal audit staff;

-Whether the internal audit department is independent

of the accounting and custody departments;

-Reporting levels of internal audit;

-Areas of coverage, and also whether the internal auditsare conducted in accordance with the generally

accepted auditing standards;

-Adequacy of technical assitance available to the

internal audit department;

-Reports submitted by the internal audit and follow up

procedures thereof.

1. The date of the balance sheet must be considered in reckoning the listing status of the company.

2. While evaluating the adequacy of internal audit system, existence or otherwise of other forms of internal controls must also

be taken into account.

Clause 4(vii): In the case of listed companies and/or other companies having a paid-up capital and reserves exceeding Rs.50lakhs as at the commencement of the financial year concerned, or having an average annual turnover exceeding five crore

rupees for a period of three consecutive financial years immediately preceding the financial year concerned, whether the

company has an internal audit system commensurate with its size and nature of its business;

Notes:

Home

49_caro_checklist Page 16 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 17/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Is maintenance of cost records prescribed

by Central Government under Section

209(1)(d) applicable to the company?

2. Obtain a list of books and records made

and maintained by the company under

Section 209(1)(d) of the Companies

Act,1956.

3. Conduct a general review of the cost

records to ensure that the records as

prescribed are made and maintained.

Clause 4(viii): Where maintenance of cost records has been prescribed by the CentralGovernment under clause (d) of sub-section (1) of section 209 of the Act, whether such

accounts and records have been made and maintained;

Home

49_caro_checklist Page 17 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 18/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Clause 4(ix)(a): Is the company regular in depositing undisputed statutory dues including

Provident Fund, Investor Education and Protection Fund, Employees’ State Insurance, Income-tax,

Sales-tax, Wealth Tax, Service Tax, Custom Duty, Excise Duty, cess and any other statutory dues

with the appropriate authorities and if not, the extent of the arrears of outstanding statutory dues

as at the last day of the financial year concerned for a period of more than six months from the

date they became payable, shall be indicated by the auditor.

Clause 4(ix)(b): In case dues of Income tax/ Sales tax /Wealth tax/ Service tax/ Custom duty/ Excise

duty/ cess have not been deposited on account of any dispute, then the amounts involved and the

forum where dispute is pending shall be mentioned.

Home

1. Obtain a statement containing the list ofvarious statutes under which the company is

required to make payments to appropriate

authorities including those relating to Provident

Fund, Investor Education and Protection Fund,

Employees’ State Insurance, Income-tax,

Sales-tax, Wealth Tax, Service Tax, Custom

Duty, Excise Duty, cess etc, the nature and

amounts of payments under each statute, the

due dates for making such payments, the

dates on which the payments were made by

the Company, the arrears due for more than

six months as at the Balance Sheet date andthe date and amount of subsequent payments,

if any made out of such arrears.

2. Obtain a general understanding of various

statutes governing the entities and dues

payable under those statutes. Make enquiries

of the management about the statutes under

which the company is required to pay dues and

the policies and procedures in place for

identifying and payment of such dues.

3. Verify the statement under 1 above and with

the general understanding obtained and

gained the underlying documents and records,

compile the the following details in the case of

arrears of statutory dues:

- Name of the statute

49_caro_checklist Page 18 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 19/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Clause 4(ix)(a): Is the company regular in depositing undisputed statutory dues including

Provident Fund, Investor Education and Protection Fund, Employees’ State Insurance, Income-tax,

Sales-tax, Wealth Tax, Service Tax, Custom Duty, Excise Duty, cess and any other statutory dues

with the appropriate authorities and if not, the extent of the arrears of outstanding statutory dues

as at the last day of the financial year concerned for a period of more than six months from the

date they became payable, shall be indicated by the auditor.

Clause 4(ix)(b): In case dues of Income tax/ Sales tax /Wealth tax/ Service tax/ Custom duty/ Excise

duty/ cess have not been deposited on account of any dispute, then the amounts involved and the

forum where dispute is pending shall be mentioned.

