2003 Report 2003 E_tcm21...H. H. Sheikh Jaber Al-Ahmad Al-Jaber Al-Sabah The Amir of the State of...

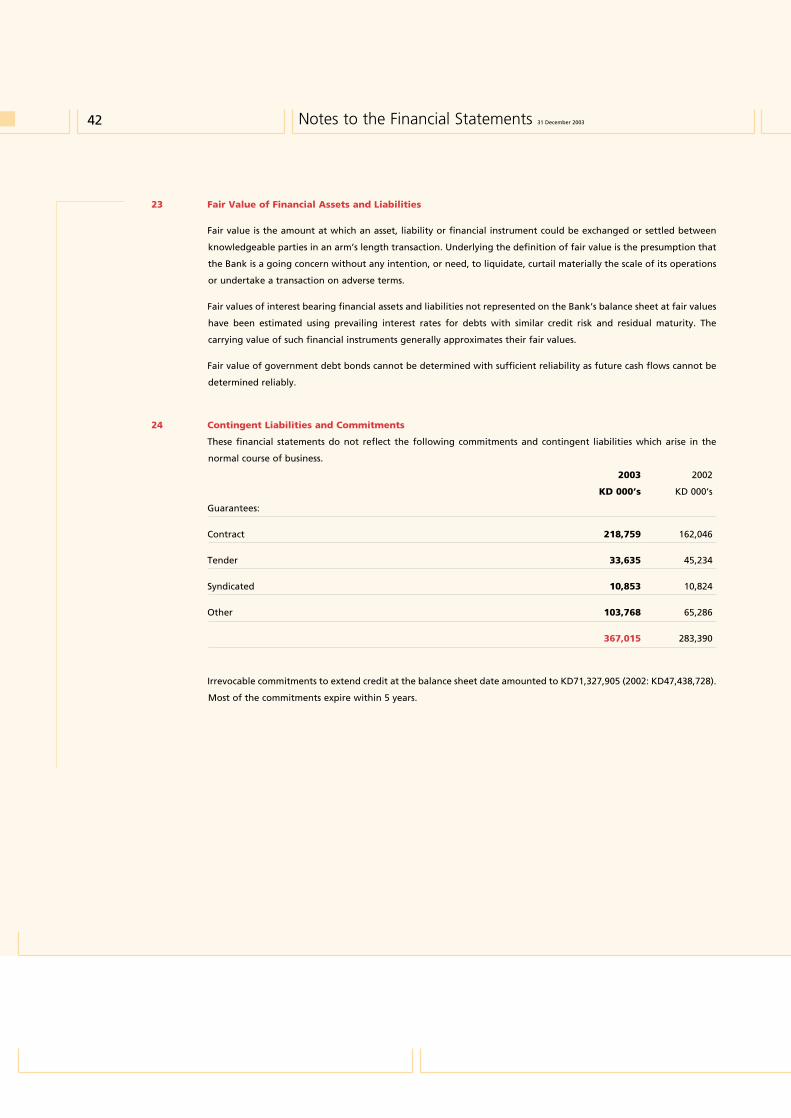

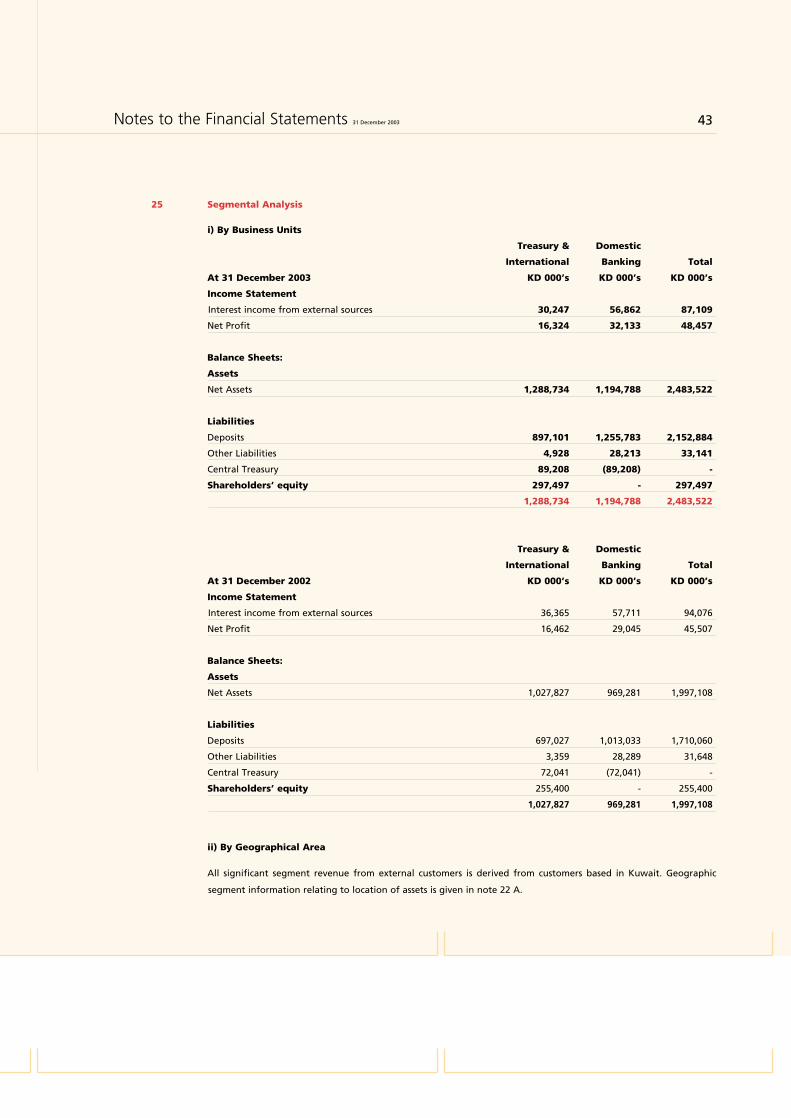

45

2003

-

Upload

duonghuong -

Category

Documents

-

view

227 -

download

0

Transcript of 2003 Report 2003 E_tcm21...H. H. Sheikh Jaber Al-Ahmad Al-Jaber Al-Sabah The Amir of the State of...

2003

H. H. Sheikh Jaber Al-Ahmad Al-Jaber Al-Sabah

The Amir of the State of Kuwait

H. H. Sheikh Sabah Al-Ahmad Al-Jaber Al-Sabah

The Prime Minister

H. H. Sheikh Saad Al-Abdallah Al-Salem Al-Sabah

The Crown Prince

AGQRƒdG ¢ù∏ée ¢ù«FQ ƒª°S

ìÉÑ°üdG ôHÉédG óªMC’G ìÉÑ°U ï«°ûdG¬∏dG ¬¶ØM

ó````¡©dG »```dh ƒ`````ª°S

ìÉÑ°üdG ⁄É°ùdG ¬∏dGóÑ©dG ó©°S ï«°ûdG¬∏dG ¬¶ØM

ƒª°ùdG ÖMÉ°U Iô°†M√ÉYQh ¬∏dG ¬¶ØM ìÉÑ°üdG ôHÉ÷G óªMC’G ôHÉL ï«°ûdG

ió`````تdG OÓ````ÑdG ô```«eCG

TAB

LE O

F C

ON

TEN

TS

CONTENTS

Financial Highlights

Board of Directors

Chairman's Message

Financial Review

Financial Statements

Auditors’ Report

Balance Sheet

Income Statement

Cash Flow Statement

Statement of Changes in Equity

Notes to the Financial Statements

02

03

04

09

17

18

19

20

21

22

23

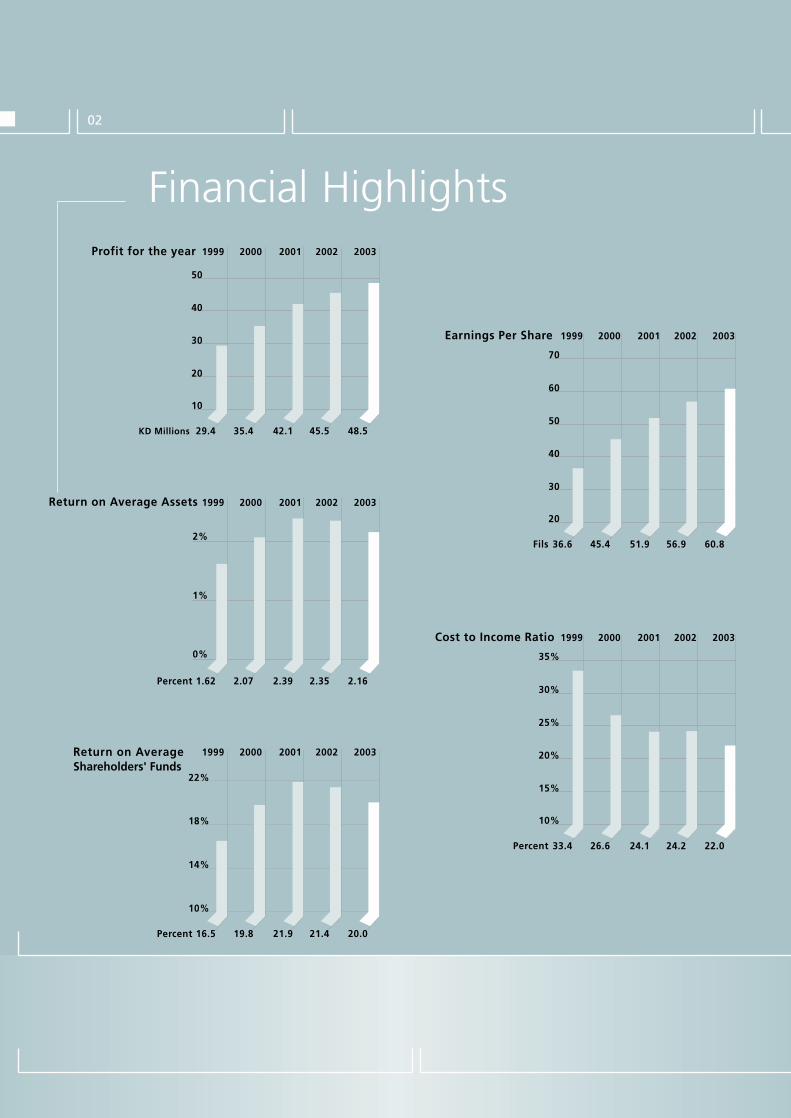

Financial Highlights

10

20

30

40

50

1999

29.4 35.4 42.1 45.5 48.5

2000 2001 2002 2003Profit for the year

KD Millions

0%

1%

2%

1999

1.62 2.07 2.39 2.35 2.16

2000 2001 2002 2003Return on Average Assets

Percent

10%

14%

18%

22%

1999

16.5 19.8 21.9 21.4 20.0

2000 2001 2002 2003Return on AverageShareholders' Funds

Percent

20

30

40

50

60

70

1999

36.6 45.4 51.9 56.9 60.8

2000 2001 2002 2003Earnings Per Share

Fils

10%

15%

20%

25%

30%

35%

1999

33.4 26.6 24.1 24.2 22.0

2000 2001 2002 2003Cost to Income Ratio

Percent

02

BO

AR

D O

F D

IREC

TOR

S

DIRECTORS

Bassam Yusuf Alghanim

Chairman & Managing Director

Salah Khaled Al-Fulaij

Deputy Chairman

Board Members

Adel Mohammed Rida Behbehani

Abdul Aziz Abdul Rahman Al-Shaya

Abdulkareem Abdulla Al-Saeed

Hussain Ahmed Qabazard

Khaled Saoud Al-Hasan

Naser Yousef Bourisli

Faisal Saoud Al-Fozan

03

Chairman’s MessageIn 2003 Gulf Bank surmounted

unprecedented regional and economic

challenges to its growth strategy and

delivered its fourth year of uninterrupted

profit and core business growth. There is

little doubt that Phase 1 of the Bank’s

“Transformation Strategy” has ensured that

the Bank has the collective skills,

commitment, vision, passion and customer

focus to transform this good Bank into a

truly great one. Following four years of

substantial investment in its staff, branches,

core banking systems and customer delivery

channels, 2003 was a benchmark year in

which the Bank embarked on the utilization

of this investment to produce superior

customer acquisition programs, customer

service, and customer retention initiatives.

Our strategy has been, and continues to be,

that exceptional shareholder value will be

generated through superior customer focus.

The Bank continued its market leading

profit growth, uninterrupted for four years,

and produced record net profits of KD 48.5

million in 2003 (US$ 164.4 million). Net

profits grew by 6.5% over 2002 and

Earnings Per Share increased by 7% to 60.8

fils. Return on Assets remained strong, at

2.16%, inspite of the severe business

disruption caused as a result of military

activity in Iraq, the very low interest rate

environment and intense local market price

competition. The Bank has upgraded and,

or replaced all of its major systems. The

resulting operational improvements,

enhanced customer service level and real

benefits produced by the Bank harnessing

the benefits of its substantial IT

investments, has been instrumental in

driving the Bank’s cost to income ratio

down to 22%, the best in Kuwait. This ratio

has continued to improve in spite of

continued investment in new branches and

the branch refurbishment program, further

enhancements to the Bank’s IT systems and

substantial investment in recruiting and

upskilling the brightest and best people for

our business. Enormous progress has been

made in strengthening Gulf Bank’s Brand

franchise, both in Retail and Corporate

Banking, and independent research

confirms that the Bank’s image and broad

appeal continues to grow amongst its

target market.

The replacement of all of the Bank’s major

IT systems and IT infrastructure over the

past three years has made it the most

technologically advanced Bank. In 2003, in

04

“ Gulf Bank... delivered its fourth year of

uninterrupted profit and core business growth ”“ ...the Bank has the collective skills, commitment,

vision, passion and customer focus to transform this

good Bank into a truly great one ”

excess of 83% of Gulf Bank’s transactions were handled

electronically. The substantial investment made in IT

infrastructure, systems and communications has given the

Bank a distinct competitive advantage. The Bank’s new

customer oriented IT systems coupled with simplification of

work practices has eliminated unnecessary or redundant

processes, resulting in efficient utilization of all resources, and

has made it a more efficient, flexible, innovative and

fundamentally profitable Bank. With our customer focused

strategy in place we are ideally positioned to utilize these

enabling technologies to further differentiate the Bank’s

service, product delivery, and further improve customer

satisfaction in the future.

Gulf Bank received Global Finance’s award for “Kuwait’s Best

Bank” in 2003. During the year further improvements were

made to the Retail Branch network. These major stand-alone

branches were constructed and opened, two of which replaced

smaller or older structures and two drive-thru ATMs were

installed at these locations. In addition, several refurbishment

projects were undertaken to align the existing branch network

with the Bank’s award winning Retail Banking branch format.

The Bank’s 24 / 7 self-service branch lobby program was further

expanded and enhanced, and included the introduction of

automated self-service check and cash lodgment facilities. The

Bank’s mobile phone messaging service (SMS) was further

expanded during the year to add Kuwait’s second major

mobile phone network. The Bank’s service now covers all

mobile phone users in Kuwait. Usage of the Bank’s internet

banking service (e-gulfbank.com) continued to grow and a

new Arabic version of the Bank’s web page was introduced at

the end of 2003. The Bank’s 24 / 7 telephone banking service

“805 805” remains the most frequented enquiry service at the

Bank. Service levels at our Telebanking service are among the

best in the region and considerably the best in Kuwait.

The Al Afdal customer salary program was augmented by the

Al Khaleej customer salary program in 2003. Both of these

complementary programs are designed to offer Kuwaiti

customers a total banking relationship. The features of both

product packages are aligned to the customers’ income level

and both programs have been supported with innovative

marketing and sales activities throughout the year. The Bank

remains the only Bank in Kuwait with a US$ 1 million prize

account “Al Danah”, which continues to be very popular. In

response to regulatory changes regarding the payment of low

income expatriate salaries, Gulf Bank in coordination with

other local banks, introduced the Al Amil program in late 2003.

Several innovative marketing programs were run throughout

2003, notably the Gulf Rewards Credit Card Discount Program

which was designed to promote credit card usage. This

program is the broadest and largest credit card discount

program in Kuwait and includes partners from major

international and local groups including airlines, hotels,

fashion retailers and health clinics. The Bank also introduced a

co-branded credit card with Kuwait National Petroleum

Company (KNPC). Gulf Bank remains the only Kuwaiti Bank to

operate and manage co-branded credit card programs.

05

“ The replacement of all of the Bank’s major IT systems and IT

infrastructure over the past three years has made it the most

technologically advanced Bank ” “ In 2003, in excess of 83% of Gulf Bank’s

transactions were handled electronically ”

Chairman’s Message continued...

