2010 Paper BS E

8

~ 6 UNIVERSITY OFMORATUWA FACULTY OFENGINEERING DEPARTMENT OF MANAGEMENT OFTECHNOLOGY B.Sc. ENGINEERING LEVEL 4 SEMESTER 1 EXAMINATION MN 3040 - BUSINESS ECONOMICS AND FINANCIAL ACCOUNTING T IM E ALLOWED : 3 HOURS FEBRUARY 2010 INSTRUCTIONS TO CANDIDATES: This paper contains 8 quest i ons with TWO (02) sections on 06 pages . This examination accounts for 60 of the module assessment . T his is a closed book examination. Mobile phones are not permitted. The maximum marks attainable are indicated in square brackets. Answer FIVE [05] questions selecting TWO [02] questions from Section A and THREE [03] questions from Section B. Use separate Answer Booklets for Section A and Section B . Clearly state the assumptions you made on the script . If you have a y doubt as to the interpretation of the wording of a question , make your own decision , but clearly state it on the answer script .

-

Upload

gimhan-jayasiri -

Category

Documents

-

view

219 -

download

0

Transcript of 2010 Paper BS E

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 1/8

~

6

UNIVERSITY OF MORATUWA

FACULTY OF ENGINEERING

DEPARTMENT OF MANAGEMENT OF TECHNOLOGY

B.Sc. ENGINEERING

LEVEL 4 SEMESTER 1 EXAMINATION

MN 3040 -

BUSINESS ECONOMICS AND FINANCIAL ACCOUNTING

TIME ALLOWED: 3 HOURS

FEBRUARY 2010

INSTRUCTIONS TO CANDIDATES:

This paper contains 8 questions with TWO (02) sections on 06 pages.

This examination accounts for 60 of the module assessment.

This is a closed book examination. Mobile phones are not permitted.

The maximum marks attainable are indicated in square brackets.

Answer FIVE [05] questions selecting TWO [02] questions from Section A and

THREE [03] questions from Section B.

Use separate Answer Booklets for Section A and Section B.

Clearly state the assumptions you made on the script.

If you have any doubt as to the interpretation of the wording of a question, make your

own decision, but clearly state it on the answer script.

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 2/8

This page is intentionally left blank

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 3/8

SECTION A:BvSINESS ECONOMICS

MN3040

Instructions to Candidates: Answer any two [02]questions from Section A.

All questions carry equal marks

Question 01

a. Give a definition for business economics and explain the basics in business

economics. [04marks]

b. Explain the basic differencebetween economic and accounting costs concepts.

[04marks]

c. Explain how business economics helppracticing engineers in their day to day

decision makings. Provide examples. [04marks]

d. Explain the main features of mixed economic system. [04 marks]

e. How do you explain the law of diminishing returns? [04 marks]

Question 02

a. With examples explain the behaviour of Sri Lankan rice market by using demand

and supply framework. [04marks]

b. Giving suitable examples explain the three types of price discrimination and

conditions for successful price discrimination. [08marks]

c. Explain importance of elasticity concept for business. [04marks]

d. What do you understand from the Angel's law? [04 marks]

Question 03

a. Explain the technical relationships betweenTotal Product [TP],Average Product

[AP] and Marginal Product [MP] curves. [04marks]

b. Giving appropriate examples, discuss the pricing andproduction behavior of

perfect competition and oligopolymarket structures. [08marks]

c. Distinguish between economies of scales and scopes. [04 marks]

d. Explain why technical progress and factor productivity are considered as key

determinants of economic growth. [04marks]

Page 1 of6

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 4/8

SECTION A:BuSINESS ECONOMICS

MN3040

Question 04

Write short notes on five of the following:

a. GNP and NNP.

b. Porter's five forces model and SCP framework.

c. Short and long run cost functions.

d. Demand estimation and forecasting techniques.

e. Monopoly and monopolistic competition.

f Movement along the demand curve and shift in supply curve.

g. Macro economics and micro economics.

h. Factors of production and basic economic problems. [04 marks for each]