Home

- Nature of the dues

- Amount

- Due date

- Date of payment

4. Whether the Company has been generally

regular in depositing statutory dues or

otherwise, report the same appropriately.

5. In the case of disputed statutory dues,

compile the following details:- Name of the Statute

- Nature of the dues

- Amount

- Forum where dispute is pending

Information under this clause should be given

separately for each period even though the

dispute relates to the same nature of statutory

dues, like income taxes etc.,

Notes:1. The scope under this clause is restricted to only those statutory dues which are required to be paid

regularly to a body.

2. Reporting under this clause is required irrespective of the fact whether or not there are any arrears

as at the balance sheet date.

3. For a matter to be considered as "disputed" there must be a positive evidence or action on part of

the company to show that it has not accepted the demand for payment of duty or tax. The sustain-

-ability or otherwise of the claim is not to be judged.

4. Penalites or interest would be covered under "amounts payable".

49_caro_checklist Page 19 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 20/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Obtain a statement containing the names of the

institution/bank/debenture holder, the period and

amounts of default, due dates thereof and dates and

amounts of subsequent payments, if any. Yes

2. Verify the statement in 1 above, with documents

such as agreements, other terms and conditions,

debenture trust deed as the case may be. Identify the

period and amount of default for reporting. Yes

Notes:

1. The requirement covers all the defaults existing on the balance sheet date, irrespective of when the defaults have occurred.

2. Dues cover all amounts including interest and principal.

3. Applications for reschedulement/restructuring will not be binding unless approved.4. Dues not paid by the company on account of unilateral disputes tantamount to default.

Clause 4(xi): Whether the company has defaulted in repayment of dues to a financial institution or bank or debenture

holders? If yes, the period and amount of default to be reported;

Home

49_caro_checklist Page 20 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 21/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Whether the company has granted any

loans and advances on the basis of security

by way of pledge of shares, debentures and

other securities?Yes

2. If yes, examine whether documents and

records include details such as the name and

address of the borrower, amount, terms and

conditions such as period, rate of interest,

security etc., disbursements, repayments,recovery of interest; full particulars of security,

names of the companies, number and class

of shares, distinctive numbers, particulars as

to tit le etc; documents needed for transfer,

details as to periodical ackowledgements of

the parties, proof to establish the power of the

party to borrow- e.g. board resolution etc.,

Yes

3. Obtain a statement containing the details of

such loans granted including name of the

party, amount of loan/advance granted,

amount outstanding as the balance sheet

date and type and nature of security and

verify the same on a reasonable test checkbasis with documents and records mentioned

in 2 above.

Yes

4. Verify the securities pledged by reference

to physical securities or statements from

depository participants. In the case of

dematerialized form of securities confirm that

the company has a valid right to sell the

shares in the event of default.

Yes

5. Whether security is in the custody of

company and market value of security is

adequate to cover the outstanding amount ofloan and interest? Yes

6. List the deficiencies for reporting. Yes

Notes:

1. The requirement of this clause does not extend to other forms of security like

hypothecation, guarantee etc.,

2. Other securities may be construed to mean bonds or promissory notes issued by a government

or semi-government authority.

Clause 4(xii): Whether adequate documents and records are maintained in cases where thecompany has granted loans and advances on the basis of security by way of pledge of

shares, debentures and other securities; If not, the deficiencies to be pointed out.