The customer is at the center of all we do. During the military

conflict in the first half of 2003, Gulf Bank provided 7 day

branch services to key clients in order to expedite important

trade during this period, and Gulf Bank was the only Kuwaiti

Bank not to reduce its customer opening hours during the

conflict. The dedication and determination of Gulf Bank’s staff

embodied the passion and spirit of the Bank’s customer

commitment. Customer satisfaction with the Bank’s customer

care programs continues to remain high and the Bank remains

vigilant of the need to continuously monitor and enhance

service levels in order to be the ‘Best’.

Unparalleled speed of decision making, innovativeness and

flexibility in creating the best financial solution for the client

and unrivaled professionalism in service delivery are the prime

reasons why Gulf Bank’s Corporate Banking Group is known as

the ”Businessman’s Bank”. In a year which witnessed modest

industry growth during the first half of 2003, the Bank’s

Corporate Banking Group produced record results for

customer growth, business volumes and profitability. The

continued popularity of Gulf Bank amongst major business

clients in Kuwait has been driven by the Bank’s “total

relationship” approach to dealing with the customers’ needs,

and the timely response to customer needs. Benefits from the

substantial investments in new systems and upskilling of the

staff servicing our business clients has helped the Bank

broaden the scope and size of current relationships and

penetrate new client sectors with its innovative product and

service programs, as well as continuously improving the quality

of the assets. The Credit Control process is second to none. The

Bank continues to enjoy the reputation as the “Businessman’s

Bank” because of our customer focus and commitment.

The Bank’s Treasury Unit received a ”state-of-the-art” Dealing

Room in 2003 with greatly enhanced functionality, cost

structure and controls. The ergonomic design addresses the

extended service hours and specialization within the Unit. The

Bank introduced a range of new products including Derivatives

and Options, in addition to supporting its current portfolio of

FX and Hedges which it continues to market to clients. Gulf

Bank’s Dealing and Treasury Services are available to customers

over a six-day working week, and the Bank provides clients

with extended trading hours, in order to cover their trading

needs in Europe and the US. The Treasury Services continue to

proactively provide customers with advice and support, much

needed in spite of the Kuwaiti Dinar – US Dollar pegging

announced in January 2003. This pegging did not eliminate

exchange risk from Dinar / Dollar activity and Gulf Bank’s

Treasury Team were ideally positioned to provide clients with

the appropriate trading advice in order to cover their business

needs in 2003.

Kuwait’s two largest capital projects in 2003 were arranged by

Gulf Bank. The Siemens AG MEW – Al Zour Gas Turbine Power

Plant Project and the LG Engineering and Construction / KNPC

– Onstream Catalyst Replacement Revamp Project were both

arranged by the Bank’s International Division. This team of

business professionals is focused on the specific needs of

multinational corporate clients, oil sector clients, and financial

institutions. Despite disruption to international trade business

06 Chairman’s Message continued...

“ Gulf Bank was the only Kuwaiti Bank not to reduce

its customer opening hours during the conflict ”

“ Unparalleled speed of decision making,

innovativeness and flexibility... are prime reasons

why Gulf Bank’s Corporate Banking Group is known

as the “Businessman’s Bank” ”

during the first half of 2003, the International Division

experienced strong growth in its customer business and

dealings from international and regional banks.

The Bank issued its first Floating Rate Note (FRN) Eurobond in

October 2003. The Note, substantially over-subscribed, was the

first from a regional bank for a 5-year period and the Bank

closed subscriptions at US$ 200 million. The FRN was arranged

by JP Morgan and Morgan Stanley and given Gulf Bank’s

reputation, both regionally and internationally, the issue “sold

itself” according to JP Morgan.

At Gulf Bank, our people are at the heart of our strategy. We

believe that it is through our talented staff that we can truly

differentiate our unique brand of service and customer care.

Gulf Bank is notable for creating and sustaining a “high

performance” culture. This culture is one that attracts and

retains the brightest and most talented people, ensures that

managers have the skills and abilities to truly lead and where

everyone lives and practices the customer focus for which we

have become known for. In 2003, Gulf Bank recruited more

Kuwaiti graduates than any other Bank in Kuwait. The Bank is

committed to providing an environment in which ambitious

high performers can excel and establishing a succession

program which perpetuates the Bank’s drive for continued

success.

Gulf Bank continues to have the lowest level of Government

Debt Bonds in the Kuwaiti Banking sector. Although the

Bank’s level of Debt Bonds is minimal, this was further reduced

by 50% during 2003 and now stands at just 0.6% of total

assets. The benefit of having such a low level of Government

Debt Bonds is that it allows the Bank to utilize its assets in

more productive, long term and higher yielding customer

business.

For Gulf Bank, 2003 was a benchmark year in which it

concluded Phase 1 of its “Transformation Strategy” and

commenced Phase II - the “Actualization Strategy”. It is

uniquely positioned to benefit from its investment in

technology, branches and people and is now poised to

orchestrate its technologically advanced resources more fully

in order to provide faster, more innovative, customer friendly

and cost efficient solutions to customers. Through its customer

promise Gulf Bank will continue to grow and produce

exceptional shareholder value for the future.

I thank our Customers, Employees and Shareholders for their

business, loyalty and dedication.

Bassam Yusuf Alghanim

Chairman & Managing Director

07Chairman’s Message continued...

“ The Bank issued its first Floating Rate Note

(FRN) Eurobond in October 2003 ”“ Through its customer promise Gulf Bank will

continue to grow and produce exceptional

shareholder value for the future ”

08

FIN

AN

CIA

L R

EVIE

W

REVIEW

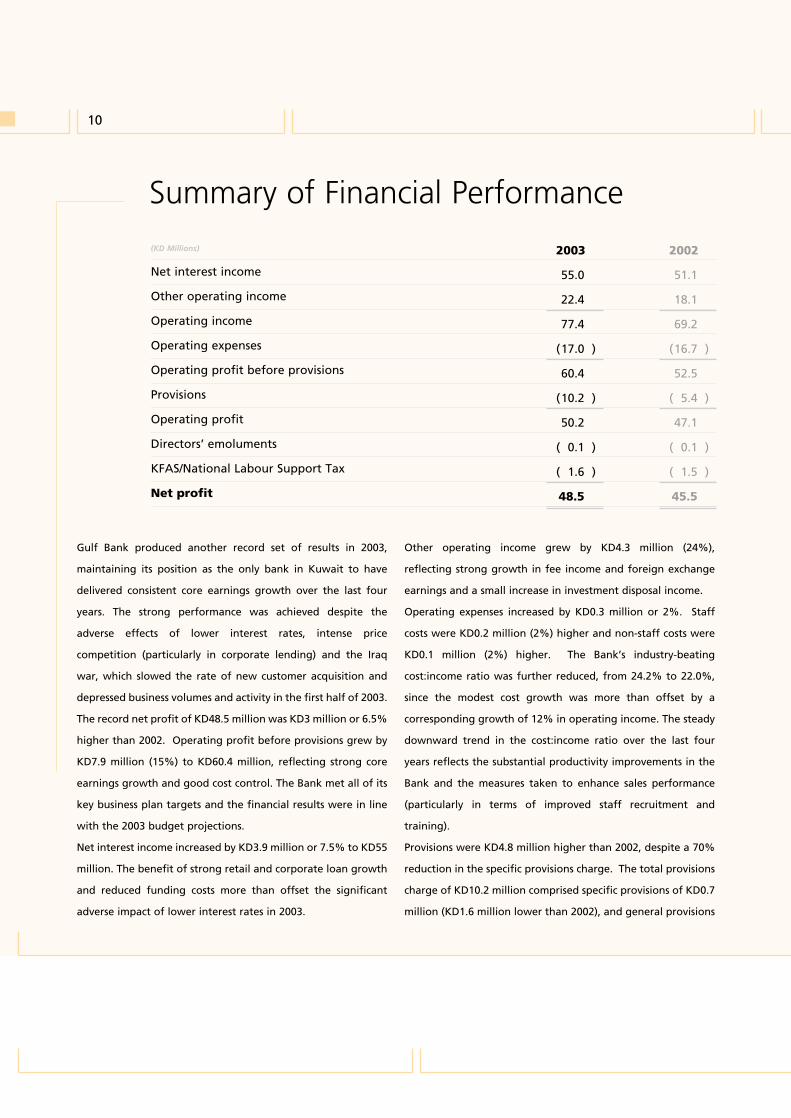

Summary of Financial Performance

Net Interest Income

Other Operating Income

Operating Expenses

Provisions

Balance Sheet Analysis

Bank Ratings

09

Summary of Financial Performance

Gulf Bank produced another record set of results in 2003,

maintaining its position as the only bank in Kuwait to have

delivered consistent core earnings growth over the last four

years. The strong performance was achieved despite the

adverse effects of lower interest rates, intense price

competition (particularly in corporate lending) and the Iraq

war, which slowed the rate of new customer acquisition and

depressed business volumes and activity in the first half of 2003.

The record net profit of KD48.5 million was KD3 million or 6.5%

higher than 2002. Operating profit before provisions grew by

KD7.9 million (15%) to KD60.4 million, reflecting strong core

earnings growth and good cost control. The Bank met all of its

key business plan targets and the financial results were in line

with the 2003 budget projections.

Net interest income increased by KD3.9 million or 7.5% to KD55

million. The benefit of strong retail and corporate loan growth

and reduced funding costs more than offset the significant

adverse impact of lower interest rates in 2003.

Other operating income grew by KD4.3 million (24%),

reflecting strong growth in fee income and foreign exchange

earnings and a small increase in investment disposal income.

Operating expenses increased by KD0.3 million or 2%. Staff

costs were KD0.2 million (2%) higher and non-staff costs were

KD0.1 million (2%) higher. The Bank’s industry-beating

cost:income ratio was further reduced, from 24.2% to 22.0%,

since the modest cost growth was more than offset by a

corresponding growth of 12% in operating income. The steady

downward trend in the cost:income ratio over the last four

years reflects the substantial productivity improvements in the

Bank and the measures taken to enhance sales performance

(particularly in terms of improved staff recruitment and

training).

Provisions were KD4.8 million higher than 2002, despite a 70%

reduction in the specific provisions charge. The total provisions

charge of KD10.2 million comprised specific provisions of KD0.7

million (KD1.6 million lower than 2002), and general provisions

10

(KD Millions)

Net interest income

Other operating income

Operating income

Operating expenses

Operating profit before provisions

Provisions

Operating profit

Directors’ emoluments

KFAS/National Labour Support Tax

Net profit

2003

55.0

22.4

77.4

(17.0 )

60.4

(10.2 )

50.2

( 0.1 )

( 1.6 )

48.5

2002

51.1

18.1

69.2

(16.7 )

52.5

( 5.4 )

47.1

( 0.1 )

( 1.5 )

45.5

Summary of Financial Performance continued...

Net Interest Income

Other Operating Income

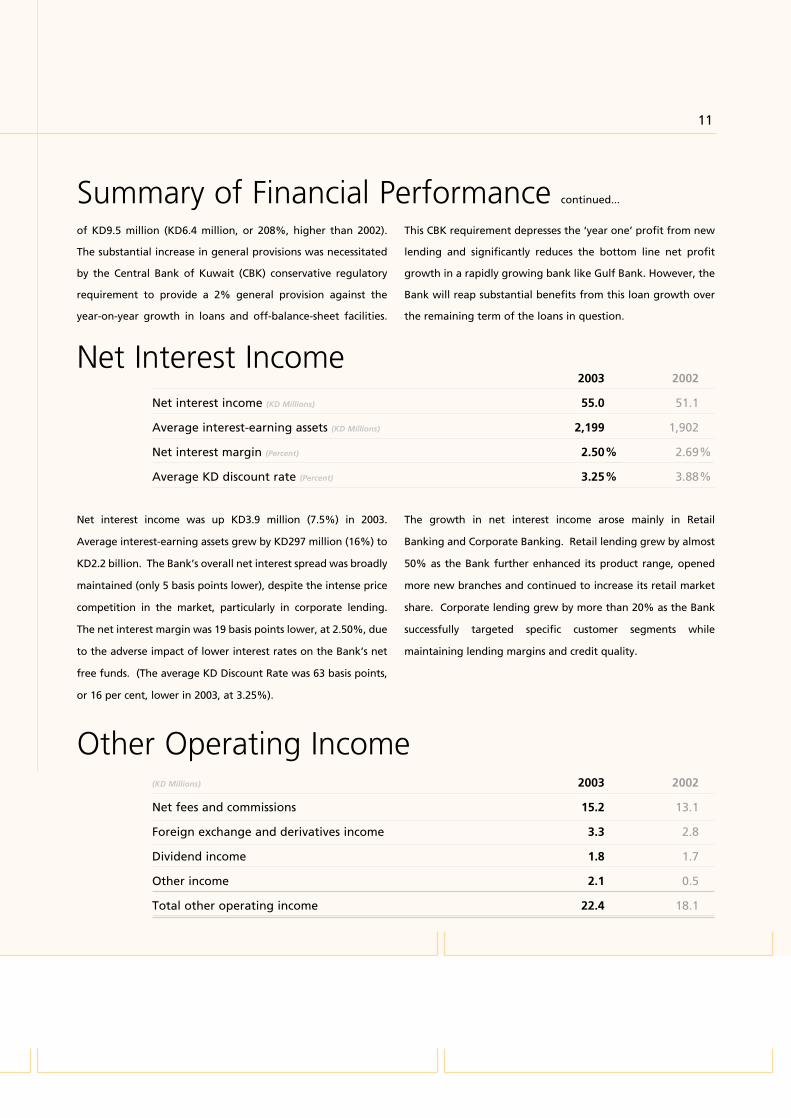

Net interest income was up KD3.9 million (7.5%) in 2003.

Average interest-earning assets grew by KD297 million (16%) to

KD2.2 billion. The Bank’s overall net interest spread was broadly

maintained (only 5 basis points lower), despite the intense price

competition in the market, particularly in corporate lending.

The net interest margin was 19 basis points lower, at 2.50%, due

to the adverse impact of lower interest rates on the Bank’s net

free funds. (The average KD Discount Rate was 63 basis points,

or 16 per cent, lower in 2003, at 3.25%).

The growth in net interest income arose mainly in Retail

Banking and Corporate Banking. Retail lending grew by almost

50% as the Bank further enhanced its product range, opened

more new branches and continued to increase its retail market

share. Corporate lending grew by more than 20% as the Bank

successfully targeted specific customer segments while

maintaining lending margins and credit quality.

of KD9.5 million (KD6.4 million, or 208%, higher than 2002).

The substantial increase in general provisions was necessitated

by the Central Bank of Kuwait (CBK) conservative regulatory

requirement to provide a 2% general provision against the

year-on-year growth in loans and off-balance-sheet facilities.

This CBK requirement depresses the ‘year one’ profit from new

lending and significantly reduces the bottom line net profit

growth in a rapidly growing bank like Gulf Bank. However, the

Bank will reap substantial benefits from this loan growth over

the remaining term of the loans in question.

11

2003 2002

Net interest income (KD Millions) 55.0 51.1

Average interest-earning assets (KD Millions) 2,199 1,902

Net interest margin (Percent) 2.50 2.69

Average KD discount rate (Percent) 3.25 3.88

(KD Millions) 2003 2002

Net fees and commissions 15.2 13.1

Foreign exchange and derivatives income 3.3 2.8

Dividend income 1.8 1.7

Other income 2.1 0.5

Total other operating income 22.4 18.1

%

%

%

%

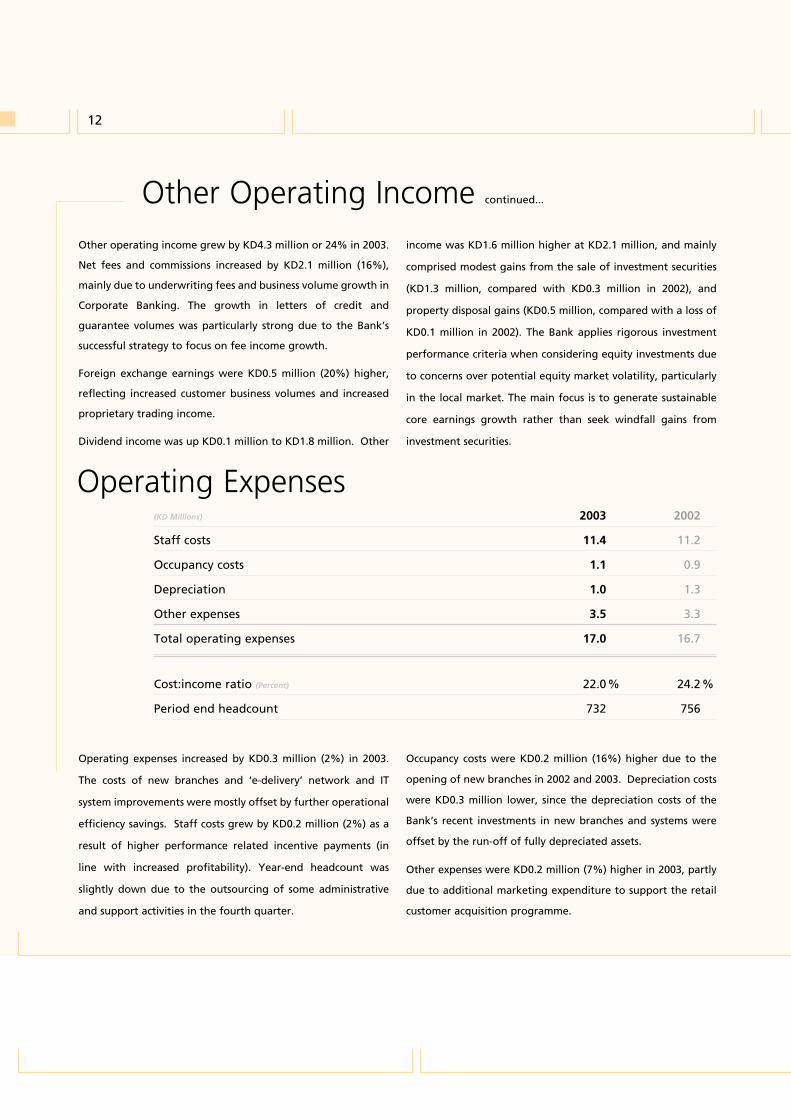

Other Operating Income continued...