Page 2 of6

End of Section A

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 5/8

SECTION B: FINANCIAL AND COST ACCOUNTING

MN3040

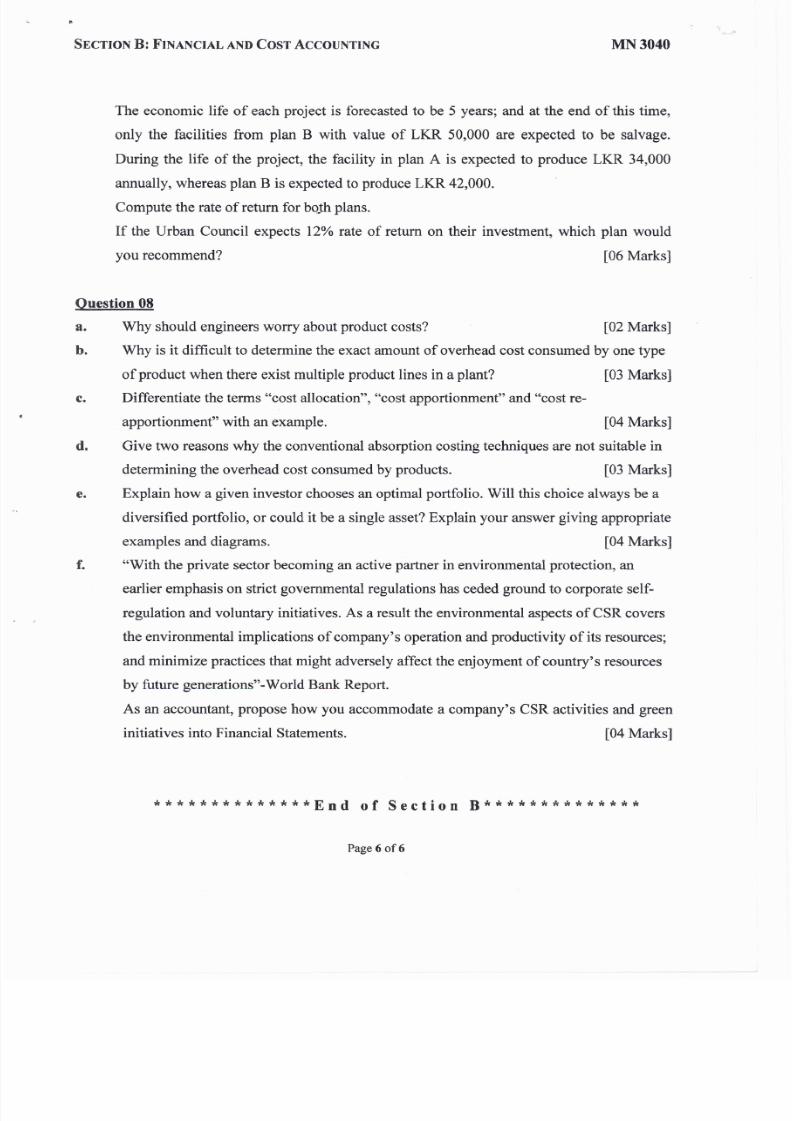

The economic life of each project is forecasted to be 5 years; and at the end of this time,

only the facilities from plan B with value of LKR 50,000 are expected to be salvage.

During the life of the project, the facility in plan A is expected to produce LKR 34,000

annually, whereas plan B is expected to produce LKR 42,000.

Compute the rate of return for both plans.

If the Urban Council expects 12 rate of return on their investment, which plan would

you recommend? [06 Marks]

Question 08

a. Why should engineers worry about product costs? [02 Marks]

b. Why is it difficult to determine the exact amount of overhead cost consumed by one type

of product when there exist multiple product lines in a plant? [03 Marks]

c. Differentiate the terms cost allocation , cost apportionment and cost re-

apportionment with an example. [04 Marks]

d. Give two reasons why the conventional absorption costing techniques are not suitable in

determining the overhead cost consumed by products. [03 Marks]

e. Explain how a given investor chooses an optimal portfolio. Will this choice always be a

diversified portfolio, or could it be a single asset? Explain your answer giving appropriate

examples and diagrams. [04 Marks]

f With the private sector becoming an active partner in environmental protection, an

earlier emphasis on strict governmental regulations has ceded ground to corporate self-

regulation and voluntary initiatives. As a result the environmental aspects of CSR covers

the environmental implications of company's operation and productivity of its resources;

and minimize practices that might adversely affect the enjoyment of country's resources

by future generations -World Bank Report.

As an accountant, propose how you accommodate a company's CSR activities and green

initiatives into Financial Statements. [04 Marks]

**************End of Section B**************

Page 6 of6

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 6/8

SECTION B FINANCIAL AND COST ACCOUNTING

MN3040

•

e. A biscuit manufacturing company offers four types of biscuits in their product range.

Budgeted data for the next yearwould be as follows.

Table Qn.6

Cracker

Cream

Chocolate

Vege

250,000

400,000

300,000

150,000

35

30

40

45

Product

Sales packets

Selling price per packet Rs.

Variable cost of an individual product is 30 of the selling price of the respective product.

Budgeted fixed cost would be Rs. 1,400,000.