Home

49_caro_checklist Page 21 of 31

8/2/2019 49 Caro Checklist

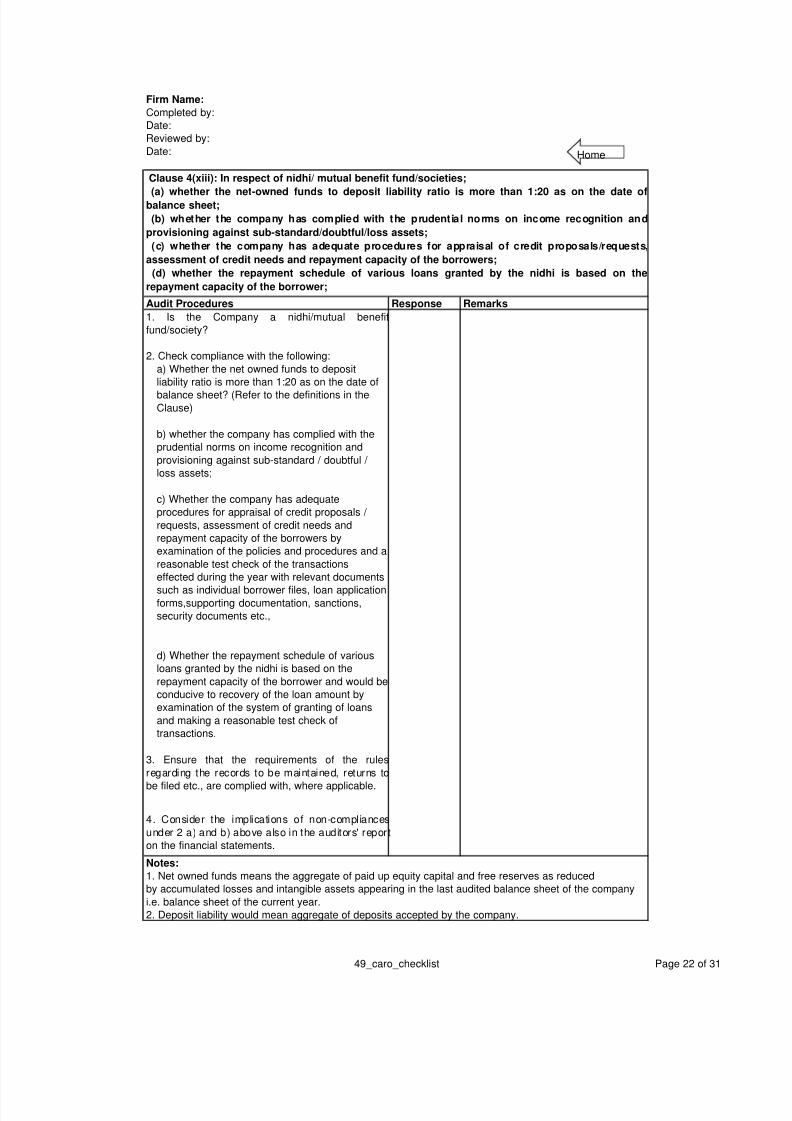

http://slidepdf.com/reader/full/49-caro-checklist 22/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Is the Company a nidhi/mutual benefit

fund/society?

2. Check compliance with the following:

a) Whether the net owned funds to deposit

liability ratio is more than 1:20 as on the date of

balance sheet? (Refer to the definitions in theClause)

b) whether the company has complied with the

prudential norms on income recognition and

provisioning against sub-standard / doubtful /

loss assets;

c) Whether the company has adequate

procedures for appraisal of credit proposals /

requests, assessment of credit needs and

repayment capacity of the borrowers by

examination of the policies and procedures and a

reasonable test check of the transactions

effected during the year with relevant documents

such as individual borrower files, loan applicationforms,supporting documentation, sanctions,

security documents etc.,

d) Whether the repayment schedule of various

loans granted by the nidhi is based on the

repayment capacity of the borrower and would be

conducive to recovery of the loan amount by

examination of the system of granting of loans

and making a reasonable test check of

transactions.

3. Ensure that the requirements of the rules

regarding the records to be maintained, returns to

be filed etc., are complied with, where applicable.

4. Consider the implications of non-compliances

under 2 a) and b) above also in the auditors' report

on the financial statements.

Notes:

1. Net owned funds means the aggregate of paid up equity capital and free reserves as reduced

by accumulated losses and intangible assets appearing in the last audited balance sheet of the company

i.e. balance sheet of the current year.