Operating Expenses

Other operating income grew by KD4.3 million or 24% in 2003.

Net fees and commissions increased by KD2.1 million (16%),

mainly due to underwriting fees and business volume growth in

Corporate Banking. The growth in letters of credit and

guarantee volumes was particularly strong due to the Bank’s

successful strategy to focus on fee income growth.

Foreign exchange earnings were KD0.5 million (20%) higher,

reflecting increased customer business volumes and increased

proprietary trading income.

Dividend income was up KD0.1 million to KD1.8 million. Other

income was KD1.6 million higher at KD2.1 million, and mainly

comprised modest gains from the sale of investment securities

(KD1.3 million, compared with KD0.3 million in 2002), and

property disposal gains (KD0.5 million, compared with a loss of

KD0.1 million in 2002). The Bank applies rigorous investment

performance criteria when considering equity investments due

to concerns over potential equity market volatility, particularly

in the local market. The main focus is to generate sustainable

core earnings growth rather than seek windfall gains from

investment securities.

Operating expenses increased by KD0.3 million (2%) in 2003.

The costs of new branches and ‘e-delivery’ network and IT

system improvements were mostly offset by further operational

efficiency savings. Staff costs grew by KD0.2 million (2%) as a

result of higher performance related incentive payments (in

line with increased profitability). Year-end headcount was

slightly down due to the outsourcing of some administrative

and support activities in the fourth quarter.

Occupancy costs were KD0.2 million (16%) higher due to the

opening of new branches in 2002 and 2003. Depreciation costs

were KD0.3 million lower, since the depreciation costs of the

Bank’s recent investments in new branches and systems were

offset by the run-off of fully depreciated assets.

Other expenses were KD0.2 million (7%) higher in 2003, partly

due to additional marketing expenditure to support the retail

customer acquisition programme.

12

(KD Millions) 2003 2002

Staff costs 11.4 11.2

Occupancy costs 1.1 0.9

Depreciation 1.0 1.3

Other expenses 3.5 3.3

Total operating expenses 17.0 16.7

Cost:income ratio (Percent) 22.0% 24.2%

Period end headcount 732 756

Operating Expenses continued...

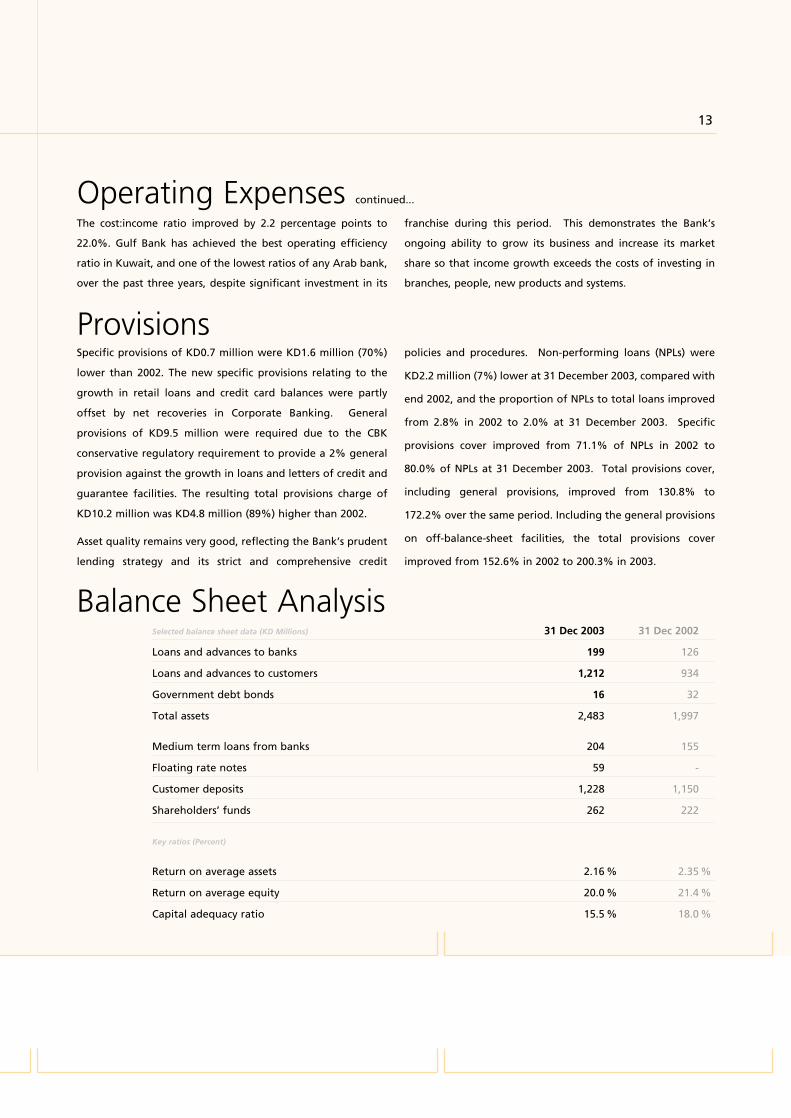

Provisions

Balance Sheet Analysis

The cost:income ratio improved by 2.2 percentage points to

22.0%. Gulf Bank has achieved the best operating efficiency

ratio in Kuwait, and one of the lowest ratios of any Arab bank,

over the past three years, despite significant investment in its

franchise during this period. This demonstrates the Bank’s

ongoing ability to grow its business and increase its market

share so that income growth exceeds the costs of investing in

branches, people, new products and systems.

Specific provisions of KD0.7 million were KD1.6 million (70%)

lower than 2002. The new specific provisions relating to the

growth in retail loans and credit card balances were partly

offset by net recoveries in Corporate Banking. General

provisions of KD9.5 million were required due to the CBK

conservative regulatory requirement to provide a 2% general

provision against the growth in loans and letters of credit and

guarantee facilities. The resulting total provisions charge of

KD10.2 million was KD4.8 million (89%) higher than 2002.

Asset quality remains very good, reflecting the Bank’s prudent

lending strategy and its strict and comprehensive credit

policies and procedures. Non-performing loans (NPLs) were

KD2.2 million (7%) lower at 31 December 2003, compared with

end 2002, and the proportion of NPLs to total loans improved

from 2.8% in 2002 to 2.0% at 31 December 2003. Specific

provisions cover improved from 71.1% of NPLs in 2002 to

80.0% of NPLs at 31 December 2003. Total provisions cover,

including general provisions, improved from 130.8% to

172.2% over the same period. Including the general provisions

on off-balance-sheet facilities, the total provisions cover

improved from 152.6% in 2002 to 200.3% in 2003.

13

Selected balance sheet data (KD Millions) 31 Dec 2003 31 Dec 2002

Loans and advances to banks 199 126

Loans and advances to customers 1,212 934

Government debt bonds 16 32

Total assets 2,483 1,997

Medium term loans from banks 204 155

Floating rate notes 59 -

Customer deposits 1,228 1,150

Shareholders’ funds 262 222

Key ratios (Percent)

Return on average assets 2.16 % 2.35 %

Return on average equity 20.0 % 21.4 %

Capital adequacy ratio 15.5 % 18.0 %

Balance Sheet Analysis continued...

Total assets increased by KD486 million or 24% to KD2.5 billion

at 31 December 2003. Almost 57% of the balance sheet was

deployed in loans and advances, compared with 53% at

31 December 2002.

Loans and advances to banks rose by KD73 million (57%) to

KD199 million. The increase reflected the granting of a

medium term loan to another Kuwaiti bank and the

resumption of new US dollar lending to international banks

following the end of the war in Iraq.

Loans and advances to customers increased by KD278 million

(30%), reflecting the strong, but prudent and strictly controlled

growth in retail and corporate lending.

Government debt bonds reduced by KD16 million (50%), falling

from 1.6% of total assets at end 2002 to 0.6% of total assets at

31 December 2003. Gulf Bank continues to benefit from having

achieved the lowest ratio of these low yielding assets of any

bank in Kuwait.

Medium term loans from banks (MTL) were increased to KD204

million to provide additional long term, stable funding for the

growth in retail lending. This MTL funding comprises 3 and 5

year KD and US dollar loans from other Kuwaiti banks.

Further long term funding was provided by the 5 year USD200

million floating rate note (FRN) Eurobond (due October 2008)

issued by the Bank in October 2003. The FRN marked Gulf

Bank’s inaugural bond transaction in the capital markets and

was priced at 65 basis points over USD 3 month Libor, in line

with the secondary market level of comparable regional credits.

The bond was 1.5 times oversubscribed, with strong demand

from a diversified investor base in Europe and Asia, as well as

the Middle East. It was the first ever 5 year USD bond issued by

a commercial bank in Kuwait and was the first international

financing from Kuwait following the end of the war in Iraq.

Customer deposits increased by KD78 million (7%) to KD1,228

million, and there was a substantial improvement in the deposit

mix. Current account balances grew by 22% and there was a

significant reduction in higher cost, ‘hot money’ time deposits

in Treasury and Corporate Banking. The total requirement for

customer deposits was substantially reduced by the increased

use of MTL and FRN funding, which is a more efficient means of

funding retail loan growth.

Shareholders’ funds increased by KD40 million (18%) to KD262

million. The growth mainly reflects the sale of treasury shares

during 2003 (net effect of KD14 million), the increases in

retained earnings (up KD8 million) and statutory reserves (up

KD5 million), and an increase in the fair valuation reserve of

KD12 million. The Bank had unrealised gains on its ‘available

for sale’ financial assets of KD22.4 million at 31 December 2003.

The return on average assets declined by 19 basis points from

2.35% in 2002 to 2.16% in 2003. The adverse impact of lower

interest rates on the income from net free funds was partly

offset by the benefits of more efficient balance sheet utilisation

(through the increased use of MTL/FRN funding), lower funding

costs (due to lower interest rates and the improved mix of

customer deposits), and the successful maintenance of lending

spreads in the face of intense price competition in the market.

The return on average equity declined by 140 basis points (6%),

14

Balance Sheet Analysis continued...

Bank Ratings

from 21.4% to 20.0% in 2003, reflecting the substantial

increase in year-end equity: up KD40 million (18%), from KD222

million to KD262 million.

The capital adequacy ratio declined from 18.0% at end 2002 to

15.5% at 31 December 2003. The reduction was in line with the

Bank’s strategy to leverage its balance sheet and increase

profitable lending for the benefit of shareholders and

customers. The capital adequacy ratio remains well above the

CBK minimum ratio of 12.0% and leaves the Bank strongly

capitalised to support the continued expansion of its business

activities in 2004.

The Bank’s ratings (upgraded during 2002) were reaffirmed in

2003. The rating ‘outlook’ from Capital Intelligence was also

increased from ‘stable’ to ‘positive’. Gulf Bank is the second

highest rated bank in Kuwait, and received similarly favourable

ratings for the 5 year FRN issued in October 2003, namely: ‘A-‘

(Fitch Ratings) and ‘BBB+’ (Standard & Poor’s).

The strong ratings reflect the financial strength, good asset

quality, strong profit growth and well focused and effective

business strategy of Gulf Bank. The Bank continues to increase

its market share and build on its position as Kuwait’s second

largest bank, despite the increasing competition in the market.

15

Long-term foreign currency ratings 2003 2002

Fitch Ratings A- A-

Moody’s Investors Service A2 A2

Capital Intelligence A- A-

Standard & Poor’s BBB+ BBB+

16

FIN

AN

CIA

L ST

ATE

MEN

TS

STATEMENTS

Auditors’ Report to the Shareholders

Balance Sheet

Income Statement

Cash Flow Statement

Statement of Changes in Equity

Notes to the Financial Statements

17

Auditors’ Report to the Shareholders

Waleed A. Al OsaimiLicence No 68 AErnst & YoungAl Aiban, Al Osaimi & Partners

07 January 2004Kuwait

Bader A. Al-WazzanLicence No 62 APricewaterhouseCoopers

Ernst & Young, Al Aiban, Al Osaimi & Partners, P. O. Box 74, 13001 SafatPricewaterhouseCoopers, Bader & Co. P. O. Box 20174, 13062 Safat

We have audited the accompanying balance sheet of Gulf Bank

K.S.C as of 31 December 2003 and the related statements of

income, cash flows and changes in equity for the year then

ended. These financial statements are the responsibility of the

Bank's management. Our responsibility is to express an opinion

on these financial statements based on our audit.

We conducted our audit in accordance with International

Standards on Auditing. Those Standards require that we plan

and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material

misstatement. An audit includes examining, on a test basis,

evidence supporting the amounts and disclosures in the

financial statements. An audit also includes assessing the

accounting principles used and significant estimates made by

management, as well as evaluating the overall financial

statement presentation. We believe that our audit provides a

reasonable basis for our opinion.

In our opinion, the financial statements present fairly, in all

material respects, the financial position of the Bank as of 31

December 2003, the results of its operations, its cash flows and

changes in equity for the year then ended in accordance with

International Financial Reporting Standards.

Furthermore, in our opinion proper books of account have

been kept by the Bank and the financial statements, together

with the contents of the report of the Board of Directors

relating to these financial statements, are in accordance

therewith.

We further report that we obtained all the information and

explanations that we required for the purpose of our audit and

that the financial statements incorporate all information that is

required by the Commercial Companies Law of 1960, as

amended, and by the Bank's Articles of Association, that an

inventory was duly carried out and that, to the best of our

knowledge and belief, no violation of the Commercial

Companies Law of 1960, as amended, or of the Articles of

Association have occurred during the year ended 31 December

2003 that might have had a material effect on the business of

the Bank or on its financial position.

We further report that, during the course of our examination,

we have not become aware of any material violations of the

provisions of Law No. 32 of 1968, as amended, concerning

currency, the Central Bank of Kuwait and the organisation of

banking business, and its related regulations, during the year

ended 31 December 2003.