1. Calculate the level of sales required to break- even. [2 marks]

11 Determine the break - even sales value of each product. [3 marks]

111. Determine the number of packets to be sold to achieve break-even under each product

category. [2 marks]

Question 07

a. Capital has the power to earn and satisfy our needs. Discuss the capital the view points of

the Lender and Borrower. [04Marks]

b. Explain the advantages and disadvantages of IRR and NPV as project appraisal

techniques? [05 Marks]

c. When comparing two projects, the use of the NPV and the IRR methods may give

different results. A project selected according to the NPV may be rejected if the IRR

method is used. Why? [05Marks]

d. Two alternative investment proposals are under consideration for a vacant lot owned by

Urban Development Council. Plan A would require an immediate investment of LKR

120,000 and the first year expenditure for property taxes, maintenance, and insurance of

LKR 4,000, with this amount expected to increase at a rate of LKR 1,000 per year. Plan B

would have a first cost LKR 170,000 and a total first expense of LKR 9,000, with an

increase ofLKR 1,000per year. (Continue to page 06)

Page 5 of6

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 7/8

SECTION

B

FINANCIAL AND COST ACCOUNTING

MN3040

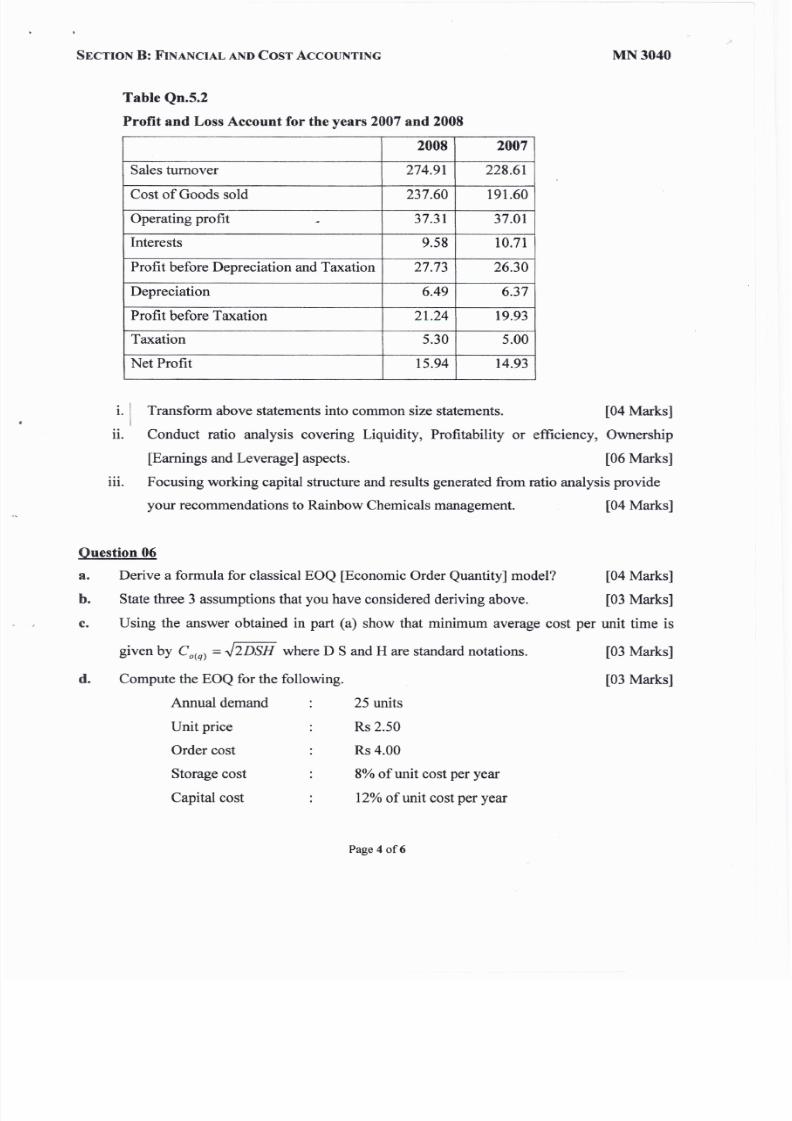

Table Qn.5.2

Profit and Loss Account for the years 2007 and 2008

2008 2007

Sales turnover 274.91 228.61

Cost of Goods sold 237.60

191.60

Operating profit

37.31

37.01

Interests

9.58

10.71

Profit before Depreciation and Taxation

27.73

26.30

Depreciation

6.49

6.37

Profit before Taxation

21.24

19.93

Taxation

5.30 5.00

Net Profit

15.94 14.93

'. Transform above statements into common size statements.

[04 Marks]

11

Conduct ratio analysis covering Liquidity, Profitability or efficiency, Ownership

[Earnings and Leverage] aspects.

[06 Marks]

111 Focusing working capital structure and results generated from ratio analysis provide

your recommendations to Rainbow Chemicals management. [04 Marks]

Question 06

Derive a formula for classical EOQ [Economic Order Quantity] model?