2. Deposit liability would mean aggregate of deposits accepted by the company.

Clause 4(xiii): In respect of nidhi/ mutual benefit fund/societies;

(a) whether the net-owned funds to deposit liability ratio is more than 1:20 as on the date ofbalance sheet;

(b) whether the company has complied with the prudential norms on income recognition and

provisioning against sub-standard/doubtful/loss assets;

(c) whether the company has adequate procedures for appraisal of credit proposals/requests,

assessment of credit needs and repayment capacity of the borrowers;

(d) whether the repayment schedule of various loans granted by the nidhi is based on the

repayment capacity of the borrower;

Home

49_caro_checklist Page 22 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 23/31

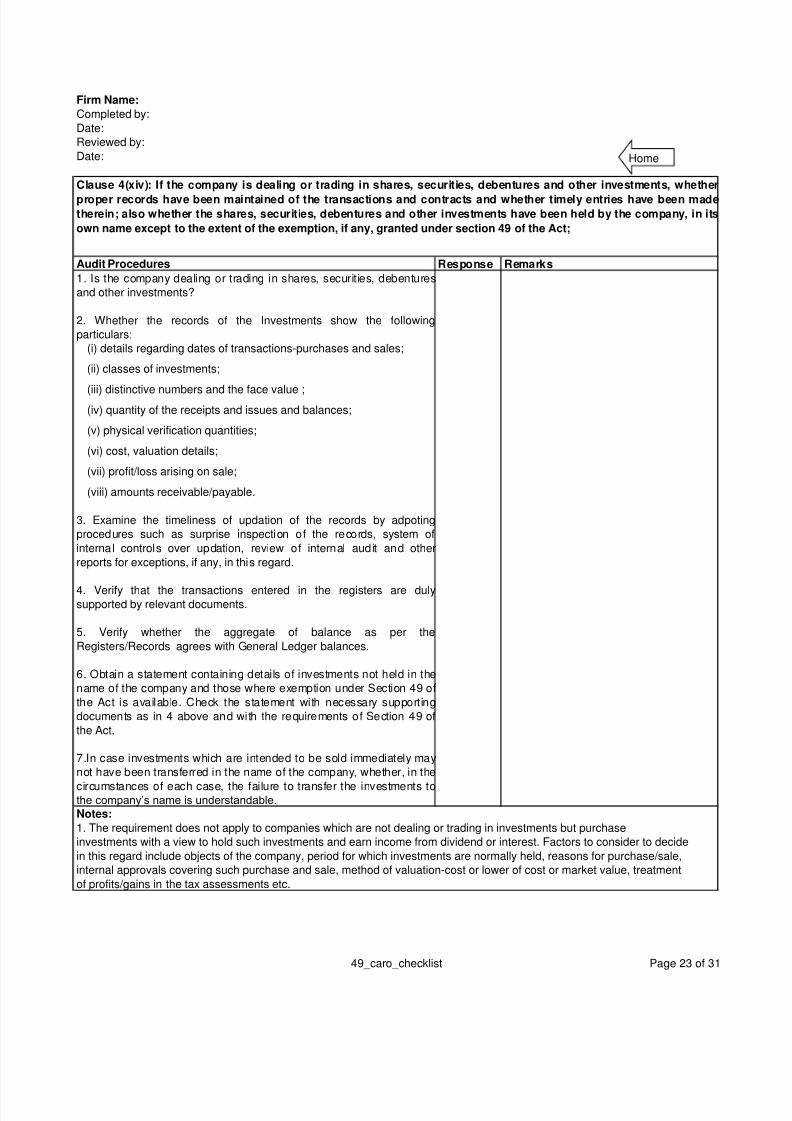

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Is the company dealing or trading in shares, securities, debentures

and other investments?

2. Whether the records of the Investments show the following

particulars:

(i) details regarding dates of transactions-purchases and sales;

(ii) classes of investments;

(iii) distinctive numbers and the face value ;(iv) quantity of the receipts and issues and balances;

(v) physical verification quantities;

(vi) cost, valuation details;

(vii) profit/loss arising on sale;

(viii) amounts receivable/payable.