18

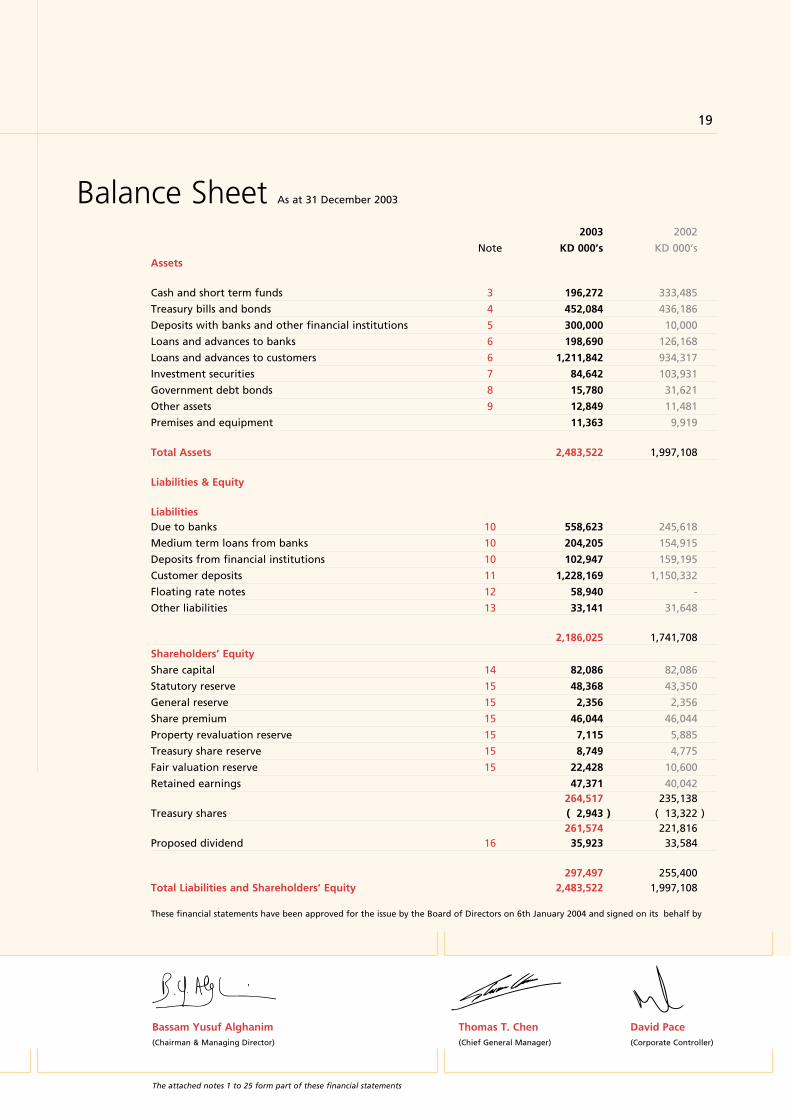

Balance Sheet As at 31 December 2003

Bassam Yusuf Alghanim(Chairman & Managing Director)

The attached notes 1 to 25 form part of these financial statements

Thomas T. Chen(Chief General Manager)

David Pace(Corporate Controller)

19

2003 2002

Note KD 000’s KD 000’sAssets

Cash and short term funds 3 196,272 333,485

Treasury bills and bonds 4 452,084 436,186

Deposits with banks and other financial institutions 5 300,000 10,000

Loans and advances to banks 6 198,690 126,168

Loans and advances to customers 6 1,211,842 934,317

Investment securities 7 84,642 103,931

Government debt bonds 8 15,780 31,621

Other assets 9 12,849 11,481

Premises and equipment 11,363 9,919

Total Assets 2,483,522 1,997,108

Liabilities & Equity

Liabilities Due to banks 10 558,623 245,618

Medium term loans from banks 10 204,205 154,915

Deposits from financial institutions 10 102,947 159,195

Customer deposits 11 1,228,169 1,150,332

Floating rate notes 12 58,940 -

Other liabilities 13 33,141 31,648

2,186,025 1,741,708

Shareholders’ Equity

Share capital 14 82,086 82,086

Statutory reserve 15 48,368 43,350

General reserve 15 2,356 2,356

Share premium 15 46,044 46,044

Property revaluation reserve 15 7,115 5,885

Treasury share reserve 15 8,749 4,775

Fair valuation reserve 15 22,428 10,600

Retained earnings 47,371 40,042264,517 235,138

Treasury shares ( 2,943 ) ( 13,322 )261,574 221,816

Proposed dividend 16 35,923 33,584

297,497 255,400Total Liabilities and Shareholders’ Equity 2,483,522 1,997,108

These financial statements have been approved for the issue by the Board of Directors on 6th January 2004 and signed on its behalf by

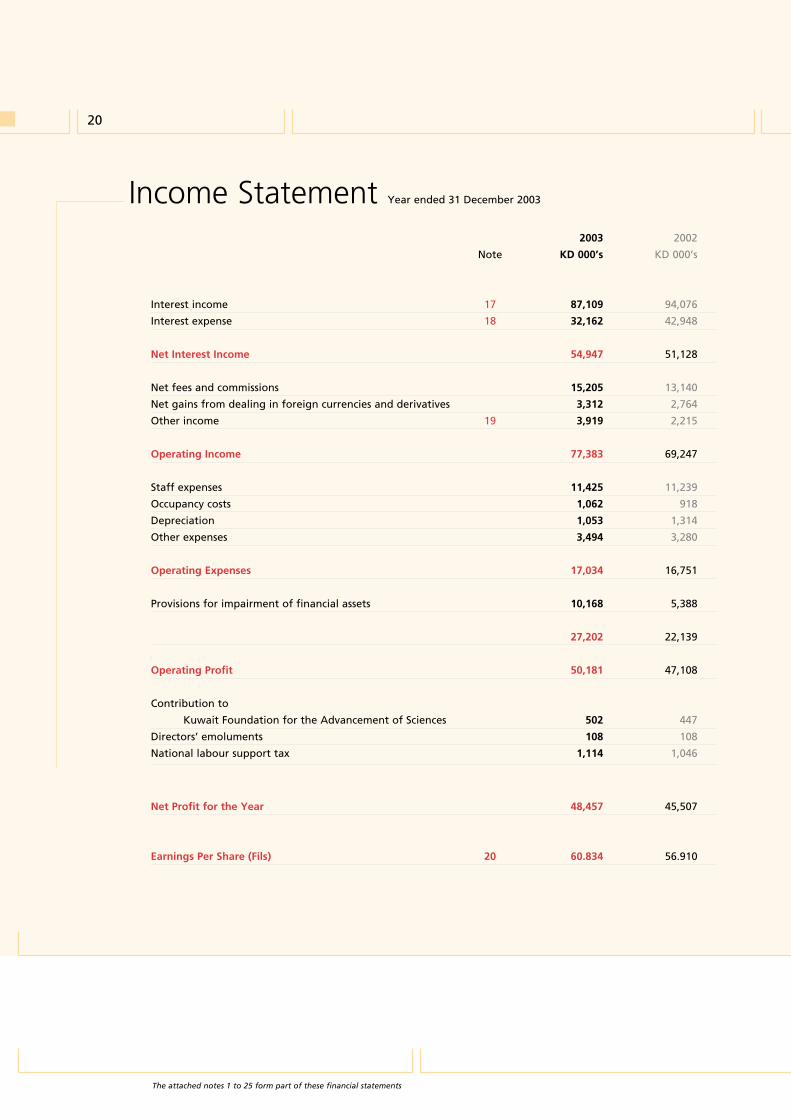

Income Statement Year ended 31 December 2003

20

2003 2002

Note KD 000’s KD 000’s

Interest income 17 87,109 94,076

Interest expense 18 32,162 42,948

Net Interest Income 54,947 51,128

Net fees and commissions 15,205 13,140

Net gains from dealing in foreign currencies and derivatives 3,312 2,764

Other income 19 3,919 2,215

Operating Income 77,383 69,247

Staff expenses 11,425 11,239

Occupancy costs 1,062 918

Depreciation 1,053 1,314

Other expenses 3,494 3,280

Operating Expenses 17,034 16,751

Provisions for impairment of financial assets 10,168 5,388

27,202 22,139

Operating Profit 50,181 47,108

Contribution to

Kuwait Foundation for the Advancement of Sciences 502 447

Directors’ emoluments 108 108

National labour support tax 1,114 1,046

Net Profit for the Year 48,457 45,507

Earnings Per Share (Fils) 20 60.834 56.910

The attached notes 1 to 25 form part of these financial statements

21

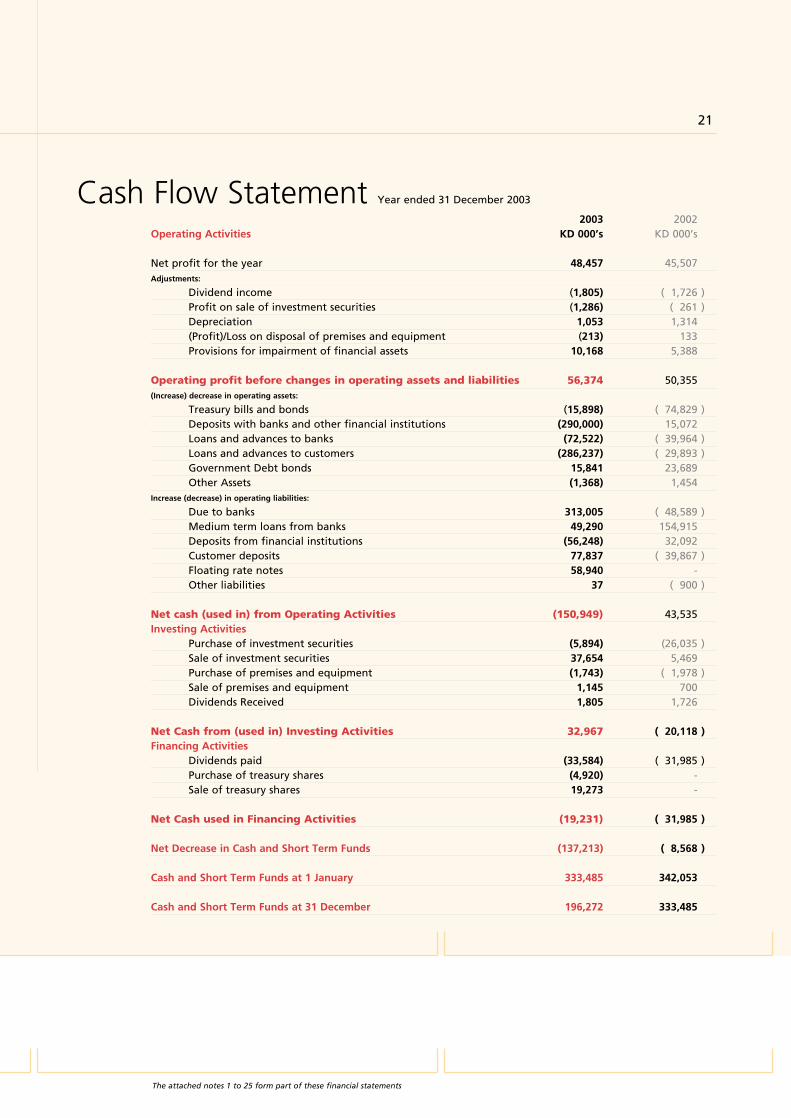

Cash Flow Statement Year ended 31 December 2003

2003 2002Operating Activities KD 000’s KD 000’s

Net profit for the year 48,457 45,507Adjustments:

Dividend income (1,805) ( 1,726 )Profit on sale of investment securities (1,286) ( 261 )Depreciation 1,053 1,314(Profit)/Loss on disposal of premises and equipment (213) 133Provisions for impairment of financial assets 10,168 5,388

Operating profit before changes in operating assets and liabilities 56,374 50,355(Increase) decrease in operating assets:

Treasury bills and bonds (15,898) ( 74,829 )Deposits with banks and other financial institutions (290,000) 15,072Loans and advances to banks (72,522) ( 39,964 )Loans and advances to customers (286,237) ( 29,893 )Government Debt bonds 15,841 23,689Other Assets (1,368) 1,454

Increase (decrease) in operating liabilities:

Due to banks 313,005 ( 48,589 )Medium term loans from banks 49,290 154,915Deposits from financial institutions (56,248) 32,092Customer deposits 77,837 ( 39,867 )Floating rate notes 58,940 -Other liabilities 37 ( 900 )

Net cash (used in) from Operating Activities (150,949) 43,535Investing Activities

Purchase of investment securities (5,894) (26,035 )Sale of investment securities 37,654 5,469Purchase of premises and equipment (1,743) ( 1,978 )Sale of premises and equipment 1,145 700Dividends Received 1,805 1,726

Net Cash from (used in) Investing Activities 32,967 ( 20,118 )Financing Activities

Dividends paid (33,584) ( 31,985 )Purchase of treasury shares (4,920) -Sale of treasury shares 19,273 -

Net Cash used in Financing Activities (19,231) ( 31,985 )

Net Decrease in Cash and Short Term Funds (137,213) ( 8,568 )

Cash and Short Term Funds at 1 January 333,485 342,053

Cash and Short Term Funds at 31 December 196,272 333,485

The attached notes 1 to 25 form part of these financial statements

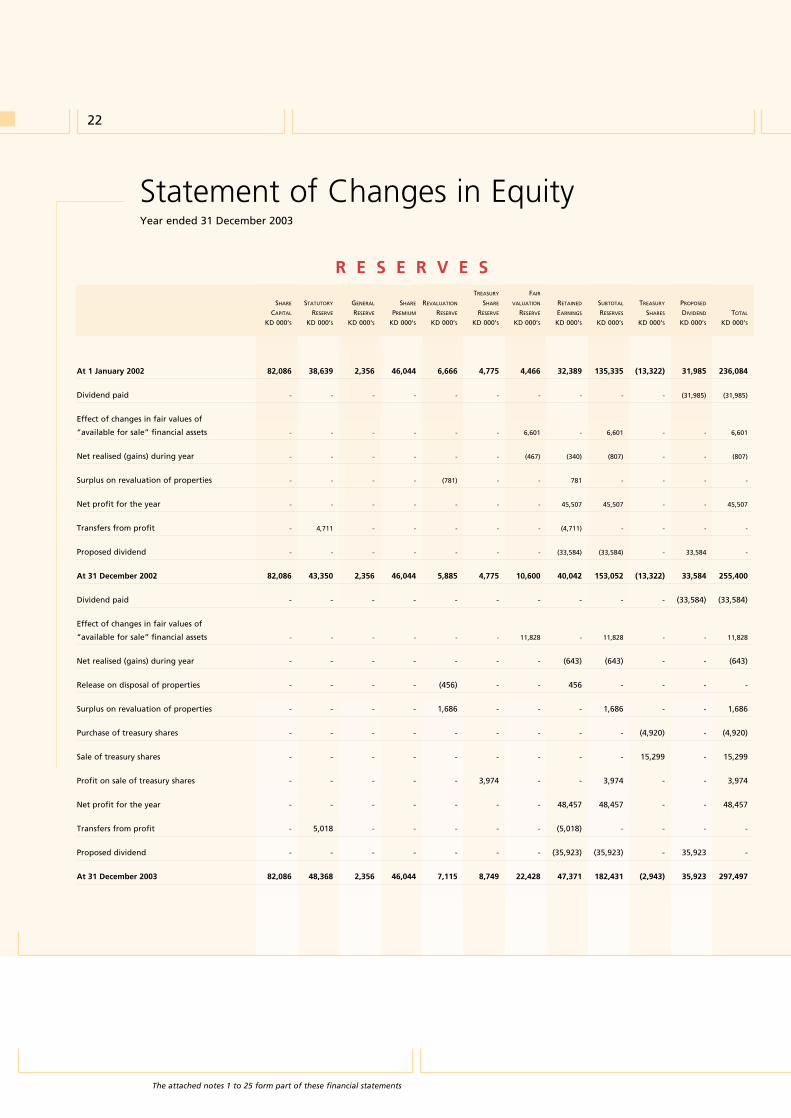

Statement of Changes in EquityYear ended 31 December 2003

22

TREASURY FAIR

SHARE STATUTORY GENERAL SHARE REVALUATION SHARE VALUATION RETAINED SUBTOTAL TREASURY PROPOSED

CAPITAL RESERVE RESERVE PREMIUM RESERVE RESERVE RESERVE EARNINGS RESERVES SHARES DIVIDEND TOTAL

KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S KD 000’S

At 1 January 2002 82,086 38,639 2,356 46,044 6,666 4,775 4,466 32,389 135,335 (13,322) 31,985 236,084

Dividend paid - - - - - - - - - - (31,985) (31,985)

Effect of changes in fair values of

“available for sale” financial assets - - - - - - 6,601 - 6,601 - - 6,601

Net realised (gains) during year - - - - - - (467) (340) (807) - - (807)

Surplus on revaluation of properties - - - - (781) - - 781 - - - -

Net profit for the year - - - - - - - 45,507 45,507 - - 45,507

Transfers from profit - 4,711 - - - - - (4,711) - - - -

Proposed dividend - - - - - - - (33,584) (33,584) - 33,584 -

At 31 December 2002 82,086 43,350 2,356 46,044 5,885 4,775 10,600 40,042 153,052 (13,322) 33,584 255,400

Dividend paid - - - - - - - - - - (33,584) (33,584)

Effect of changes in fair values of

“available for sale” financial assets - - - - - - 11,828 - 11,828 - - 11,828

Net realised (gains) during year - - - - - - - (643) (643) - - (643)

Release on disposal of properties - - - - (456) - - 456 - - - -

Surplus on revaluation of properties - - - - 1,686 - - - 1,686 - - 1,686

Purchase of treasury shares - - - - - - - - - (4,920) - (4,920)

Sale of treasury shares - - - - - - - - - 15,299 - 15,299

Profit on sale of treasury shares - - - - - 3,974 - - 3,974 - - 3,974

Net profit for the year - - - - - - - 48,457 48,457 - - 48,457

Transfers from profit - 5,018 - - - - - (5,018) - - - -

Proposed dividend - - - - - - - (35,923) (35,923) - 35,923 -

At 31 December 2003 82,086 48,368 2,356 46,044 7,115 8,749 22,428 47,371 182,431 (2,943) 35,923 297,497

R E S E R V E S

The attached notes 1 to 25 form part of these financial statements

23

Notes to the Financial Statements 31 December 2003

1. Incorporation and Registration

Gulf Bank K.S.C. is a public shareholding company incorporated in Kuwait on 29 October 1960 and is registered as a

bank with the Central Bank of Kuwait. Its registered office is at Mubarak Al Kabir Street, PO Box 3200, 13032 Safat,

Kuwait. The number of employees as of 31 December 2003 was 732 (2002:756).