State three 3 assumptions that you have considered deriving above.

[04 Marks]

[03 Marks]

c. Using the answer obtained in part (a) show that minimum average cost per unit time is

d

given by CO q

= J DSH

where D S and H are standard notations.

Compute the EOQ for the following.

Annual demand 25 units

[03 Marks]

[03 Marks]

Unit price

Order cost

Storage cost

Capital cost

Rs 2.50

Rs 4.00

8 of unit cost per year

12 of unit cost per year

Page 4 of6

7/23/2019 2010 Paper BS E

http://slidepdf.com/reader/full/2010-paper-bs-e 8/8

SECTION B FIN AN CIA L A N D C OS T A CC OU NT IN G

MN3 4

Instructions to Candidates: Answer any three [03] questions from Section B. All questions

carry equal marks.

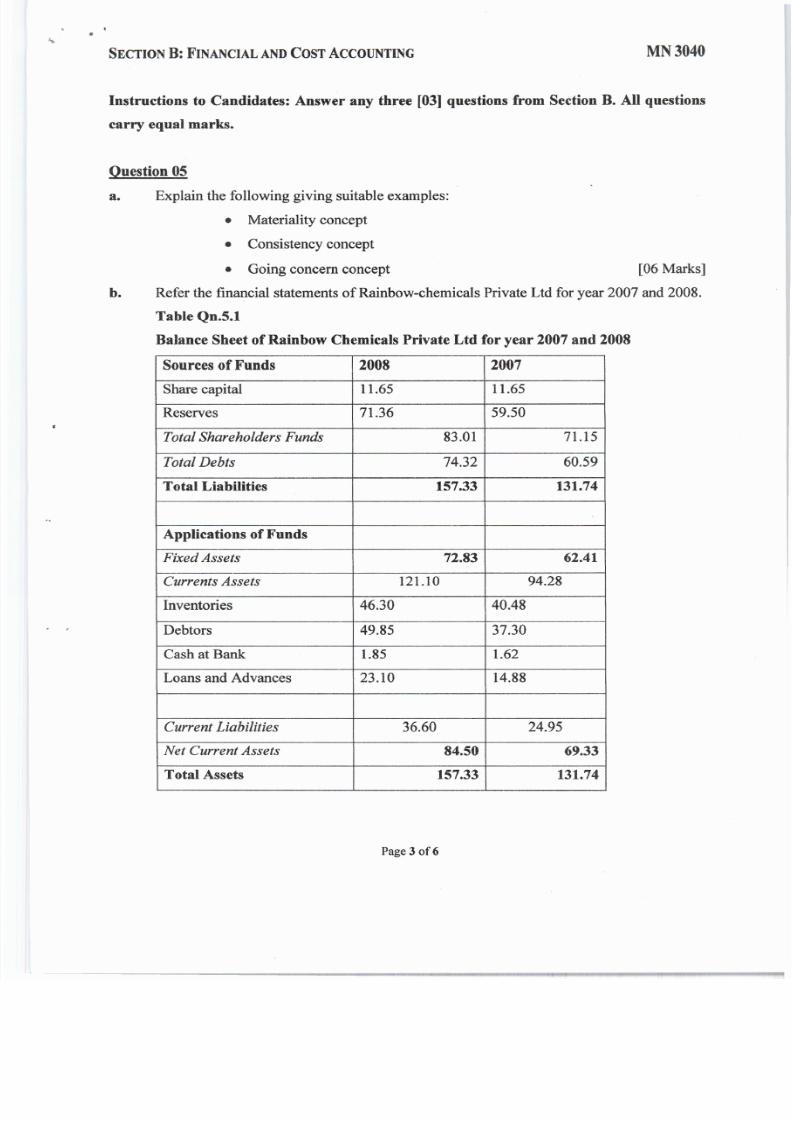

Question 05

a. Explain the following giving suitable examples:

• Materiality concept

• Consistency concept

• Going concern concept

[06 Marks]

b. Refer the financial statements of Rainbow-chemicals Private Ltd for year 2007 and 2008.

Table Qn.5.1

Balance Sheet of Rainbow Chemicals Private Ltd for year 2007 and 2008

Sources of Funds 2008

2007

Share capital

11.65

11.65

Reserves

71.36

59.50

Total Shareholders Funds

83.01

71.15

Total Debts

74.32

60.59

Total Liabilities 157.33

131.74

Applications of Funds

Fixed Assets

72.83

62.41

Currents Assets

121.10

94.28

Inventories

46.30 40.48

Debtors 49.85

37.30

Cash at Bank

1.85 1.62

Loans and Advances 23.10

14.88

Current Liabilities

36.60

24.95

Net Current Assets

84.50

69.33

Total Assets

157.33 131.74

Page 3 of6