3. Examine the timeliness of updation of the records by adpoting

procedures such as surprise inspection of the records, system of

internal controls over updation, review of internal audit and other

reports for exceptions, if any, in this regard.

4. Verify that the transactions entered in the registers are dulysupported by relevant documents.

5. Verify whether the aggregate of balance as per the

Registers/Records agrees with General Ledger balances.

6. Obtain a statement containing details of investments not held in the

name of the company and those where exemption under Section 49 of

the Act is available. Check the statement with necessary supporting

documents as in 4 above and with the requirements of Section 49 of

the Act.

7.In case investments which are intended to be sold immediately may

not have been transferred in the name of the company, whether, in the

circumstances of each case, the failure to transfer the investments tothe company’s name is understandable.

Notes:

1. The requirement does not apply to companies which are not dealing or trading in investments but purchase

investments with a view to hold such investments and earn income from dividend or interest. Factors to consider to decide

in this regard include objects of the company, period for which investments are normally held, reasons for purchase/sale,

internal approvals covering such purchase and sale, method of valuation-cost or lower of cost or market value, treatment

of profits/gains in the tax assessments etc.

Clause 4(xiv): If the company is dealing or trading in shares, securities, debentures and other investments, whether

proper records have been maintained of the transactions and contracts and whether timely entries have been madetherein; also whether the shares, securities, debentures and other investments have been held by the company, in its

own name except to the extent of the exemption, if any, granted under section 49 of the Act;

Home

49_caro_checklist Page 23 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 24/31