2. Significant Accounting Policies

a) Basis of presentation

These financial statements have been prepared in conformity with International Financial Reporting Standards (IFRS)

and interpretations issued by the International Accounting Standards Board (IASB). The financial statements are

prepared under the historical cost basis of measurement as modified by the revaluation of financial assets held as

available for sale, all derivative contracts and land and buildings.

The financial statements have been presented in Kuwaiti Dinars rounded off to the nearest thousand.

b) Financial instruments

Classification, recognition/de-recognition and measurement of financial instruments

Classification

In accordance with IAS 39 the Bank classifies its financial assets as “held for trading”, “originated financial assets” and

“available for sale” and its financial liabilities as “non-trading financial liabilities’’.

“Held for trading” are those financial assets which are acquired principally for the purpose of generating a profit from

short term fluctuations in price. This includes derivative financial instruments.

Financial assets that are created by the Bank by providing money directly to a borrower are classified as “originated

financial assets”.

Financial assets which are not classified as above are classified as “available for sale”, and are principally those

acquired to be held for an indefinite period of time, which may be sold in response to needs for liquidity or changes

in interest rates or equity prices.

Financial liabilities, which are not held for trading, are classified as “non-trading financial liabilities”.

Management determines the classification of these financial instruments.

Recognition/de-recognition

A financial asset or a financial liability is recognised when the Bank becomes a party to the contractual provisions of

the instrument. A financial asset is de-recognised when the Bank loses control of the contractual rights that comprise

the financial asset and a financial liability is de-recognised when the obligation specified in the contract is discharged,

cancelled or expired.

All regular way purchases and sales of financial assets are recognised using settlement date accounting. Changes in

fair value between the trade date and settlement date are recognised in income. Regular way purchases or sales are

purchases or sales of financial assets that require delivery of assets within the time frame generally established by

regulations or conventions in the market place.

Derivatives with positive market values (unrealised gains) are recognised as other assets and derivatives with negative

market values (unrealised losses) are recognised as other liabilities in the balance sheet.

24

2 Significant Accounting Policies continued...

Measurement

All financial instruments are initially recognised at cost (which includes transaction costs).

On subsequent re-measurement, financial assets classified as “held for trading” are carried at fair value with resultant

unrealised gains or losses arising from changes in fair value included in income. “Originated financial assets” are

carried at amortised cost using the effective yield method, less any provision for impairment. Those classified as

“available for sale” are subsequently measured and carried at fair values. Unrealised gains and losses arising from

changes in fair value of those classified as “available for sale” are taken to fair valuation reserve in equity. “Non-

trading financial liabilities” are carried at amortised cost using the effective interest method.

When the “available for sale” asset is disposed of, or impaired, the related accumulated fair value adjustments are

transferred to the income statement as gains or losses.

Fair values

Fair values of quoted instruments are based on quoted closing bid prices or using the current market rate of interest

for that instrument. Fair values for unquoted instruments are estimated using applicable price/earnings or price/cash

flow ratios refined to reflect the specific circumstances of the issuer.

The fair value of a derivative is the equivalent of the unrealised gain or loss from marking to market the derivative

using prevailing market rates or internal pricing models.

Impairment

A financial asset is impaired if its carrying amount is greater than its estimated recoverable amount. An assessment

is made at each balance sheet date to determine whether there is objective evidence that a specific financial asset,

or a group of similar assets, may be impaired. If such evidence exists, the impairment loss is recognised in the income

statement.

Loans originated by the Bank are subject to credit risk provisions for loan impairment if there is objective evidence

that the Bank will not be able to collect all amounts due. The amount of provision is the difference between the

carrying amount and the recoverable amount, being the present value of expected future cash flows, including

amounts recoverable from guarantees and collateral, discounted based on the original effective interest rate.

The provision for impairment of loans and advances also covers losses where there is objective evidence that probable

losses are present in components of the loans and advances portfolio at the balance sheet date. These have been

estimated based on the historical patterns of losses in each component, the credit ratings allocated to the borrowers

and reflecting the current economic environment in which the borrowers operate.

Loans and advances are written off when there is no realistic prospect of recovery.

c) Provisions

Provisions are recognised when, as a result of past events, it is probable that an outflow of economic resources will

be required to settle a present, legal or constructive obligation and the amount can be reliably estimated.

d) Treasury shares

The cost of the Bank’s own shares purchased, including directly attributable costs, is recognised as a change in equity.

Gains or losses arising on sale are separately disclosed under shareholders’ equity and in accordance with the

instructions of Central Bank of Kuwait, these amounts are not available for distribution. These shares are not entitled

to any dividends.

Notes to the Financial Statements 31 December 2003

25

2 Significant Accounting Policies continued...

e) Revenue recognition

Interest receivable and payable are recognised on a time proportion basis taking account of the principal outstanding

and the rate applicable. Once a financial instrument categorised as “originated financial assets” is written down to

its estimated recoverable amount, interest income is thereafter recognised based on the rate of interest that was used

to discount the future cash flows for the purpose of measuring the recoverable amount. Other fees receivable or

payable including loan commitment fees are recognised when due. Dividend income is recognised when the right to

receive payment is established.

f) Fiduciary assets

Assets held in trust or in a fiduciary capacity are not treated as assets of the Bank and accordingly are not included in

these financial statements.

g) Foreign currencies

Foreign currency transactions are recorded at rates of exchange ruling at the dates of the transactions. Monetary

assets and liabilities in foreign currencies at the year end are translated into Kuwaiti Dinars at rates of exchange ruling

at the balance sheet date. Foreign exchange contracts outstanding at the year end are revalued at the forward rates

ruling at the balance sheet date. Any resultant gains or losses are taken to the income statement.

3 Cash and Short Term Funds 2003 2002KD 000’s KD 000’s

Balances with the Central Bank of Kuwait 137,100 287,029

Cash on hand and in current accounts with other banks 20,473 16,418

Money at call and short notice 3,704 12,960

Deposits with banks and other financial institutions maturing within one month 995 7,078

Certificates of deposit maturing within one month 34,000 10,000

196,272 333,485

Cash and short term funds consist of cash in hand and on current account with other banks together with money at

call and deposits with banks and other financial institutions maturing within one month.

The Bank classifies cash and short term funds as “originated financial assets”.

4 Treasury Bills and Bonds

These financial instruments are issued by the Central Bank of Kuwait on behalf of the Ministry of Finance. They

mature within a period not exceeding one year.2003 2002

KD 000’s KD 000’s

Treasury bills 163,122 197,429

Treasury bonds 288,962 238,757

452,084 436,186

The Bank classifies treasury bills and bonds as “originated financial assets”

Notes to the Financial Statements 31 December 2003

26

5 Deposits with Banks and Other Financial Institutions 2003 2002KD 000’s KD 000’s

Time deposits 5,000 -

Certificates of deposit 295,000 10,000

300,000 10,000

The Bank classifies deposits with banks and other financial institutions as “originated financial assets”

6 Loans and Advances to Banks and Customers

Loans and advances represent monies paid to banks and customers and the Bank classifies them as “originated

financial assets”. The Bank’s assessment of the credit risk concentration, based on the primary purpose of the loans

and advances given, is provided below.

At 31 December 2003

Loans and advances to customers

Other

Middle Western Asia Rest of

Kuwait East Europe Pacific World Total

KD 000’s KD 000’s KD 000’s KD 000’s KD 000’s KD 000’s

Personal 336,944 - - - - 336,944

Financial 117,650 17,897 12,231 1,213 14,265 163,256

Trade and commerce 227,426 4,980 - - - 232,406

Crude oil and gas 11,113 421 - - - 11,534

Construction 141,063 2,514 7 - - 143,584

Government - 5,640 - - 1,537 7,177

Others 70,887 4,432 - 747 - 76,066

Manufacturing 21,376 8,916 - - - 30,292

Real Estate 260,146 - - - - 260,146

1,186,605 44,800 12,238 1,960 15,802 1,261,405

Less: Provision for impairment (49,563)

1,211,842

Loans and advances to banks 70,689 33,958 27,367 44,671 22,281 198,966

Less: Provision for impairment (276)

198,690

Notes to the Financial Statements 31 December 2003

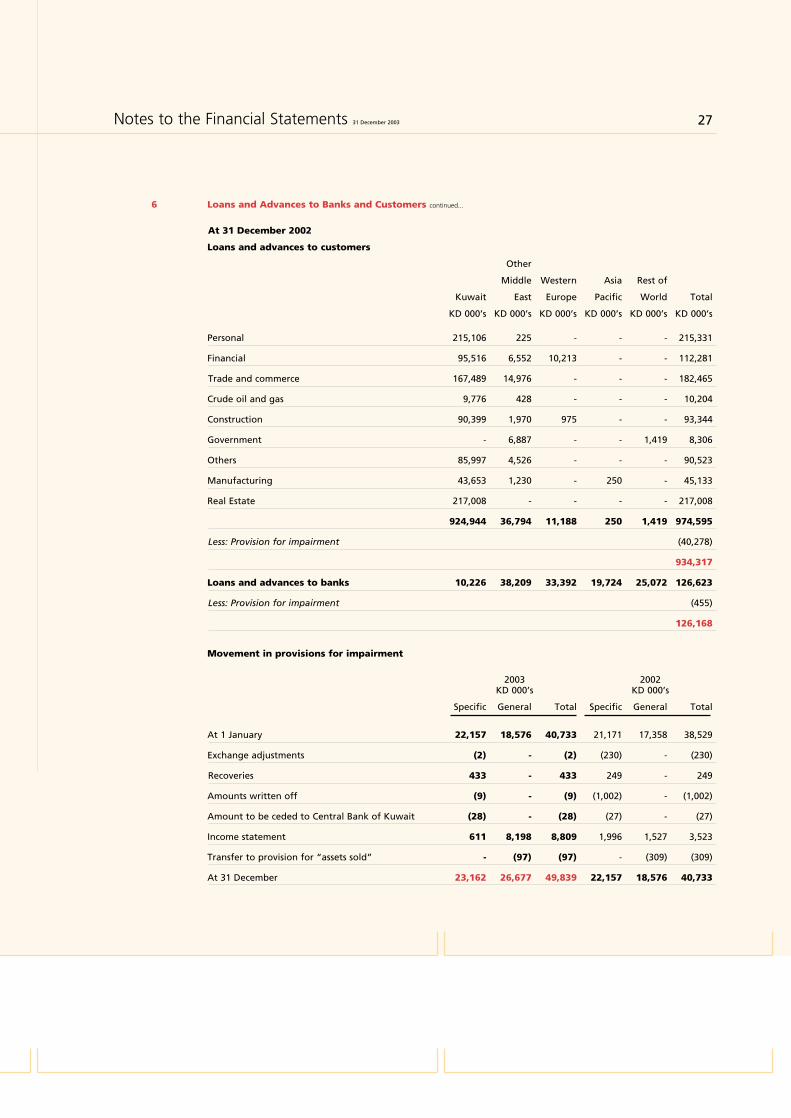

27Notes to the Financial Statements 31 December 2003

6 Loans and Advances to Banks and Customers continued...

At 31 December 2002

Loans and advances to customers

Other

Middle Western Asia Rest of

Kuwait East Europe Pacific World Total

KD 000’s KD 000’s KD 000’s KD 000’s KD 000’s KD 000’s

Personal 215,106 225 - - - 215,331

Financial 95,516 6,552 10,213 - - 112,281

Trade and commerce 167,489 14,976 - - - 182,465

Crude oil and gas 9,776 428 - - - 10,204

Construction 90,399 1,970 975 - - 93,344

Government - 6,887 - - 1,419 8,306

Others 85,997 4,526 - - - 90,523

Manufacturing 43,653 1,230 - 250 - 45,133

Real Estate 217,008 - - - - 217,008

924,944 36,794 11,188 250 1,419 974,595

Less: Provision for impairment (40,278)

934,317

Loans and advances to banks 10,226 38,209 33,392 19,724 25,072 126,623

Less: Provision for impairment (455)

126,168

Movement in provisions for impairment

2003 2002KD 000’s KD 000’s

Specific General Total Specific General Total

At 1 January 22,157 18,576 40,733 21,171 17,358 38,529

Exchange adjustments (2) - (2) (230) - (230)

Recoveries 433 - 433 249 - 249

Amounts written off (9) - (9) (1,002) - (1,002)

Amount to be ceded to Central Bank of Kuwait (28) - (28) (27) - (27)

Income statement 611 8,198 8,809 1,996 1,527 3,523

Transfer to provision for “assets sold” - (97) (97) - (309) (309)

At 31 December 23,162 26,677 49,839 22,157 18,576 40,733

28

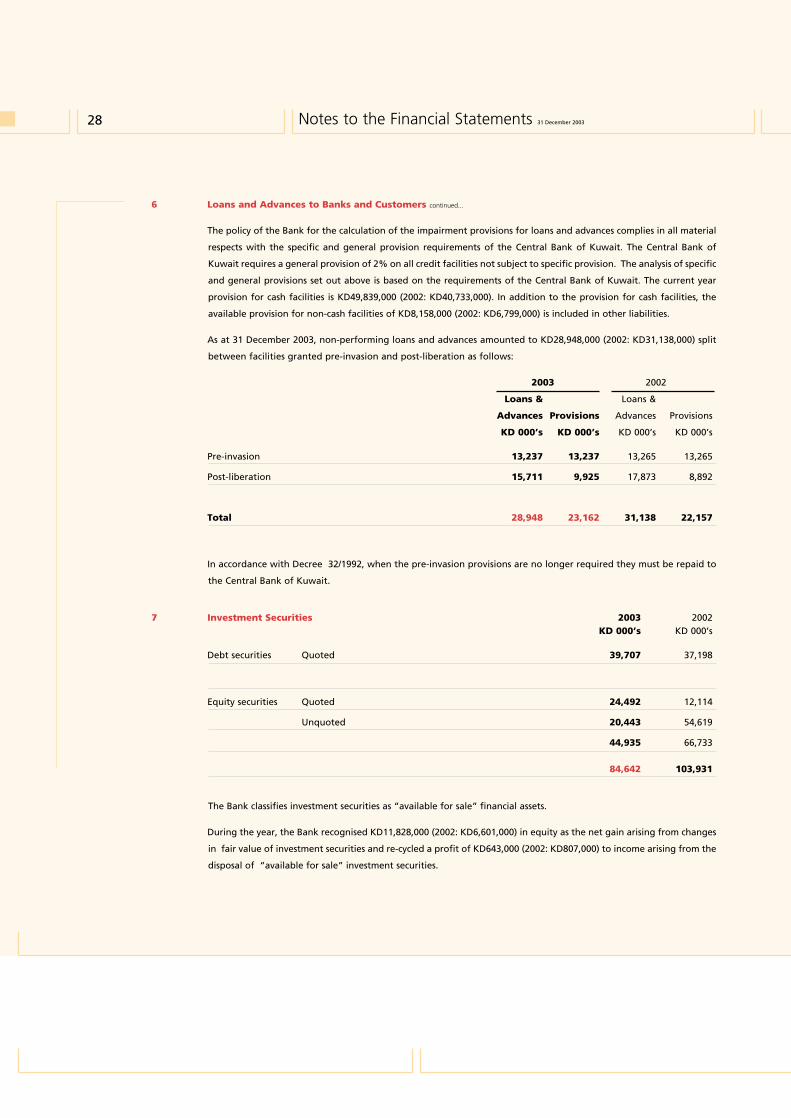

6 Loans and Advances to Banks and Customers continued...

The policy of the Bank for the calculation of the impairment provisions for loans and advances complies in all material

respects with the specific and general provision requirements of the Central Bank of Kuwait. The Central Bank of

Kuwait requires a general provision of 2% on all credit facilities not subject to specific provision. The analysis of specific

and general provisions set out above is based on the requirements of the Central Bank of Kuwait. The current year

provision for cash facilities is KD49,839,000 (2002: KD40,733,000). In addition to the provision for cash facilities, the

available provision for non-cash facilities of KD8,158,000 (2002: KD6,799,000) is included in other liabilities.

As at 31 December 2003, non-performing loans and advances amounted to KD28,948,000 (2002: KD31,138,000) split

between facilities granted pre-invasion and post-liberation as follows:

2003 2002

Loans & Loans &

Advances Provisions Advances Provisions

KD 000’s KD 000’s KD 000’s KD 000’s

Pre-invasion 13,237 13,237 13,265 13,265

Post-liberation 15,711 9,925 17,873 8,892

Total 28,948 23,162 31,138 22,157

In accordance with Decree 32/1992, when the pre-invasion provisions are no longer required they must be repaid to

the Central Bank of Kuwait.

Notes to the Financial Statements 31 December 2003

7 Investment Securities 2003 2002KD 000’s KD 000’s

Debt securities Quoted 39,707 37,198

Equity securities Quoted 24,492 12,114

Unquoted 20,443 54,619

44,935 66,733

84,642 103,931

The Bank classifies investment securities as “available for sale” financial assets.