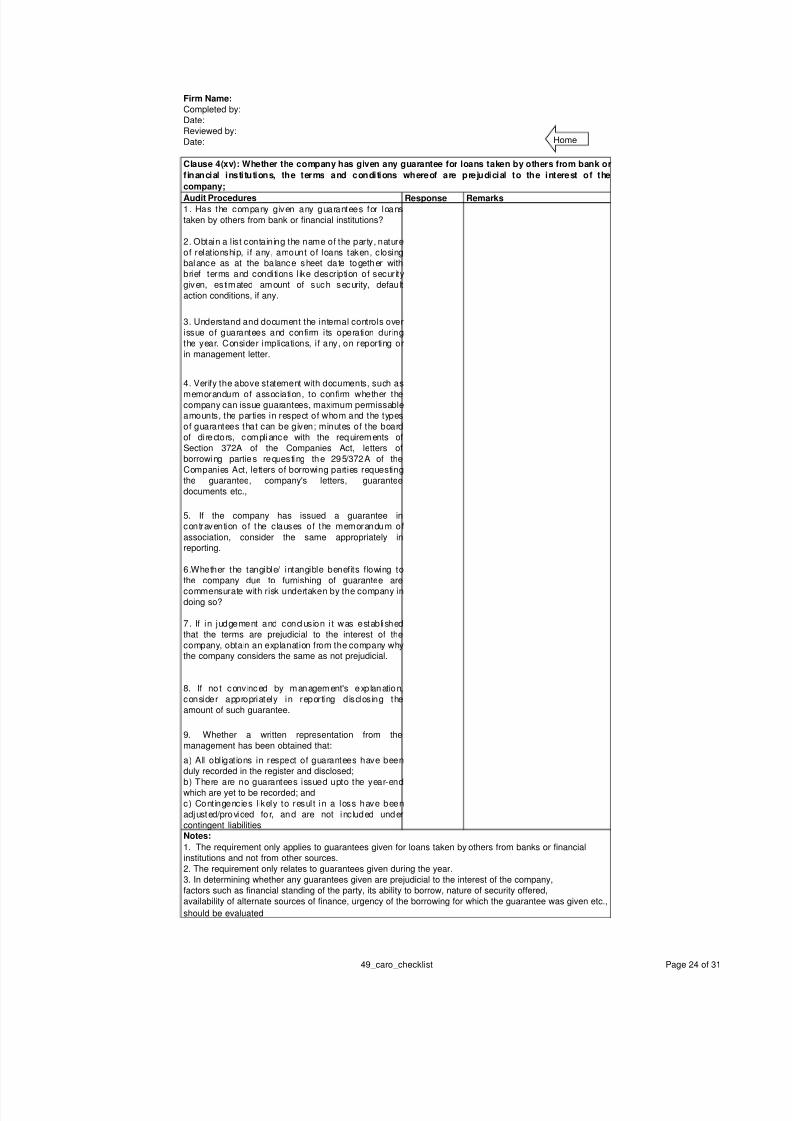

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks1. Has the company given any guarantees for loans

taken by others from bank or financial institutions?

2. Obtain a list containing the name of the party, nature

of relationship, if any, amount of loans taken, closingbalance as at the balance sheet date together with

brief terms and conditions like description of security

given, estimated amount of such security, defau lt

action conditions, if any.

3. Understand and document the internal controls over

issue of guarantees and confirm its operation during

the year. Consider implications, if any, on reporting or

in management letter.

4. Verify the above statement with documents, such as

memorandum of association, to confirm whether thecompany can issue guarantees, maximum permissableamounts, the parties in respect of whom and the types

of guarantees that can be given; minutes of the board

of di rectors, compliance with the requirements of

Section 372A of the Companies Act, letters of

borrowing parties requesting the 295/372A of the

Companies Act, letters of borrowing parties requesting

the guarantee, company's letters, guarantee

documents etc.,

5. If the company has issued a guarantee incontravention of the clauses of the memorandum of

association, consider the same appropriately inreporting.

6.Whether the tangible/ intangible benefits flowing to

the company due to furnishing of guarantee are

commensurate with risk undertaken by the company indoing so?

7. If in judgement and conclusion it was established

that the terms are prejudicial to the interest of the

company, obtain an explanation from the company whythe company considers the same as not prejudicial.

8. If not convinced by management's exp lanation,

consider appropriately in reporting disclosing the

amount of such guarantee.

9. Whether a written representation from the

management has been obtained that:

a) All obligations in respect of guarantees have been

duly recorded in the register and disclosed;

b) There are no guarantees issued upto the year-endwhich are yet to be recorded; and

c) Contingencies l ikely to result in a loss have been

adjusted/provided for, and are not inc luded under

contingent liabilitiesNotes:

2. The requirement only relates to guarantees given during the year.

3. In determining whether any guarantees given are prejudicial to the interest of the company,

factors such as financial standing of the party, its ability to borrow, nature of security offered,

availability of alternate sources of finance, urgency of the borrowing for which the guarantee was given etc.,

should be evaluated

Clause 4(xv): Whether the company has given any guarantee for loans taken by others from bank or

financial institutions, the terms and conditions whereof are prejudicial to the interest of the

company;

1. The requirement only applies to guarantees given for loans taken by others from banks or financial

institutions and not from other sources.

Home

49_caro_checklist Page 24 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 25/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Has the company obtained any term loans or made

any utilisation during the year? Yes

2.Obtain a statement containing the specific terms of

loans and the details of application-amounts, dates and

the purpose.

3.Verify the statement with documents such as sanction

letters and other documents containing the terms and

conditions and those relating to actual utilisation.

4. If term loans were not applied for the purpose for

which they were obtained, indicate the amount and the

purpose for which it was ultimately utilised.

5. In the case of temporary application of funds for other

purposes before they were utilised for the stated

purpose, mention such fact in the report.

6.Whether the funds flow statement has been reviewed

where one to one correlation is not possible?

Notes:

1. Working capital term loans are not within the scope of this clause.

2. The reporting requirement under this clause also covers temporary use of surplus funds.

3. It is not necessary to establish a one to one relationship with the amount of term loan and its utilisation.

Clause 4(xvi): Whether term loans were applied for the purpose for which the loans were obtained;

Home

49_caro_checklist Page 25 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 26/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1.Obtain a statement containing the specific

terms of funds and details of use-amounts

and nature.