During the year, the Bank recognised KD11,828,000 (2002: KD6,601,000) in equity as the net gain arising from changes

in fair value of investment securities and re-cycled a profit of KD643,000 (2002: KD807,000) to income arising from the

disposal of “available for sale” investment securities.

29Notes to the Financial Statements 31 December 2003

8 Government Debt Bonds

The Bank classifies government debt bonds as “originated financial assets”.

The Central Bank of Kuwait purchased resident Kuwaiti and GCC customers' debts existing at 1 August 1990, in addition

to related interest up to 31 December 1991, on behalf of the Government of Kuwait in accordance with Decree 32/1992

and Law 41/1993, as amended by Law 80/1995, in respect of the financial and banking sector. Pursuant to the

provisions of Law 41/1993, some amendments may be made to customers’ debt balances, which are being reviewed by

the Central Bank of Kuwait.

The purchase value of these debts was determined in accordance with the Decrees and was settled by the issue of

bonds, with a value date of 31 December 1991. The bonds mature over a maximum period of twenty years from the

value date. The Central Bank of Kuwait has redeemed KD15,841,000 during 2003 (2002: KD23,689,000). Interest on

the bonds is at a rate fixed semi-annually by the Central Bank of Kuwait and is payable semi-annually in arrears; the

average rate for 2003 was 1.89% (2002: 2.67%).

The Bank is required to manage the purchased debts without remuneration in conformity with the regulations as

promulgated by Decree 32/1992 in this respect.

9 Other Assets 2003 2002KD 000’s KD 000’s

Accrued interest receivable 9,661 7,067

Sundry debtors 3,188 4,414

12,849 11,481

The Bank classifies other assets as “originated financial assets”.

10 Due to Banks and Deposits from Financial Institutions 2003 2002KD 000’s KD 000’s

Due to banks

Current accounts and demand deposits 5,733 21,389

Certificates of deposit 393,500 30,000

Time deposits 159,390 194,229

558,623 245,618

Medium term loans 204,205 154,915

Deposits from financial institutions

Current accounts and demand deposits 17,333 32,407

Time deposits 85,614 126,788

102,947 159,195

30

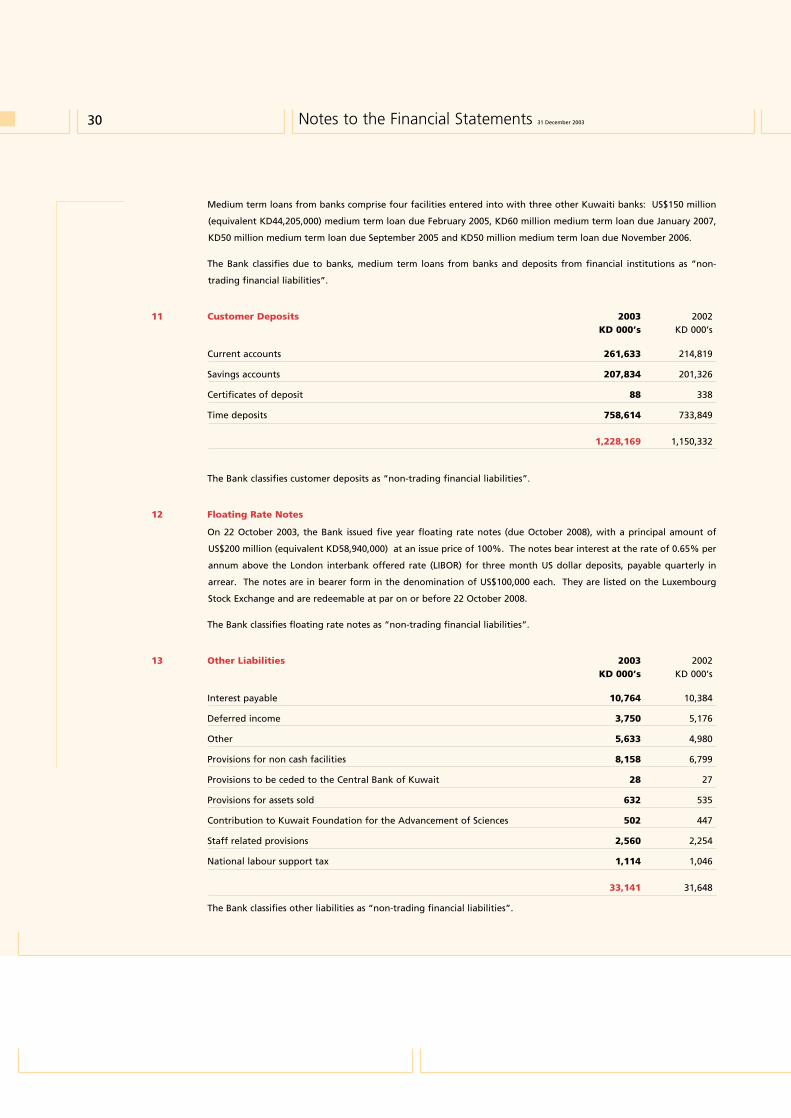

Medium term loans from banks comprise four facilities entered into with three other Kuwaiti banks: US$150 million

(equivalent KD44,205,000) medium term loan due February 2005, KD60 million medium term loan due January 2007,

KD50 million medium term loan due September 2005 and KD50 million medium term loan due November 2006.

The Bank classifies due to banks, medium term loans from banks and deposits from financial institutions as “non-

trading financial liabilities”.

11 Customer Deposits 2003 2002KD 000’s KD 000’s

Current accounts 261,633 214,819

Savings accounts 207,834 201,326

Certificates of deposit 88 338

Time deposits 758,614 733,849

1,228,169 1,150,332

The Bank classifies customer deposits as “non-trading financial liabilities”.

12 Floating Rate Notes

On 22 October 2003, the Bank issued five year floating rate notes (due October 2008), with a principal amount of

US$200 million (equivalent KD58,940,000) at an issue price of 100%. The notes bear interest at the rate of 0.65% per

annum above the London interbank offered rate (LIBOR) for three month US dollar deposits, payable quarterly in

arrear. The notes are in bearer form in the denomination of US$100,000 each. They are listed on the Luxembourg

Stock Exchange and are redeemable at par on or before 22 October 2008.

The Bank classifies floating rate notes as “non-trading financial liabilities”.

13 Other Liabilities 2003 2002KD 000’s KD 000’s

Interest payable 10,764 10,384

Deferred income 3,750 5,176

Other 5,633 4,980

Provisions for non cash facilities 8,158 6,799

Provisions to be ceded to the Central Bank of Kuwait 28 27

Provisions for assets sold 632 535

Contribution to Kuwait Foundation for the Advancement of Sciences 502 447

Staff related provisions 2,560 2,254

National labour support tax 1,114 1,046

33,141 31,648

The Bank classifies other liabilities as “non-trading financial liabilities”.

Notes to the Financial Statements 31 December 2003

31Notes to the Financial Statements 31 December 2003

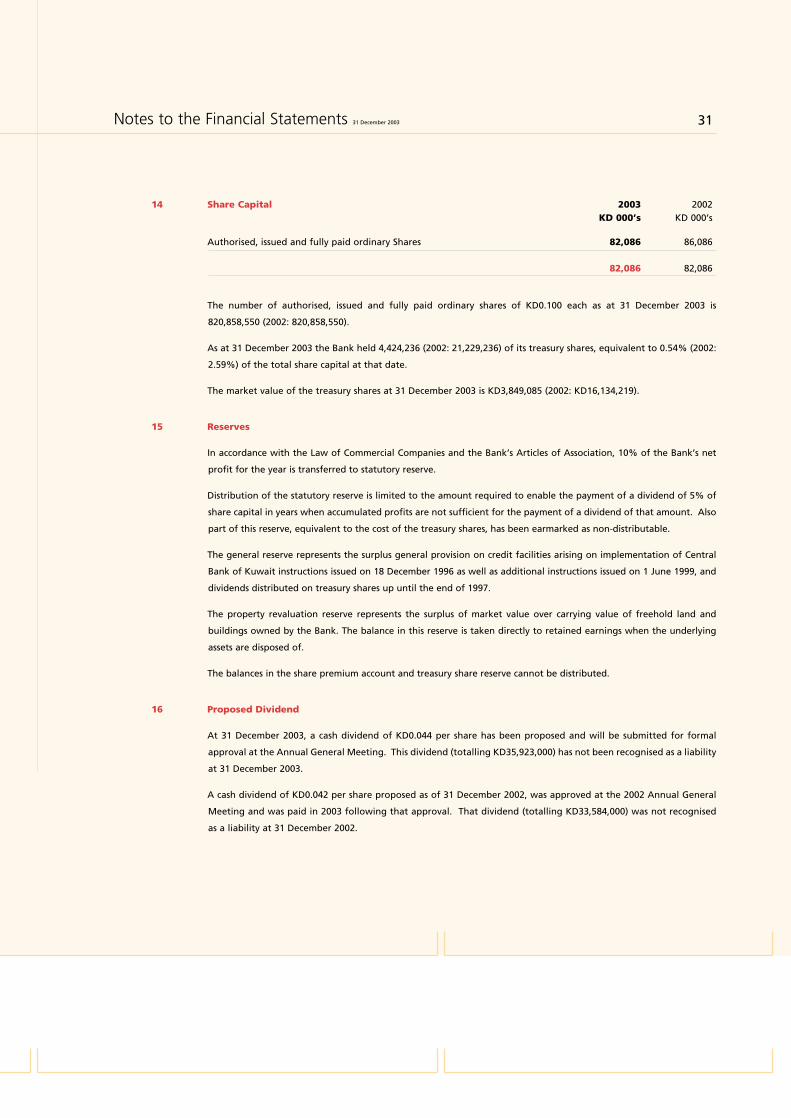

14 Share Capital 2003 2002KD 000’s KD 000’s

Authorised, issued and fully paid ordinary Shares 82,086 86,086

82,086 82,086

The number of authorised, issued and fully paid ordinary shares of KD0.100 each as at 31 December 2003 is

820,858,550 (2002: 820,858,550).

As at 31 December 2003 the Bank held 4,424,236 (2002: 21,229,236) of its treasury shares, equivalent to 0.54% (2002:

2.59%) of the total share capital at that date.

The market value of the treasury shares at 31 December 2003 is KD3,849,085 (2002: KD16,134,219).

15 Reserves

In accordance with the Law of Commercial Companies and the Bank’s Articles of Association, 10% of the Bank’s net

profit for the year is transferred to statutory reserve.

Distribution of the statutory reserve is limited to the amount required to enable the payment of a dividend of 5% of

share capital in years when accumulated profits are not sufficient for the payment of a dividend of that amount. Also

part of this reserve, equivalent to the cost of the treasury shares, has been earmarked as non-distributable.

The general reserve represents the surplus general provision on credit facilities arising on implementation of Central

Bank of Kuwait instructions issued on 18 December 1996 as well as additional instructions issued on 1 June 1999, and

dividends distributed on treasury shares up until the end of 1997.

The property revaluation reserve represents the surplus of market value over carrying value of freehold land and

buildings owned by the Bank. The balance in this reserve is taken directly to retained earnings when the underlying

assets are disposed of.

The balances in the share premium account and treasury share reserve cannot be distributed.

16 Proposed Dividend

At 31 December 2003, a cash dividend of KD0.044 per share has been proposed and will be submitted for formal

approval at the Annual General Meeting. This dividend (totalling KD35,923,000) has not been recognised as a liability

at 31 December 2003.

A cash dividend of KD0.042 per share proposed as of 31 December 2002, was approved at the 2002 Annual General

Meeting and was paid in 2003 following that approval. That dividend (totalling KD33,584,000) was not recognised

as a liability at 31 December 2002.

32

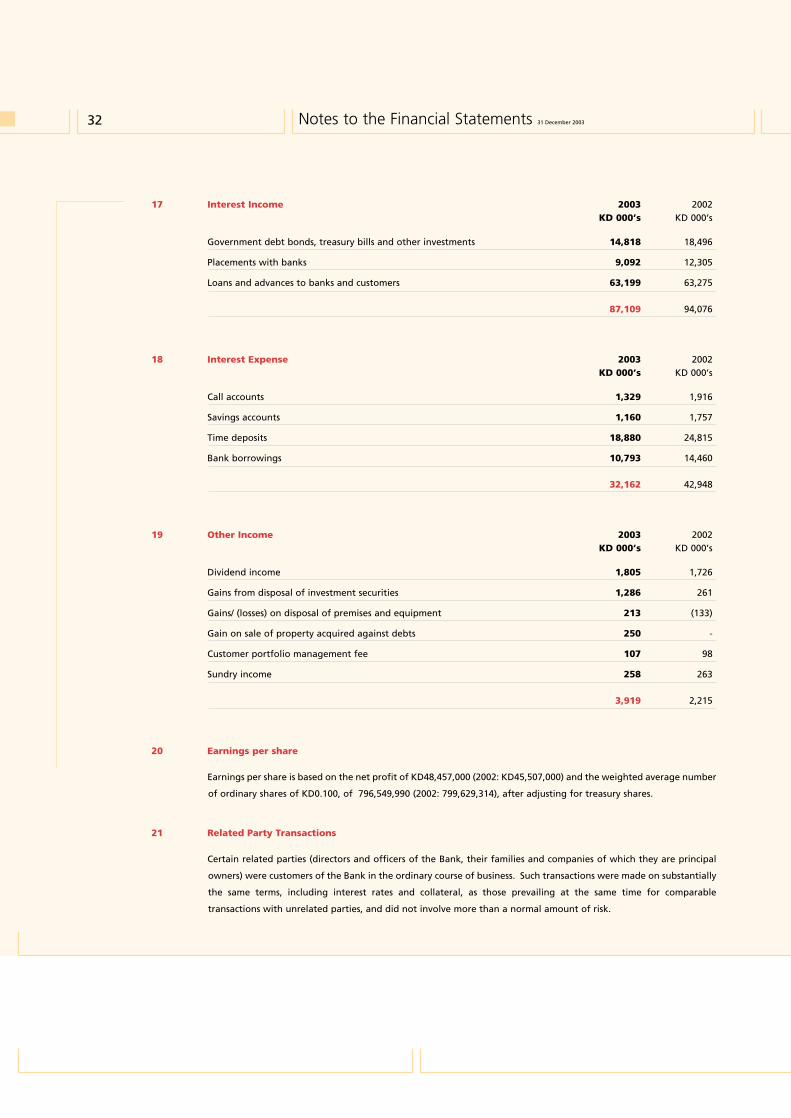

17 Interest Income 2003 2002KD 000’s KD 000’s

Government debt bonds, treasury bills and other investments 14,818 18,496

Placements with banks 9,092 12,305

Loans and advances to banks and customers 63,199 63,275

87,109 94,076

18 Interest Expense 2003 2002KD 000’s KD 000’s

Call accounts 1,329 1,916

Savings accounts 1,160 1,757

Time deposits 18,880 24,815

Bank borrowings 10,793 14,460

32,162 42,948

19 Other Income 2003 2002KD 000’s KD 000’s

Dividend income 1,805 1,726

Gains from disposal of investment securities 1,286 261

Gains/ (losses) on disposal of premises and equipment 213 (133)

Gain on sale of property acquired against debts 250 -

Customer portfolio management fee 107 98

Sundry income 258 263

3,919 2,215

20 Earnings per share

Earnings per share is based on the net profit of KD48,457,000 (2002: KD45,507,000) and the weighted average number

of ordinary shares of KD0.100, of 796,549,990 (2002: 799,629,314), after adjusting for treasury shares.

21 Related Party Transactions

Certain related parties (directors and officers of the Bank, their families and companies of which they are principal

owners) were customers of the Bank in the ordinary course of business. Such transactions were made on substantially

the same terms, including interest rates and collateral, as those prevailing at the same time for comparable

transactions with unrelated parties, and did not involve more than a normal amount of risk.

Notes to the Financial Statements 31 December 2003

33Notes to the Financial Statements 31 December 2003

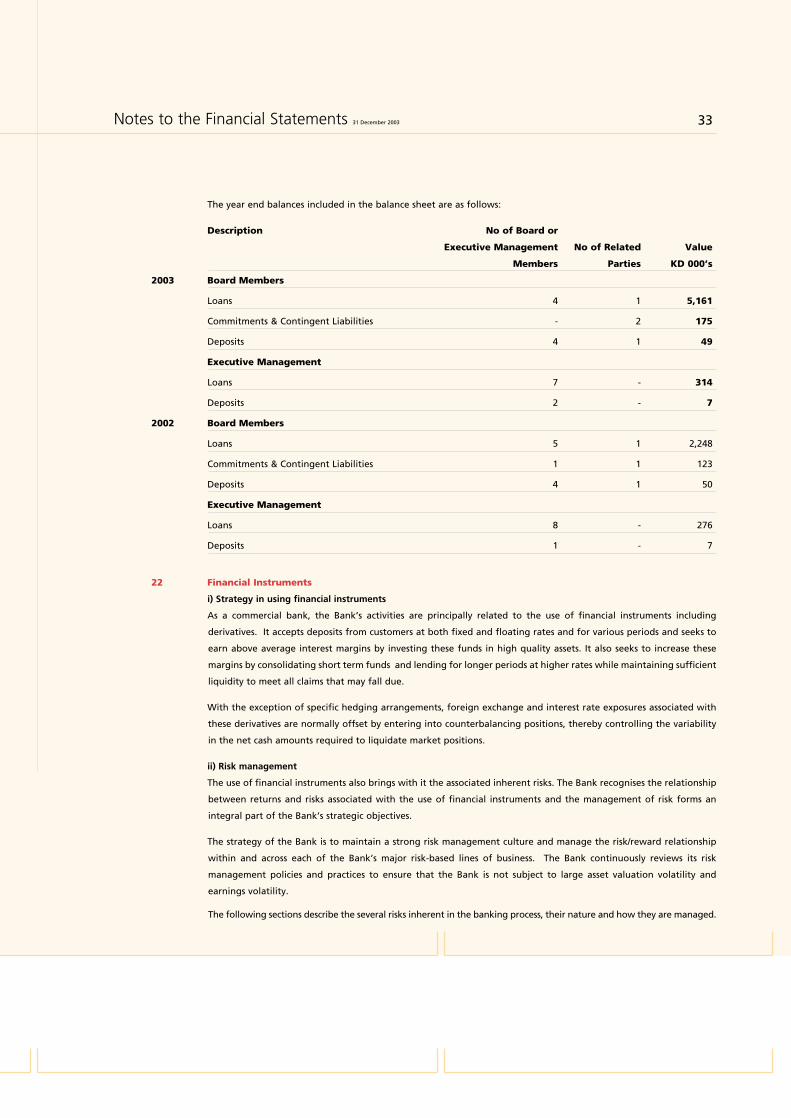

The year end balances included in the balance sheet are as follows:

Description No of Board or

Executive Management No of Related Value

Members Parties KD 000’s

2003 Board Members

Loans 4 1 5,161

Commitments & Contingent Liabilities - 2 175

Deposits 4 1 49

Executive Management

Loans 7 - 314

Deposits 2 - 7

2002 Board Members

Loans 5 1 2,248

Commitments & Contingent Liabilities 1 1 123

Deposits 4 1 50

Executive Management

Loans 8 - 276

Deposits 1 - 7

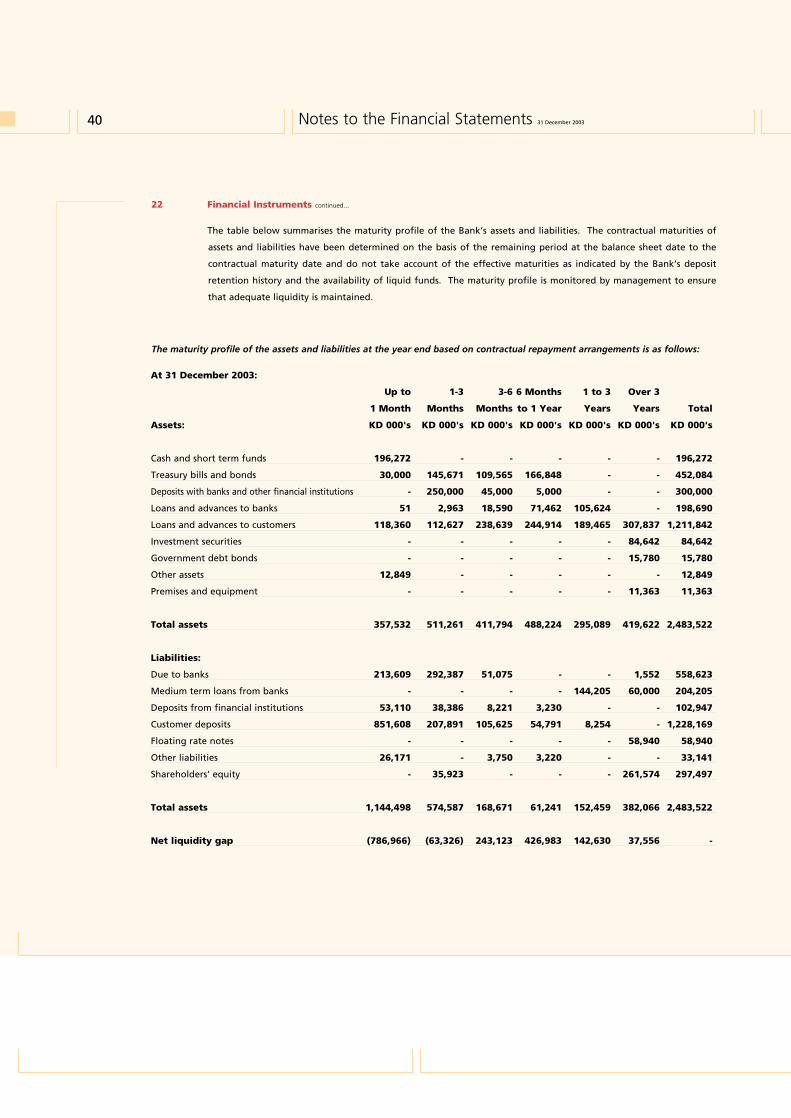

22 Financial Instruments

i) Strategy in using financial instruments

As a commercial bank, the Bank’s activities are principally related to the use of financial instruments including

derivatives. It accepts deposits from customers at both fixed and floating rates and for various periods and seeks to

earn above average interest margins by investing these funds in high quality assets. It also seeks to increase these

margins by consolidating short term funds and lending for longer periods at higher rates while maintaining sufficient

liquidity to meet all claims that may fall due.

With the exception of specific hedging arrangements, foreign exchange and interest rate exposures associated with

these derivatives are normally offset by entering into counterbalancing positions, thereby controlling the variability

in the net cash amounts required to liquidate market positions.

ii) Risk management

The use of financial instruments also brings with it the associated inherent risks. The Bank recognises the relationship

between returns and risks associated with the use of financial instruments and the management of risk forms an

integral part of the Bank’s strategic objectives.

The strategy of the Bank is to maintain a strong risk management culture and manage the risk/reward relationship

within and across each of the Bank’s major risk-based lines of business. The Bank continuously reviews its risk

management policies and practices to ensure that the Bank is not subject to large asset valuation volatility and

earnings volatility.

The following sections describe the several risks inherent in the banking process, their nature and how they are managed.

34 Notes to the Financial Statements 31 December 2003

A) Credit Risk

Credit risk is the risk that one party to a financial instrument will fail to discharge an obligation and cause the other

party to incur a financial loss. The Bank attempts to control credit risk by monitoring credit exposures, limiting

transactions with specific counterparties, and continually assessing the creditworthiness of counterparties. In addition

to monitoring credit limits, the Bank manages the credit exposure relating to its trading activities by entering into

master netting agreements and collateral arrangements with counterparties in appropriate circumstances, and

limiting the duration of exposure. In certain cases, the Bank may also close out transactions or assign them to other

counterparties to mitigate credit risk.

Concentrations of credit risk arise when a number of counterparties are engaged in similar business activities, or

activities in the same geographic region, or have similar economic features that would cause their ability to meet

contractual obligations to be similarly affected by changes in economic, political or other conditions. Concentrations

of credit risk indicate the relative sensitivity of the Bank’s performance to developments affecting a particular industry

or geographic location.

The Bank seeks to manage its credit risk exposure through diversification of lending activities to avoid undue

concentrations of risks with individuals or groups of customers in specific locations or business. It also obtains security

when appropriate.

Concentration of assets, liabilities and off-balance-sheet items

a. Credit risk concentration

The credit risk concentration within loans and advances, which form the significant portion of assets subject to credit

risk, is given in Note 6.

35Notes to the Financial Statements 31 December 2003

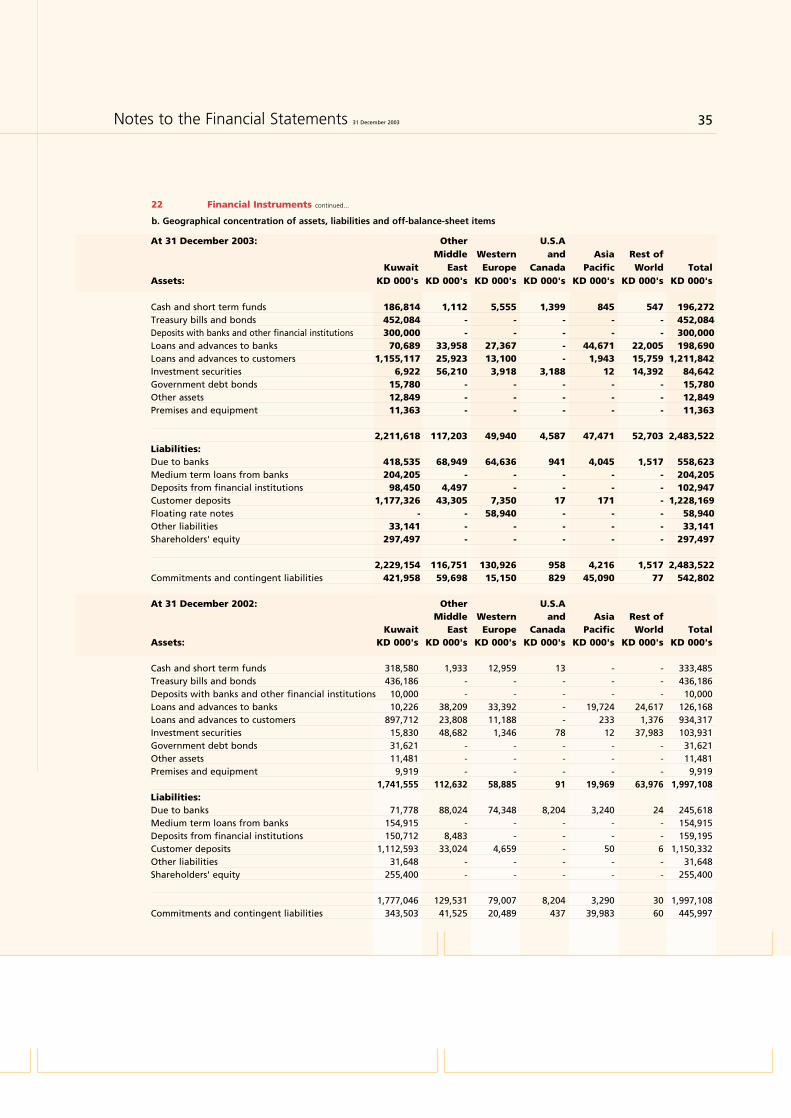

22 Financial Instruments continued...

b. Geographical concentration of assets, liabilities and off-balance-sheet items

At 31 December 2003: Other U.S.A Middle Western and Asia Rest of

Kuwait East Europe Canada Pacific World TotalAssets: KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's

Cash and short term funds 186,814 1,112 5,555 1,399 845 547 196,272Treasury bills and bonds 452,084 - - - - - 452,084Deposits with banks and other financial institutions 300,000 - - - - - 300,000Loans and advances to banks 70,689 33,958 27,367 - 44,671 22,005 198,690Loans and advances to customers 1,155,117 25,923 13,100 - 1,943 15,759 1,211,842Investment securities 6,922 56,210 3,918 3,188 12 14,392 84,642Government debt bonds 15,780 - - - - - 15,780Other assets 12,849 - - - - - 12,849Premises and equipment 11,363 - - - - - 11,363

2,211,618 117,203 49,940 4,587 47,471 52,703 2,483,522Liabilities:Due to banks 418,535 68,949 64,636 941 4,045 1,517 558,623Medium term loans from banks 204,205 - - - - - 204,205Deposits from financial institutions 98,450 4,497 - - - - 102,947Customer deposits 1,177,326 43,305 7,350 17 171 - 1,228,169Floating rate notes - - 58,940 - - - 58,940Other liabilities 33,141 - - - - - 33,141Shareholders' equity 297,497 - - - - - 297,497

2,229,154 116,751 130,926 958 4,216 1,517 2,483,522Commitments and contingent liabilities 421,958 59,698 15,150 829 45,090 77 542,802

At 31 December 2002: Other U.S.A Middle Western and Asia Rest of

Kuwait East Europe Canada Pacific World TotalAssets: KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's

Cash and short term funds 318,580 1,933 12,959 13 - - 333,485Treasury bills and bonds 436,186 - - - - - 436,186Deposits with banks and other financial institutions 10,000 - - - - - 10,000Loans and advances to banks 10,226 38,209 33,392 - 19,724 24,617 126,168Loans and advances to customers 897,712 23,808 11,188 - 233 1,376 934,317Investment securities 15,830 48,682 1,346 78 12 37,983 103,931Government debt bonds 31,621 - - - - - 31,621Other assets 11,481 - - - - - 11,481Premises and equipment 9,919 - - - - - 9,919

1,741,555 112,632 58,885 91 19,969 63,976 1,997,108Liabilities:Due to banks 71,778 88,024 74,348 8,204 3,240 24 245,618Medium term loans from banks 154,915 - - - - - 154,915Deposits from financial institutions 150,712 8,483 - - - - 159,195Customer deposits 1,112,593 33,024 4,659 - 50 6 1,150,332Other liabilities 31,648 - - - - - 31,648Shareholders' equity 255,400 - - - - - 255,400

1,777,046 129,531 79,007 8,204 3,290 30 1,997,108Commitments and contingent liabilities 343,503 41,525 20,489 437 39,983 60 445,997

36 Notes to the Financial Statements 31 December 2003

22 Financial Instruments continued...

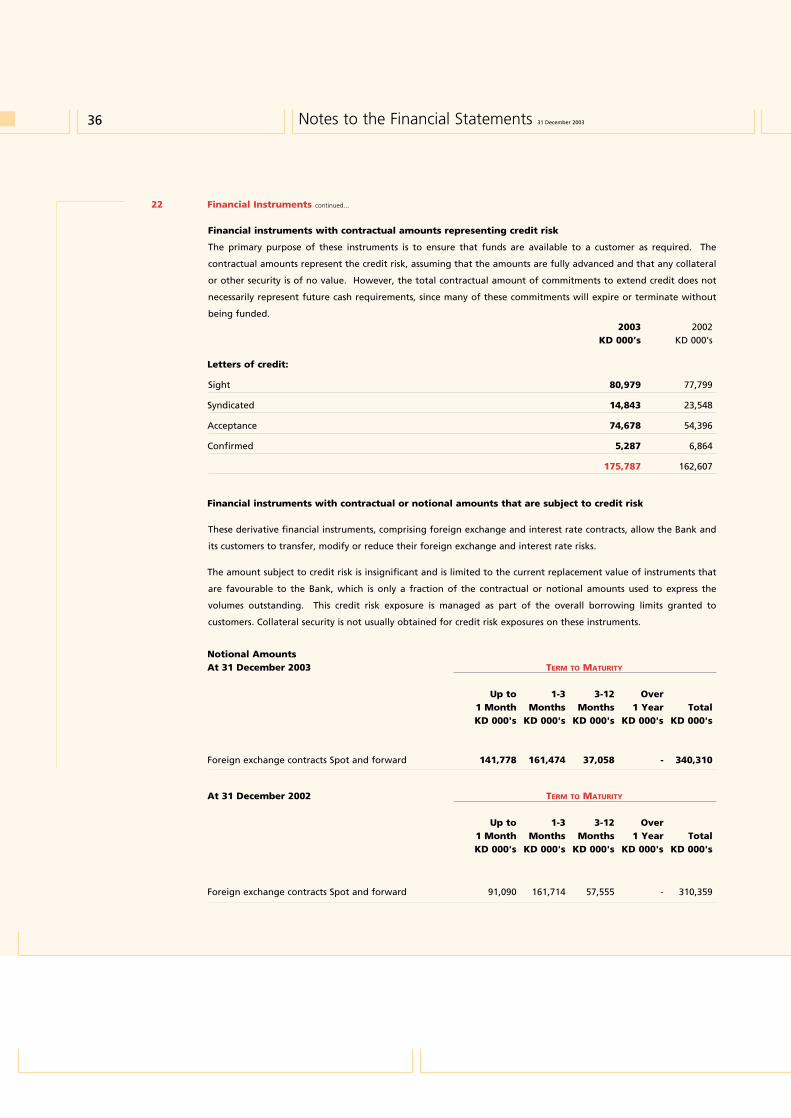

Financial instruments with contractual amounts representing credit risk

The primary purpose of these instruments is to ensure that funds are available to a customer as required. The

contractual amounts represent the credit risk, assuming that the amounts are fully advanced and that any collateral

or other security is of no value. However, the total contractual amount of commitments to extend credit does not

necessarily represent future cash requirements, since many of these commitments will expire or terminate without

being funded.2003 2002

KD 000’s KD 000’s

Letters of credit:

Sight 80,979 77,799

Syndicated 14,843 23,548

Acceptance 74,678 54,396

Confirmed 5,287 6,864

175,787 162,607

Financial instruments with contractual or notional amounts that are subject to credit risk

These derivative financial instruments, comprising foreign exchange and interest rate contracts, allow the Bank and

its customers to transfer, modify or reduce their foreign exchange and interest rate risks.