2. Compare the quantum of long term funds

with the long term application of funds.

3. Compare the quantum of short term funds

with the short term application of funds.

4. If the differences point towards use of

short term funds for long term investment,

consider appropriately in reporting.

Notes:

1. Long-term sources of funds would include share capital, reserves and surplus, provision

for depreciation, long term debt securities, long term loans. Long term application of funds would

include investment in fixed assets, long term investments and other assets of similar nature,

repayment of long term loans and advances or redemption of debt securities, use for core working

capital etc., Short term sources of funds include temporary credit facilities like cash credits,

overdraft, reduction in current assets or increase in current liabilities etc., Short term application offunds includes all application otherwise than for long term use, increase in current assets or

decrease in current liabilities etc.,

2. The requirement has to be determined on the basis of the overall picture of the sources and

application of funds based on the balance sheet of the company unless a one to one direct

relationship can be established between a particluar source and application.

Clause 4(xvii): Whether the funds raised on short-term basis have been used for long terminvestment; If yes, the nature and amount is to be indicated;

Home

49_caro_checklist Page 26 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 27/31

Firm Name:

Completed by:Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Has the company made any preferential allotment of shares to

parties and companies covered in the Register maintained underSection 301 of the Companies Act,1956?

2. Obtain a statement containing the names of the parties and

companies, nature of relationship, description of allotments made-equity/preference, number of shares, price and terms and

conditions of the allotments made during the year.

3. In the case of listed companies check whether the price forshares issued on a preferential basis is not less than higher of the

following-

-the average of the weekly high and low of the closing prices ofthe related shares quoted on the stock exchange during the sixmonths preceding the relevant date.

- the average of the weekly high and low of the closing prices of

the related shares quoted on the stock exchange during the twoweeks preceding the relevant date.

4. In the case of listed companies, confirm and verify that the

company has complied with the requirements of guidelines laid

down in this regard by SEBI.

5. In the case of private company and an unlisted public company,examine the method used for valuation of the shares and also

ascertain the reasonableness of the assumptions underlying the

calculation.

6. If in the judgement and conclusion, it was eastablished that theprice charged is not fair, obtain a representation from the

management as to why such price charged is not prejuducial to

the interest of the company and consider appropriately inreporting.

7. Consider compliance with the requirements of SA 620 (formerly

AAS-9) "Using the work of an Expert" if the valuation report of an

expert is used as the basis.

8. If the company has made a preferential issue by passing anordinary resolution, also examine the relevant order of the

Government passed in this regard. If, on the basis of order, it is

concluded that the price charged is not prejudicial, state the fact of

reliance on such order for the purpose of reporting.

9. Obtain a representation from the management as to why thecompany considers that the price charged is not prejudicial to the

interest of the company and evaluate whether the explanation is

convincing

Notes:

1.The term "shares" includes both preference as well as Equity.

2. In the case of a listed company, allotment of shares under Section 81(1A) of the Companies Act,1956 is known aspreferential allotment of shares.

Clause 4(xviii): Whether the company has made any preferential allotment of shares to parties and companies

covered in the Register maintained under section 301 of the Act and if so whether the price at which shares

have been issued is prejudicial to the interest of the company;

Home

49_caro_checklist Page 27 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 28/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Has the company issued any debentures and the

same outstanding at the end of the year?

2. Verify the debenture trust deed executed under

Section 117A of the Act in respect of debentures issued

during the year with particular reference to security

requirements.

3.Verify whether such security or charge is created as

required under section 125 and 130 of the Act by

examining the documents evidencing the charge-forms

filed with ROC etc.,

Clause 4(xix) Whether security or charge has been created in respect of debentures issued?

Home

49_caro_checklist Page 28 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 29/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1. Has the company made any public issue or made any

utilisation during the year?