The amount subject to credit risk is insignificant and is limited to the current replacement value of instruments that

are favourable to the Bank, which is only a fraction of the contractual or notional amounts used to express the

volumes outstanding. This credit risk exposure is managed as part of the overall borrowing limits granted to

customers. Collateral security is not usually obtained for credit risk exposures on these instruments.

Notional AmountsAt 31 December 2003 TERM TO MATURITY

Up to 1-3 3-12 Over1 Month Months Months 1 Year TotalKD 000's KD 000's KD 000's KD 000's KD 000's

Foreign exchange contracts Spot and forward 141,778 161,474 37,058 - 340,310

At 31 December 2002 TERM TO MATURITY

Up to 1-3 3-12 Over1 Month Months Months 1 Year TotalKD 000's KD 000's KD 000's KD 000's KD 000's

Foreign exchange contracts Spot and forward 91,090 161,714 57,555 - 310,359

37

22 Financial Instruments continued...

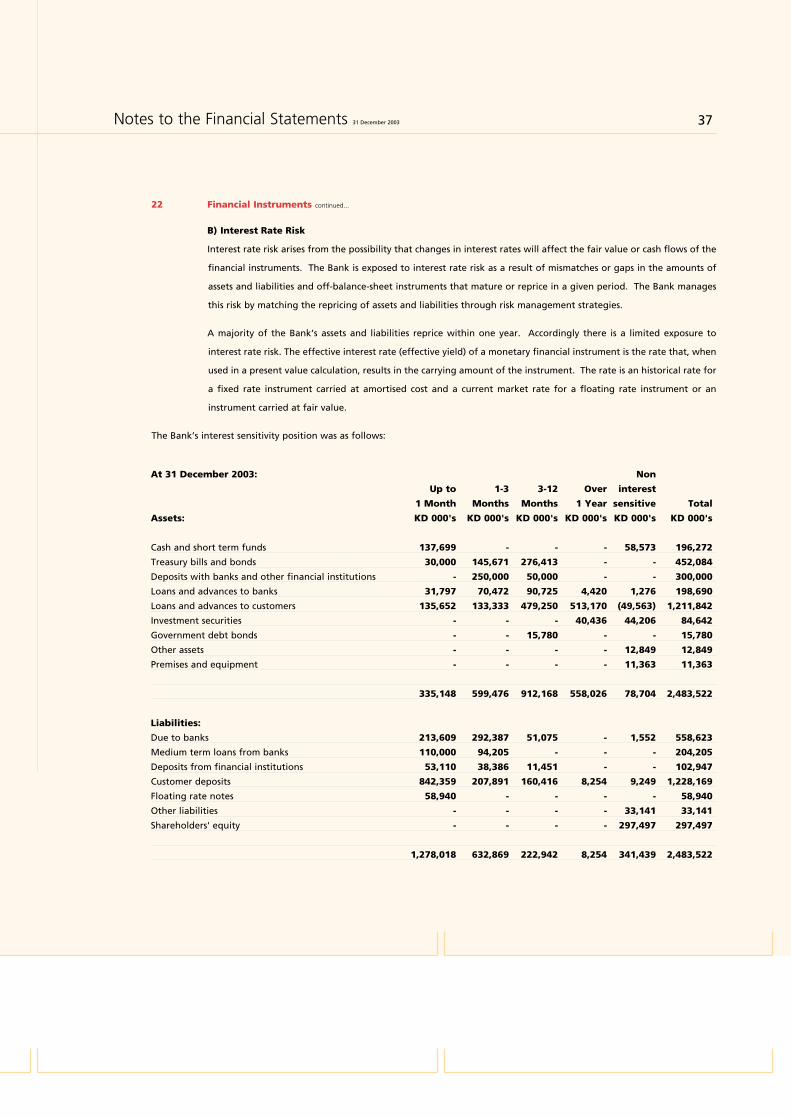

B) Interest Rate Risk

Interest rate risk arises from the possibility that changes in interest rates will affect the fair value or cash flows of the

financial instruments. The Bank is exposed to interest rate risk as a result of mismatches or gaps in the amounts of

assets and liabilities and off-balance-sheet instruments that mature or reprice in a given period. The Bank manages

this risk by matching the repricing of assets and liabilities through risk management strategies.

A majority of the Bank’s assets and liabilities reprice within one year. Accordingly there is a limited exposure to

interest rate risk. The effective interest rate (effective yield) of a monetary financial instrument is the rate that, when

used in a present value calculation, results in the carrying amount of the instrument. The rate is an historical rate for

a fixed rate instrument carried at amortised cost and a current market rate for a floating rate instrument or an

instrument carried at fair value.

The Bank’s interest sensitivity position was as follows:

At 31 December 2003: Non

Up to 1-3 3-12 Over interest

1 Month Months Months 1 Year sensitive Total

Assets: KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's

Cash and short term funds 137,699 - - - 58,573 196,272

Treasury bills and bonds 30,000 145,671 276,413 - - 452,084

Deposits with banks and other financial institutions - 250,000 50,000 - - 300,000

Loans and advances to banks 31,797 70,472 90,725 4,420 1,276 198,690

Loans and advances to customers 135,652 133,333 479,250 513,170 (49,563) 1,211,842

Investment securities - - - 40,436 44,206 84,642

Government debt bonds - - 15,780 - - 15,780

Other assets - - - - 12,849 12,849

Premises and equipment - - - - 11,363 11,363

335,148 599,476 912,168 558,026 78,704 2,483,522

Liabilities:

Due to banks 213,609 292,387 51,075 - 1,552 558,623

Medium term loans from banks 110,000 94,205 - - - 204,205

Deposits from financial institutions 53,110 38,386 11,451 - - 102,947

Customer deposits 842,359 207,891 160,416 8,254 9,249 1,228,169

Floating rate notes 58,940 - - - - 58,940

Other liabilities - - - - 33,141 33,141

Shareholders' equity - - - - 297,497 297,497

1,278,018 632,869 222,942 8,254 341,439 2,483,522

Notes to the Financial Statements 31 December 2003

38 Notes to the Financial Statements 31 December 2003

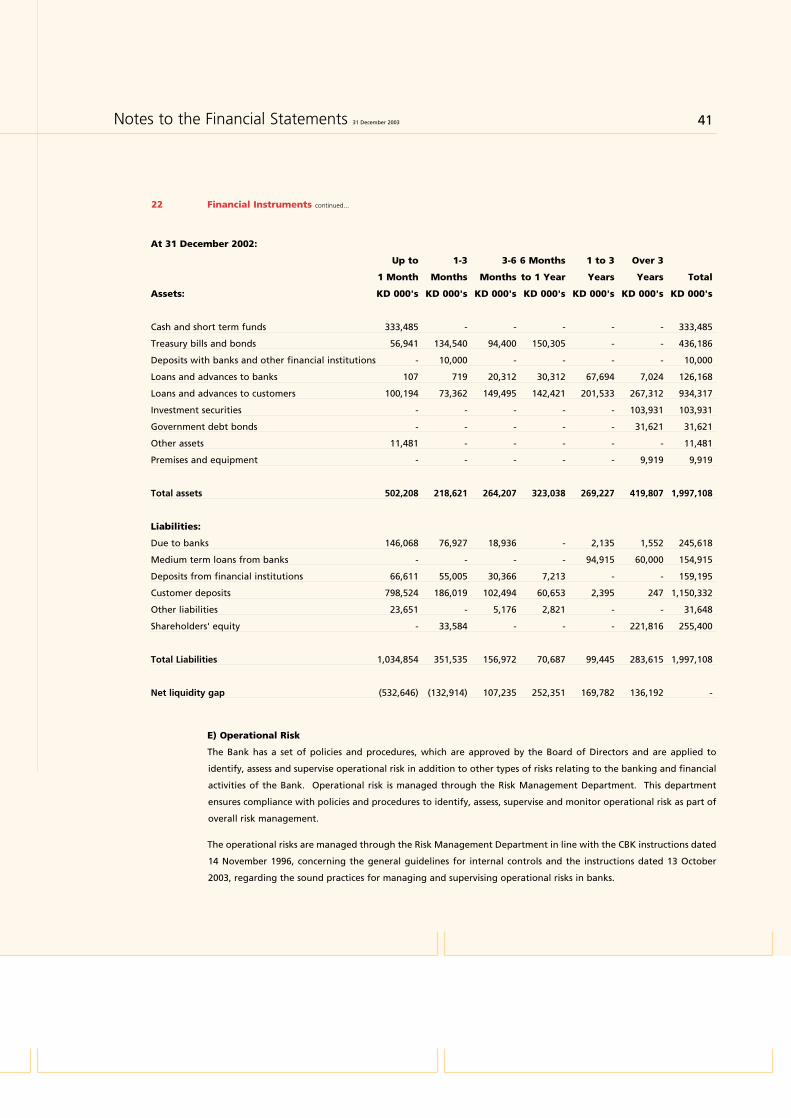

22 Financial Instruments continued...

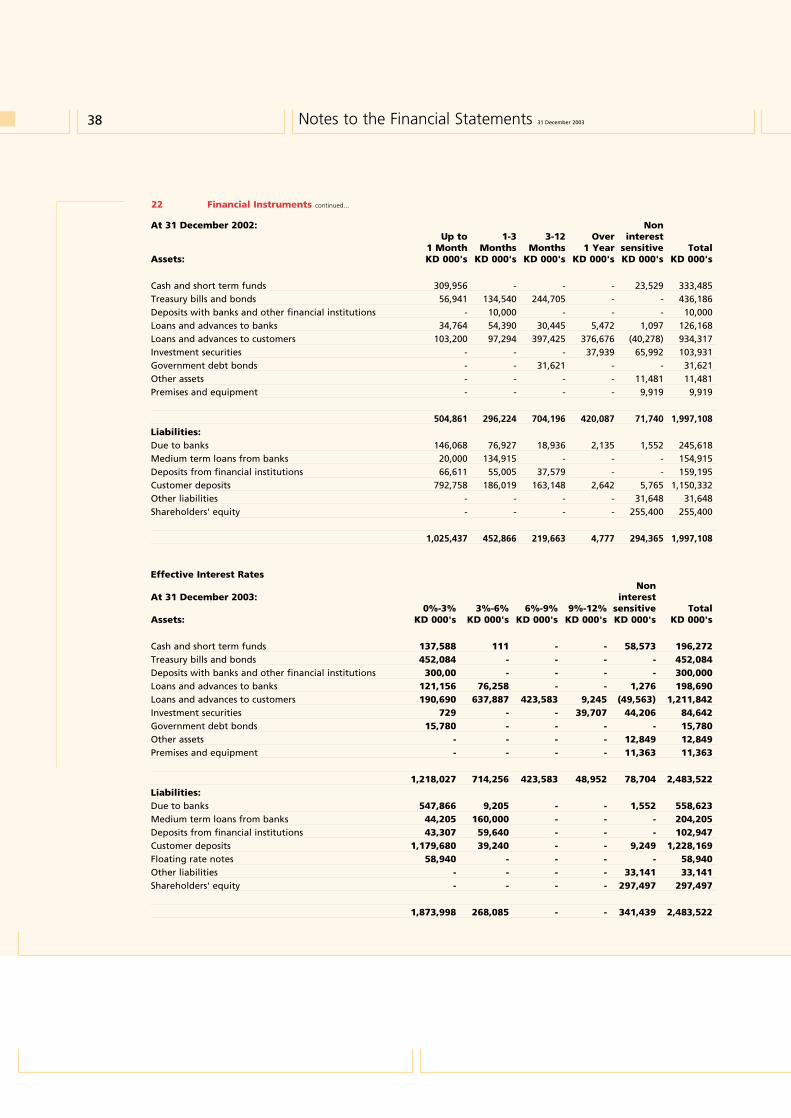

At 31 December 2002: NonUp to 1-3 3-12 Over interest

1 Month Months Months 1 Year sensitive TotalAssets: KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's

Cash and short term funds 309,956 - - - 23,529 333,485Treasury bills and bonds 56,941 134,540 244,705 - - 436,186Deposits with banks and other financial institutions - 10,000 - - - 10,000Loans and advances to banks 34,764 54,390 30,445 5,472 1,097 126,168Loans and advances to customers 103,200 97,294 397,425 376,676 (40,278) 934,317Investment securities - - - 37,939 65,992 103,931Government debt bonds - - 31,621 - - 31,621Other assets - - - - 11,481 11,481Premises and equipment - - - - 9,919 9,919

504,861 296,224 704,196 420,087 71,740 1,997,108Liabilities:Due to banks 146,068 76,927 18,936 2,135 1,552 245,618Medium term loans from banks 20,000 134,915 - - - 154,915Deposits from financial institutions 66,611 55,005 37,579 - - 159,195Customer deposits 792,758 186,019 163,148 2,642 5,765 1,150,332Other liabilities - - - - 31,648 31,648Shareholders' equity - - - - 255,400 255,400

1,025,437 452,866 219,663 4,777 294,365 1,997,108

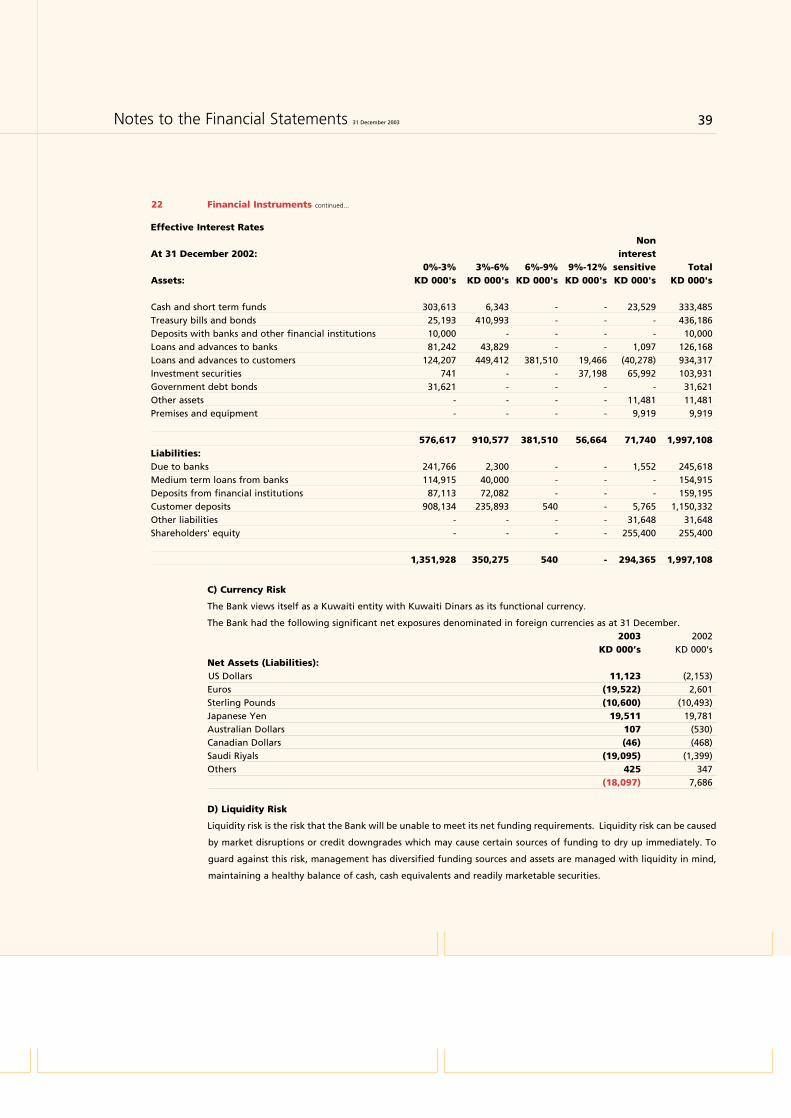

Effective Interest RatesNon

At 31 December 2003: interest0%-3% 3%-6% 6%-9% 9%-12% sensitive Total

Assets: KD 000's KD 000's KD 000's KD 000's KD 000's KD 000's

Cash and short term funds 137,588 111 - - 58,573 196,272Treasury bills and bonds 452,084 - - - - 452,084Deposits with banks and other financial institutions 300,00 - - - - 300,000Loans and advances to banks 121,156 76,258 - - 1,276 198,690Loans and advances to customers 190,690 637,887 423,583 9,245 (49,563) 1,211,842Investment securities 729 - - 39,707 44,206 84,642Government debt bonds 15,780 - - - - 15,780Other assets - - - - 12,849 12,849Premises and equipment - - - - 11,363 11,363