2. Obtain a statement containing the quantum of money

raised on public issue of any security made by the

company during the year and details of end use of

money so raised.

3. Verify such statement with reference to end use as set

out in the Prospectus. Where the issue exceeds Rs. 500

Crores, refer the half yearly reports of the monitoring

agency as submitted to SEBI.

4. Verify the disclosure made by the company in the

financial statements in this regard.

5. If we are not satisfied with the disclosures made in the

financial statements, consider the matter for reporting

setting out clearly the information which should have

been dislosed.

6. Whether the cash flow statement has been reviewed

where one to one correlation is not possible?

7. If we are unable to determine the end use of money

raised from public issues state the fact together with the

reasons thereof in our report.

8. Whether a representation from the management has

been obtained as to the completeness of the disclosures

with regard to the end use of moneys raised by public

issues.

Clause 4(xx): Whether the management has disclosed on the end use of money raised by public issuesand the same has been verified;

Home

49_caro_checklist Page 29 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 30/31

Firm Name:

Completed by:

Date:

Reviewed by:

Date:

Audit Procedures Response Remarks

1.Complete our understanding and assessment of

fraud considerations as per steps given under "Fraud

Risk" in MYClient file. Done

2. On the basis of work carried out as above, are we

satisfied that there are no indications of fraud on or

by the company noticed or reported during the year?

Done

3. If any fraud is noticed or if there is a doubt about

the existence of fraud, carry out procedures as

mentioned in SA 240 (formerly AAS-4) "The Auditor's

Responsibility to consider fraud and error in an audit

of Financial Statements" Done

4. If the response to 2 above is "No" determine the

nature and extent of such frauds and implications on

our reporting. Done

5. Where any fraud on the company or by the

company has been noticed or reported, whether the

the nature and amount of frauds has beendetermined and disclosed? Also, whether

management representation has been obtained to

this effect?Done

Notes:

The following are the indicative sources relating to identification of Fraud:

i. the reports of internal reviews/audits conducted, if any.

ii.inquiries of the management about any frauds on or by the company that it has noticed or that have been

reported to it.

iii. discussions with other employees of the company.

iv. examination of the minutes book of the meetings of Board, audit committee etc.,

v. Reports, if any, on inspection/investigation by Regulatory/Government Authorities.

Clause 4(xxi): Whether any fraud on or by the company has been noticed or reported during the year; Ifyes, the nature and the amount involved is to be indicated

Home

49_caro_checklist Page 30 of 31

8/2/2019 49 Caro Checklist

http://slidepdf.com/reader/full/49-caro-checklist 31/31

Firm Name:

Clause No. Area/Requirement Brief Description of the Issue How addressed in the Audit

4(i) (a) Fixed Assets

4(i) (b) Fixed Assets

4(i)( c) Fixed Assets

4(ii) (a) Inventories

4(ii) (b) Inventories

4(ii) ( c) Inventories

4(iii)(a) Loans granted

4(iii)(b) Loans granted interest & terms

4(iii)(c) Loans granted repayment

4(iii)(d) Loans granted overdue

4(iii)(e) Loans taken

4(iii)(f) Loans taken interest and terms

4(iii)(g) Loans taken repayment

4(iv) Internal Control System

4(v)(a) & (b) Register under Section 301 etc.,

4(vi) Acceptance of Deposits

4(vii) Internal Audit

4(viii) Cost Records

4(ix) (a) & (b) Statutory dues

4(x) Accumulated losses etc.,

4(xi) Dues to Banks & FIs etc.,

4(xii) Loans and Advances granted

4(xiii)(a) Chit Fund company

4(xiii)(a) to (d) Nidhi/mutual benefit fund/society

4(xiv) Dealing or Trading in Securities

4(xv) Guarantees4(xvi) Term Loans

4(xvii) Funds raised

4(xviii) Allotment of shares

4(xix) Debentures

4(xx) Money raised on public issue

4(xxi) Fraud

Home